Leeham News and Analysis

There's more to real news than a news release.

Boeing First Quarter Results: Tariffs, Return flights, $10.55bn asset sale

By Karl Sinclair

Boeing first quarter 2025 earnings report.

April 23, 2025, © Leeham News: As aircraft destined for delivery for airlines in China were turned around and returned to the US, the Boeing Company (BA) released 1Q2025 results today. Results were better than expected, with the loss lower than forecast and Free Cash Flow better than analysts forecast.

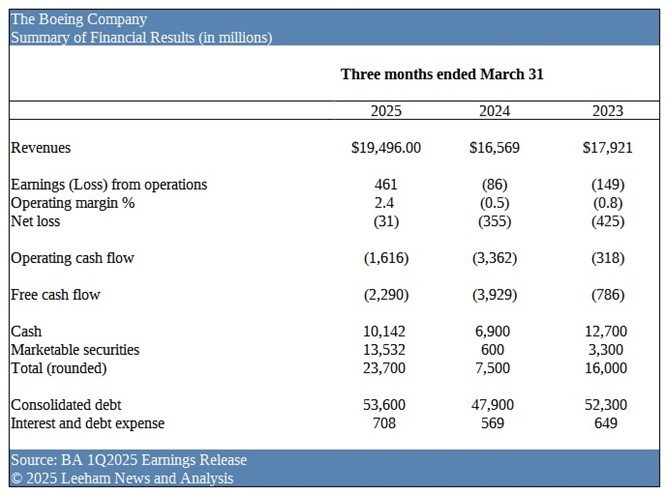

Revenue in the quarter was $19.5bn, the loss per share before charges was 49 cents and free cash flow, while negative at $2.3bn, was well below analyst projections.

Boeing ended the quarter with $23.7bn in cash and marketable securities, down from $26.3bn on Dec. 31. Debt was $53.6bn, down slightly from the end of last year. Boeing has an untapped $10bn line of credit.

The company said it still expects to return to a new production rate on the 737 MAX line of 38/mo. Production for the 787, how at 5/mo, is forecast to go to 7/mo this year. Both figures are lower than previously targeted (42/mo and 10/mo, respectively).

Yesterday, Boeing announced that it had reached a deal with Thoma Bravo – a software investment firm, to spin-off parts of the company for $10.55bn in cash. The deal includes Jeppesen, ForeFlight, AerData and OzRunways assets, and is expected to close by the end of 2025.

Planes returned from China

Two 737-8 MAX aircraft originally destined for Xiamen Airlines departed the Boeing Completion and Delivery Centre in Zhoushan, China, bound for Seattle (WA), since April 18.

While the fallout from the tariff war between the Trump Administration and the world (with an emphasis on China) have yet to fully take hold, the effects can be felt across the industry and especially in the Pacific Northwest.

The latest indications are that Donald Trump is beginning to realize the futility of tariffs and is beginning to make noises about walking them back. “They won’t be 145%, but they won’t be 0%”, he said late Tuesday, when referring to China.

Whether this is enough to placate China and restore deliveries that were halted country-wide, remains to be seen.

In its position at the top of the supply pyramid, with a customer base 80% outside of the US, Boeing faces enormous risk on both the sales and expense side of the equation.

Sale of Jeppesen

Boeing will retain some of the core digital capabilities after the sale of Jeppesen is completed but expects that some 3,900 employees will be affected in the transaction.

“This transaction is an important component of our strategy to focus on core businesses, supplement the balance sheet and prioritize the investment grade credit rating,” said Kelly Ortberg, Boeing president and chief executive officer.

Boeing had hinted in the FY2024 earnings call that it would be “trimming and pruning” the company, and since Jeppesen had been named as a target, this hardly comes as a surprise.

Company Level Results

Boeing was expecting a difficult first-half of 2025, which would level out as the year progressed. Free Cash Flow was projected to be negative, with a burn rate of between $4bn-$5bn for the year.

The company is expecting to take on an additional $4.3bn in debt, when the Spirit Aerosystems acquisition is finalized mid-year. Shareholders will get diluted to the tune of ~$4bn in the all-stock transaction.

