Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Boeing unlikely to meet FAA’s 90-day deadline for new safety program April 18, 2024

- Focus on quality not slowing innovation, says GKN April 18, 2024

- Boeing defends 787, 777 against whistleblower charges April 17, 2024

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

- Bjorn’s Corner: New engine development. Part 3. Propulsive efficiency April 12, 2024

MTU investors day: views of its engine programs, future airplane timelines; separately, Embraer COO interview

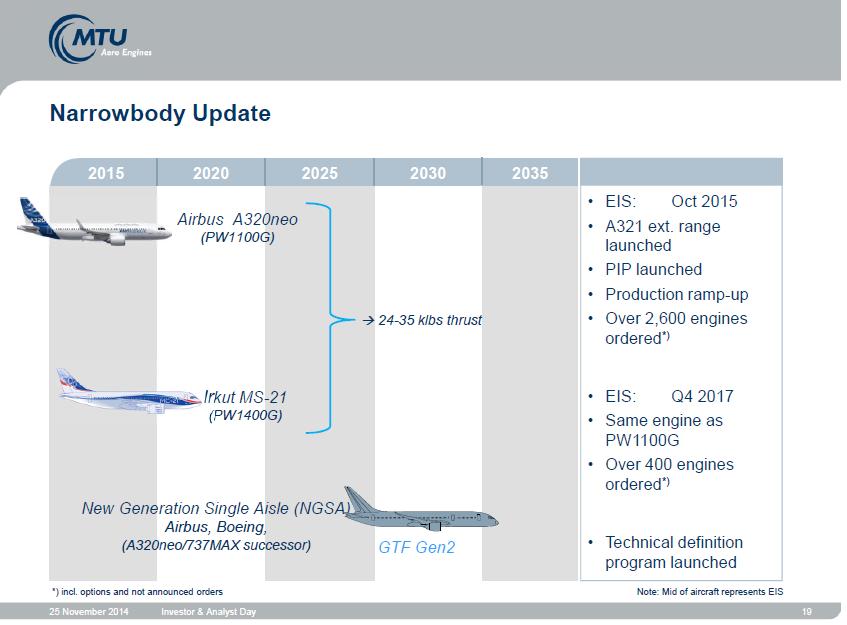

Figure 1. Technical milestones have been passed on PW GTF programs for the applications on Bombardier, Airbus, Mitsubishi and Irkut airplanes and are approaching for Embraer. Source: MTU Investors Day. Click to enlarge.

Nov. 30, 2014: MTU Investors Day: MTU is a major participant in engine development and supplies, participating on the GEnx, GTF and GEnx program. It’s also a member of the joint venture in International Aero Engines and it’s a major player in the aftermarket Maintenance, Repair and Overhaul (MRO) sector, providing a serious competitive alternative to the aftermarket contracts offered by the engine OEMs. Its held an investors day conference Nov. 25. Highlights included:

- Milestones have been passed on the Pratt & Whitney Geared Turbo Fanengine for the Bombardier CSeries, Airbus A320neo family, the Mitsubishi MRJ and Irkut MC-21; and are on schedule for the Embraer E-Jet E2.

- The success of the GTF is requiring huge production commitments.

- The large number of airplane/engine programs require a major ramp-up of production during the next few years.

- The major investment in new engines is largely over for now, leading to the expectation of long-term revenue from MRO.

