Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Boeing unlikely to meet FAA’s 90-day deadline for new safety program April 18, 2024

- Focus on quality not slowing innovation, says GKN April 18, 2024

- Boeing defends 787, 777 against whistleblower charges April 17, 2024

- Dissecting Boeing CEO’s statement next new airplane will cost $50bn April 15, 2024

- Bjorn’s Corner: New engine development. Part 3. Propulsive efficiency April 12, 2024

Bjorn’s Corner: The challenges of Hydrogen. Part 15. Hydrogen cost

By Bjorn Fehrm

November 13, 2020, ©. Leeham News: In our series on hydrogen as an energy store for airliners, we now look at the cost of hydrogen.

The current cost-efficient production is predominantly by reforming natural gas, meaning it’s a process that involves carbons. Hydrogen as an energy transporter then makes no sense as the point is to de-carbonize our energy supply.

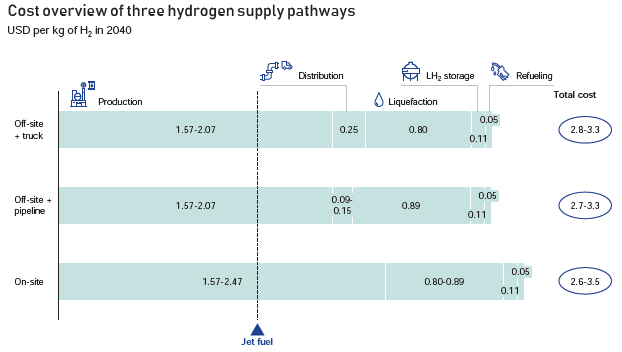

Figure 1. Cost of Hydrogen by 2040 as projected by the EU study. Source: EU.

Hydrogen production cost

When we talk about hydrogen production and its cost, we must separate the short-term and long-term goals.

Short term, we can accept that hydrogen comes from carbon fuels to build-up the eco-system. The whole system needs bootstrapping with adequate access to reasonably priced hydrogen.

The longer-term hydrogen production chain must transfer to non-carbon sources (or natural gas with carbon capture). Such investments are happening. The latest two weeks ago, when the Norwegian company Nel signed up to deliver 40-50MW of green hydrogen, produced through electrolysis from hydropower, to steel production in Norway. The present carbon-based energy for the steel plant emits 100,000 tonnes CO2 per year. The switch to green hydrogen energy will reduce this by 60%.

The most recent study on hydrogen production cost is the EU study; Hydrogen-powered aviation. Hydrogen produced in the quantities required for a green conversion of the transport industry, including aviation, would cost around $3 per kg by 2040, Figure 1.

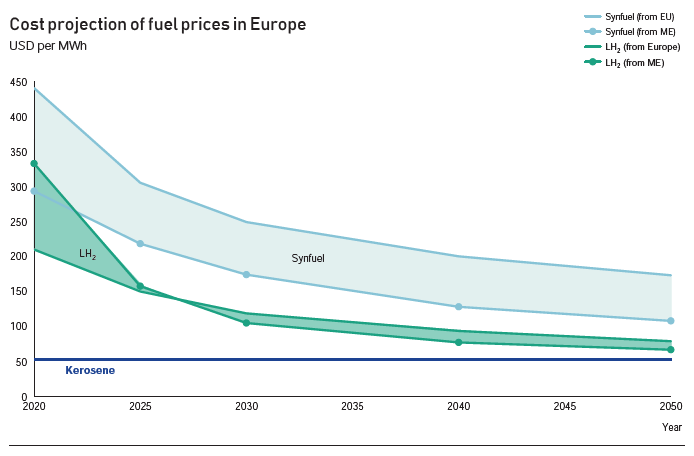

The equivalent energy cost for Jet-A1 would be around $2 if the prices stay flat from today. Alternatives like synfuels would cost more than $4.

Figure 2 shows the long term evolution of fuel prices as projected by the EU study. Observe it’s per MWh, thus per unit of energy.

Figure 2. Long term development of fuel prices as projected by the EU study. Source: EU.

The projection builds on the continuation of today’s low fossil fuel prices. It’s then quite an achievement that sustainable energy production can come within 30-50% of the production costs of something that relies on Sun energy capture in nature over the last million years, now pumped up and burned off in a non-sustainable process.

The different production methods for green hydrogen needs development and built to scale to get to the above figures. But the change has started. The Nel electrolysis process referenced above will be more efficient than today’s processes. And it uses renewable hydropower as the energy source.

These considerations only really start to apply once a country has made a 100% transition to “green”energy for its other requirements — such as industry, rail transport and home heating. If a country still has a mix of “green” and “grey” energy, then any “green” capacity diverted into producing H2 by electrolysis is going to be at the expense of another “grey” sector: in other words, you have to choose whether carbon is going to be produced by aviation or by a fuel-burning generating station on the ground. Using excess power (e.g. on windy nights) is somewhat illusory, because grid managers fret about windstill nights, and would prefer to burn hydrogen buffers to cope with those situations.

