Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Boeing CEO promises company is turning around…again April 24, 2024

- Solid start for stand-alone GE Aerospace despite cuts to LEAP output April 23, 2024

- SPEEA, Boeing at impasse over safety program, union says April 23, 2024

- Better transparency needed on Boeing’s 1Q earnings call April 22, 2024

- Bjorn’s Corner: New engine development. Part 4. Propulsive efficiency April 19, 2024

HOTR: Lessors warn Airbus

By the Leeham News team

Oct. 26, 2021, © Leeham News: Two mega-lessors warned Airbus against dramatically upping production rates of the A320 family, London’s Financial Times reported Oc t. 23.

t. 23.

“[B]old plans to speed up production are unjustified given still subdued demand from airlines after the coronavirus pandemic,” The Times wrote. Airbus notified suppliers earlier this year to study going to a production rate of 70 aircraft per month by 2025. Rates might go even higher, to 75/mo, Airbus said.

“The chief executives of Avolon and AerCap, wrote to Guillaume Faury, Airbus chief executive, in recent weeks to express their concerns that the aircraft market would not support the most aggressive increases in output rates, according to four people familiar with the situation. A surge in supply of new aircraft, potentially flooding the market, could push down the value of the lessors’ existing fleets. They make their money by renting to airlines,” the paper wrote.

Warnings aren’t new

Lessor warnings and complaints about production rates are nothing new. During every major, unusual economic downtown, lessors voiced concerns over rates at Airbus and Boeing. These downturns included the two Gulf Wars, 9/11, and SARS.

Lessors make significant portions of their profits by selling relatively young aircraft from their portfolios. Residual value at the time of the sales must be high or robust to support profits. A supply imbalance can push down values—and lease rates—making profits harder to come by.

While major customers of Airbus and Boeing, lessors compete with the OEMs to place airplanes. But Christian Scherer, the chief commercial officer at Airbus, doesn’t view lessors as rivals.

“I would dispute the fact that we’re rivals with our leasing partners,” Scherer said during a press gaggle at the IATA AGM Oct. 3-5 in Boston. “We try to manage our relationship with the leasing market in a way that does not create bubbles, good or bad.”

The Times also wrote, “Industry executives said the European company was keen to take advantage of what one described as a ‘once-in-a-lifetime opportunity to crush Boeing’.”

But in a subsequent interview at IATA with LNA, before The Times article was published, Scherer maintained that demand supports production rates in the 70s and not taking advantage of Boeing’s current travails.

“If it was about market share, we’d be talking about rates that started with an eight, seriously,” Scherer said. “This is about meeting demand. I can tell you those scenarios of rates in the 70s are strictly to meet demand.”

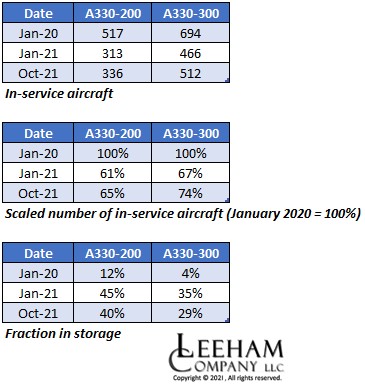

Comparing in-storage A330-200s and A330-300s

LNA has been discussing the order book weakness of small twin-aisle aircraft. There are only 59 outstanding orders in that aircraft category with Airbus and Boeing (40 787-8, 11 A330-800, and 8 A330-200). LNA estimates that half of them are iffy.

When one looks at the number of in-storage A330-200s and A330-300s, a similar story of fading popularity emerges.

The below table shows statistics about the A330-200s and A330-300s in service and storage in January 2020, January 2021, and October 2021. We only consider aircraft in commercial service, whether passenger or freight.

The number of in-service A330-300s has recovered to 74% of its pre-pandemic level, with 29% of the fleet in storage. Forty percent of the A330-200 fleet is in storage, and the number of in-service aircraft is back to 65% of the January 2020 level. The A330-300 seems to be weathering the COVID-19 pandemic better than its smaller counterpart.

I guess it’s natural. Many pundits out there laud Boeing as one member of a two part duopoly in aircraft OEM, thus justifying a substantial company value.