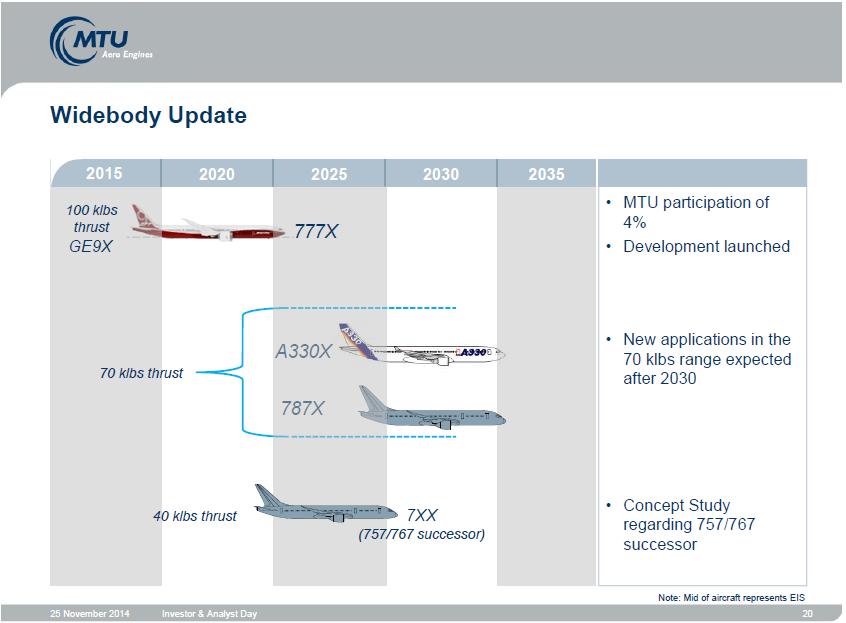

Figure 2: MTU sees the need for new engines in the 2025 period for a replacement for the Boeing 757/767 and successors to the Airbus A330 and Boeing 787 around 2030. These are estimate dates, not firm plans. Source: MTU Investors Day. Click to englarge.

- That said, MTU is looking toward the future with new engines for the 757/767 replacement, the New Small Airplane (NSA) and the follow-ons to the Boeing 787 (the 787X) and A330 (A330X). The 757/767 replacement timing is targeted for about 2025 in the MTU view, which coincides with what we reported months ago. MTU sees a 757/767 replacement market of 400-600 aircraft, compared with the 200 for the 757 replacement seen by Airbus.

- Development of the NSA would follow that of the 757/767 replacement,

Figure 3: MTU sees the New Small Airplane replacement around 2030. Source: MTU Investors Days. Click to enlarge.

according to MTU’s update. This sequence tracks what we reported months ago. The 2030 timeline is consistent with recent statements by Boeing CEO Jim McNerney but is a few years later than the 2027 timeline we anticipated.

- The falling price of fuel doesn’t mean there will be cancellations or deferrals of present orders. It could mean extended service of the Boeing 757 and the PW 2000 engine and aircraft powered by the GE Aviation CF6 engines, however, in the MTU view.

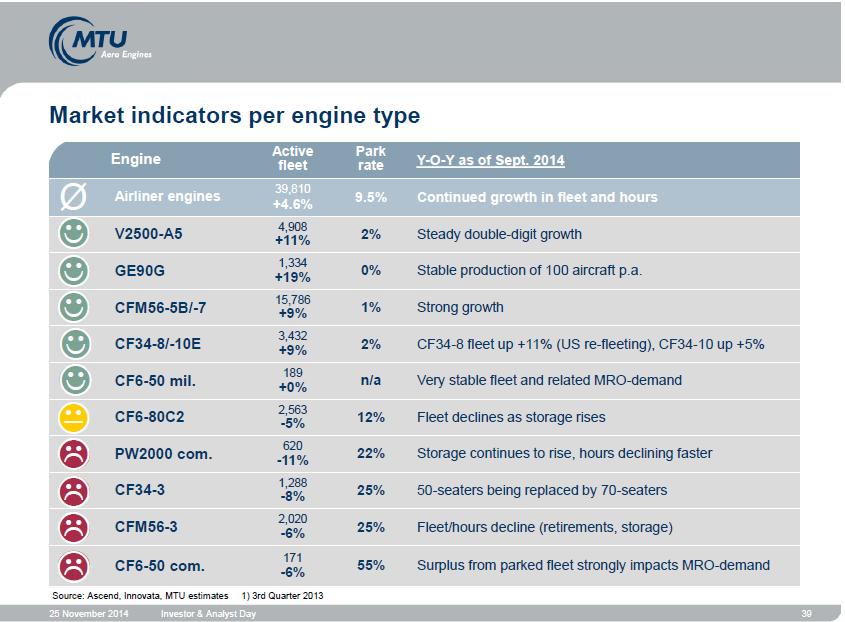

Figure 4: MTU is a major player in the engine aftermarket MRO sector. The market potential of in-service engines is illustrated above. These are only engines for which MTU offers MRO services. Source: MTU Investors Day. Click to enlarge.