Most countries in the world are nowhere near 100% green energy production.

Even now, when the renewable energy is at 15%, in some places they need to stop the windmills at night due over capacity.

If you produce H2 with that power, instead of stopping the production, you have your H2 for windstill nights and probably more

That 15% is increasing and the problem is getting bigger

Yeah, it’s certainly worth a try. If the grid managers can appease their worries, then let it roll and see how it pans out.

There seems to be some agreement that renewable grids need lots of excess capacity to cope with calm & cloudy conditions. Hence the falling hydrogen prices in the graphs. Battery storage is miniscule compared to thermal power. That unavoidable excess is the big driver of the H push. The energy can be converted or wasted, & as batteries won’t work for a lot of thing, this looks like the best way forward.

You are right, in fact, 85% of the worldwide energy supply is carbon-based as described in last week’s Corner. And we all agree that air transport is perhaps the last area you should force to leave carbon-based fuels. Other areas have a technologically easier change.

But in the public eye, air traffic is the most visible and debated consumer of carbon-based energy and there must be a Lighthouse project to show the way to a more sustainable situation, or we are eternally kicking the can down the road for our children to handle.

Maybe the current carbon problem will precipitate a re-acceptance of nuclear power: after all, with nuclear power you only have the (remote) future *possibility* of disaster, whereas with carbon-based power you have the (very real) current *guarantee* of disaster. Fukushima only happened because some idiot placed diesel backup generators in a location where they could be flooded: without that shortfall, there would have been no meltdown. If you force carbon-based producers to capture their CO2 and store it underground, then it’s not that different to storing nuclear waste underground.

With nuclear, there would be more options to switch to non-carbon energy, less of a headache for grid managers, and more electricity for H2 generation.

Poor Greenpeace: before they could just rally against nuclear power, but now they have to choose between the lesser of two evils.

Bryce, nuclear power is just not competitive. Even without calculating the unfathomable cost for “safe” storage of nuclear waste. Building a nuclear plant has become such a burden that even France all but come to a full stop and is now heavily investing in wind and solar energy.

Until today there is not a single “safe” final disposal site on this planet. And if you busy yourself a little with geology you will soon discover that such a “safe” storage is in fact near impossible to find.

So no, this is not an option at all.

On the other hand if we’d put a stopper on all the lobbyist of the highest profitable companies this world has ever seen (oil and gas producers) a decade or two earlier we would not be in such a dire situation that we have to do everything at the same time to avoid a complete climate crash.

Sounds like a page taken directly from a Greenpeace propaganda brochure.

The reality on the ground is somewhat different:

https://www.world-nuclear.org/information-library/current-and-future-generation/plans-for-new-reactors-worldwide.aspx

I’m fighting nuclear power all my life, as I grew up near the place where they originally meant to develop a nuclear deposit in Germany. (Gorleben). When I was a student I looked into the whole topic really closely and figured out that in the long run can’t compete with wind and sun for the cost of electricity.

For your information, I have never been a member of Greenpeace, but of Die Grünen (the German green party) pretty much all my life.

Propaganda is a word we use mostly in context to the Nazis in Germany, and I don’t think it is proper to use it in context with Greenpeace. Besides, the link that you posted is referring to the website of the “propaganda machine” of the worlds nuclear power companies. Nobody should expect them to provide the “reality on the ground”.

I have studied their website a bit and tried to find some information about final deposits but couldn’t find anything. Maybe you can find that for me?

They also don’t seem to be very interested in economics, so for a quick overview we can take a quick look at wikipedia: https://en.wikipedia.org/wiki/Cost_of_electricity_by_source

I think these two reasons (cost and deposits) suffice to conclude that Nuclear energy has no future, especially as the cost for solar and wind energy keep coming down while those for nuclear keep going up.

@Gundolf

It’s fantastic for you that you’ve developed all these personal insights…well done! However, unfortunately for you, not everybody shares them.

I live within 120km of 3 nuclear power plants and I have zero problems with that.

Maybe you should write to the governments listed in the overview article that I sent you and tell them that they’re naughty boys! Get back to us and tell us how they replied.

Meanwhile, back in the real world: since grid managers still need solutions for dull days and windstill nights, the nuclear discussion won’t be going away any time soon.

I have been living 50 km away from the nearest nuclear power plant and didn’t have a problem with that either. But when they planed to put highly radioactive waste into a salt dome in Northern Germany (Gorleben, you may want to google that) that triggered massive protest for good reason. Decades later the authorities finally conceded that a salt dome is indeed not a safe place to deposit radioactive waste long term. Now we are searching for a deposit some place in Germany and guess what – nobody want’s it in their neighborhood. If you let me know where you live, maybe we can put in a request in to store it right there? I’m sure the people in your area would love to have it.