“Airbus can’t satisfy the worldwide demand for aircraft, by itself” is a common refrain. But that shouldn’t stop them from trying, should it?

Lessors benefit from keeping aircraft values high and to some degree wish they could set the value of the merchandise. Airbus benefits from supplying as much demand as possible. As newer, more fuel efficient models come on line – the older, less efficient aircraft that lessors own, decrease in value.

Economics is all about scarcity. Push out some 850 new aircraft a year in the NB segment and your assets aren’t so scarce anymore, are they?

Little bit of the tail, trying to wag the dog

Not easy to follow:

A330 200 Oct21 65% active and 40% in storage does it make 100%?

Hi, the 65% is, 336/517, or the number of active aircraft compared with Jan 2021. The 40% indicates the total fraction of the A330-200 fleet in storage. One is on the active fleet, the other on the total fleet.

It seems Airbus has 6500 aircraft in the backlog & airlines have huge aging A320CEO and 737NG fleets. Many leased.

I am curious:

Are there any comparative numbers around for profits/yield

between airframers, leasers and airliners ( the lessee )

Introducing the NEO back when produced a similar reaction.

as someone wrote elsewhere: quelle suprise! Water is wet 🙂

The Airbus projections look overly optimistic.

The worldwide crisis isn’t anywhere near over yet — the situation in Europe is worsening again, and the USA will follow in 6-8 weeks in accordance with the usual trend. However, pandemic relief funds for businesses have now dried up, and fuel prices are increasing. With the GOP26 coming up, the air is full of the usual aviation scapegoating — including renewed calls for heavy duties on jet fuel. Add it all up and airlines may be heading into worse headwinds than they’ve had to endure in the past few months.

Being able to use untaxed fuel ( or not ) is quite the market distortion. Rail, Road/Busses : both pay significantly more for fuel..

Taxes on automotive fuel (excise, value added taxes) are to pay for roads, bridges and tunnels. Aircraft don’t use roads or traffic lights so don’t need to pay fuel taxes. There is no distortion. Landing fees pay for the airport. Airports built in the wrong place go broke. Passengers pay taxes when they buy tickets. Airlines and their shareholders pay taxes on profit. One never taxes an input to business, one only taxes income or when consumption takes place otherwise the taxes compound.

Trains don’t pay fuel tax as far as I know though perhaps the subsidies they often receive and cheap land they are issued they should. Mining trucks don’t pay fuel tax because they don’t use roads nor do farmers tractors.

When the majority of cars on the road are electric distance driven taxes will need to be levied though perhaps electricity used for charging can be charged at a higher rate.

The current plan for aviation is to require SAF to be used and to require inefficient aircraft to use more SAF or pay for offsets. Very expensive. Voluntary at the moment but the big stick is already out and ICAO compliance will become compulsory.

People tend to do the right thing voluntarily.

@William

You have summed up the old normal perfectly

If anyone has learned anything it’s that this is no longer, to what extent is not yet clear – the process has been largely unwished and involuntary, yet the clear result of inefficiences distortions and mistaken assumptions

Fuel will be taxed, one way or another ; will get a lot more expensive – that’s probable/certain – the old arguments against to be replaced by the new in favour

The rest..a lot of the rest (OEM airplane production levels, airtravel, airfreight vs seafreight, supply chain resilience, financing) will be the result of decisions made in Asia

balloney. taxes are not purpose bound.

you work off some feelgood fake “market” theory.

“The federal government and states both impose gas taxes, with much of the revenue raised going toward fixing highways and other infrastructure projects.”

https://www.investopedia.com/gas-taxes-and-what-you-need-to-know-5118477#:~:text=Federal%20and%20state%20governments%20impose%20gas%20taxes%20to,10%20cents%20to%20nearly%2060%20cents%20a%20gallon.

Even states that divert some car fuel tax to non-infrastructure purposes, still spend most of it on infrastructure:

https://reason.org/policy-brief/how-much-gas-tax-money-states-divert-away-from-roads/

@ William’s point is perfectly valid: aviation doesn’t need point-to-point infrastructure on the ground, so there’s no justification for a tax on aviation fuel. So, instead of using the term “tax”, why not call the various proposals what they really are, i.e. a punitive levy.