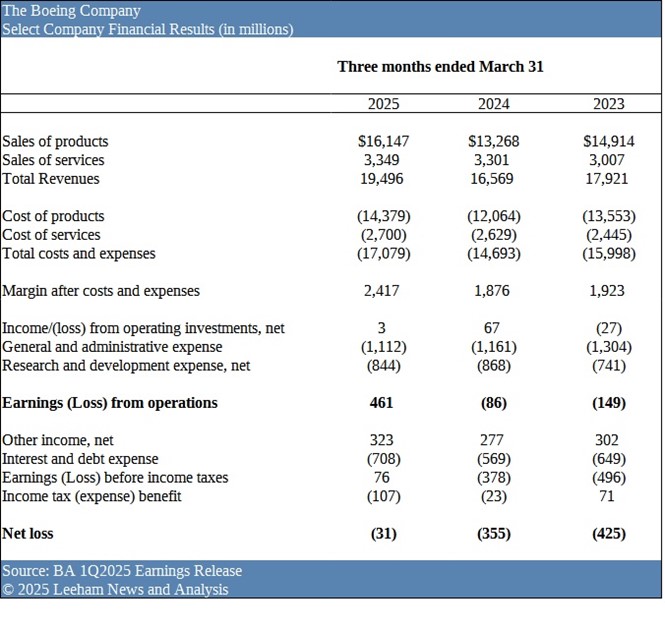

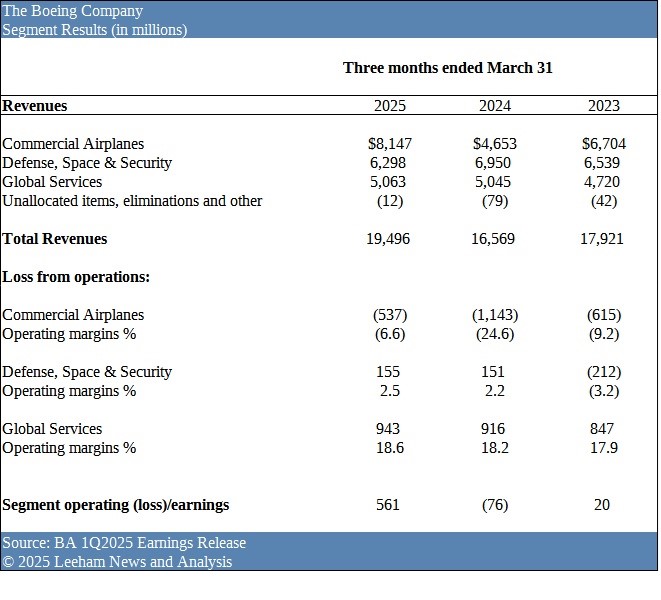

Company revenues outperformed 2023, with a 2.4% operating margin.

Company revenues outperformed 2023, with a 2.4% operating margin.

As expected, cash burn from operations was ($1.616bn) and FCF was ($2.29bn) for the quarter.

Consolidated debt, while up YOY, was relatively flat from FY2024, at $53.6bn. Interest dipped slightly from $755m to $708, over the past quarter.

Product sales drove the increase in revenues, versus 2023 – which was the stated barometer year.

Operations produced a positive result of $461m, while the net loss narrowed to ($31m).