Not sure if you have noticed that not only China is investing heavily in solar and wind energy, but also pretty much all the other countries on the list. You will see that in the coming years more and more nuclear power plants will be closed and planed ones be scrapped. The only real reason to run nuclear power plants, and has been from the start, was to produce material for nuclear weapons. Skip that and nuclear power loses all charm.

Of course you need reserve power for dark and windless days, but nuclear power is not useful for that purpose at all, as it is not flexible in its output. Water, biogas, hydrogen is and of course batteries are. Batteries as in houses, cars and specific battery farms like the one Tesla built in Australia: https://www.popularmechanics.com/science/a31350880/elon-musk-battery-farm/

Regrading economics you apparently have nothing to share, so I guess that is settled.

It appears that not every government is put off by the allegation that the economics of nuclear power don’t add up; after all, what price can you put on being able to maintain a reliable supply? And what price do you attach to CO2 capture and storage?

A parliamentary majority in NL wants to build extra (thorium) nuclear power plants, for exactly the reasons that I set out above. The article is in Dutch.

https://www.msn.com/nl-nl/nieuws/Binnenland/vvd-en-cda-willen-serieus-onderzoek-naar-kernenergie/ar-BB196DIn

They will do research into things they already know which is it is to expensive. But political useful.

You are right in that the used nuclear fuel can be remanufactured to new fuel many times. Still todays reactors might be too expensive to build meeting all requirements, just look at the latest Finnish reactor Olkiluoto 3 built by Areva, still new designs are worked on and might be safer and much cheaper to operate. The competition will be tough as the +10MW windmills will come inte serial production and reduce in price as volume shoots up.

Windmill farms need a lot more space than nuclear plants.

Singapore, for example, could easily build a nuclear plant for its energy needs, but has nowhere near enough room for a sufficient number of windmills. Offshore also isn’t an option due to the busy shipping lanes all around the state.

And besides: nuclear plants keep producing output on windstill days/nights, whereas windmill farms don’t.

Singapore is special. Only large independent city state that is not completely financially dependent on oil. All other countries are big enough for a wind/solar network or have a population to small for a nuclear power plant

Nuclear is so much more expensive that a combination of solar/wind/daily storage/overbuild/few days of closed business is cheaper

There isn’t enough room in The Netherlands either.

There may be enough geometric area, but people in a crowded country aren’t willing to sacrifice the little bit of nature that they have and turn it into a sea of windmills.

Solar panels are becoming more ubiquitous on buildings…but they don’t generate electricity at night, and generate relatively little electricity in winter.

Same story for Belgium, Hong Kong, New York City…you name it.

Bryce

A) You should not look at it from the Dutch level but the EU

B) A large part of the North Sea is Dutch and windy

HK & NYC are cities, not countries and they are already dependent on their country for water so why not electricity

@ Char

The seas around NL contain some of the busiest shipping lanes on the planet…good luck with that. A few have been built in quieter maritime areas, but limits are now approaching. The country is still at less than 20% green power.

Also, people in rural areas are not particularly enthusiastic about having their landscape filled with windmills for the purpose of providing cities with power — either intranationally or internationally.

And the consistent elephant in the room with regard to wind power: where does the power come from on windstill days? Grid managers don’t like processes that they can’t turn up and down with a knob.

@bryce

People who live in exurb places don’t like windmills. In more rural places they are more liked because they bring in money. And sea has still a lot of potential. Only a relative small part is used

Bryce, you have obviously never been to The Netherlands. Besides, as Char commented correctly, you have to look at energy production and distribution at least on a EU scale, as we are used to since the start of the coal and oil age.

If you look at uranium, oil, coal and gas, the Netherlands depend 100% on imports. With solar and wind energy they can become fully or at least mostly independent. What’s wrong with that?

@Gundolf

I actually live in The Netherlands!

I’ll repeat the argument that I already stated above, but that you ignored because it simply doesn’t fit your agenda: although there may be enough geometric area in the Netherlands to fill it with windmills, people don’t want that type of landscape pollution in the limited bit of countryside that is available here. Period. So, although windmills have been placed in various windy locations near the coast, resistance to placing them elsewhere is fierce.

If other countries/regions in Europe want to fill up their landscape with 150 meter giants, and export the electricity to NL, then off they go!

Bryce, I see you prefer chemical, nuclear or otherwise pollution over visual pollution. Well I don’t and I believe you will be hard put to explain you point of view some day to your grandchildren.

I see that there is only one nuclear power plant in The Netherlands, which supplies 4% of the countries electric energy. There is no long term deposit for nuclear waste, nor are there any plans to build one.

Wind power in The Netherlands is now at 19%, with plans to expand this to over 30% over the next couple years. There are no plans for a new nuclear power plant. Seems like the government in The Netherlands it quite up to date.