@Bryce

You are essentially correct – but this way of thinking is changing

The ‘justifications’ for taxation are changing (these are mere policy decisions/excuses rather than objective laws of human conduct) – just as are the justifications for renewed or increased government spending on infrastructure and using various punitive as well as incentive financial programs to promote cleaner technologies

Put it this way – there is a lot more prestige feelgood PR and money to be made by taxing aviation fuel in line with a whole program of green techs than by not

Highway paid by gas tax is a political fantasy:

-> “The gasoline tax that bankrolls the federal Highway Trust Fund is politically untouchable, leading lawmakers and presidents of both parties to balk at raising it since 1993. But the money to pay for the nation’s growing needs for roads, bridges and transit has to come from somewhere — and the main answer has been to borrow it, adding it onto the yawning federal deficit.”

https://www.politico.com/states/florida/story/2021/06/30/drivers-used-to-pay-for-roads-washington-is-killing-that-idea-1387515

Some confusion between Australian taxes, which all go to Federal consolidated revenue, & the US where some states have fuel taxes & use them for infrastructure

Budget papers show Australian motorists will pay $49.3 billion in net fuel excise over the next four years. These papers also show that the equivalent of almost of all this, $46.8 billion, will be re-invested in land transport projects.

Australian AA. There is a GST tax as well which is general revenue but also earmarked for different purpose

@William

Fuel tax is part of general revenue, don’t let others BS you.

https://www.google.com/amp/s/amp.theguardian.com/environment/2021/oct/19/fuel-duty-losses-green-transition-new-taxes-treasury-warns

Nonsense. It’s quite complicated, depending on which taxes you include (Vat on car spares for example?, or tolls paid to private companies ) but in the UK about 20 % of taxes applicable to motorists are spent on roads and motoring infrastructure.

The biggest cause of pollution at an airport is usually the immense amount of road traffic they generate.

A nice example of the current flurry of climate-associated aviation scapegoating that’s going to cause a real headache for the industry in years to come:

“Climate change: Make people fly less, ministers told”

https://www.bbc.com/news/science-environment-59045851

It seems that hordes of people think that the climate problem will magically go away if aviation stops — isn’t it fascinating that a large population can be so delusional?

compare:

What is 40 lawyers on the bottom of the ocean?

.. A good beginning.

you have to start somewhere.

Norwegian greens want to mandate “flight quotas”

Wonderful! To ensure consistency, they should also mandate:

– Road traffic quotas;

– Shipping quotas — which will ultimately translate to import quotas on all the “stuff” imported and exported in Norway;

– Cement and steel quotas — after all, these 2 sectors are among the largest producers of CO2;

– Home heating/cooling quotas;

– Land use quotas — agriculture produces large quantities of CO2 and methane.

But, of course, those other quotas aren’t on the agenda, because Grety isn’t nagging about them.

@Uwe@Bryce

This market is nothing like stabilised – if anything greater uncertainty is the result of partial improvements which call into question other issues, such as raised here, viz green tech mandates, and the problem of domestic and international travel ‘protocols’ to use a neutral term

Economic recoveries are stymied by many of the same, plus catastrophic supply chain issues – tempting freighter conversions when – nobody knows nothing – cargo prices may subside before such can be made profitable

How long will fuel remain untaxed? When will pilots strike?

This is such a serious situation that, in the US, the relevant Secretary has been on parental leave since August, shows no sign of emerging

Airbus has to increase its production rate significantly or iffy orders will get cancelled.

Guillaume Faury has to be careful not to upset the finance people lest they avenge themselves by buying Boeing. According to one anecdote Leahy seems to have alienated money guys on more than once occasion. I somehow can’t imagine Tom Enders let things get to this.

We are approaching time when airlines will be compelled to renew fleets to new types to reduce emissions. How will that be financed? Certainly the lease finance companies shouldn’t be left holding the can.

It also occurs to me that the astronomical production rate of the A320 and B737 MAX compared to previous generations will lead to drastic reductions in production costs that will devalue any A320ceo or B737NG rapidly.

Where is the value add that lessors supply to explain their profits?

IHO they are not too far removed from mob tactics.

You don’t appreciate the various advantages of leasing rather than purchasing?

Have you never rented a car? Or a holiday home? Or a tux?

