Leeham News and Analysis

There's more to real news than a news release.

Airbus predicts services will grow faster than aircraft deliveries

October 06, 2022, © Leeham News: Airbus presented their 20-year Global Services Forecast (GSF) for the world’s airliner business today. It’s a complement to the aircraft Global Market Forecast (GMF) that Airbus presented in July.

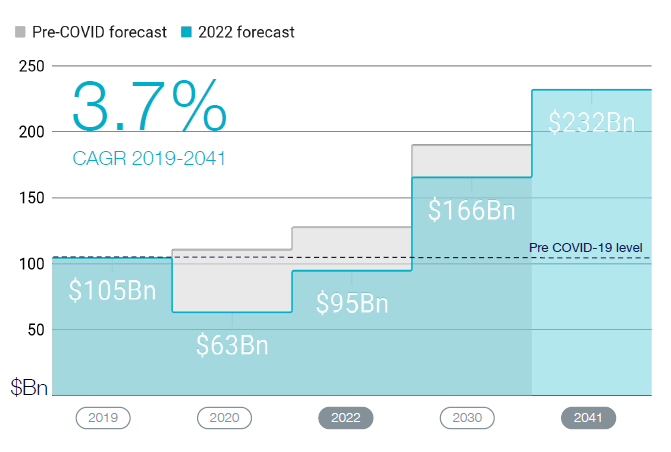

The services business for the over 100-seat air transport market grows from $105bn pre-COVID to $232bn by 2041, an increase of 221% or a 3,7% CAGR (Compound Annual Growth Rate), Figure 1.

Figure 1. The growth of services to the worldwide over 100-seat air transport market. Source: Airbus.

The Services Market grows faster than Aircraft deliveries

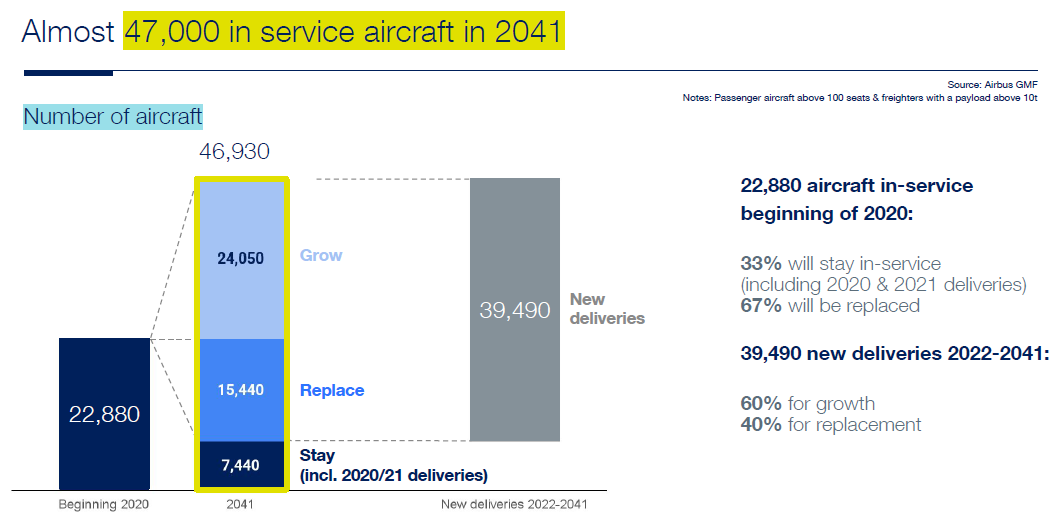

Airbus Global Services Forecast (GSF) complements the aircraft market forecast, predicting growth from 23,000 airliners flying today to 47,000 flying daily by 2041, Figure 2.

Figure 2. Airbus Global Market Forecast (GMF) for the airliner market over 100 seats. Source; Airbus.

