Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

- Bjorn’s Corner: New engine development. Part 3. Propulsive efficiency April 12, 2024

- A350-1000 or 777-9? Part 2 April 11, 2024

- Pontifications: Boeing “transparency”–not so much. April 9, 2024

- Airbus charges and write-offs since 1999: more than €33bn April 8, 2024

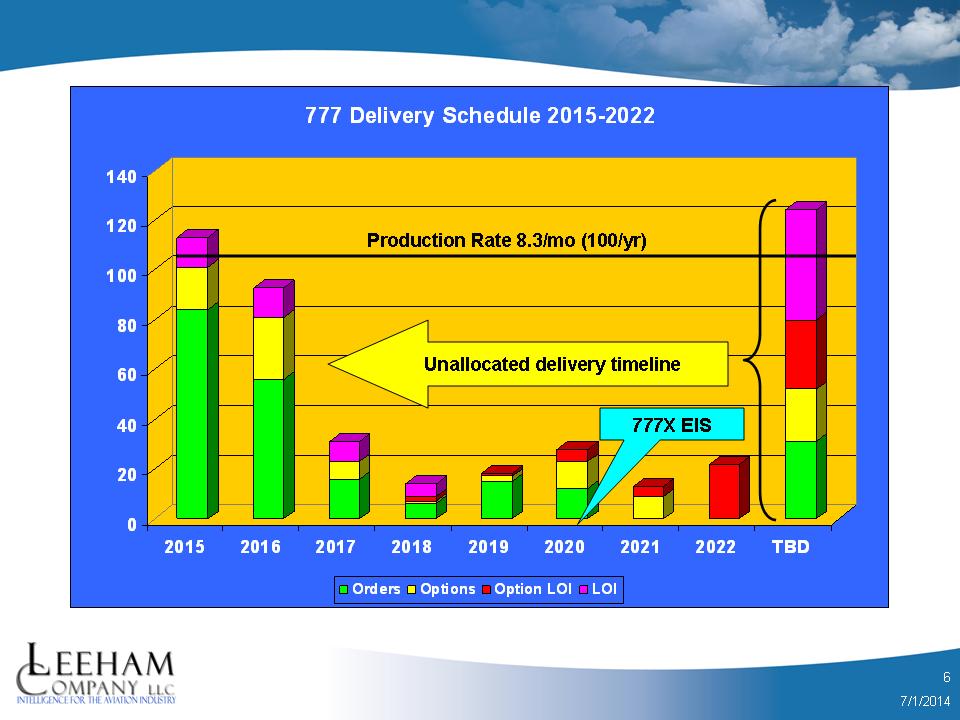

Boeing’s production gap challenge for the 777 Classic

Wall Street aerospace analysts are becoming increasingly concerned that Boeing will fall short of its goal to maintain 777 production rates at the current 8.3/mo through the introduction of the 777X, planned for entry-into-service in 2020.

One analyst predicts a rate reduction from 8.3/mo to seven and then to five as 2020 gets closer. Others are beginning to hint that they won’t be far behind in lowering expectations. But don’t tell this to Randy Tinseth, VP Marketing for Boeing.

“We have things in the pipeline and we’re working on those,” he told us July 1. “We’re confident the sales will come home and we’re confident we’ll bridge the gap.”

Boeing’s firm order backlog of nearly 300 777 Classics (our term—Tinseth objects to its use) shows shortfalls in scheduled deliveries-to-production of 100 airplanes a year. But Boeing CEO Jim McNerney said on an earnings call that including expected conversions of options and letters of intent, plus those sales campaigns Tinseth says are in the pipeline, Boeing will be able to maintain production.

Boeing has a major challenge ahead to fill the production gap for the 777 Classic to the EIS of the 777X.

Boeing also has about 120 firm orders, options, letters of intents and LOIs for Options for which delivery timelines haven’t been allocated in the Ascend data base.

“We’re confident we’re going to fill the back half of 2016,” Tinseth says. “We’re adding to the customer base. There’s no question it will be a challenge- we have three years of production [to fill] and we have six years to do it.”