- The Open Rotor engine is no longer on the MTU horizon. This does not mean that some day it won’t reemerge.

- The engine aftermarket sector is assessed in Figure 4. Revenue from MRO services will be a major part of MTU’s business model during the next several years.

- Lower oil prices might make it economically viable to reactivate some of the older airplanes. The key is whether oil prices will remain low or not.

Embraer COO interview: Our Oct. 15 posting of our interview with the chief operating officer of Embraer is now open to all readers.

The Open Rotor engine is dead as long the noise issue is not solved.

To put such an engine on top of an Blended Wing Body will not change much of the problem. Low frequencies don’t care much about obstacles. Low frequencies just deflect around obstacles.

The next aircraft generation has to be quieter.

I also don’t believe in BWB for civil aircraft. Maybe canards with large GTF engines on top of the wings.

The scoop on your statement is that there will be no “discontinuities” in aircraft development.?

Wing + Tube + Turbofan. system changes ( design detailing, manufacturing), finetuning.

That is a steep hurdle for a Boeing NSA.

I believe there will be no big “discontinuities” in aircraft production. A BWB design will need far more different frame sections than an barreled fuselage. The problem is not only related to the structure but also to the interior that must fit to the BWB shape. A more complex design will be more expensive. How big is the BWB advantage?

Does the 787 composite advantage pays of against the A330? – “No more moonshots!”

http://commons.wikimedia.org/wiki/File:X-48B_seen_from_left_down.jpg

A nice view from beneath from a BWB study in flight. You can see the engines then you will hear them without any reduction.

I also have a personal fear to open rotor according to something else:

http://www.dailymail.co.uk/news/article-2827918/Air-Canada-passenger-hit-head-propeller-breaks-loose-slices-cabin.html

I try to avoid certain seats on turbo props.

Due to noise and safety reasons I believe there is no future for the open rotor or an unducted fan. Put a simple duct around any noise source and it will be quieter. Therefore a ducted turbofan will always be quieter than an open rotor.

Rolls-Royce Ultra with variable pitch fan blades looks quit as an ducted open rotor.

I think one of the biggest advantages of a tube with wings is how the same platform can be easily stretched or shrunk to meet different market sizes. How would you do that with a BWB?

I’d agree that BWB makes less sense when you’re using conventional greenhouse gas–emitting jet fuels. For a sustainable future, the industry will in all likelihood have to move away from the current jet fuels in the not too distant future. Thus, the industry can choose if they want to move forward and adapt much more proactive strategies, or rather remain in a state of a reactive adaptation, or non- strategy, where many of the players seem to be “happy enough” about the status quo.

So, yes — the current tube and wing configuration seems to be a perfect match to the conventional greenhouse gas–emitting jet fuels. However, if we as a civilization are serious about moving towards a much less carbon-intensive future, then all options should be on the table. As a starter, the combination of the huge internal volume of a BWB and the voluminous liquid hydrogen fuel may be a good match. Here’s one concept:

http://ntrs.nasa.gov/archive/nasa/casi.ntrs.nasa.gov/20040033924.pdf

You are aware of the fact that there are already Direct Methanol Fuel Cells (DMFC) available for commercial purpose?

http://www.sfc.com/en

So the fuselage and wing concept would therefore still work with methanol instead of jet fuel. No need for BWB.

There is one problem with methanol. Energy density of jet fuel is about 2.5 times higher than methanol.

BTW even fuel cells emit carbon dioxide.

“BTW even fuel cells emit carbon dioxide.”

Only if your fuel actually contains carbon. Which is not the case with LH2 as fuel.

The DMFC cells are rather new. Most types that can work on CnHm fuels work with high temperature processes.

Well illustrated good interesting article *****

“MTU sees a 757/767 replacement market of 400-600 aircraft, compared with the 200 for the 757 replacement seen by Airbus.”

Logically Airbus is looking at the isolated 757 replacement market, they are in the process selling the A321 LR to 757 operators AA, DL and UA.

The segment under the 787-800 / A330 is obviously much larger. US Transcon, TATAL, Intra Asia, Leisure flights. Easily >2000 in the next 20 years. At the cost of A330 / 787-8s. Boeing jumping on that segment and creating something optimized for it seems a good idea to me.