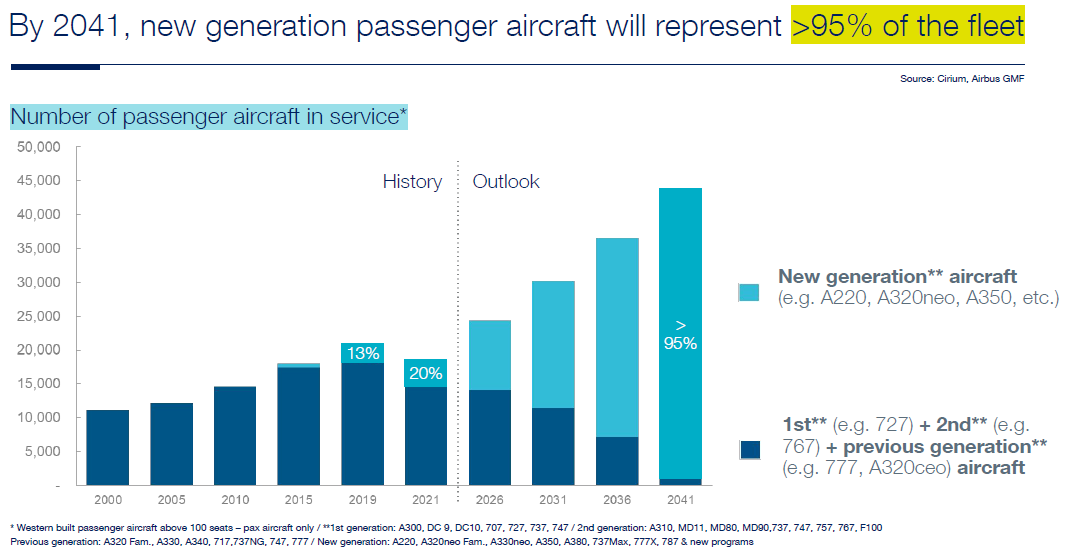

By 2041 80% of the aircraft will be single-aisle with 20% widebody. The latest generation of airliners will represent 95% of the fleet after close to 40,000 new deliveries have replaced older aircraft, Figure 3.

Figure 3. The airliner replacement curve over the next 20 years, according to GMF. Source: Airbus.

The passenger traffic (in RPKs, Revenu Passenger Kilometers) grows by 3.6% CAGR in this period, and the yearly aircraft deliveries by 3.2% CAGR. The services related to this growing passenger and cargo market are outpacing them both, with a 3.7% CAGR.

The effects of the COVID pandemic are disappearing faster than predicted, and we will be back to a regular market for services end of 2023 or early 2024. The effect of the Pandemic will not be noticeable as the market grows from 2022 to 2041.

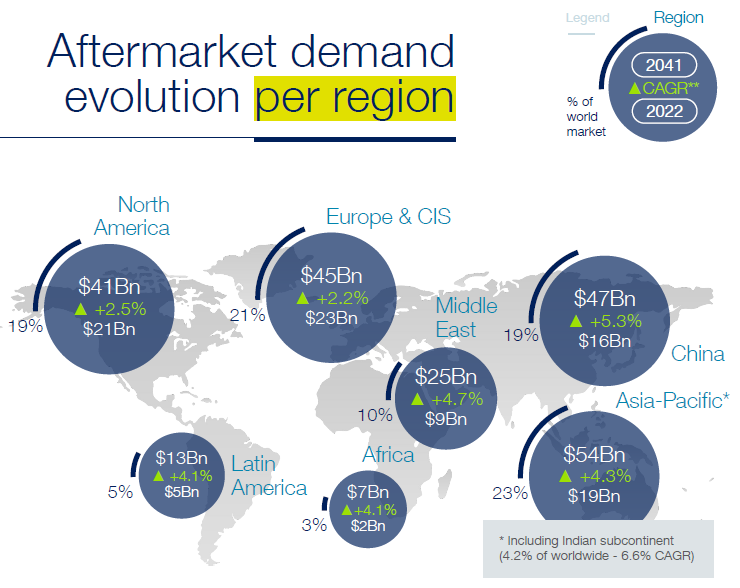

The largest services markets shift from Europe & CIS and North America to Asia-Pacific during this period, Figure 4.

Figure 4. The regional growth of the services market. Source: Airbus.

Maintenance dominates the services market

The largest part of the services market is the maintenance of aircraft and their engines, Figure 5. In fact, the order should be reversed; engine maintenance is the dominant maintenance expense for the airlines.

A growing component of the Maintain market is the disassembly and recycling of older aircraft. Airbus is working to ease this process both in the design of the aircraft and the methods to do this cleanly and to reuse up to 90% of the materials in the used aircraft. It includes refurbished spare parts that go back to the market. Today’s reuse of scrapped airliners is around 70%.