Hi Bjorn Fehrm,

About Figure1:

1. Truck transportation: I’ll ignore that option, because it will be irrelevant, might be, but for some small airports.

2. On-site production: It will very unlikely to happen, I would rather say it will never happen, because it will be too expensive; the long story short: only the cost of power transmission, transportation and administration will be $40-$85/MWh (very much dependent on the transmission distance to the nearest power station). Let’s assume it 5c/kWh in average, even if the electricity production cost is for free.

3. H2 Pipeline: One of the most typical feature of the hydrogen economy will be developing and after that established hydrogen grids with industrial, commercial and even residential connections and so airports definitely connected to it. In short- the corporate price of the hydrogen will be based mainly on LCOH (production cost), hydrogen purchase agreement (HPA) cost and pipeline transportation cost. It finally will end-up at about $2/kg at the main input pipeline valves of the airport. (Forget about all other predictions!)

– The price of the liquefaction is not fixed in dollar terms ($0.8), it is mainly a function of the electricity price and the energy consumption is currently about 10.25kWh/kg of H2, which may decrease slightly when technology improves. Airports are industrial consumers, they are getting cheap electricity, but it is unlikely to be less than 9-10c/kWh ever. So another option would be producing electricity from the available pipeline H2 by Fuel Cell Power Station (FCPS). Each 1kg of H2 can easily produce about 25kWh electricity plus heat to supply some airports needs. That makes 8c/kWh autonomous production. So, for 10.25kWh/kg for liquefaction, it will result in $0.82 additional cost so far for OPEX : $2 + $0.82 = $2.82/kg. Add some CAPEX induced costs and one can easily end up to $3.5/kg. This is not bad at all!

It must be mentioned that the jet fuel prices could be $0.5/l now, but that does not include the environmental costs (CO2 etc). By the way the same applies to the ship fuels. That privilege will disappear the moment the first ePlanes emerge, so the fuel cost can easily go up to $1.5 – $1.6/l, which will make it much more expensive than H2. European airliners will be the first to ban flights to destinations, where green H2 is not available and will require certificate (declaration) of origins for that.

All pricings are normalized for 2030.

Just in the beginning of the message above I posted:

” the cost of power transmission, transportation and administration”

Please read as ” the cost of power transmission, DISTRIBUTION and administration”

Sorry!

I did read that you can mix natural gas and hydrogen i natural gas pipes and filter out hydrogen where you need it on the grid, still need some development and trails, still it makes H2 distribution to airports easier.

Hi Björn,

A fellow Swede here with a question about the risks with large scale hydrogen production. Since it is the lightest element in the universe, is there not a risk that leaking hydrogen escapes the athmosphere and disappears out into the universe?

Even if it would take a VERY long time I’m not sure I like the idea of that since it would also deplete our water supply in the long run.

Seems to me hydrogen might be the most non-renewable resource there is… but I am looking forward to hearing your insights on the subject!

The earth’s atmosphere contains hydrogen gas, though a tiny fraction. As this doesn’t disappear into space I don’t think leaks will.

It does disappear into space.

https://en.wikipedia.org/wiki/Atmospheric_escape

Three factors strongly contribute to the relative importance of Jeans escape: mass of the molecule, escape velocity of the planet, and heating of the upper atmosphere by radiation from the parent star. Heavier molecules are less likely to escape because they move slower than lighter molecules at the same temperature. This is why hydrogen escapes from an atmosphere more easily than carbon dioxide. Second, a planet with a larger mass tends to have more gravity, so the escape velocity tends to be greater, and fewer particles will gain the energy required to escape. This is why the gas giant planets still retain significant amounts of hydrogen, which escape more readily from Earth’s atmosphere.

Actually you’re correct that hydrogen does escape the atmosphere at a far larger rate than heavier gases. But it also reacts in the atmosphere with hydroxyl ions. So together, these mechanisms account for low hydrogen concentrations.

But the amount of fugitive hydrogen that surely will leak from a hydrogen economy, is still only a small percentage of the capacity of the atmosphere to handle/lose it. Thus it will not accumulate as fugitive carbon products do. And the loss is miniscule compared to the total amount we have available in water. So no worries there.

Thanks for your reply, sounds good but are you sure?

Just thinking that we managed to burn enough fossils in just ~150 years to negatively impact the environment. What will happen over the long run if we deploy H2 as a large scale energy solution?

I do not know myself, but it feels like a risk we might want to assess properly.

Carbon fuel consumption creates very stable carbon byproducts which mix easily with the atmosphere (similar density and gaseous properties) and require significant energy input to disassociate back into carbon and oxygen.

Nature has evolved a complex chain mechanism to retrieve the carbon via photosynthesis, using solar energy. It’s very inefficient but occurs over a huge surface area of the earth, so has sufficient capacity to balance the natural carbon emissions of living organisms.

We have greatly overrun that natural capacity with fossil fuels, thus the present buildup and effect on climate. The carbon cycle is heavily weighted to production at present.

