Leeham News and Analysis

There's more to real news than a news release.

RTX Q1 2025 Earnings: GTF Talk Takes A Back Seat To Tariffs

By Chris Sloan

First quarter 2025 Earnings Report.

April 22, 2025, © Leeham News: The chorus of tariff-dominated earnings season calls continued as RTX took its turns at bat.

President and Chief Executive Christopher Calio aligned with other CEOs to demonstrate that aerospace is in sync with the presidential administration in correcting the trade deficit.

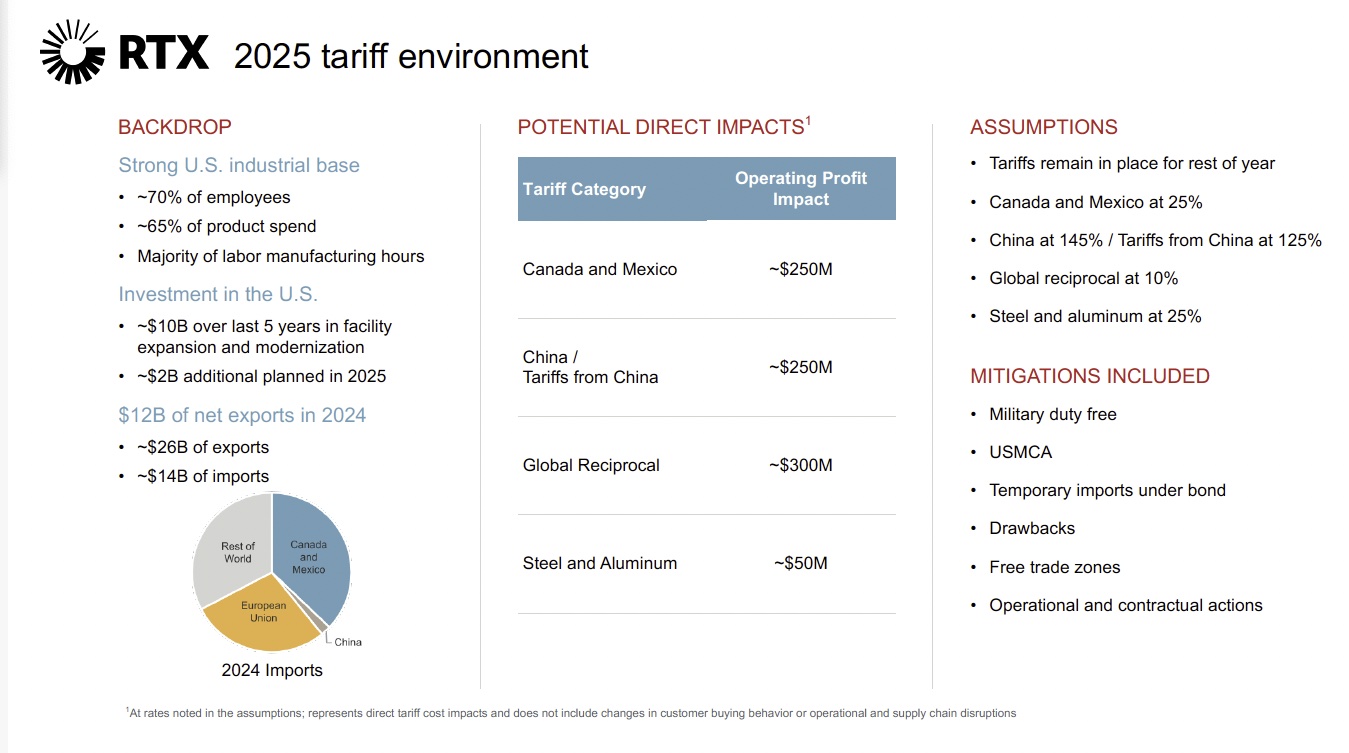

“We really believe that the aerospace and defense industry is really well positioned to meet what the administration’s north star in trade objectives are and that this industry has just been a shining example of that.” Calio cited RTX as a net exporter of goods exceeding imports by $12bn, offering a host of stats to build his case to reduce aerospace-related tariffs. “Our industrial base is largely located in the U S, including about 70% of our employees. On the supply chain side, about 65% of our product spend is with U.S. suppliers. Over the last five years, we’ve invested nearly $10 billion to enhance our domestic manufacturing footprint, with planned capabilities of $2 billion additional planned in 2025.”