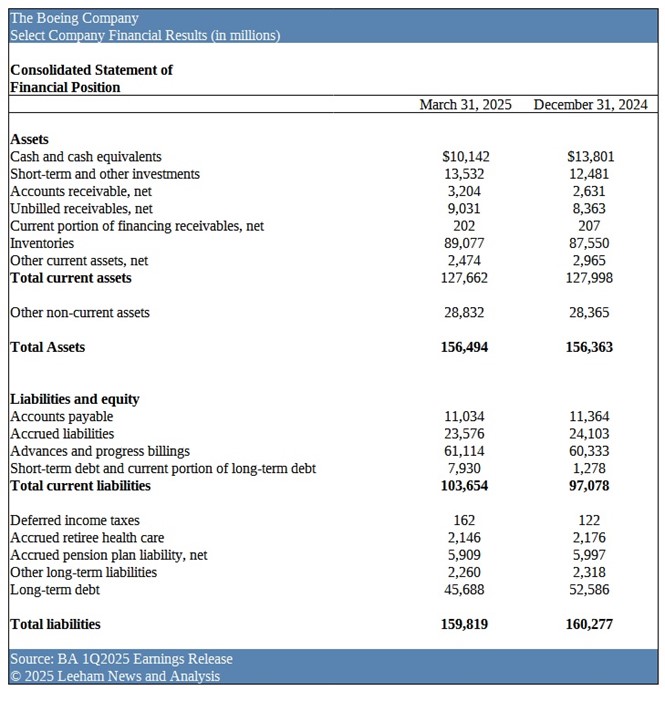

As expected, cash and equivalents dropped as the predicted cash-burn took effect in 1Q2025.

As expected, cash and equivalents dropped as the predicted cash-burn took effect in 1Q2025.

Inventories rose ~$1.5bn during the quarter, the cause of which will be determined when the 8-K is filed.

Boeing took in an added $781m in customer deposits, during the period.

Short-term debt increased dramatically, as long-term obligations become due during the year, meaning more cash spent to repay debt.

Segment Analysis

On the FY 2024 earnings call, investors were told to expect 2025 to be a repeat of 2023.

Margins at Boeing Commercial Aircraft (BCA) and Boeing Defense, Space and Security (BDS) were projected to be negative, while Boeing Global Services (BGS) was expected to continue producing profitable results.

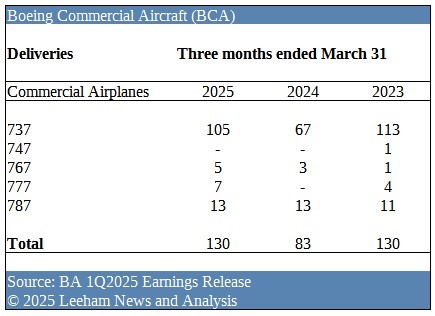

Deliveries at BCA were indeed a repeat of 2023, with an exact total of 130 aircraft turned over to customers in the quarter. Delivery mix was slanted towards widebodies with 25 delivered in 2025, versus 17 in 2023.

Deliveries at BCA were indeed a repeat of 2023, with an exact total of 130 aircraft turned over to customers in the quarter. Delivery mix was slanted towards widebodies with 25 delivered in 2025, versus 17 in 2023.

The 767 program once again showed delivery improvement, even as tanker numbers dropped, during the period.

When compared Year-Over-Year (YOY), 1Q2025 was a vast improvement, increasing dramatically from 2024 by 47 units.

This was primarily drive by pent-up inventory finally being released to customers, built up during the closing stages of 2024.

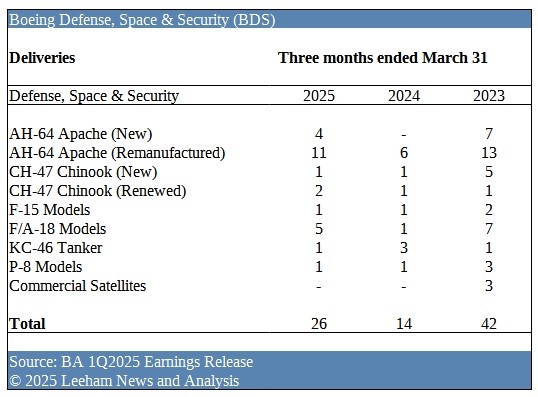

First quarter deliveries at BDS did not match 2023 levels, with only the Ch-47 Chinook (Renewed) growing modestly by a single unit increase. Every other program either declined or was relatively flat.

However, deliveries were up versus 2024, almost doubling from 14 to 26, driven by the F/A-18 and both AH-64 programs (New and Remanufactured). KC-46 Tanker numbers dropped, a result of cracks being discovered during pre-delivery inspections.

Commercial Satellites had a second consecutive first quarter with no deliveries, as Boeing tries to decide what to do with the program.

The increase in company revenues was driven by BCA, a jump of $1.443bn over 2023. This was helped by an increase in the widebody delivery mix.