For hydrogen production from water, there is no natural cycle or balance. Hydrogen production either returns to water (vast majority) or it escapes the atmosphere (a small percentage). So there is not the same risk of an unbalanced cycle.

Another way to view it is that for the carbon cycle, the carbon atmospheric products represent the lowest energy state and most stable forms. Similarly for hydrogen, water represents the lowest energy state and most stable form.

Thus with fossil fuels, the earth-system naturally settles on carbon atmospheric products and water as the preferred, stable outcomes. For hydrogen fuels, we have only water as the preferred, stable outcome.

This is also why hydrogen is sometimes viewed as a carrier of energy, rather than a source, We invest energy in water to make hydrogen, then extract it again to return the hydrogen to the water state.

Another perspective is in terms of hydrogen packaging. For fossil fuels, the packaging is done with carbon atoms. The handling properties of that packaging are highly attractive, which is why we use them. But the downside is the stable carbon products left over after the hydrogen has returned to the stable water state.

We do get more energy out of the carbon reaction, in addition to the base hydrogen reaction, but the cost is the buildup of carbon products. That cost is becoming untenable. The suitcase is very nice, but we are stuck with an increasingly catastrophic accumulation of suitcases afterwards.

There are other packaging options for hydrogen, such as with nitrogen atoms (ammonia) instead of carbon. But those mainly substitute different forms of the same leftover product problem. And none have the desirable handling characteristics of carbon packaging.

Since the carbon packaging is attractive, another solution is to artificially create or foster that packaging (synfuels or biofuels) using atmospheric carbon. But that process requires our energy investment, which has already been invested for us by the sun in fossil fuels. This approach is favored by some as an alternative to hydrogen fuels. It essentially attempts to recycle the suitcases.

With pure hydrogen (no packaging), we again have to make an energy investment, and the handling properties are far from ideal, but we get away from the byproduct issue altogether (no suitcases).

So we come back to fossil fuels as being the easiest, cheapest and most convenient source of energy, which has allowed our technological society to develop. But now we have to use that technology to move on to other sources, or risk deterioration of our own habitat (overwhelmed by the suitcases).

Rob –

I think you’ve missed HPA’s point.

Hi Rob,

Thanks for taking the time to write that lengthy explanation, I understand better now!

Where does the steel come from now?

Following the entire world mfg system, I can note that Doosan Moxy (Norway) makes an articulated dump truck in Norway.

If your steel supply is no longer local, then you loose an industry (which includes Scania engines from Sweden)

I would fight tooth and nail to keep a US mfg of equipment. Good jobs, supply chain for all the fiddly bits and pieces that go into a ADT. World class support of a good engine mfg next door. High tech transmission and drive train

What does an Optic cost a country?

In the future it might be the software that is the big value in trucks and heavy machinery that get more and more automated, the structure is then only a fraction of the total value.

Just the rear view mirrors might soon 1000’s of lines of code.

I belive Scania makes its engines in Sweden in a new foundary in Sodertalje as well as its gearboxes also now used by MAN. It will be similar to smartphones where the software is the major value.

Still a sound structures design reduces the need for massive amounts of software that try to compensate for a poor structure.

Its an interesing point that I have not seen covered, how much of a vehicle vlaue is software.

I have coin flip mentality, its part of the package or not. At this point impossible to separate (though you might come up with rough value split)

That said, the best software in the world does not overcome a bad design and build.

It has to work right for software to do its end and then it has to continue to stay running or the entire cost is broke down.

Electronics into off road was a follower for a reason. You had to get not just the processor and sensors robust, the connectors had to be far more robust to survive to transmit data.

I worked with sensors that you could not wire nut in a clean environment – as best I could come up with the joint oxidized and you got bizzare readings. For some reason a crimp worked forever (not a sealed crimp)

A while back we found out that VW used solder connections under the carpet on our car. Random werid things for 5 years running were explained (yes, they got corroded).

But back to the point, Hydro allows a viable eluaminu or steel smelt operation and you change to to H2 and then what happens to the steel rpoducion?

If you are lucky, they use a carbon fuel to keep going (in as far as local jobs go)

If not, Doosan looks at ti and says, ok, we are priced out of the market, we are going to make them in South Korea now (and South Korea uses what for energy?)

You don’t disrupt system without consequences

It is (a very reasonable) assumption that steel made with H2 will have fewer contaminants like S than cokes made steel so a first factory will not have a problem selling its product. Making it will on the other hand will be hard like most things attempted for the first time. That is why making iron with H2 has not been done yet. It is not that it is expected that the price is higher but that it costs billions to build the first factory of which success is not certain. Making extreme high quality steel with H2 is probably much easier than with cokes and the easy of a process is often reflected in price.

But the first factory has only a 50/50 change of being an operation success but it cost a few hundred million to build one. That is why it hasn’t been tried before.

Also most iron made in mature markets like the EU isn’t made virgin but by melting down scrap metal.