RTX is not immune to tariffs

Calio warned RTX is far from immune to the wide-ranging tariffs. “Like many companies in the industry, our supply chain and customer base, we import raw materials, parts, and modules from around the world.” He warned that the tariffs would sharply crater profits by $850mn if they remained in place, flagging that not all regulatory and operational mitigation would address our tariff exposure.

Granular direct impacts of $250m from Canada and Mexico, $250m from China/Tariffs from China, $300m in global reciprocal, and $50m in steel and aluminum would begin to have a real impact in the back half of the year as inventory is liquidated.

“I’d say the Raytheon impact is very minimal – think about that as like a penny per share kind of a number – the rest of it, the residual impact, is split pretty evenly between Collins and Pratt,” suggested RTX Chief Financial Officer Neil G. Mitchill Jr.

Analyst Scott Mikus of Melius Research observed RTX’s exposure to tariffs exceeded that of competitor GE Aerospace. “Based on RTX’s assessment, it could face an $850m headwind (net of mitigation efforts) from tariffs, which equates to ~8% of segment operating profit. For context, GE embedded a $500m impact from tariffs into its guidance. Given the timing of paperwork associated with duty drawbacks, the potential impact to RTX’s 2025 cash flow could be ~20% higher than the hit on the P&L.”

A Watchful Eye on Pricing, China, Supply Chains, and Economic Slowdowns

The company was vague on whether tariff costs would be passed directly onto customers through price increases or temporary surcharges, possibly due to still delicate relationships with customers on the heels of GTF and Collins problems, but didn’t rule anything out.

“We’ve been operating in a highly inflationary environment over the last several years, so we’ve done pretty well at knowing where and how to pass along higher costs through pricing. Again, the situation is fluid. So we came into the year with a number of levers we would potentially pull if we saw things change in the marketplace to let things sort of play out,” said Calio.

With renewed concern that this latest distraction could derail the supply chain’s recovery, Calio sought to reassure investors. “We’re going to stay super tight with our supply base, making sure that we’re all working together on tariff mitigation, the movement of work, and making sure that we don’t see those disruptions. We’ve seen in the past what happens when you are herky jerky with your supply chain, like we saw in Covid. The company sought to assuage investors’ fears over China, stating that RTX has been developing multiple (material and component) sources globally since coming out of COVID-19, and that those are accelerating.

Slowing global economies are adding to a full plate of problems, yet RTX is cautiously optimistic that aircraft utilization will remain strong, supporting continued aftermarket demand. Given the backlog levels, on the OE front, they expect production of new aircraft to stay strong, with engineless, incomplete airframes still being pumped out of factories. “The demand there remains very strong, obviously, it’s a constrained environment, there’s a lot of demand for new aircraft, and we expect that to largely continue. If you think about the aftermarket, there was clearly tremendous demand for the GTS aftermarket. Expect us to be on track to continue to deliver growth there throughout the rest of the year,” said the sanguine CFO. However, they disclaimed that it closely monitors consumer sentiment as the peak summer travel season approaches.