What I’m concerned about though, is the assumption the MAX will be good enough until 2030. Wishful thinking in my opinion.

– The 737MAX is quickly becoming a one trick pony (-800/-8).

– The NEO, COMAC, MS-21 offer superior noise levels, cargo capability, capacity growth options and comfort.

– The Cseries, MRJ and E2 will offer superior economics <150 seats.

Boeing looks at the opportunity to grab the market for a 200-300 seat medium range platform. After that they want to do the NGSA (New Generation Single Aisle) at the end of next decade, around 2030.

Likely the market won't allow them. The MAX likely isn't good enough anymore for airlines to invest for the next 20 years, say after 2020. Like the market didn't allow Boeing to do the NSA when they came up with a 2020/21 EIS. In 2011 Southwest, Delta and AA told them nice concept, but too late for us, we'll look for alternatives.

http://www.reuters.com/article/2011/08/05/uk-southwest-airbus-idUSLNE77401020110805

Maybe the MAX is out of production and replaced by 2035, but in 2030, the MAX is still good for a few hundred aircraft that year.

Midway saw “mile long” lines yesterday. What does Southwest do to increase capacity? Ask A or B to design an aircraft for Midway like the 727 was designed for LaGuardia?

737-9 come empty and they go empty, eh?

A380 reduced MTOW version ;-?

You’ll probably need white cloved sardine can fillers

like they have in Tokyo’s tube stations 😉

“in 2030, the MAX is still good for a few hundred aircraft that year.”

Why? What minimal margins and marketshare will be acceptable? It reminds of 2011 when Randy declared the 737-800 was still better then the NEO & Airbus only catching up. The 739ER was the perfect 757 replacement.

A large part of the public absorbed, discussed and accepted that vision.

Within a year the airlines had corrected Boeing, the hard way. This could happen again with the MAX. I think it could be sooner then most feel.

Look at who Boeing tries to woe.

Those are the real customers 😉

Airlines are increasingly separated from the airframers

by financial entities that have decidedly different objectives.

@Uwe: LOL, I think you mean “woo” not “woe.”

He, yes.

Getting older I notice that there is a slight increase in getting trapped by homonyms and similar spelling issues. Probably should do more spoken language immersion.

Stealth is no major feature for commercial aircrafts, and that is why we will not see blended wing designs any time soon – if ever.

It is also not the question of engines. You can put a new and improved engine on pretty much any wing. Bypass ratios will go up and up, but for that you don’t need a new plane.

But why is McNerny talking of “moonshots”? Because the Boeing engineers

keep telling the managers that the new NSB can only be made from CFRP. And that with the 787 loosing money like crasy.

But only with CFRP you can reduce the weight and improve performance as it will be necessary. Moor’s law, in some special variation, applies here too. Airbus plays Tic-Toc like Intel. Boeing must watch out not to become AMD. So the big question that is on the table is how to mass-produce CFRP narrobodies profitably. But the method they have chosen for the 787 is certainly way too slow and expensive.

So what to do? There certainly is no supplier who can solve this, so the aircraft manufactureres have to invest big time to develop such production technology (maybe hot-RTM?) on their own and build new machinery and factories. And here you have your “moonshot”.

there are other possibilities out there other than BWB that offer step change performance improvement opportunities over traditional tube and wing.

the most producible, and most amenable to being stretched to enable a family of aircraft is the side by side double bubble lifting body.

using an A320 tube diameter, it is possible to build a twin aisle, 10 across coach, 8 across coach+, 6 across first fuselage that supports 2 wide Ld3-45 cargo and seats 230 people in 20 rows of coach and 5 rows of first.

combine that with a canard config with honda-like overwing engines you can keep the MLG short and relatively far aft to save a lot of structural weight while still having good rotation angles and dramiatically better L/D ratios.

toss in 2nd gen active laminar flow control (using 789 lessons learned),

3rd gen GTF (with 4+:1 gear and CMC hot section tech),

panelized CFRP construction (less weight optimal but more volume production and maintenance friendly),

dual function winglet/ruddervators to eliminate or at least greatly reduce the size/weight and drag of the vert stab,

mid body main doors for improved turn time (and no need for folding canards)

and you have one hell of an efficient airplane that fits well within the class C gate box.