The data in the Chart clearly illustrates the challenge Boeing has. Tinseth says Boeing “needs to sell 40-50 airplanes a year to make that happen,” but the gap appears larger than this, and it assumes 100% conversion of the Options and LOIs.

If the 124 TBD airplanes were allocated for delivery over the 2015-2020 period evenly (with 2015 getting only seven to top off), our math shows Boeing needs to 40-57 airplanes a year to maintain the current production rate. But this assumes everything goes right: 100% conversions, no global events to suppress sales, etc.

Boeing plans to bundle 777 Classic orders with 777Xs, but the sole example this year so far–All Nippon Airways–produced a sale of just six Classics. Boeing has booked only seven Classics YTD and announced sales of a total of 10.

Tinseth said Boeing believes the long-suffering cargo market will make a comeback in 2016/17, supporting 777F and 747-8F sales.

“Both 777F and 748F both are important,” he says. “There is a broad customer base for the freight market. Traffic in that market has been a challenge, but there has been strong growth rate over the past four months. We think there will be a supply-demand balance 2016/17.” He says that Boeing expects to produce two-three freighters a month split between both airplanes. But, he adds, the cargo “market has to deliver, no question.”

Freighters face a dilemma: there are virtually hundreds of B747-400 awaiting conversion, or being already converted and unterutilized. A strong demand of new build freighters may be caused by raising fuel prices (a B777F burns 15-20% less fuel per unit of cargo), but raising fuel prices will damp economic growth and air cargo growth in general.

Overall, I see potential for some freighters (also as MD11 replacement), but no prospects for the B747-8F.

Maybe Boeing can sell some as tankers?

Any ideas where these sales would come from?

I can see some of the US legacy carriers (Delta / United) tipping in for a dozen here or there ….. or maybe some of the package carriers would find the business case for discounted 777’s sound for replacing some of their older aeroplanes early.

Maybe Boeing could build white tail 777F’s to help fill the gap (which probably wouldn’t be a bad idea).

Other than that I can only see top up orders for existing carriers waiting for the 777X or A350-1000 to enter into their fleets.

Considering we don’t know who has signed the LOI’s, we could already be double counting.

Ascend does list the customers of everything but the “Unannounced.”

Any ideas where these sales would come from ?

From this end has been widely promoted and described/identified how in the short term one of either A or B could bring (and keep !) alive their respective (777 vs A330) WB FAL, by creating a bi-valved dual-bwb (for ‘blended wide-body’ AND ‘best wing-box’) Ultra-freighter (UF), capable of AGA (loaded transversally) … we evaluate the market out there to apprx. 300 such contraptions if 350 metric tonnes payload (26 AGA) can be carried over 6,200 nm … the message hasn’t got across, too bad … 300 UF = 600-equivalent WB (777 or A330) fuselages sold for 2.8 times the unit market price of the resp. WB, wherefore the UF as a strategy is value-incrementing.

There’s not going to be a jumbo tanker program that could plausibly solve the 748 program in time. Anything USAF above 767 will be either 777 or A330. (Hint, it will probably start with a 7 and end with a 7 no matter what). There’s really not much of a need for two types nowadays though.

Does anyone really see a new major procurement being completed during the present administration/budget situation?

If the analysts are having such concerns about the 777, what does that say for the A330 situation? They see no problem? Or its even worse there? Not that we want to divert the attention to Airbus here!

I have a suspicion the purpose designed air freighter will not recover the way it has in the past. Too many economic disruptions have hurt the market and it seems that an increading amount of freight is being packed in passenger aircraft.

Scott did that exercise for the A330 as well:

https://leehamnews.com/2014/03/27/filling-the-production-gap-for-a330-and-777-classic-huge-challenge-ahead/

He sees a similar challenge from 2016 onwards – in order to make the same assessment as he did for the 777 above, though, we’d need an EIS for the A330neo so Scott can do the maths based on proposed production rates and A330ceo orders up to A330neo EIS.

As the head of conversions at Airbus stated a while ago – you’d be foolish to pretend that the belly space in all those A330s and 777s isn’t having a *significant* impact on the market for dedicated freighters (new-built and converted).

