Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

- Bjorn’s Corner: New engine development. Part 3. Propulsive efficiency April 12, 2024

- A350-1000 or 777-9? Part 2 April 11, 2024

- Pontifications: Boeing “transparency”–not so much. April 9, 2024

- Airbus charges and write-offs since 1999: more than €33bn April 8, 2024

Rolls-Royce and the leasing market

By Bjorn Fehrm

22 Jan. 2015: When talking to leasing companies at the annual Growth Frontiers 2015 conference in Dublin, Rolls-Royce is the engine manufacturer that is perceived as the least desirable on their airplanes.

This has no reliability or performance background, Rolls-Royce has a good reputation for producing solid and reliable engines which serves their operators well. It is rather the success of Rolls-Royce’s after market program, TotalCare, which is the at the root of the Leasing companies problems with Rolls-Royce.

Lessors and TotalCare

Airplane leasing has an important role in the commercial airplane market, this is not only to finance and lease (rent) airplanes to operators but also to provide the liquidity of available aircraft and engines to the market when operators need extra assets for one reason or the other. This “oiling” of the market takes several forms:

- Shorten delivery times for new aircraft. Leasing companies put speculative orders with aircraft and engine manufacturers and can thereby lease aircraft / engines to operators within shorter timeframes than if they ordered new airplanes from the OEM. This can be used for initial deliveries, for mid delivery additions or for topping up a fleet of airplanes after ordinary deliveries have finished.

- Place the aircraft that comes off the initial lease period as 7-15 year old airframes with the second lease operator, thereby including any refurbishing and cabin adaptation necessary to the transition operations of due diligence of the asset, renewing contracts, transfer any maintenance provisions etc.

- Buying used aircraft from operators (or other leasing companies) and place them with their next carrier in the market.

In all these operations the leasing companies prefer to have the maximum of choice for partners and solution providers and the meaning in the leasing community is that airplanes with Rolls-Royce engines present the least flexibility in this respect. Engines on midlife aircraft can represent up to 50% of the aircraft value or more so any real or perceived constrains around the engines are important issues for the leasing community.

Rolls-Royce answer

Rolls-Royce Senior Vice President, Customer Strategy & Marketing, James Barry therefore used his presentation at the conference to talk about what the company is doing to change any real or perceived constrains for their Trent engine portfolio. He started by pointing out:

- Engine maintenance costs does only represent 7% of total operating costs for an aircraft and an engines condition has a significant influence on the largest cost item, fuel, which even with today’s prices represent 30-40% of operating costs for a widebody aircraft that uses Trent engines.

- The Trent fleet is still young, the oldest Trent 700 is now 18 years old and the average age of that fleet is still below 10 years [the average age of the total Trent fleet flying is around 10 years with the Trent 800 having the highest average age of around 13 years]. So the flexibility in after market solutions asked for by the leasing community has not been in demand according to Rolls-Royce. As this time has now come the company is addressing the issues.

Barry then described how the needs of operators and owners of Trent engines change over time, Figure 1.

Figure 1. Rolls-Royce picture of the different phases of an airline engines lifecycle and the corresponding need for different aftermarket solutions. Source: Rolls-Royce.

In the first part of a Trent engines life the operator priorities maximum risk transfer to the engine supplier and highest overall reliability. Any disruption to a widebody service means a large number of passengers have to have their transportation re-arranged with ensuing high costs and loss of passenger confidence. Barry points out that most Trent engines are still in this phase.

As the airframe and engines comes into mid-life or older the priorities of owners and operators change, they now want to wind down the value of the airframe and engines so that at end of life the value of the asset is extracted to the desired level for storing or part out.