Figure 5. The three main services markets and their growth. Source: Airbus.

The Train and Operate market is under heavy stress presently as many flight, cabin, and maintenance crew members left the industry during COVID, as did other ground support personnel.

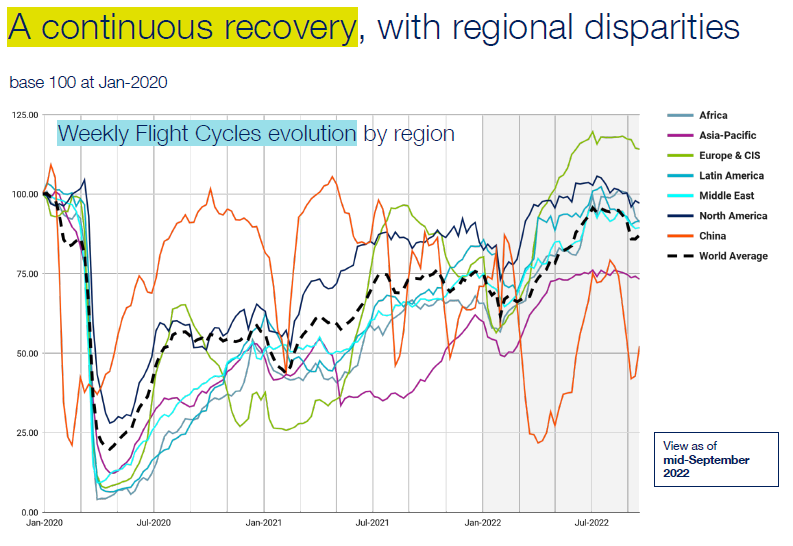

The traffic has returned faster than predicted, with the summer of 2022 breaking the pre-pandemic level for weekly flights in Europe and CIS. Figure 6.

Figure 6. Weekly flights, comparing Jan 2020 to now per region. Source: Airbus.

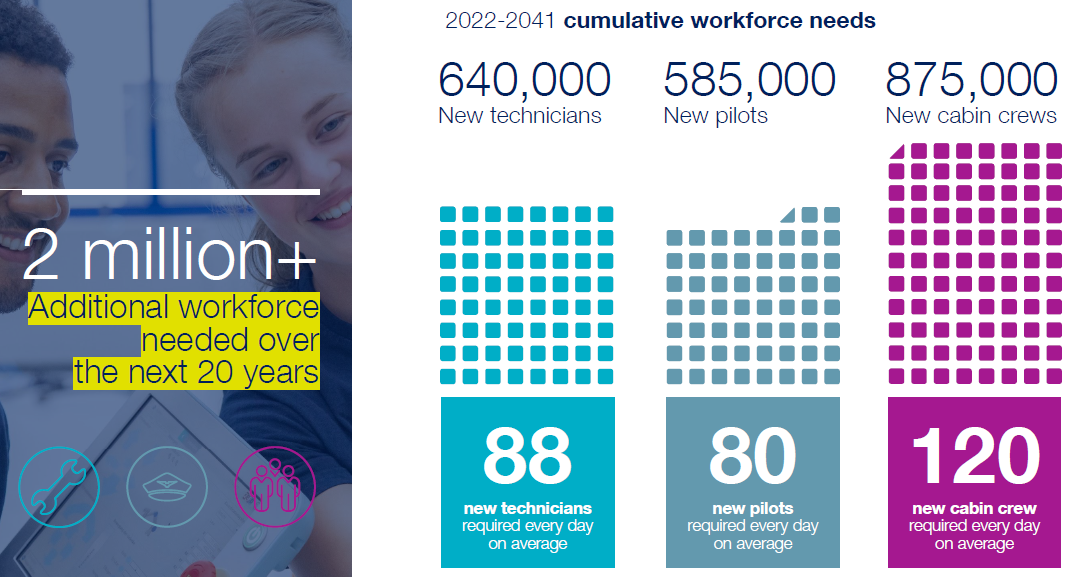

Over the 20 years, about 2m persons need to be trained for their roles in the air transport business, with almost 600,000 pilots needing training and certification as Air Transport Pilots, Figure 7. It creates a training market for 30,000 Air Transport Pilots (ATPL) per year.

Figure 7. The workforce training demand from 2022 to 2041. Source: Airbus.