Hello my good old friend Bilbo,

you know, what you propose there is a tripple moonshot, and I bet my hat that is exaclty what will not happen – not at Boeing nor at Airbus.

When you look into the Palantir you will probably see a single-aisle with a somewhat larger diameter than the A320, that’s all. It will allow for a little wider aisle (for short haul) or wider seats (for long haul) and of course containerized freight.

Maybe panels are the right solution for (fast) mass-production. But not if they are made in an autoclave, the process takes half a day. Hot-RTM would allow to make a part in less than an hour. If I am not mistaken, the fan of the Leap-engine is the first made with RTM (resin-transfer-molding) woven CFRP. Don’t know if that is cold (40°C temperature or the mold) or hot (100-140°C), but cold is not any faster than autoclave cured prepregs.

But to make parts for the body and wing of an airliner in that process will afford giant investments in R&D, machinery and tooling. Investments that no supplier would be able or willing to shoulder.

And this is the onion that McNerney is not willing to bite. 🙂

Looks like A350 doors are done in RTM:

http://www.wickert-presstech.de/typo/inhalt//aktuelles/single-news/?tx_ttnews%5Btt_news%5D=4&L=7

spoilers and stuff:

https://www.google.de/search?q=resin-transfer-molding+airbus

and over the pond:

https://www.google.de/search?q=resin-transfer-molding+boeing

they appear to still invent it at the forefront of technology 😉

Gundolf,

sadly you are 100% correct that the 737/a320/757 replacement will no doubt be a 6 wide single aisle tube and wing that looks very much like every other current commercial aircraft.

it will be built out of zero risk materials , use zero risk engines, zero risk aerodynamics and be boring as hell.

it will be assembled in a Maqiladora in the free trade zone south of Brownsville Texas by workers who have never flown on an airplane much less built one.

it will be 6 years late and result in Boeing getting bought out by Fiat in a transaction engineered by congress.

it will be a monument to wall street engineering.

A question regarding the first graphic above.

The A320neo PW1100G shows “Q4 2014” in engine certification. Is it yet to be done despite the on-going neo flight testing or have I misunderstood it?

We don’t specifically know the answer to @nyx’s question but assume certification has yet to be completed. Recall that the P1500G (CSeries) engine was flying for a while before certification was achieved, so we believe this to be the case with the P1100G (A320neo).

Thanks Scott.

So they have a little over 4 weeks to make good. I also see that the MRJ will have first flight before engine certification but the order is reversed for the MS-21.

I don’t doubt the ability to produce airliners, but how about airport capacity? In the 2025 to 2035 timeframe, probably there will still be two pilots per aircraft and more people moving through existing airports. I could see a market for 10K 180 seaters, NEO, MAX, and new designs. Additionally, the increased capacity density and fixed cost per flight will drive the need for a twin aisle for 200 to 250 seats, which could easily be a market for another 10K units in this period. Where will the optimal wingspan for operating dense airports and the optimal wingspan for fuel efficiency cross paths?

o McNeneaney putting on his shirt is a “moon shot”

If you don’t want to be in the airplane business, then get out of the business. Plane (pun intended) simple.

The 787 was not a moon shot, almost 100% of its problems were incredibly poor management of biblical proportions and those not were driven by same lousy management. For the technical leap there have been remarkably few failures and those can be attributed to management decisions on out source and cost, resource starvation and the work force attacks.

The materials are know, the research is there, you have customers that participate and order when you deliver, a lot of industries would like that sort of certainty.

The 787 stacked huge orders because it was the right aircraft for the right market well documented and supported by the operators with their orders.

The engineering issues were few, wing joint was a weight reducing attempt, the battery issue is well documented. Production quality issue are procedural not structural.

Trying to build it in two different locations with a green work force making the critical key structures that go to both is the current problem and they laid off the contract workers (now rehired to some degree) that were gluing that together.

.. it was such an advanced design that management expected the plane to self assemble.

Actually the process stumbled on lack of interface definitions and not communicating those 😉

An underlying reason was that higher up understanding of production processes did not mirror reality. i.e. the map definitely was not the territory caused by how management and workforce ( actually the unions/trade organizations) think and interact.

Pingback: Embraer - Aviation News - 1 Dec 2014 -