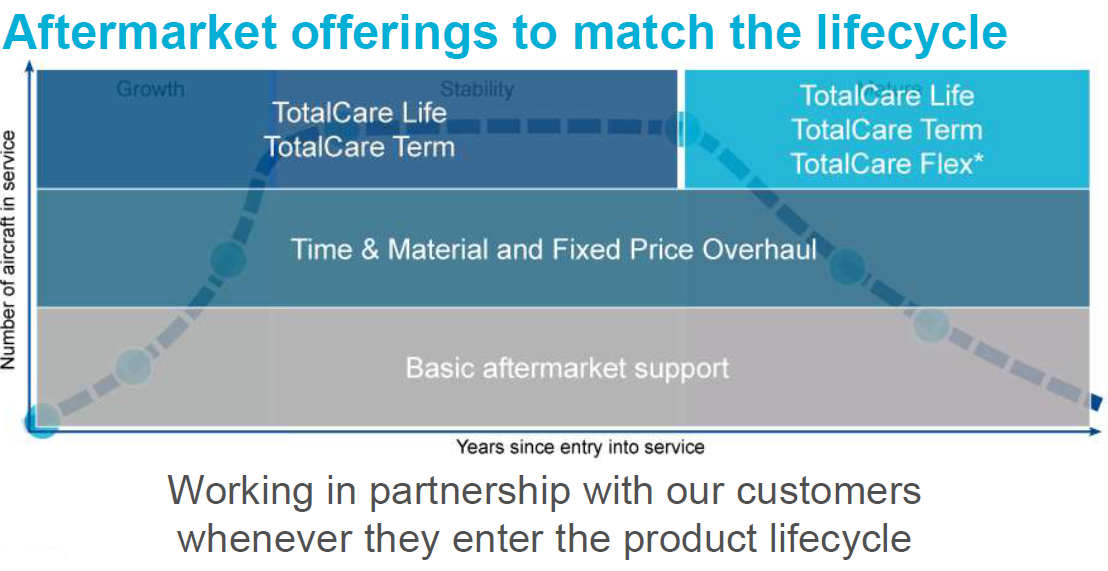

“To respond to the market’s needs” says Barry, “we have always maintained a flexible after market services offering”, Figure 2.

Figure 2. Aftermarket portfolio for Trent engines. Source: Rolls-Royce.

“For reasons of attractiveness the overall majority of operators have chosen TotalCare Life or Term for their engines”. “We have however listened to our customers and we are therefore complementing our TotalCare offering with TotalCare Flex” says Barry. “TotalCare Flex is designed to gradually extract the value of the engine to the owner so that the asset has the desired value at the end of its life”.”We do that by using used spare parts and other arrangements in a joint plan with the engines owner”.

TotalCare Flex is still in its pilot phase with the first Rolls-Royce customers but Rolls-Royce expect to brief the market on its terms and conditions later this year. It contains flexibility for change of operators, shorter deal periods, use of used marterials etc. to lower cost per flight hour assures Barry. United is already operating an early verson of TotalCare Flex and others are working with Rolls on the final product.

Rolls-Royce believe that the leasing market shall find that many of their issues with TotalCare shall thereby be solved. Barry also pointed out that the number of third party service providers for Trent engines will grow as the programs now enter a phase where there is a market for such companies, Figure 3.

Figure 3. Rolls-Royce and joint venture shops (blue) and up-and-coming 3rd party shops (yellow and brown). Source: Rolls-Royce.

A340-600 and Trent 500

Barry then gave a status update for their maintenance cost program “Four engines for the price of Two” together with Airbus for A340-600 operators. It assures that the maintenance costs for A340’s four Trent 500 shall not be higher than the cost for maintaining two GE90-115 on a 777-300ER.

This program is in full swing and Rolls-Royce is implementing it in cooperation with Lufthansa Technik at their joint engine MRO company N3 in Germany (the N3 name is denoting it is exclusively set up to service Rolls-Royce 3 shaft engines; right now Trent 700, 500 and 900). Barry reiterated Rolls-Royce’s commitment to the program and to its primary goal, to bring the lifecycle costs of the A340-600 engines in line with those for the 777-300ER. Beneficiary will be customers which will pick up A340-600 aircraft coming to the market from e.g Virgin Atlantic, IAG / Iberia and other A340-600 operators.

With the 3rd party shops, is their competitive leeway cost-wise in labour only, or does RR also allow fitting of alternately sourced parts on younger engines?

As far as we know there is no alternative supplier of spare parts, that leaves repair of parts and used parts from part out engines. This is available but Rolls-Royce to our knowledge has such a grip on the Trent market (contrary to the RB211 market) that there is no meaningful 3rd party activity at the moment. Part of that is that only the Trent 800 for the 777-200/-200ER and -300 (non ER) has been long enough in the market for any volume of MRO activities, and Rolls has been good at tying up first time operators with TotalCare. Only when these 777 goes into second or third operator will there be real demand for 3rd party MRO.

OK, thanks Bjorn.

Glad to learn that RR starts to realize they need to change direction. ANY – Rolls powered aircraft has a residual value below that of other engine manufactures. Per the above, engine MX costs may only be 7% of total operating costs (not sure if this is true) but this doesn’t factor in the extra depreciation RR owners see.

RR has a monopoly on the MX, and aftermarket. Without opening up the market to third parties, operators will either pay for overpriced shop visits or phase out their aircraft below book.

There is no meaning of opening up the MRO market to 3rd party at declining stage of engine life cycle. Becauese nobody will be interested to develope repairs (DER/OEM) and RR holding all the used materials (if there is any). Even very little margin on labor cost that 3p MROs may offer would be nullified by handling charges.

It is difficult for an Engine Manufacturer to recognize that their monopoly in the Aftermaket (that they continuously strive to achieve) will have detrimental consequences on the long term success of their product.

It is the market driven competition (among OEM, independent MROs, Casting houses, PMA sources, brokers, lessors, etc.) in the Post-Production life of an engine family that drives the reduction in specific operating and maintenance costs and motivates operators to keep such products in service.

This competition drives the introduction of improvements in material technologies, repair and maintenance technolgies into the slowly aging engines, resulting in increased realiability and durability and reduction in specifc MX costs.

Unfortunately there is an intrinsic conflict of interest bettween OEM Aftermarket and Product Improvement, especialy after the termination of production. OEMs have hard times to acknowledge and especially to act on this matter.