“The equivalent energy cost for Jet-A1 would be around $2 if the prices stay flat from today. Alternatives like synfuels would cost more than $4.”

Is the price of kerosene assumed to stay flat or the price of a barrel of oil? I ask this because at the moment jet fuel is a by-product of refining oil which does not need cracking etc.to supply demand . But in 2040 the demand for gasoline or diesel will have crashed so i expect that kerosene will need a high price in relation to the raw oil price to pay for the cracking etc. it will need to supply demand.

Interesting to note that, being an article about aviation, you are costing LH2. So, with the hard part included, liquidation, the cost per kwhr is quite competitive.

As an aside, given that BEVs are now produced large scale & aren’t likely to drop so much in price, while FCEVs aren’t and will, esp as platinum content is falling to the same level as an ICEV, these numbers pretty much condemn Tesla.

BEV and FCEV* are very similar with only a different source of electricity to run the car. Both have electric motors, 4 wheels, seats etc. The only difference between a BEV and a FCEV is that a FCEV has a fuel cell, a high pressure H2 tank and less battery.

*FCEV needs much more cooling so has more air-resistance so needs more energy per distance.

So now we come to how to design a FCEV.

It is an electric car and regenerative breaking is simple with an EV so you need batteries to save the electricity.

Fuel cells cost is per kwh/h so adding batteries to accelerate is cheaper that having a bigger fuel cell.

Your battery is now so big that it pays to add a plugin because mains electricity is much cheaper than H2.

But now it still pays to make the battery even larger so you can easily drive your daily commute on main electricity and with the advantage you only have to visit a H2 station if you go somewhat further.

You now have a car that will be slower to accelerate than a Prius and not because of the battery weight. To be faster than a Prius you still need to add batteries.

For BMW acceleration you need 150 miles equivalent of batteries, but do you need a fuel cell in such a car?

Problems with a FCEV:

-Use more energy, because H2 needs more energy & car is less efficient

-No H2 refueling stations because every FCEV is a plugin and the ones that do exist have a three day waiting list during the holidays because than they are only used

– High pressure fuel tank is a high pressure tank. They need an expensive check up after a relative limited number of years (i believe 15) without which the car is scrap metal (or more likely a battery conversion to city car)

-All those plugins have so little battery that everyone will recharge their car immediately so peaks in electricity demand because of FCEV and also want to recharge on days without wind unlike pure battery who can forgo a day or two of recharging.

-making a fuel cell and integrating it in a car is hard and expensive so only a few companies can do it. (is a positive for those companies and countries that can do it)

About Tesla:

BEV are still not produced on scale (getting there) or for long so the parts that make them different from FCEV (the batteries) are still going to loose a lot of their price and some of their weight. And Tesla is more a BMW with batteries. Making a fast car with fuel cells will stay a lot longer expensive, mainly because the need to use a lot of batteries, So i don’t see fuel cells as a danger for Tesla.

Firstly model 3 + Y, same car, is produced in similar numbers to ICEVs, no reason to expect prices to fall more. Car companies are expecting to produce FCEVs at similar prices to ICEVs this decade. A mk 1 Mirai with 11 thousand dollars of platinum in it only costs the same to make as a mk 1 Prius. Now the bulk of the Platinum is coming out, if production goes up, expect price parity.

Storage media have been found which can reduce pressure to under 100psi. NW uni’s recent announcement is part of a US DOE project specifying under 100bar.

A Tucson is $23 thou acc to internet, written off over 15 yrs and with capital at 5% prob comes to say 37k or 2500 pa. A model Y is $53k. Over 15 yrs let’s say $82.5k to make it a neat 5500 pa. Diff is 3k per year. H2 currently $10 kg in US, a Nexo does 100km/kg. 12000 km pa=120 kg=$1200. Unless model Y comes down to capital cost of $3500pa or about $37000 for a mainstream SUV, not a stripper model, it’s game over as soon as the infrastructure and volume exists.

EU study quoted shows H prices will keep falling, $2 kW/h looks like a reference to the whole powertrain considering current US prices get down to abt $10kg. ANU talks about $2 to $3 kg by the end of the decade and presumably that is $AU. At that point BEVs would have to be cheaper than FCEVs, probably under $20000 for an SUV, to attract buyers

In similar numbers? If you look at the last thirty years than number the 3/Y is made in is 3 orders smaller. It is also a first generation in its class for Tesla. There is still a lot of cost cutting possible in the not battery part of the car . And with the most expensive part, the battery, there is even more costs to cut.

Was the first gen Prius really sold below production cost? Mirai is clearly sold below production cost and with a 0-100 time of 9.2 sec (new one 0.4 sec faster) not really a Camry beater and definity slower than VW ID3. And not only platinum is expensive but also the high pressure tank. And the other parts are just an electric car so they will continue to go down in price in line with BEV’s.