The increase in company revenues was driven by BCA, a jump of $1.443bn over 2023. This was helped by an increase in the widebody delivery mix.

Margins were still negative (6.6%) but improved over previous years.

BDS earnings and margins were flat, YOY, but a welcome sign at the beleaguered division.

BGS quietly went about its business, producing a very solid 18.6% margin on sales of $5bn.

Once again

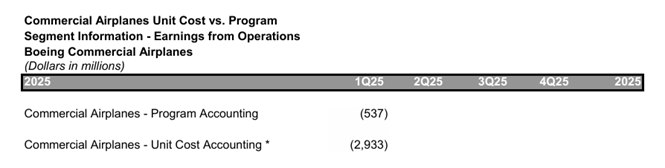

Looking deeper into the 1Q2025 results, with the help of the Boeing online unit cost vs program accounting cost page, was revealing:

BCA claimed negative margins of ($537m) during the quarter, however on a unit-cost basis, the loss was ($2.933bn), indicating that deferred production costs, stored in Inventory, will be on the rise.

~$2.4bn in costs incurred during 1Q2025 will now be capitalized, to be expensed against future deliveries.

Market Effects

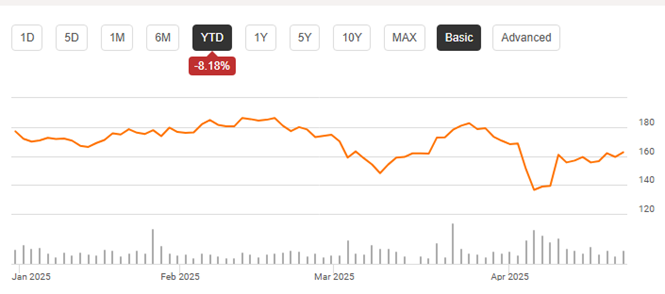

Boeing share price has been on a roller-coaster ride, since the beginning of the year.

Source: Seeking Alpha

Driven by the effects of the on-again, off-again, tariffs – investors have been hard pressed to judge future company performance, until a stable environment has been established.

The whip-saw swing has happened despite a slew of relatively good news, including decent delivery performance, awarding of a $20bn contract to BDS for the next-generation fighter aircraft and a bump in commercial aircraft orders.

Results will be updated following the 1Q2025 conference call with CEO Kelly Ortberg and CFO Brian West at 10:30 a.m. EST.

A further update will occur when the quarterly 8-K report has been filed with the Securities and Exchange Commission (SEC).

@ Karl Sinclair

As regards the Thoma Bravo sale, do we have any idea what (effective) revenue/earnings the divisions concerned (typically) contribute to BA’s profit and loss account?

Bottom line: BA receives a one-off of $10.55B, but at what expense to its recurrent revenue/earnings flow?

Any mention in conference call?

It’d cause a dent to BGS.

But I guess West is going to dance around it.

You are early. Earnings call is happening at 10:30 EST.

Yeah I know. Not waiting for cc to post.

More divestitures are coming.

> Boeing CFO Brian West says the backlog of aircraft for China stands at about 10%, putting outstanding jets between roughly 560 and 630. That means about 7-8% are in its backlog as undisclosed orders. 20-year forecast is 20% of demand.

https://bsky.app/profile/jonostrower.com/post/3lnihhk5oiu26

+1

Short term debt (to be repaid within 12 months) is now at $7.93B … up $6.7B from Q4 2024 (and moved from long term debt).

The $10.55B sale to Thoma Bravo will come in handy to cover this repayment, and to cover cashburn in the coming quarters.

***

Further, BA appears to have sold (or gifted to staff) 4,155M of its treasury shares in Q1.

Will China reverse course and take aircraft from Boeing? Clearly COMAC cannot replace them short term and Airbus is fully booked for many years. Losing China long term would be a big hit to Boeing. We’ll see.

China has hundreds of aircraft on order from Airbus — ordered years ago.

A sizable portion of Airbus’ monthly deliveries goes to Chinese customers. Take a look for yourself on Planespotters.