Hints: capital expenditure, disposal after use, depreciation, servicing.

for corporate the difference is in taxes and things.

leasing is direct outlay and can be deducted from profits.

buying is investment. yearly write down for n years.

Not that I disagree with you, but lessors free up capital for airlines to spend elsewhere. Banks probably don’t wanna be stuck dealing with millions of dollars of repossessed airframes sitting around, trying to find a buyer. They do so for homes, because there is usually another home buyer waiting around the corner willing to take it off their hands.

There is also a considerable amount of effort that goes into getting an aircraft(s) back from an airline, whipping it into shape (if need be, just look what happened to the Jet Airways 777 recently) and fixing it up for the next customer. Also, if your asset is sitting their, collecting dust unused, it needs to be maintained otherwise it loses value quickly.

I’m guessing that the value the lessor brings to the table, besides financing – is the ability to hold onto inventory, modify the aircraft to customer needs and essentially rent the plane to the airline.

Value add is literally how they make profit. If airlines didn’t see value they wouldn’t use them or pay fees that produce profit.

@William

Who are the ultimate customers? They determine which NB jet they want, not lessors.

The leasing companies are full of it. They just talk their playbook like clock work. Nothing unexpected here.

I doubt Faury could deliver on those production rates if he wanted. You do not have to be a real astute observer of the current supply chain environment to figure that out. As we use to say in Texas . . . “all hat, no cattle.”

Of interest in today’s news:

“Airbus hits back at engine maker as production row lingers”

“Airbus Americas Chief Executive Jeff Knittel told CNBC: “Customers are asking us to bring airplanes forward not push them out. To accommodate customers, to ensure that we have airplanes available, in our view ramping up is an important next step. The speed of that is the question, not whether we need to ramp up.””

https://finance.yahoo.com/news/airbus-hits-back-engine-maker-144542192.html

A fuller version of this story:

https://www.channelnewsasia.com/business/airbus-fends-growing-revolt-over-jet-output-plans-2270776

Negotiation tactics.

Speaking of which, isn’t one of the revenue streams for lessors, the acquisition and subsequent selling of delivery slots to needy airlines?

Let me elaborate, if you will;

*Phone buzzing*

“ABC aircraft leasing, Bob here.”

*salesman with feet up on desk, leaning back in chair*

“Oh hey Dude! How’s it going? What? Oh yah, fuel prices huh? Yah – I saw that. Yah, I’m reading an internal report right now – says that they’re going even higher. Sucks, huh? Yah, blasted oil companies, I hear ya.”

*feet still up on desk*

“Need new aircraft, huh? Which ones? Neo’s huh? Oh yah – those are tough to get, selling like hotcakes. Can’t get a slot for 5 years, eh? Damn, that’s terrible. Friggin’ Airbus. Wait a sec – did you say Neo’s? Like 321’s? Hang on a sec, lemme check something…”

*feet still up on desk, waits 30 seconds*

“Yah, I though so – we have some slots coming up, just when you need ’em. Right in your wheelhouse. No, I’m not sh!tting you. Hang on a sec, there’s a note here…”

*hasn’t moved an inch*

“Oh man, that was too good to be true, Yah, they’re spoken for. Who? Well, I can’t really tell you but….. their name rhymes with Wet Glue. Yah, those a$$holes. Yah, me too – hang on a sec! There’s another note in the file…”

*looks at his nails for 30 seconds*

“Guess what? They haven’t put a deposit down yet. When? Two days. What’s that? Yah – cash on the barrelhead, that’s what I say too. I dunno, maybe. They are paying a premium for those slots. Really? I’d have to ask the boss and see what it would take. I mean, if he gave his word to those guys, even though they are…you know, well he hates to break it.”

*stares up at ceiling*

“Listen. I’m going to tell him you’re a really good friend in need and ask him to bend over backwards to get you those slots. It may cost you some. I’m not sure that, even then, he’d do it. He’s like that. Maybe we can bail you out, here…I’m not sure.”

*checks watch*

“Okay, I’ll have some news later today – but hey, we gotta move fast if you want ’em. IF we can get ’em. I’m not promising anything. You bet. Anytime. Talk to you soon. Bye.”

*takes feet off desk to check exotic vacation spots on computer*

VERSUS

*feet back on desk*

“Hey, it’s Bob. You still needing those Neo’s?”