About the Tuscon. What has the price of a Tucson to do with a future price of a low cost FCEV. We know the parts of a FCEV are the same as an BEV except for batteries and fuel cell so the minimum price if fuel cells would be free is the cost of a BEV without the cost of the batteries. Batteries in a Y is not $30k assuming the 3 is sold above the costs of its parts.

$2 kWh is like extremely expensive mains electricity. More than order more than households pay. Is ANU not that plan to make H2 from brown coal and export it to Japan for “greenish”.

Electricity is cheaper, even at $US 2 for H2 so a FCEV should be cheaper than a BEV SUV but a Dacia Spring SUV is rumored to be $20K. I don’t see how FCEV can attracted many buyers.

About the popularity of the SUV. A SUV is a sedan with some added glass and steel that sells for thousands more. Not surprising car makers push them. But an EV SUV needs not only some glass and steel but also need more batteries to get the same range because an SUV has much more air resistance. So don’t be surprised if car makers start to push sedans more.

Firstly last 30 years is irrelevant, no vehicle today has been more than ten yrs in production. The 3/Y has been around long enough to get the production right. Model S so long it’s at the end of its life.

Tesla are producing nearly 500000 annually, more than a lot or even most ICEVs, claiming the price will come down doesn’t add up, esp as lithium producers are having trouble surviving at current prices. Just been reported that Tesla is axing the cheapest Model 3 which they never wanted to build anyway. Factor in that BEVs are all sold with a $5000 subsidy, plus sold zero emission credits & there is no reason to expect the price to fall below current pricing.

I don’t think Toyota have ever admitted losing money on either the Prius or the Mirai, they only say production costs are the same at inflation adjusted pricing. 9-10 sec to 100km is normal family car, more just needs a bigger, more expensive fuel cell. Even if I owned a Ferrari (joke) I wouldn’t be taking the kids on holidays in it. It appears the pressure in the tank can be vastly reduced, probably to 100 bar looking at NWU’s work for US DOE. Not sure it will be reduced though, as tanks are so strong they are literally bullet proof. Not sure if these tanks have a limited life span, they’re carbon fibre now, not metal.

I don’t know what ANU based their figures on as there is a fight going on in Australia over exporting H from reformed gas using CCS or solar. Gov wants to use gas but industry is installing GWs of solar for H production & export. Seen recently that PV is down to 6c KW/Hr. Depends on electolizer costs, I think PV will win this as they are dropping dramatically.

As far as I know Tesla don’t quote their battery price but Bloomberg quote$156 kW hr. Add fitting+margin etc and the only sensible thing seems to be compare with another vehicle , using the Tucson example, as space behind the front seats is the same as the mod Y, gives $30k but it is obviously more, from the buyers point of view, the Y doesn’t have an expensive ICE. Makers say the price of an FCEV will be the same as an ICEV, hence the comparison.

I don’t know where $2 kW/h came from, but it is for aircraft, not cars, $2/kg seems to be accepted. US price has gone from $16 to $10 in a few years but it won’t keep dropping that quickly.

Will the $20k Duster give 500km range? As for SUVs, they are just the old stn wagon recycled. They are popular because modern sedans have a big footprint for a small usable space in order to be more efficient. EVs have exactly the same drawback. People are going to axe their government before they axe the SUV, and I think they’ll axe their government before they’ll buy an EV, unless it offers a one for one replacement, so I’m really hoping FCEVs take off

Models come and go but parts stay the same. And developing a new part is much more expensive than slightly changing an existing part. Taking 30 years is the right thing to do.

It is true that that production of this 3/Y should be as good as it gets, but the 3 needs at least a re-design or two to get into steady state. That will be 2035 or later.

Model S is not end of life but it needs a refresh. But i think you overrate of how much cars change with a model change.

500000 for a lower cost family of cars is not that much. Especially not for a model family who will experience major under the hood change when the new 3/Y will be designed. This are not Golf numbers

Lithium and the other raw materials in a battery pack are only a few hundred dollar. They are not important in the price of a car. Emission rights are only low single digits of the price of a car. Nice to have but not enough for a profitable business.

Toyota probably lost money on the first generation of Prius & Mirai, but the question is how. Is it because of design costs, production design costs or material cost. I think the material costs of the Mirai were already higher than the sale price

I like the look of the Mirai outside maybe of the mouth. It looks fast,. Is priced as a fast car. But sadly it is not a fast car. But they could add batteries. That is a cheap and easy way to make it faster. But than people will ask for a plugin and makes H2 future uncertain.

They say the price of a FCEV will be the same as an ICE but they don’t say if it will be price of a Rolls Royce or a Darcia. I’m to lazy to look it up but the size of a battery in a Tesla is high double digits. So take 100 kWh x Bloomberg price ($156) and you get a max price for a battery in a Y as $15600. FCEV model if fuel cells were free would be $15000 cheaper. That is not Tuscons $20000

A kg H2 for $2 may be accepted but i don’t see how they could make it for that price assuming. You need sub 5 cent electricity for that and free workers and free machines. And sub 5 cent electricity can be used for a lot of other profitable stuff with a known market.

