Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Bjorn’s Corner: New engine development. Part 4. Propulsive efficiency April 19, 2024

- Boeing unlikely to meet FAA’s 90-day deadline for new safety program April 18, 2024

- Focus on quality not slowing innovation, says GKN April 18, 2024

- Boeing defends 787, 777 against whistleblower charges April 17, 2024

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

Forecast 2022: ATR has monopoly, De Havilland looks to hydrogen and Embraer lurks with new design

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Introduction

Jan. 31, 2022, © Leeham News: ATR is now effectively the only turboprop manufacturer outside of China and Russia in the 40-80 seat sector. The models are the ATR 42-600, ATR 42-600S (STOL), and ATR 72-600.

The series was built on simplicity with unpowered controls and the simplest possible systems. It has worked well for ATR when selling to markets that want airlift to the lowest possible cost. It also means the design is at its limits capacity and speed-wise, any more capacity or performance and it needs powered controls and more elaborate systems. It was behind ATR’s desire to develop a new, larger model in the past.

The series was built on simplicity with unpowered controls and the simplest possible systems. It has worked well for ATR when selling to markets that want airlift to the lowest possible cost. It also means the design is at its limits capacity and speed-wise, any more capacity or performance and it needs powered controls and more elaborate systems. It was behind ATR’s desire to develop a new, larger model in the past.

But ATR has little reason to develop a new turboprop now that it is in a monopoly position. This could change if Embraer proceeds with its concept for a new family of two turboprops, a 70- and a 90-seat aircraft. Embraer’s base design could form the basis of a hydrogen-burning gas turbine model in the future.

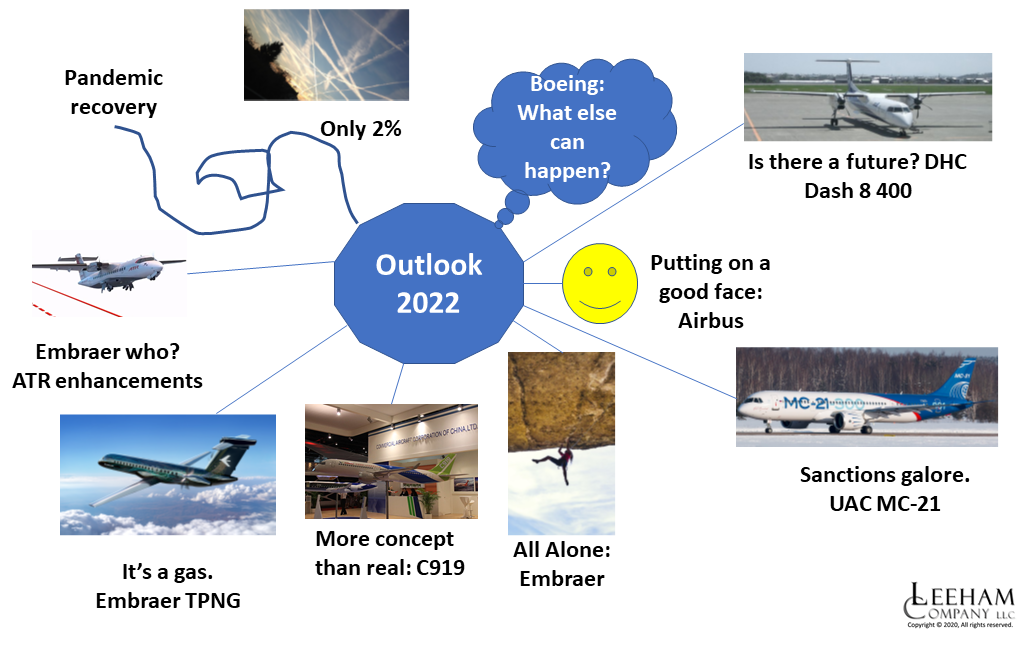

2022 Outlook depends largely on pandemic, Boeing recovery

Subscription Required

By the Leeham News Team

Dec. 13, 2021, © Leeham News: Attempting a forecast for the new year historically has been reasonably easy. One just started with the stability of the current years, and maybe the previous one or two years, and looked forward to next year.

Until the Boeing 737 MAX grounding, COVID-19 pandemic, and the Boeing 787 suspension of deliveries.

These events upended everything. Boeing’s outlook for 2020 depended on what happened to return the MAX to service. The grounding, initially expected by many to be measured in months, ultimately was measured in years.

The 2020 outlook for the rest of the aircraft manufacturers blew up that March with the global pandemic.

Then, in October 2020, Boeing suspended deliveries of the 787, exacerbating its cash flow crunch.

Commercial aviation began to recover some in late 2020. Airbus, which reduced but didn’t suspend deliveries throughout 2020, saw signs of hope for the narrowbody market—less so for widebody airplanes.

There is a lot of uncertainty, however, that makes looking even one year ahead challenging.

Regional Aircraft production

Subscription Required

By Vincent Valery

Introduction

Nov. 22, 2021, © Leeham News: Last week, LNA looked at Airbus and Boeing’s planned twin-aisle production rates. We now turn our attention to production rates in the regional aircraft market.

The production of the Mitsubishi Heavy Industry-owned CRJ ceased earlier this year, while De Havilland of Canada’s Q400 will also end soon. Few expect production on the latter program to restart.