*removes feet and sits up straight*

“They did? New delivery slots, huh? That’s great news!”

*grits teeth*

“So you won’t be needing our slots, huh? That’s cool, those other guys are going to take them. How much? Really huh?? Well, good for you!”

*breaks pencil in two*

“No, I’m happy for you. If you’re happy, I’m happy. Of course.”

*standing now*

“You bet. Call me if you need anything else. Thanks and you too. Bye”

*slams phone down and throws coffee cup against wall*

I’m just saying…

Kinda funny, because lessors have a very clear motivation to keep the numbers of available Neos low.

Airlines like AF – KLM, IAG or United who were late to the party and didn’t order their SA replacements yet would be well paying and profitable customers if Airbus can’t serve them.

United already got the worse end with the most fav. customer clause form AA at Airbus, and had to buy 250 Max 10, due to A321neos would have not come at the price and with the production slots.

AF needs at least 60 A320neos, but Airbus doesn’t have slots – unless they can bring the rate up.

IAG with it’s brands has already a few Neos in, but need about 200 more. 100 Neos for BA, and the rest for Iberia, Vueling and Aer Lingus.

Airbus could sell Neos to AF and IAG easily, both of them are sole A320 operators, and the IAG airlines already operate Neos. If Airbus could get them some slots and a good price.

The LOI form IAG with Boeing for the Max wasn’t even worth the paper, why would they add Maxes if they already have Neos in?

Airbus has to get the rates up, to fill demand and to convert its backlog lead into financials.

About 1900 Neos are delivered, 7500 have been ordered – that’s 5600 outstanding, with a rate of 60 a month that’s close to 8 years.

AF and IAG can’t wait 8 years for new SAs.

Airbus must bring the rate up.

Airbus does not have to. Airbus is noted for managing their backlog and I don’t see them doing a big jump then drop back.

Reality is that they would have to have Boeing production numbers and their own to cut into the backlog. Call it 120 a month for round numbers.

Fleets that currently fly the NG or MAX will continue to do so. Fleets looking to shift have to assess what they can get and how soon and decide to or not to.

A lot is baked in for the next 5 years and even 10 years.

Leasers want to maintain their profits (or recover from losses).

Will a Lease company suddenly stop buying from Airbus if they make too many? If the demand is there they will buy Airbus.

And can the supply chain keep up?

Its all going to be in flux, Boeing has shot itself in the foot but has the ability to ramp up more than Airbus and deliver sooner and in numbers.

And you can’t ignore the A220 as it plays into this market and numbers and adds to Airbus overall single aisle.

Lessors are essentially squatting on delivery slots, hoping to either sell the slot/aircraft to an airline or lease the aircraft to an airline. The value of that slot goes up, when demand is high and supply remains steady.

If however, there is an increase in supply, why would an airline go through a leasing company to purchase an aircraft (who would have to add on an additional percentage to cover their costs) instead of buying direct? (all other financing things being equal)

The production bump adds another 420 jets a year. Lessors pretty much have their orders in, but to keep prices high and airlines from running directly to Airbus to get jets, they might have to place additional orders. Perhaps Airbus views lessors (privately, of course) of having too much power in the marketplace and this is a way to lessen their grip?

(Unless you’re a small guy and the purchasing power of a lessor can be a benefit to you.)

On a side note:

Agree with your A220 assessment. It looks like AF has neatly sidestepped the whole backlog issue by jumping in with the A220. They placed their order in December 2019 and less than two years later have the aircraft flying in their fleet. The latest production updates have about 4 more aircraft headed their way shortly with 2 in flight testing, one waiting for it’s first flight and another in final assembly. By 2022 all of their A318’s & 319’s will be gone. Order to complete replacement in 3 years….not bad.

I wonder if other airlines have taken note.

i don’t get your point.

YOu can’t fly A320s and NGs till the wings fall of. IAG, AF-KLM and others have a serious need for SA replacement.

Rising fuel prices doesn’t make it better, as it makes the NEO / Max case better.

AF has solved the lower end issue with the A220 order as replacement for A318/19, that doesn’t solve they have some pretty old A321s nor does it help Transavia or KLM with their SA fleet.