And Airbus has relatively early slots available for A330neos — which is fortuitous, since the A330 is popular in China. It seems that China is currently in negotiations to place a large order for them…

https://www.airdatanews.com/major-chinese-airlines-consider-ordering-more-than-100-airbus-a330neo/

@Fuller

The greatest risk to Chinese operators are the ones who have orders for C919 not in the Big 3. I could see some operators taking aircraft on secondary market if needed in a pinch.

Chinese lessors have 300 C919s on order.

Nothing stopping them from leasing those frames to smaller Chinese carriers.

COMAC is planning 75 C919 deliveries this year. How many Boeings would it have received in the same period, without tariff disruption? A lot fewer, methinks.

Not my point…the backlog is predicated on C919 reaching full production levels. They could have 1000 lease orders on backlog for that matter.

Big 3 likely to get first pick…others fending for themselves beyond that. I am not in the business of handicapping Chinese production, but pointing out the exposure. That production ramp is supposed to get to 150 in a few years too. Regardless of tariffs, very little imminent Boeing backlog to China. They made their 2025/6 plans a while ago.

Just because the Big 3 get “first pick” doesn’t mean that others get left out in the cold.

Take a look at the production lists at AB and BA — lots of frames for the big customers, but concurrently plenty of frames for smaller carriers.

Max nix.

The Maniac is backing off, he claims he did a great deal and how we are all going to get rich (US). The usual insanity.

The non Big 3 are going to hope it settles. They do not want to be an experiment with the C919s. They actually have to compete.

Wind up like the airline in Mexico with all those extra S100s. Spare parts donners but you got to take the parts out and then put them in and they break again.

And all the hullabaloo about Chineeseing the C919. Need to make up your minds.

China will want Airbus first, then the airlines will want Airbus or Boeing and the last thing they want is a C919.

Chineese leasers march to the government tune.

I do not know how free the other airlines in China are, I doubt they are free reign airlines.

53% of the Aircraft in China are leased, I don’t know how that breaks down between the big guys and small guys.

Leasing is a way of getting around buying.

No one other than Chineese government knows.

Well, this is why I call our poster, an instant solution provider, he knows everything and can speaks on behalf of the Chinese big three!

👇

Reality is the thing that doesn’t go away even if you don’t like it.

I see fear in the eyes of a fan. Desperate.

I think we are talking past each other; you are assuming the telegraphed delivery plan is rock solid. Somebody gets the short end if it is not real.

There was 1 delivery in 2022, 2 in 2023, 13 in 2024.

A plan that shows 75 in 2025 and 150 by 2028 is…ambitious.

Boeing announces delivery plans all the time that are unhinged with reality. Airbus is chronically late. Comac may hit those rates. I would not take that bet, but that is my opinion.

@Casey:

You assume its a conversation and not what it is which is an absolute.

China is wonderful, the rest of Europe and US is not.

China is even worse capture of the AHJ certification, but as China is pure gold that is fine vs an FAA that is partly (or was) captured.

The Illogical twists make a pretzel look like a straight line.

“Boeing announces delivery plans all the time that are unhinged with reality. Airbus is chronically late. Comac may hit those rates. I would not take that bet, but that is my opinion.”

The above per your post you can take to the bank as a reality. China does not know what its going to do let alone someone posting from afar. The C919 is a dilemma for them. Get rid of its Western content at the risk of huge delays (10 years) making Chinese equipment that is not proven? Stick with Western stuff?

Its all about image and the image is what China says it is.

What we do know is the US election swung on a narrow 1.5%. Run it again and it would go the opposite way.

Stefanic got her dream job taken away from her because it was a vote in the house they could not afford to loose but also high probability that a Democrat would win a special election (that is a two swing vote).

Its all in flux. No one has certain plans because no one knows where its going, even more so now than previously.

And even when it settles out, there is going to be downs all over the place that are not going to settle out for years.

US is the big looser as its now considered non reliable.

I saw the assembly lines with my own eyes. Comac will make the rates they are claiming providing they can get parts from Western manufacturers.

Thanks for this comment.

COMAC may not even need parts from Western suppliers: they’ve hoarded engines for 2025 production, the CJ-1000A is coming soon, and substitution of other western parts is well within China’s ability.