GTF Enjoys Good News For A Change

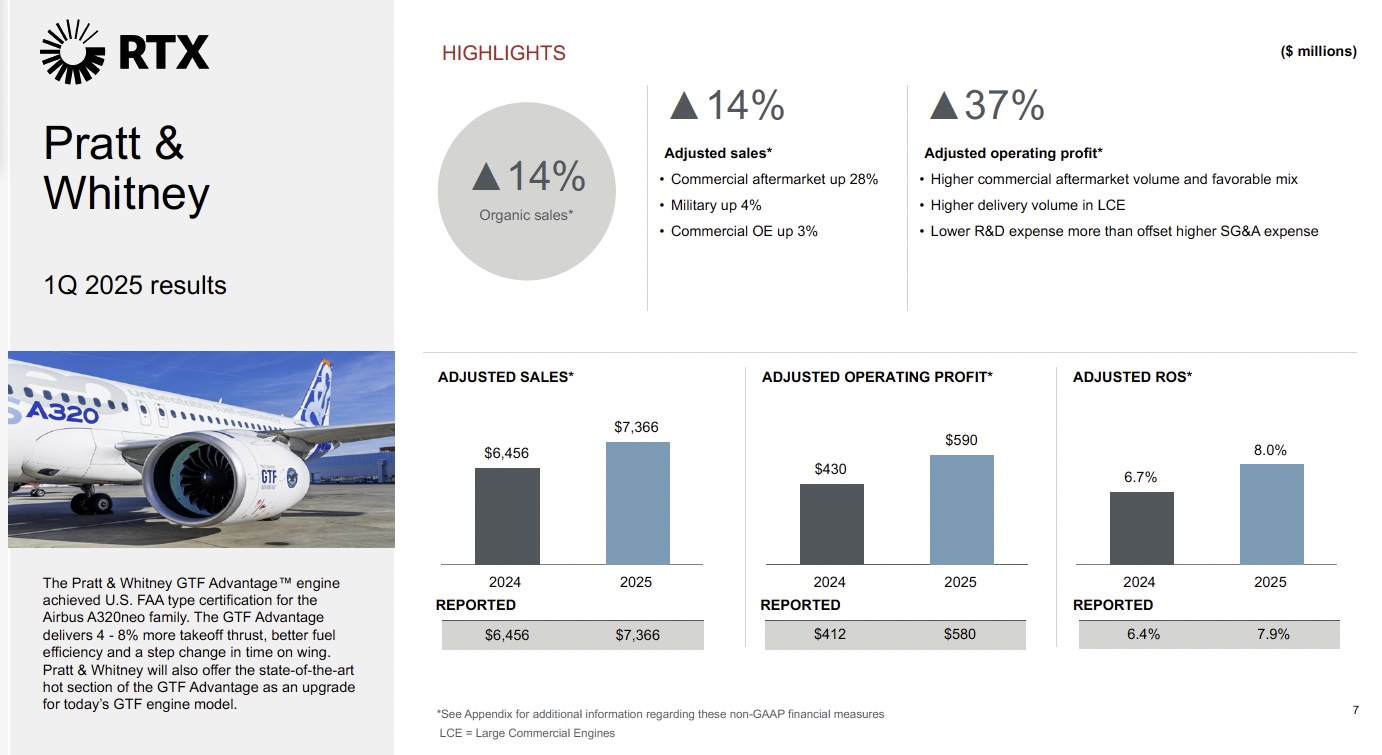

If there’s one bright side to the tariffs, it’s that investor’s attention has at least temporarily shifted from the GTF’s travails – which enjoyed a much needed spate of good news. MRO activity for the PW1100 engine surged 35% year-over-year and 14% sequentially, with the company projecting over 30% growth for the full year. Executives say the ramp-up in output is a critical factor in reducing aircraft-on-ground (AOG), which are expected to decline in the second half of 2025.

Meanwhile, the FAA has certified Pratt & Whitney’s new GTF Advantage engine—a significant milestone for the program. Drawing on a decade of operational insights from the geared turbofan platform, the Advantage engine is expected to deliver up to double the time on wing compared to current models. It will enter service with full-life maintenance plans. Initial deliveries to Airbus remain on schedule for later this year.

In addition, Pratt & Whitney is working to certify an upgrade package that will allow existing PW1100G-JM engines to receive approximately 90% to 95% of the Advantage’s durability enhancements during scheduled MRO visits.

MRO and V-2500

Pratt & Whitney remains on track to meet its 2025 outlook of approximately 800 V2500 engine shop visits, with first-quarter activity representing about 25% of the annual forecast. Shop visit inductions for the V2500 were up 7% year-over-year in Q1, and the company notes a shift toward heavier overhauls due to the aging fleet. Despite 11 retirements of V2500-powered aircraft in the first quarter, overall fleet retirements remain low. Executive emphasized that the V2500 continues to benefit from strong customer demand, especially in the narrowbody segment, and is expected to maintain consistent MRO activity in the near term—even amid potential fluctuations in broader market demand. As the AOG GTF fleet gradually returns to service and new airframes are delivered, the company anticipates a future tapering in V2500 shop visit volume, but not until further out on the horizon. P&W reports similar stability for its legacy PW2000 and PW4000 engine programs, with shop visit trends and customer demand aligning with internal forecasts.