A Max order for later makes somewhat sense, but AF switching from A320 to Max with the A220 beyond?

That doesn’t sound sensefull for me at all, especially when there’s a french company offering the better product, and the French are as proud of their country as the americans.

AF is a natural Neo customer, and Airbus needs slots for 60 A320/21 neos for AF. And those are needed somewhat now, not in 2028.

Same is true for IAG. BA, Aer Lingus, Iberia and Vueling all already fly some Neos, but nowhere enough for replacement. They need 200 more.

No way Airbus gets them served without raising the rate.

I don’t see how a slow and expensive to manufacture A220 helps, when the A321neo is an absolute bestseller.

AIrbus is not bound to keep the rates low because existing customers wants it. That’s absurd.

AF are reportedly negotiating with Airbus for A225s with deliveries starting in 5 years. Doubt if they’ll ever take A320NEOs. If AF are negotiating A225s, so’s DL. Airbus might be in a hurry to close out some of their A320NEO backlog before customers start chasing the newer metal. Also would allow them to shift to concentrating on the A321 + directives.

I think the hangup might be the cockpit lack of commonality.

Some will prefer the all one fleet type and cross link into the Airbus Widebody.

The A321 has no real competition so they can get better pricing.

Flip is the A220 can only come on so fast. Boeing was making 787 at 14 a month (granted it was far too much).

Its going to be 5 years or better before Airbus could sub in all A220 to the A320.

Not sure how a single engine choice plays into it either. Some might not care and some might care a lot.

DL & AF already operating the A220. For other operators I guess it will depend on whether they see a large A321 fleet with a small A320 fleet in their future.

Would AB listen to its customer?

-> “Now David Neeleman addressing the ground, with a shout out to Rob Dewar, the godfather of the A220 program.

And also suggests that he’s pushing Airbus to boost range from 3400nm to 4000. That would be a huge shift in terms of missions it could serve.

https://mobile.twitter.com/WandrMe/status/1453032373164158990

What magic design process adds 600nm of range?

It means a larger fuel load, and that means higher gross weight for a plane with a very long max range as it is.

Airbus has the A319 neo for that job.

-> “The extra 600 nautical miles would allow for long-haul international flights from cities deeper into the US and open up Central Europe and South America flights from the East Coast.”

It is the combined production from Boeing and Airbus that potentially can lead to oversupply.

Pre-covid19, and pre-737 grounding, the total production was about 100 aircraft per month combined for the 737 and A320 family. Both manufacturers were about to increase production output, to a combined 120+ rate. It is not unlikely that this future rate will not be shared 50/50 between the OEM. It might be 70 per month for Airbus and 50 per month for Boeing.

Sounds about right.

Add in A220. Working up to rate 14.

Delta, Lufthansa , Korean, AF c fly it as well as the A320 types.

Delta for the right deal and availability they could slot in MAX into their NG group.

There are only 59 outstanding orders in that aircraft category with Airbus and Boeing (40 787-9, 11 A330-800, and 8 A330-200).

Wouldn’t that be 787-8?

@Rick: yes, the 788.

Rick:

Thanks, I was trying to wrap my mind around that , about to look it up.

You have to wonder if the lack of commonality with the -9/10 is a factor there.

Well that and not delivering any 787s at all these days.

It’s the MAX /CEO that the lessors and engine manufacturers are worried about, because that’s where they make all their profits.They want to force airlines to operate old machinery.

I don’t suppose this is enough to bring about the long anticipated crash of the Ryanair daily rental model?DOL did state that he was going to have to hang on to older planes for longer because he couldn’t get a decent price for MAX 10s.

As far as emissions are concerned, we’ve been through all the options and there is nothing available for at least 10 years. All the airlines can do at the moment is order MAX/NEO generation just to stand still with the growth that they have always depended on.

Off Topic

Seattle Times:

FAA flags potential safety problem in layout of controls on Boeing 757 and 767 planes

https://t.co/4LytWH3kmB?amp=1

Bit late…both models are 40 years old !

-> “We are not shipping anything today on 787,” Raytheon CEO Greg Hayes said on today’s earnings conference call, according to the Wall Street Journal.

The company supplies ~$10M in parts and equipment, such as cockpit systems, for each of the jets.