KLM E-Jet

MHI also halted the development of its MRJ/SpaceJet, with a program restart unlikely at this point. These exits mean that ATR and Embraer will be the only major regional OEMs outside China and Russia.

ATR announced plans to raise its combined ATR42 and ATR72 production to 50 aircraft annually. LNA will investigate whether the turboprop’s order book justifies such an increase.

LNA will separately analyze the Embraer E175 and E-Jet E2 production. Since the E-Jet E2 Embraer program competes with Airbus’ A220, we will also look at production plans on the latter.

Summary

- An optimistic ATR production plan;

- Comparing E175 and E Jet-E2 production;

- Steady A220 production plans;

- Orders at risk;

- Other OEMs.

ATR, Pratt & Whitney launch new turboprop engine

By Judson Rollins

November 16, 2021, © Leeham News: ATR and Pratt & Whitney Canada jointly announced a new PW127XT engine for the ATR-42 and -72 series at the Dubai Air Show. The XT designation stands for “extra time on wing.”

Pratt & Whitney says the engine will offer 40% greater time on wing, 20% lower maintenance cost, and 3% lower fuel consumption than the current-generation PW127M.

The 40% time on wing assumes a 60-minute average mission in “benign environments.” The reduction in maintenance cost is driven by a requirement for just two scheduled engine events in ten years. Fuel burn improvements were achieved via a new compressor and updated turbine module. Read more

Pontifications: Engines drive timing of new Embraer TPNG

The first report appeared Oct. 18, 2021.

By Scott Hamilton

Oct. 25, 2021, © Leeham News: Embraer appears marching toward launching a new turboprop aircraft next year with a targeted 2027 entry into service.

The timing will be determined by the engine. Pratt & Whitney, GE Aviation and Rolls-Royce have development programs. PW and GE are farthest along. PW is thought to have the best chance of winning Embraer’s business. (Pratt & Whitney supplies the engines for the E2 jet. GE supplied the engines for the E1.)

In an interview at the IATA AGM Oct. 3-5 in Boston, Arjan Meijer, the president of Embraer Commercial Aviation, said the competition remains open today.

Pontifications: The reshaped commercial aviation sector

By Scott Hamilton

July 12, 2021, © Leeham News: With Washington State and the US open for business following nearly 18 months of COVID-pandemic shut-down, there is a lot of optimism in commercial aviation.

In the US, airline passenger traffic headcounts are matching or exceeding pre-pandemic TSA screening numbers. Airlines are placing orders with Airbus, Boeing and even Embraer in slowly increasing frequency.

The supply chain to these three OEMs looks forward to a return to previous production rates.

It’s great to see and even feel this optimism. But the recovery will nevertheless be a slow if steady incline.

2021 fleet trends: small jets get bigger, bigger jets get smaller – and the old makes way for the new

Subscription Required

By Judson Rollins

Introduction

May 13, 2021, © Leeham News: Aviation data provider Cirium said last week that just under 7,850 commercial aircraft were still in storage, down from 8,684 at the beginning of the year and a peak of 16,522 at the apex of the COVID-19 crisis last April.

Although there was an initial spike in aircraft retirements in March and April 2020, the total number has stayed in line with historical norms to date. However, order books for most types have stagnated or even gone backward since the start of the pandemic.

A few trends are becoming clear: larger single-aisles are thriving, larger twin-aisles are disappearing, and sub-100-seat orders are flatlining. Not surprisingly, older-generation aircraft are disappearing at an accelerated rate.

Summary

- Airlines are upgauging their single-aisle orders in anticipation of lower yields and competitive battles.

- Widebody order books continue to struggle; the bigger the airplane, the worse the demand.

- Regional jet and turboprop order backlogs have stagnated.

Bjorn’s Corner: The challenges of hydrogen. Part 32. Wrap-up: Going forward

By Bjorn Fehrm

April 9, 2021, ©. Leeham News: Last week we made a summary of the history of initiatives for sustainable aviation, now we look at the likely developments over the next 10 years.

What is the likely development for different classes of airliners and what technologies will be popular?

Pontifications: Recovery plans from the pandemic at ATR, De Havilland

By Scott Hamilton

March 29, 2021, © Leeham News: Aviation stakeholders’ attention understandably focuses on Airbus and Boeing as the industry works its way through the COVID-19 pandemic. Embraer gets less attention than the Big Two.

But two other OEMs must be considered as well: ATR and De Havilland Canada.

Outside of China and Russia, whose home-grown industries sell only to these markets, ATR and DHC are the only manufacturers of turboprops in the 50-90 seat sectors.

LNA revealed on Jan. 12 that DHC would suspend Dash 8-400 production after the small backlog rolled off the assembly line. The privately held company delivered 11 airplanes last year due to the pandemic.

About 900 aging regional turboprop aircraft need to be replaced in the coming years.

De Havilland to pause production this year after backlog built

By Scott Hamilton

Jan. 12, 2021, © Leeham News: De Havilland Canada will pause production later this year when the current Dash 8-400 backlog is assembled.![]()

According to data reviewed by LNA, there are 17 Dash 8s scheduled for delivery to customers this year. There are two more that don’t have identified customers. It is unclear if these will be built.

DHC notified suppliers to stop sending parts and components to avoid building whitetails.

De Havilland assembled the Dash 8s at the Toronto plant previously owned by Bombardier. The lease on the facility expires in 2023. There is no decision whether to move the final assembly line to Western Canada, where DHC is headquartered.