Collins Remains Reliable

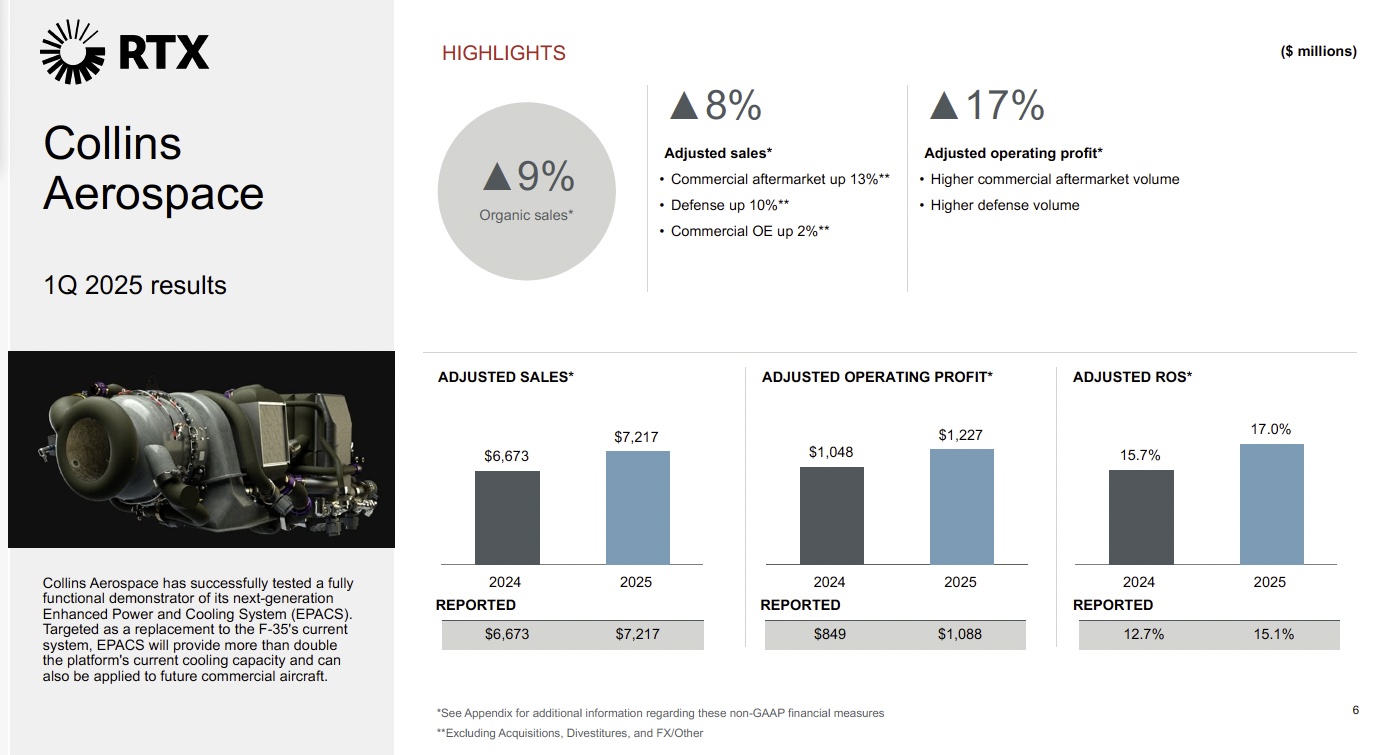

A constrained environment is counteracting any economic slowdown at the Collins division, even going into April following Liberation Day. “The airframers have strong firm backlogs and are focused on continuing the ramp right, they need to keep material flow going through their shops from the supply chain. So we don’t see any material changes there, and again, we see a ramp ahead, and we want to stay out of their way,” Calio remarked. The heat exchangers that have bedeviled Boeing 787 deliveries are a subsiding pain point. “We’re going to continue to keep a close eye on that as Boeing continues to ramp,” he added, referring to Boeing’s quest for 787 rate 10 a month.

A Solid Quarter, But What’s Next?