@Rudolf

My reticence to assume the stated rates is that there is more to making a plane than a FAL. That FAL is dependent on quality feedstock. Just ask Boeing about quality feedstock. Ask Airbus about a lack of engines.

COMAC is reliant on an entire ecosystem that must ramp. Not impossible, but difficult. There is a universe of possible deliveries. The stated production rates are the high end, not the mean.

Assembly lines are one thing, filling them is a different story.

Just like everyone else China has to manage a supply chain that is not under their control.

Boeing has the room in Charleston for 10-14 x 787 a month, they are at rate 5 roughly right now.

Have you talked with Boeing workers over there?

Al Jazeera:

> “I wouldn’t fly on one of these planes,” one worker tells him, “because I see the quality of the fu**ing sh*t going down around here”.

Another worker replies, “it’s sketchy”. Asked what he means, the worker adds, “yeah I probably would, but I kind of have a death wish too”.

A third says of the 787s assembled at South Carolina, “we’re not building them to fly. We’re building them to sell. You know what I’m saying?”

> The Boeing worker also says that he is concerned that some of his colleagues are on drugs, saying he has seen “people talking about doing drugs, looking for drugs”, specifically marijuana, cocaine and prescription painkillers.

> Cynthia Cole, former president of Boeing’s engineers union SPEEA, adds that she would no longer fly on a Boeing 787. “I’ve been kind of avoiding flying on a 787 and seeing this, I would definitely avoid flying on a 787.”

that’s from 2017…

Well, there is plenty of evidence to support my post, not conjecture, unlike his.

Scott, you know as well as me there are documented recent issues:

https://www.seattletimes.com/business/boeing-aerospace/new-boeing-whistleblower-says-raising-substandard-work-on-787-got-him-fired/

https://www.seattletimes.com/business/boeing-aerospace/faa-opens-new-investigation-into-boeing-787-wing-to-body-join-work/

@Pedro: And you’d be much better off citing recent issues than something from eight years ago.

Jeppensen is sold off at a great price.

They kept the core to Boeing needs. Satellites should be next and if you can’t sell, close down and write off.

“Boeing Turns In Solid Q1, But Analyst Flags Ongoing Delivery Hurdles”

“Epstein notes that Aero Analysis Partners, an intelligence boutique specializing in coverage of aerospace OEMs, observed that Boeing’s 737 deliveries in April are falling short of expectations, with only 16 units delivered so far—lower than the 22 delivered during the same period last month, which was already below projections.”

“On the production side, AAP expects Boeing to average 28 737 rollouts per month in the second quarter—a slight increase that accounts for the fact that first-quarter output was boosted by aircraft completed in late 2024 but delayed by a strike, the analyst writes.

“The firm also believes Boeing might reach a monthly production rate of 38 later this year, although sustaining that pace could be difficult.”

https://www.benzinga.com/trading-ideas/movers/25/04/44965748/boeing-turns-in-solid-q1-but-analyst-flags-ongoing-delivery-hurdles

***

An average of 28 MAXs p/m…at that rate, Q2 is shaping up to be another loss for BCA.

16 is almost 38. 😉

Its an mfg endeavor not a spring race

Realistically on average the 737 production is at roughly 28- 30.

Are those numbers with or without the Bryce factor?

Our resident Eternal Pessimist.

BCA Q1 2025

Revenue 8,147m

Loss from Operation (537) [under program accounting]

Op margin (6.6%)

Thanks @Karl Sinclair mentioned actual result is much worse under unit cost accounting:

Loss from operation (2,933m)

Op margin (36%)

Deliveries

737 105

787 13

Indeed!

130 deliveries produced a 36% operational loss!!

You really have to hand it to the BCA sales team for selling so many aircraft below cost 👍

And there’s now $30.5B lurking in the Deferred Production Balance — though it seems that most analysts (choose to) overlook that.

+1

They’ll make it up in volume. 😉

Everyone,

AW: All-Russian Superjet 100 Takes To The Skies

https://aviationweek.com/air-transport/aircraft-propulsion/all-russian-superjet-100-takes-skies

And in March:

https://aviationweek.com/air-transport/aircraft-propulsion/superjet-100-takes-russian-pd-8-engines

nice.