Next years Spring will have a range of 200+km

Too many missing details to really answer, for example, if a battery pack costs 15,000 to produce, the manufacturer will want 15% markup minimum, , takes it to 17,250. Add transport+insurance, esp for Li batteries. 20,000. Tesla need to install it, 21,000, + Tesla mark up. 25000, plus share of transport, taxes costs etc. Easy to see $30k here, but only the manufacturer really knows. Google “Deloitte Fuel Cell report” for a more informed opinion than I can make. They see Total Ownership Costs of FCEV beating both diesel and battery for trucks and buses in all markets before 2030.

I think those prices are in the car. Tesla’s claimed prices are sub $100. And there is still a lot of expected cost reductions in the pipeline. Also the raw material costs of a battery pack is only a few hundred dollar.

Batteries for 500 miles will be a few thousand in ten years. H2 network will not be build out in ten years. But why go to a tank station, and they wont be as simple, fast or everywhere as current gas station. when you can tank your battery powered EV at home for $3000(minus price of fuel cell) more.

Yet another example of the failure of climate alarmists to integrate: https://wattsupwiththat.com/2020/11/11/the-contradictions-of-green-policies-to-limit-co2-emissions/.

Regarding Leeham’s constant push on Boeing to develop a new aircraft model, I note:

If petroleum prices remain low due to human creativity and productivity, and politics are rational (dream on Keith ;-), now conventional configurations are adequate.

But if too many voters drink the coolaid, there will be less need for any aircraft and quite different configurations will be better. Manufacturers might try to do both, at great extra expense.

737MAX, re-engine 767, and the 777X are sufficient for the first path. The benefits of infrastructure, and knowledge, are great.

For the second path, a range of options from wild to turboprops can be thought of. Hey! Airbus has a big turboprop airplane, … (Well, I can’t think of any recent designs that are large, Lockheed’s sizeable turboprop is old in structure and needs a bigger tail, C27J and Airbus 225 are not greatly different from Viking Dash 8 and ATRs. Japan’s patrol/SAR seaplane is aging and has a narrow fuselage. Maybe Russians have something. 🙂

I wonder which of the oil giants has paid for that chaotic piece of nonsense. I have really tried to make any sense of it, on the basis of all that I know and understand of European energy policies and developments, and may I ad I’m not completely stupid, but this wild collection of colorful graphs, baseless theories, allegations and plain lies is just not making ANY sense. Some people may like this kind of denial and green-bashing, but on this forum I think pretty much all readers are smarter than that.

On the subject of cleaner transport, and also wind energy:

“Sweden’s new car carrier is the world’s largest wind-powered vessel”

What an innovative concept!

https://edition.cnn.com/travel/article/oceanbird-wind-powered-car-carrier-spc-intl/index.html

NEL CEO Jon Andre Lokke just predicted green H2 at $1.5/kg (production cost) by 2025 in many parts of the world. Not everywhere, though. Others, including BNEF, have predicted this cost level by 2030. MorganStanley has predicted a few advantageous areas can achieve green H2 at competitive price with fossil produced H2 by 2022. The EU projection of $1.57-2.07/kg in 2040 seems to be a bit of an outlier at this point, but who knows. For people who understand Scandinavian language, you can watch for yourself. The cost prediction at 86 min 3 sec. https://www.regjeringen.no/no/aktuelt/toppmote-hydrogen/id2785501/

1kg H2 = 33kWh

$1.5/kg for H2

5 $cent per kWh

So if you make it from electricity than it has to cost less than 5c. If you take the optimistic 2kWh electricity for 1kWh H2 than it is 2.5 cent. That is an very cheap price for electricity without paying for the machinery to pay for the H2

Yes, that prediction may be somewhat optimistic. Most reports I’ve read are hoping for $3/kg.

The other issue is that if electricity comes down that much, it will compete directly with hydrogen, except for remote applications (aviation, naval shipping, backwoods, etc).

And it would reduce the burden of carbon capture, which will spur develop there, and possibly for synfuels as well.

So the market will evolve and costs will drop over time, but there may be competition from other technologies. Any progress is good, though, on whatever front.

Too many missing details to really answer, for example, if a battery pack costs 15,000 to produce, the manufacturer will want 15% markup minimum, , takes it to 17,250. Add transport+insurance, esp for Li batteries. 20,000. Tesla need to install it, 21,000, + Tesla mark up. 25000, plus share of transport, taxes costs etc. Easy to see $30k here, but only the manufacturer really knows. Google “Deloitte Fuel Cell report” for a more informed opinion than I can make. They see Total Ownership Costs of FCEV beating both diesel and battery for trucks and buses in all markets before 2030.