In Train and Operate, the continuous improvement of the operation efficiency of airlines through smarter and more efficient flying shall gain us a further 5% reduction in CO2 emissions.

An important part of the Enhance business is the cabin refurbishments and upgrades during the 23 years of an aircraft’s life.

Examples of the types of services that will be demanded in 2041 are given in Figure 8. The 5,000+ maintenance inspections for the aircraft are only the heavy checks done about midlife for an airliner, also called D checks. The more frequent C checks, also hangar based, are not in these figures.

Figure 8. Examples of the services delivered by 2041 to support the 440,000 daily flight hours. Source; Airbus.

The 7,000+ engine checks are the workshop overhauls needed to restore the engines’ performance and replace life cycle limited parts (LLPs). The spare parts for these overhauls are the primary revenue stream in the maintenance business for the aircraft.

Having worked on the services side at Boeing for part of my career proved that Boeing’s pricing was usually too high for the airlines to sign a contract, but it depended on what the service was. One of Boeing (and Airbus) best marketing deals is the material contracts. It’s a win win for the airline operators. Managing inventory is extremely costly.

Worth noting is these individual Boeing services operate as their own separate P&L, sometimes makes it tough to meet your revenue targets when the airplane sales guys give away your business to make an airplane sale.

Another big cost center for Boeing is their AOG services worldwide, I’m sure it is for Airbus as well.

Something to clarify from this piece is that neither Boeing nor Airbus manage or accomplish engine services and overhauls, airlines make the contracts direct with the engine OEM’s or with MRO’s such as Delta Tech Ops/Lufthansa Tech to name just two big ones. They also can compete with the airframe OEM’s on a much larger reduced cost basis for anything from component services to D check overhauls.

Good points, thanks, Airdoc.

Agreed. Best source is someone that worked at the front line of whatever is being discussed and add that well written is important. .

“neither Boeing nor Airbus manage or accomplish engine services and overhauls, airlines make the contracts direct with the engine OEM’s or with MRO’s such as Delta Tech Ops/Lufthansa Tech to name just two big ones. ”

This is an interesting point.

It begs the question – why? Do AB & BA have non-compete clauses with engine makers to not step on their turf? You would think that if an airline could service engines for themselves and others, that an OEM could easily put together the talent and space to do it.

I’m sure that Pratt, GE, Rolls & others offer this service to airlines, right? I wonder how they feel about a customer like Delta encroaching on their revenue stream?

Frank:

The engine makers do have in house ops. But look at the big picture.

The engine mfgs pay high salaries. The service areas are all over the world and how many operations to overhaul do you open up? RR is the most restrictive (or tries).

At least in the US there are laws concerning propriety maint.

So, look at a major airline ops. They have line mechanics to fix those items they can on the tarmac. Ooops, engine is toast, someone has to pull it and then ship it (unless you are lucky and next door to a repair center).

So, Delta has a big repair operation and as they do it at scale, they can spread the costs over the fleet. And, hmmm, if we can overhaul engines, we can no just do our, we can bid on others.

Then comes along GE, who has to bid engine overhauls and they get undercut by Delta. Ooops, layoffs, sorry guys, we lost the contract.

In the past the engine mfgs made money on parts. Now parts last a lot longer though there are a number that are replaced on overhaul, but, sigh, overhauls periods are longer apart as well.

Not all airlines do their own hull maint, those they hire out, to, yep, lowest acceptable bidder or even the lowest.

There was a maint operation in Spain that messed up the ailerons or the spoilers (Air Astana as I recall). The pickup crew failed to run the checks despite both alerts and a check system in place.

They took off and when they went to turn it went nuts. They actually survived though it took a couple of hours as I recall to sort out some semblance of control (the Embraer was so badly stressed it was written off but the crew survived).

From the follow up, low bidder that did not understand how the rigging was supposed to be run (Embraer got dinged for non clear instructions , but no one ran the same software check nor did anyone physically look at the surfaces and, oh, you made a left turn but the opposite surface activated.

You would not see the equal issue with an engine mfg but there are lots of independent MRO that can and do charge less.

Diesel mfgs have regional non OEM businesses that adher to the mfg parts and training. $150 an hour vs my $45 an hour (no I did not get that) and I often fixed engines. There were parts makers that you could buy non OEM parts from (we did not use them as our use was extremely low as we had 4 to 12 engines depending on the job I was working)

We hired out some jobs due to the tooling needed (not worth spending $1500 for tooling when we replaced injectors once in 25 years).