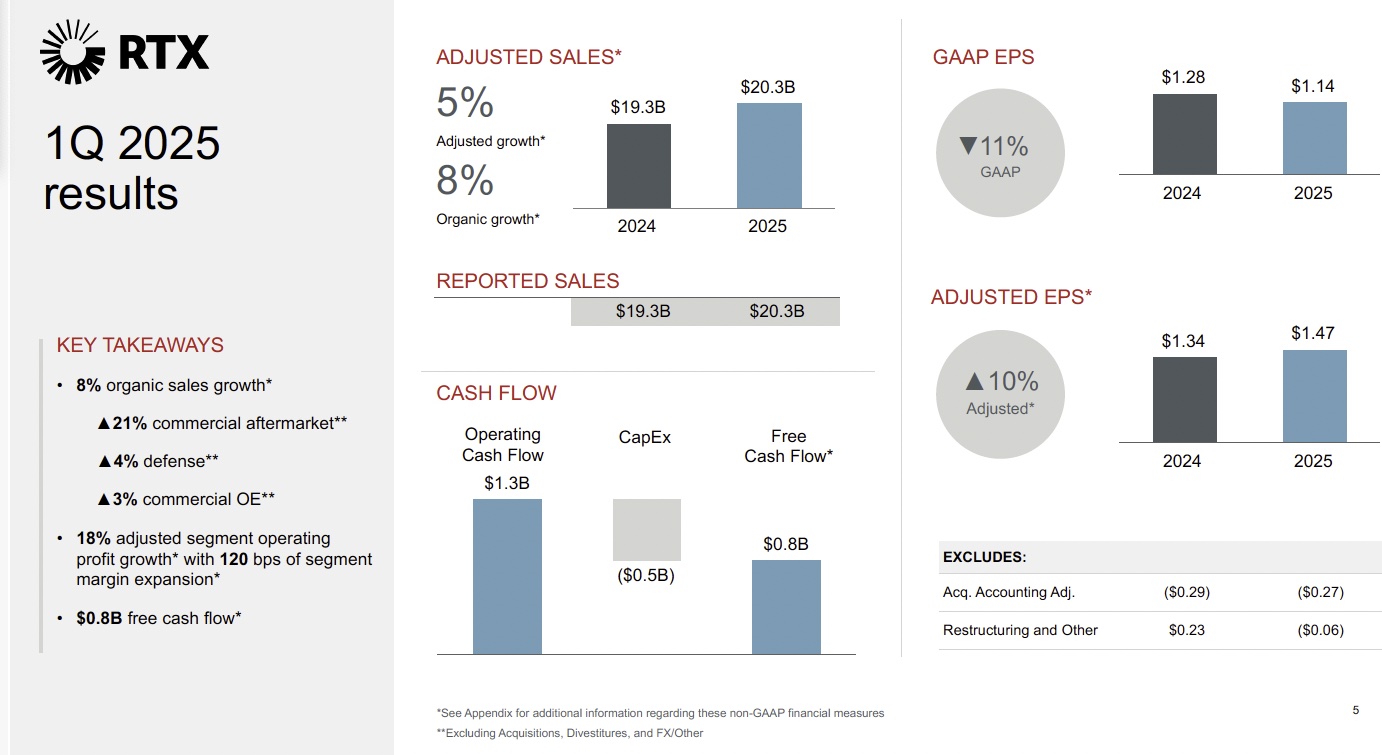

RTX reported total sales of $20.3bn, reflecting a 5% increase compared to the same period last year. Net income attributable to common shareholders was $1.5 billion, representing a 10% decline year-over-year. Pratt recorded sales of $7.37bn for the quarter—up 14% year-over-year. Operating profit for the segment rose significantly, increasing 41% to $580 million. Collins Aerospace posted $7.22bn in sales for the quarter, marking an 8% year-over-year increase. Operating profit surged 28% to $1.09bn.

In the first quarter of 2025, RTX reported sales of $20.3 billion, up 5% from the prior year, with net income of $1.5bn. Growth was driven by strong demand in its commercial aerospace segments, while overall profitability declined 10% year-over-year amid continued pressure in the defense business.

“Considering the dynamic macroenvironment, RTX had a pretty good 1Q25, RTX’s 8% core sales growth came in 2.5 points ahead of consensus and will likely rank near the top of our coverage list,”said the Melius analyst.

Unless or until the insanity quits, no one can make even educated guess, just a WAG.

The impacts are not immediate, they are 3-6 months out and when Rubio says we don’t care if you come to the US, that has a long term impact on people planning to and the flip is true, do you want to go to countries you have ticked off?

You could see anything from a 2008/Covid dump to 9/11 class impacts. Best outcome is the lunatic keeps over and saves us from ourselves though only 1.5% more voted for the clown. The rest of us are caught up in that inability to look beyond the end of their noses.