So I would agree that it’s not likely we’re going to see the dedicated freighter bounce back to previous levels of popularity. There’s very little growth in the freight market as it is, and ever more belly capacity on pax aircraft is becoming available.

“Not that we want to divert the attention to Airbus here!”

An A330 production analysis is available here:

https://leehamnews.com/2014/03/27/filling-the-production-gap-for-a330-and-777-classic-huge-challenge-ahead/

Next time do a little bit research before making such statement 😉

My point was about the fact that the analysts haven’t said anything about the issue concerning the A330. They seem to have focused on the 777.

So my questions related to how the analysts see the situation at Airbus.

I had already read Scott’s article back when he originally posted it.

Unfortunately we don’t see what the European analysts write; they probably have discussed the A330 situation.

A330 NEO keeps its existing wing, and management is hostile to a large updating.

Anyway AIRBUS Policy is to constantly update its machines very different at Seattle! , (spending on 330 was said to be around 100mn€/year) so there is not much dead wood to remove from this frame.

So NEO EIS will probably require much less time than 777

Problem should be more manageable.

Leahy managed a similar problem very well for the 320 NEO.

It does not mean that there is no problem.

BUZZ has been going for quite some time of a large chinese order for regional 330

that could bridge most of the gap.

We should know more before the end of the year, maybe even at Farnborough????

Well, it’s not getting new wings, and it’s “only” getting modified versions of an existing engine variant. That should save a lot of time.

Rumoured EIS is around 2017/18. Probably 2018, I’d say.

Airbus see a problem or they wouldn’t bother to NEO with a RR TRENT derivative in 2017-2018, the would wait for the next generation Advance or GTF in 2020+. If they go ahead with a TRENT 1000-TEN NEO its because they can’t fill the gap and need to do something.

“Airbus see a problem or they wouldn’t bother to NEO with a RR TRENT derivative in 2017-2018, the would wait for the next generation Advance or GTF in 2020+.”

Of course they do. I mean, unless there is a problem with projected deliveries, it is never a good economic decision to re-engine an aircraft! That’s why Aircraft makers wait for the last minute to do so….and some even wait longer, or too long, if they must.

If Airbus “pulls the trigger” now, they can probably proceed with out an A330 production gap. And that would be cool…and it could also be bad for the “Big B”.

It the A330 NEO is as efficient as Leahy and Bregier claim, then it’s going to put a big dent in 787 sales and profits. There will be much wailing and gnashing of teeth in Chicago. Boeing employees in Seattle will cry and declare blood vengeance. Workers in South Carolina will come home drunk and mean and kick their hound dogs through the hedge.

I know someone who broke their foot kicking their dog, maybe a case for a better medical benefits in SC??

AirAsia keeps pushing.

http://www.bloomberg.com/news/2014-07-01/airasia-ceo-pushing-airbus-to-commit-to-killer-a330-upgrade.html

.. and Virgin Atlantic shows interest in A330neo

http://www.flightglobal.com/news/articles/virgin-atlantic-shows-interest-in-a330neo-400951/

The carrier is due to take delivery of its first Dreamliner in late September. It will be the first European airline to receive the larger B787-9 version of the aircraft.

Scott, How rapid a rampu up would you see Boeing going on the 777x program. I cannot see it realistically accelerating from 0 to 8 or 10 in less than 3 years?

Doing the math, from 2015 through 2019 they need to have a backlog of 500 aircraft. If all firm sales (300) and all LOIs (120) come through then they are looking at 80 they need to sell (presuming all come through as you mentioned). I see a series of firesale discounted sales as likely.

Boeing hasn’t said what the ramp up will be but typically it’s about increments of 2 per month per year. In other words, 2/mo for 2020, 4 in 2021, etc.

Assembly of the first 777X should start in 2017 and I expect the line to ramp-up towards 1 frame per month after the last prototype leaves the assembly line (similar like it happened with the 787 and A350). This could be achieved in 2018 I presume, although I have no idea how many testbeds Boeing will build.

Next I expect the line to ramp-up to 2 frames per month just before the jet reaches certification in 2020, followed by a quick ramp-up of 2 frames per month per year. So that’s 4 per month in 2021, 6 per month in 2022 etc.