So its all a balance. And as Airdoc noted, companies require areas of ops to make a profit. But your operation has to use the company resources (the Personal department) and pay a fee based on an operation that you may not even have a benefit in or from.

In my case Honeywell who had the contract at one time charged us $2500 a month and fed us so called Preventative Maint software that crashed (the manger was a computer guy, he back up his system, crashed it, figured out the bugs (reloading the stuff that worked to get his reports and our PM tasking out) and then trouble shot it for 3 other sites until they got it sorted out and then 3 months later, rinse wash and repeat.

We could have hire a local firm to do the Personal end easily but we could not. There was lots of good PM software out there. But Honeywell had an IT department that needed work so they gave us garbage.

You had to constantly fight with your own company and that cut into the work you could do.

Honeywell gave it up (dumped us) as the way they had it setup we were a loss.

@Frank

One must keep in mind that the engine OEM’s data and technical information is proprietary to them, same as this is for the airframe OEM’s. We always struggled with engine data streaming real-time via ACARS at Boeing, especially GE. RR and P&W tend to be much friendlier.

P&W invented the ‘Power by the Hour’ maintenance service, and RR has a program titled TotalCare. These programs are extremely cost beneficial to the airline customer with on wing service, technical real time data management and overhaul services. They also guarantee spare engine availability pretty much worldwide.

The MRO’s such as Delta Tech Ops offer great overhaul service but not the other attributes and that leads back to proprietary technical data.

The engine companies really are true leaders in this business.

Boeing tried to mimic this power by the hour program in a similar fashion. it wasn’t successful mainly because of pricing and the fact that Boeing couldn’t operate on an airline ops tempo and deliver as they promised they could.

@Frank

I should have added, MRO’s like Delta Tech Ops or LHT are licensed by the engine OEM’s to accomplish proprietary work. The airline customers manage the builds and what should be accomplished at the ESV (engine shop visits).

Each engine is unique on what needs to be accomplished to make it airworthy and stay on wing with ultimate reliability.

It used to be that you need around 200 engine shop visits of the same type per year for an airline shop to be constantly profitable with good agreements with the Engine OEM. Few airline shops can get enough firm contracts to hold this tempo. One problem is spare parts with constant modifications and which part can go with other parts making your engine shop spare parts stock quickly being old and with too few rotations per year. Most shops have more spare parts buyers than sellers of spare parts making the problem grow together with accounting issues as your book value is close to purchase price but market price can drop very quickly hence if you manage to sell your PRE SB spares you get cash but book a loss in your SAP R/3 system.

” MRO’s like Delta Tech Ops or LHT are licensed by the engine OEM’s to accomplish proprietary work.”

Thanks Doc.

This is what I was looking for. So the engine makers get a cut of what Delta/LHT and others do, which brings them in additional revenue. I wonder how it works when both an OEM and a 3rd party are bidding on a repair contract?

Do they try to keep prices relatively stable (which is kinda illegal) or will they cut each others’ throat?

Keep your friends close, keep your enemies even closer…

To answer your question about contract bidding. Usually it’s money talks, BS walks. In other words it’s all about pricing, which I definitely understand. (I don’t it like, but I get it) This is why so many US operators source heavy checks, repaints and modifications to central America and sometimes Asia. Cheap labor, no taxes.

But jet engine work is a whole different ballgame. Most engines are operated ETOPS, so the rework is utmost critical. Yeah some will challenge me that airframes are just as critical and this is true. But as we have a saying in the airline world, ETOPS stands for Engines Turn Or People Swim. Think about that.

In cases such as the Ethiopian 787 that recently did a severe tail strike in the Congo, that’s gonna be a repair job for Boeing AOG. There’s no MRO’s in the world that can accomplish this complex CFRP fix.

I think in Engine & Components MRO (the money makers) economies of scale are indeed existential.

The big airlines have their shops, some independents (e.g. MTU, AAR) have build up their customer bases, but OE’s still play an important role. As do lessors.

Over the last decades many aircraft engines were sold/ financed to include 10 yr maintenance deals.

To make it more complicated, most engines shops don’t have all the capabilities in house to do an engine overhaul. So they outsource to each other, OE shops, specialists in various degrees, Most players are partners, customers, service providers as well as competitors from each other..