Not sure if this was stated earlier…looks like 35 aircraft left from the MCAS era (down from 55 Q4 2024)…25 of which are for China. Not sure if those are through completions or will need retrofit. Q2 deliveries likely going to have to substantially be new tails.

No real guidance on Max7 or Max10…not exactly re-assuring

B777-9 is “2026” which is odd because that is anywhere from 9 – 20 months away.

B777-8F is 2028

B777-8P is “at least 2030” which does not really seem like a plan as much as it is an idea.

This is not directly on topic, but I suspect that Mr. Hamilton won’t mind.

-+-+-

Peeved by Boeing’s recent F-47 “win”, LM is planning to offer a souped-up F35+ :

“Lockheed Mulls F-35 ‘Plus’ After NGAD Loss to Boeing”

“After losing out to Boeing in the high-stakes Next-Generation Air Dominance (NGAD) race, Lockheed Martin isn’t licking its wounds — it’s gearing up for a major comeback.

“The world’s largest defense contractor is now considering a souped-up “fifth-generation-plus” version of its F-35 fighter jet, promising around 80 percent of the advanced capabilities expected in the futuristic F-47, but with a much friendlier price tag.”

““We’re basically going to take the [F-35] chassis and turn it into a Ferrari,” said Lockheed CEO Jim Taiclet. “It’s like a NASCAR upgrade, where we would take the F-35 [and] apply some of those co-funded technologies both from NGAD and the F-35 program.”

“The F-35 “Plus” could include next-gen upgrades like an advanced passive infrared radar system, though Lockheed is keeping the full specs under wraps — for now.”

https://nextgendefense.com/lockheed-f35-ngad-loss/

So why was the F-35 not a Ferrari in the first place? Uncle shug-shug’s MIC gravy train continues..

Precisely: promise a Ferrari, but deliver a Vanette.

Will anyone fall for that ruse a second time?

Further to its article on this subject in June last year, the Air Current is now reporting a further stagnation of Boeing’s interest in the X-66 TTBW concept:

“Boeing shelves plans to fly NASA X-66 flight demonstrator”

https://theaircurrent.com/feed/dispatches/boeing-shelves-plans-nasa-x-66-flight-demonstrator-ttbw/

Another red herring 🐟

One wonders if BA was ever actually seriously committed to this project…or was it just a PR stunt?

Calhoun paused funding and resources after Alaska 1282.

The recent revelation of substantial ice accumulation on the trusses — requiring an elaborate de-icing system — may have served to further put BA’s interest “on ice” (no pun intended).

@Transworld accused me recently of spreading fake news when I said that Boeing engineers had been moved away from the X-66 and re-assigned to other projects — so it’s good that you’ve provided authoritive confirmation 👍

+1

Wow. OMG! The X-66/TTBW was peddled by our poster like the greatest thing after sliced bread.

Certifying a high wing airplane for wheels-up or water landing it another issue.

The latter. TTBW would need much wider airport gates, which would never fly. Smoke and mirrors for the Rubes..

The wings will fold.

Well, that was the intention…though not sure how it would work out in reality.

Thin wing = less (or no) fuel storage in wing.

Trusses get in the way of ground crew.

Truss icing problem.

The concept has been around for a century — there are reasons why it never made it into mainstream commercial aircraft.

Nice toy for the NASA nerds to play with, but a damp squib for BA.

Also the truss would transfer part of the lift into the fuselage, pinching it toward the wingbox. This is a totally different load regime. The fuselage would need to be strengthened to bear the compression load vertically, which is hard and heavy.

I wonder how difficult it’s to turn an existing MD-90 into a high wing aircraft. Another project on the cheap at the start turning into a disaster, after the VC-25B. Boeing has lost its mojo?

Sure they will.. and I want a pony, too.

Chinese airlines took delivery of about 6 jets this month.

https://www.bloomberg.com/news/articles/2025-07-14/boeing-s-triple-china-deliveries-sign-of-easing-trade-tensions

They took even 3 in one day earlier this month