So even if the current 777 line would go down to 5 or 6 jets per month in 2019, the combined 777/777X output will still be around 8 jets per month.

If Boeing has trouble selling the 777 Classic now, how easily will they be able to sell them in 2021 and 2022, when 777X is in production?

According to Wikipedia, the firm order backlog was 280 at the end of May. Subtract remaining current year deliveries, and that leaves 220. Add the 120 LOIs (assuming they can be firmed up) and Boeing will still need to move 160 more 777 Classics, either by new sales or by getting customers to use their options.

Everett has a mixed record of model changes.

Between 1988 and 1993, Boeing was building 747-400 passenger airplanes mixed with a few 747-200F’s. That was because the -400F did not become available until 1993. The change from -400 to -8 was different. There was a clean break between the last -400 [line number 1419, a -400F] and the first -8.[line number 1420, a -8F]

What will happen from the 777-300ER to the 777-8 and -9? if Everett can handle two different wings, there may be some overlap between the last -300ER’s and the first -8’s and -9’s.

What about the 777F? So far there hasn’t been any mention of a 777-8F or -9F. If a mixed wing line is feasible, and if the demand is there, the 777F could remain in production with the existing wing and engines after the final 777-300ER. The 777F would be available for the next tanker competition to replace the KC-10’s. But that’s a different thread.

Hi Scott,

Long-time reader here; I find your analyses very interesting – always a pleasure to read. I have one pet peeve though – your charts. They are always so bright and honestly, they make my eyes hurt. Maybe try to tone the colours down a bit; make the charts a bit easier on the eyes? Just a constructive comment from me.

I always thought the charts looked pretty dull and I intended to brighten them up. Go figure.

Hamilton

I like the charts. The charts may not be in the most attractive colors, but they are quick to scan and easy to read/study – and this is about all I ask of a chart. Thanks for sharing them with us.

Anyways…talking about colors: what color is the best color to paint a Bike Shed? (and that’s what I really think about the attractiveness of Chart Color)

The charts are fine. FYI – In corporate america, there are a lot of powerpoint rangers who make a living trumping style over substance.

I believe the number of new passenger aircraft with big bellies that will be delivered in the next 7 to 10 years are going to cut into the dedicated freighter business significantly. CX are leading the way on this with he 77W with their balance between seats , cargo and frequency.

It seems pretty simple.

Either Boeing sells 777 current models or they don’t

If they sell enough then nothing happens.

If they don’t, then they cut back production, that just affects people.

Its not like its going to affect the management or anything, after all you need to have your priorities.

Boeing will lower the price until it faces a loss with each sold unit. Keeping a minimum rate can be included. Otherwise, a multi-year dip is just normal in aircraft programs. The management is incentived to produce the maximum number of aircraft to earn the maximum value of money and give the maximum return to the shareholder.

And themselves

“Traffic in that market has been a challenge, but there has been strong growth rate over the past four months.”

The cargo growth is better than it has been but it is nothing to write home to mom about. According to IATA, the growth rate is 4.2% year-to-date. That is below Boeing’s long term forecast of 5.0% per year.

http://www.iata.org/pressroom/pr/Pages/2014-27-05-01.aspx

IATA/ICAO publish statistics of significance to apprx. 2 % of world’s containerised merchandise moved by air (belly-freight + maindeck freight) by its members … the other 98 % are moved by Shipping in TripleE and the alike. 200 Billion RTK vs 10 Trillion RTK. David vs Goliath ? Give Shipping the right tool, and Modal Change will start happening. 1% modal change equates to 50 % rise in ICAO airfreighting statistics.

Problem is that it also works in the other direction — a one percentage point move in the sea freight direction means a 50% drop in air freight. And ships’ efficiency gains can be more substantial than those for new aircraft.

Apparently some 737 fuselages on rail delivery from Wichita to Renton went swimming. http://imgur.com/EJVBCzL

Just Wow..

They typically swim upstream to lay their eggs and then swim back to the ocean to mature and grow wings.

that’s hilarious . . . the picture really does conjure up that image

Jimmy Kimmel by chance?