Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Boeing unlikely to meet FAA’s 90-day deadline for new safety program April 18, 2024

- Focus on quality not slowing innovation, says GKN April 18, 2024

- Boeing defends 787, 777 against whistleblower charges April 17, 2024

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

- Bjorn’s Corner: New engine development. Part 3. Propulsive efficiency April 12, 2024

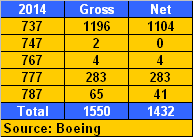

Boeing 2014 orders: 1,550 gross, 1,432 net

Update, 8:45am PST: Boeing sent us this breakout of 777 and 737 orders:

777-300ER: 49

777 Freighter: 14

777X: 220

737 MAX: 891

Original Post:

Boeing received 1,550 gross orders and 1,432 net orders in 2014, one of its best years.

As is typical, the narrow-body 737 was by far and away the leader in orders. Boeing doesn’t break out the 737NG v 737 MAX in its monthly table. The 777 was buoyed by firming up the massive number of 777X commitments announced at the Dubai Air Show in November 2013. Although Boeing doesn’t break out, in this table, the 777X v 777 Classic, the company ended the year with around 60 777 Classic orders, an important number to fill the production gap we and others have been writing about last year.

As is typical, the narrow-body 737 was by far and away the leader in orders. Boeing doesn’t break out the 737NG v 737 MAX in its monthly table. The 777 was buoyed by firming up the massive number of 777X commitments announced at the Dubai Air Show in November 2013. Although Boeing doesn’t break out, in this table, the 777X v 777 Classic, the company ended the year with around 60 777 Classic orders, an important number to fill the production gap we and others have been writing about last year.

The 767 commercial model continues to wind down, as the last ones off the line–all freighters–get delivered. The line will shift over to solely the USAF KC-46A once the 767Fs are delivered.

The 747-8 put in another dismal year, with two gross orders and two cancellations.

Boeing delivered 723 airplanes last year: 485 737s, 19 747s, 6 767s, 99 777s, 114 787s.

Reuters has this update of Airbus’ order position through November, in advance of the annual Airbus press conference on Jan. 13, where full year numbers will be announced. Airbus has a habit of finishing Decembers with a surge of orders, often topping the Boeing numbers.

You got a typo there 777NG v 737 MAX.

Fixed.

10 777F orders in Dec.

Deliveries of 238 widebodies is impressive. A widebody is worth at least two single aisles. Boeing is outproducing Airbus by a wide margin.

About one half of that is produced at cost higher than resultant revenue.

Same can be said of the A350 and A380.

Yup.

Only it is a significantly smaller percentile of the production in that segment at Airbus.

( Anyway, the 748 was kindly omitted on the lossy side).

I wasn’t aware that production costs were an issue for the 748. Development costs, yes, not selling well, yes, but production costs? The line has been around for a really long time. Granted, they may be selling dirt cheap for the last several years, but not many of them have sold over the last several years.

With regard to the A350, the percentage on the lossy side, as you put it, will grow significantly over the next several years until the per frame break even is reached. Not exactly sure when the A380 will stop being lossy.

The 748 line has accumulated further deferred cost.

( and it was in a forward loss position anyway.)

$.5b for the year ? Numbers were cited here some posts ago afair. the 748 was a rather expensive exercise to “keep Airbus honest” .. or whatever. In regularly brilliant hindsight Boeing would have been served well

to have never taken up the 748, had done much better 787 oversight and planning, a more more realistic stance in promising and finally spend less money on astroturfing 😉

condensed: compete on products and not on PR, hyperbole or via bashing campaigns.

I don’t think that $0.5B was really due to production per se. If I recall correctly, fixing the tail tank flutter issue and other improvements and then certifying those improvements was the source.

As far as PR/bashing campaigns are concerned, exactly how much money did Boeing spend on bashing Airbus? I didn’t catch that in the financials.

Uwe – what you said can be said about quite a few aerospace programs, right? No matter what they do will never result in you representing anything but a lossy forecast. They delivered 723 lossy frames to a host of customers who also ordered 1550 gross frames. Give them their do please because lossy or not they were out there selling frames while you continue to type damning comments about their offering. Maybe you should begin following the China programs because they never share anything about their activities. Maybe things won’t be so lossy for the future.

It depends on price if a widebody is really “worth” more than a single aisle aircraft. E.g. what price Boeing receives for each 787 delivered?

There were 29 787-9 orders this year. It appears customers are getting back in line post delay.

Hey Scott- any way you guys can look at where the 787 passes the A330 as the largest operating fleet? Based on current sales numbers the A350 will never surpass either the A330 or the 787. Thanks

1144 A330 built, 1097 operational. 10 a month potentially going down to 9 or even less.

232 787 built, 228 operational. 10 going to 14 a month.

current outcome is no gain. future outcome brings 5,,7 a month advantage to the 787.

Doing the numbers in a simplistic way with

1100 A330 today and a future gain at 8/m versus

230 787 today and a future gain of 14/m ( rather generous asumptions )

I get 145 month ~= 12years for equal fleetsizes of 2260 in

~2027. In the real world I wouldn’t expect this datum before 2030..2032.

The problem I see with your analysis is that it does not account for old aircraft leaving the fleet over your time of interest. This will happen sooner for the A330 than for the 787.

The problem I see with your analysis is that it fails to account for older frames leaving the fleet over the next 15 to 20 years. This will happen sooner for the A330 than for the 787.

That is balanced by far by accounting 787 @14/m from day one. ….. and I don’t think we’ll loose too many A330 beyond hull loses.