Earlier this week, Albany International (NYSE:AIN), which specializes in composite materials, cited low 787 production in forecasting just ~$10M in revenues from the program this year compared with $50M in 2019.

Boeing is increasingly expected to resume 787 deliveries early next year, later than previously anticipated, WSJ reports

https://www.google.com/amp/s/seekingalpha.com/amp/news/3758635-raytheon-stops-787-shipments-as-boeings-dreamliner-pain-spreads-to-suppliers

How many 787 have been produced but delivered now? A silent drama in the background..

One assumes that you meant NOT delivered (typo)?

According to the link below, there were 100 undelivered 787s in inventory last July. Add 5 per month since then and the current figure comes out around 115. That equates to about $18B just sitting on the ground (at typical discounts).

https://www.aviationtoday.com/2021/07/29/boeing-awaits-faa-decision-requirements-service-787s/#:~:text=There%20are%20100%20total%20787s%20currently%20in%20Boeing%27s,the%20additional%20work%20we%20shared%20earlier%20this%20month.

Ah yes, the familiar BA behavior: keep moving the finish line 😏

Remember how Muilenburg told us on a regular basis that the MAX would be certified “next month”?

And look at how poor Tim Clark is being kept in the dark w.r.t. the 777X intro.

If Airlines have money available and want to buy A321neo’s, Airbus will build them after verifying the Customer can pay the correct amount at the correct time. Of cause it will effect leasing companies that might get stuck with 737-800’s and A320ceo’s. The leasing comapnies can just complain and try to convince the banks not to lend that much Money to Airlines, just enough to pay the lease fee’s and scheduled maintenence of the Aircrafts.

In yet another manifestation of the “Cobra Effect” that is money printing we see that when large institutions can borrow money at essentially zero percent and lend it out at >7% bizarre things occur. This is essentially free money. It distorts markets. Misallocation of capital takes place.

It never ends well and because money printing now is on an unprecedented scale this time it will end extremely badly indeed.

Lessors that have taken on a lot of Airbus product during the pandemic encourage Airbus to restrict supply to other customers, thus boosting the value of their own holdings?

Well I wouldn’t be surprised…

It is our suppliers’ fault we cannot deliver enough A320.

On the subject of fleet planning, LOT’s ongoing grievances w.r.t. the 737 MAX have entered a new phase:

“LOT Polish Airlines is suing Boeing for a huge sum”

“The lawsuit was preceded by many months of conciliatory negotiations, which had not led to a satisfying conclusion for either LOT or Boeing. LOT’s spokesman, Krzysztof Moczulski, announced that the lawsuit was filed to a court in Seattle on Tuesday.

LOT CEO Rafał Milczarski explained in early October that the company has suffered severe financial losses due to the grounding of Boeing 737 MAX planes.

“We are holding and held talks with Boeing. For now, these negotiations did not bring expected results and for this reason we will use all solutions available to use to receive compensation,” Milczarski had said.

He added that LOT “could and would not give up a single thing which Boeing owed us. This is a completely natural approach, and we will put these claims forward towards Boeing.””

https://rmx.news/article/lot-polish-airlines-is-suing-boeing-for-a-huge-sum/

On the perils of the (perhaps) unintended consequences of misunderstood PR driven policies

Oil prices forecast to hit all time highs over the next decade – due to underinvestment due to green policies carbon targets – all part of the same trend as …is it called airmiles shaming?

Even if a solution is found it’ll be along traditional green class lines – the 10% rich countries will maybe work out some alternative supply, the 90% poor will be stuck with peak oil prices or no oil at all

https://oilprice.com/Energy/Crude-Oil/A-Global-Oil-Shortage-Is-Inevitable.html

Yep — tough times coming for fuel-intensive sectors such as aviation, smelting, glass agriculture, etc.

The current surge in natural gas prices in Europe is also partially due to the green transition: it’s been a relatively poor year for wind/solar output, and there is therefore more demand for the de facto fallback, i.e. natural gas.

Poor Joe Average didn’t realize that the green transition would sting him so badly in his purse…

your are living in lala land.

underinvestment ..

is mostly driven by undertaxation of corporate profits.

.. and the general dogma of “profits at all cost”.

plot investment in general and into infrastructure vs taxation.