Will be interesting to see how well the Dreamliners age.

Wow, amazing year for Boeing. Yet another year with a two-to-one book-to-bill ratio; backlogs keep building. All time high delivery rates notwithstanding, the book-to-bill ratio keeps rolling along at two. The 777 Classic got more orders than the 787, so apparently the ER can be offered at a mix of availability and price that airlines find attractive.

Impressive industry record setting year of 787 deliveries; despite out-of-sequence and traveled work the ten frames per month rate is now proven. On average 123 days were needed from loading to delivery in December, according to All Things 787, up from October (120) but down from November (125). With a more favorable mix of 787-9 frames to be delivered in the year 2015, and potentially a lessened need for contract workers, the 787 program will this year very likely take a step towards non-negative cash flow. However, presuming frames are delivered in the sequence they were ordered, the frames to be delivered this year were ordered in the year 2006, when according to media reports frames were offered at very substantially discounted prices. Same holds for the A350 ‘Mark 1’ orders, by the way.

This has to be Boeing’s yr for orders. Surely?

But yr on yr for past 5 yrs Airbus still ahead on orders and deliveries I believe?

A and B are almost exactly 50/50. The reason is that whoever is temporarily behind will offer better price and availability, and whoever is temporarily ahead will offer less sharp pricing and less favorable availability. Further, whoever is temporarily behind in terms of product will push to improve their product, while whoever is temporarily ahead will never act to upset a market that they are riding high. That’s the dynamics of the duopoly.

A very good year for Boeing! Best thing imo is 787 deliveries getting up to speed.

I agree. 114 deliveries (100 late model -8’s, plus 10 -9’s, plus 4 reworked -8’s) is impressive considering the 10/month rate break at the end of 2013, certifying the -9 and integrating it into the production system, and dealing with the wing crack issue.

Going forward, 2015 will be all about streamlining the production system and continuing the path down the learning curve. Boeing has to eliminate traveled work once and for all, while simultaneously ramping up the Charleston FAL and throttling back the surge line in Everett. This is a tall order, but doable. They also have to start finding takers for the terrible teens so they can reduce the inventory standing around KPAE.

I’m curious to see what the 2015 delivery guidance will be. 130 frames perhaps?

Why 130? 10/mo production rate is not more than 120 for the year, is it not?

You’re right, but I was thinking that Boeing might try to reduce the backlog of frames in Everett. Currently there are 13 frames in Everett awaiting their first flight, 3 frames that are in pre-delivery flight testing, and 3 -9 test frames that are having their test equipment removed and being brought up to certification standards. Plus there are an additional 11 early build -8’s that are awaiting rework and change incorporation. Not counting the frames in pre-delivery flight testing, makes 27 frames standing around! I’m quite sure Boeing could deliver less than an additional frame/month to cut the backlog by 10 this year.

it would seem that Airbus aren’t daunted!

http://www.reuters.com/article/2015/01/06/airbus-group-orders-idUSL6N0UL32220150106

Not surprising really, a lot of A330Neo were firmed up in December, there’s the Indigo order, possibly, and a few other sizeable MoUs. And one or the other manufacturer is probably going to get a good start to 2015 thanks to Avianca.

To be followed up are the 575 Boeing 737 aircrafts sold to “unidentified customers” that is more than 50% !!!

We will see if Airbus play the same game

And in the years to come Boeing will announce order already accounted for in these 575

If Boeing have already claimed them as firm orders for unidentified customers they cannot count them again in 2015, all they can do is reveal the identity of the purchasers.

The MoUs I referred to for Airbus are announced orders that have not as yet been turned into firm contracts and so are not yet added into the sales figures. Traditionaslly, Airbus’s fifth quarter consists of firming these up. whereas Boeing seem to amass large numbers of unidentified customers. Two different ways of playing the same game!

Can we please stop with the “5th quarter” nonsense. It is just 2 weeks of the year and any orders announced in this period and counted to the previous year should not have any material impact on the totals as long as the period between the annual briefings is 12 months!

It is a strange thing with “Unidentified Orders”.

up to 2007 ( starting with their earlierst record from 1958 ) we see 8 UO frames. From 2008 to june 2012 a further 68.

Then UO frames seem to explode: another 1040 UO frames to the end of 2014.

What has changed? I don’t think that airlines have suddenly become shy?

apropos: depending on how UO to $NamedAirline conversions are handled by Boeings reporting interface my enumeration may be (significantly?) off.

What definitely remains is that UO orders represent

quite a significant piece of the order pie today.

Sometimes when you will order anyway, it is beneficial to have equipment ordered before next years price increases.

I agree 626 aircraft for “Unidentified Customer(s)” is on the high side. But no one feels like asking questions, so it must be OK.

http://active.boeing.com/commercial/orders/index.cfm

Yes we already exchange message about this subject … Scott says it is correct I stil look for away to believe it

Seems like counting delivered aircraft is a too simplistic measure. What is the total empty weight delivered or MTOW delivered? What is the retail value delivered?

I’m taking a rough guess that Boeing just delivered US 150 billion of aircraft in 2014, and Airbus delivered about 100 billion or so.

TC, why do you think boeing has nearly 50% higher average selling price than airbus for deliveries ? A380 vs. 747-8, number of A321 vs. 737-9…

For reference, in 2013 Airbus had 53% unit share and 53% revenue share on net orders. (Leahy annual press conference 2014 slides).

to TC

Just taking care of the sales figures in US dollars is just even more simplistic measure . Just think of what is called “creative accounting” … for example, how Boeing is charging each 787 sold with its share of deferred cost !!! usw.