Leeham News and Analysis

There's more to real news than a news release.

Boeing First Quarter Results Update: China is 10% of the backlog, with 500 in “Unidentified”

By Karl Sinclair

April 23, 2025, © Leeham News: China represents 10% of Boeing’s commercial airliner backlog,

Boeing first quarter 2025 earnings report.

CFO Brian West clarified on the Boeing 1Q2025 earnings call. About 50 aircraft are scheduled to be delivered to China this year, but all are in limbo due to President Donald Trump’s trade war tariff fight, which began this month.

Previously thought to represent some 2% of the commercial backlog, with another 2%- 3% added for lessors, it was revealed that China represents 10% of the Boeing (BA) backlog. There are 130 Boeing jets identified in the backlog destined for China. With 6,319 Unidentified orders, about 500 are placed by China’s airlines and lessors.

“We have roughly 50 airplanes in our plan this year going into China, so we’re going to be pretty pragmatic with what we do here. For those airplanes that haven’t been built yet, we’ll be looking to maybe redirect those to other customers. For the airplanes that have been built, we call it re-marketing,” said Boeing CEO Kelly Ortberg on the CNBC financial network this morning.

Re-marketing, as Ortberg puts it, can be a costly endeavour.

At the end of FY2024, Boeing still had 50 aircraft in inventory (40 for China) it needed to “re-market.”

The 737 MAX program also incurred abnormal production costs and write-offs of ~$22bn since the grounding.

It was revealed that Boeing also had four 787s in production destined for China.

Holding onto inventory, especially commercial aircraft that need to be maintained, can be an expensive exercise.

Increasing production rates

Perhaps Ortberg was slightly optimistic when he said, “We will increase to five airplanes a month when we go through rate increases. The first one will be 38 to 42. The next rate increase, likely about six months after the first rate increase, will be from 42 to 47. And we want to be in the mid-50s when we get production stabilized.”

According to Ortberg, Boeing is currently producing at 31/mo, and jumps of that magnitude in six-month increments, especially in the current supply chain environment, are unheard of.

Ortberg also believes that Boeing will be able to recoup tariffs imposed on foreign-made components when they are sold outside the US.

“The tariffs we’re paying, for example, in Japan and Italy, for those airplanes that we deliver outside of the US, we’re able to draw that back”, he said.

Under the current US law, “new tariff rates that are being adopted apply only to permanent imports into the United States,” law firm Vedder Price said on April 8, six days after Trump announced tariffs. “While subject to a bond and certain other requirements, temporary imports will not be subject to tariffs. Keep in mind that temporary imports involve items that will not be sold or used in the United States. Instead, the item enters the United States on a temporary basis only and typically for the purpose of undergoing repairs, alterations or some processing and then will leave the United States within the required timeframe.”

On the demand for aircraft already produced for Chinese customers, Ortberg said, “Customers are calling, asking for additional airplanes. This is really gonna be just a short-term challenge for us to either have China reverse course and take the airplanes or get us in a position to re-market those airplanes. And as you know, to re-market them, we’ll have to do some things like painting them and things like that”.

Painting them and reconfiguring may sound simple, but it’s not.

Jeppesen Sale

When queried about the impact on future earnings that might occur once the deal to sell Jeppesen, ForeFlight, AerData, and OzRunways closes in late 2025, West was non-committal.

“… [T]he service business will continue to perform in that [it will] grow in the mid-single-digits revenue and deliver nice mid-teen margins,” West said. BGS delivered a margin of 18.6% in 1Q2025, up 40 basis points, year over year. That is closer to high-teens than mid-teens.

If Boeing stays the course, what it will do with the $10.5bn it receives at the end of 2025 will also be fairly obvious.

“Debt balance ended at $53.6 billion, down $300 million due to the pay down of maturing debt and leaving $550m of debt maturities remaining in the year,” detailed West.

At the end of 2024, short-term debt and the current portion of long-term debt jumped to $7.93bn from $1.278bn.

Boeing will pay down $550 m in debt in the next three quarters. Therefore, about $7.380bn in debt is due in 1Q2026.

The $10.55bn in cash received for the Jeppesen sale will be used to pay that obligation, leaving Boeing with $3.17bn in cash from the deal.

2Q2025 Guidance

Cash burn in the second quarter is expected to be similar to 1Q2025, with perhaps a slight improvement, showing in the expected annual burn rate of $4bn-$5bn.

Expected 737 MAX and 787 deliveries are projected to hold, even with the impacts of the Chinese embargo.

West also explained who would be on the hook for any input increases due to tariffs.

“I’d also say that, keep in mind that over time, any input related costs will work its way through to price escalators. It should mostly neutralize over time. Then in addition to what Kelly said about the suppliers, as you know, many are on fixed price, like a program contract, where the importer record does pay the tariff,” he said.

LNA first reported that Boeing views sales contract escalation clauses as its mechanism to pass the tariffs on to the buyer.

Boeing will try to use contract clauses to pass through increases to customers, while letting suppliers take the hit for any tariffs paid for goods shipped to Boeing.

CNBC financial pundit Jim Kramer made an interesting point prior to the start of the interview with Kelly Ortberg.

He said that countries around the world should order Boeing aircraft to pressure decision-makers about America’s largest exporter. With delivery slots unavailable until the early 2030s, he intimated that those ‘orders’ could be cancelled and used as a negotiating tactic.

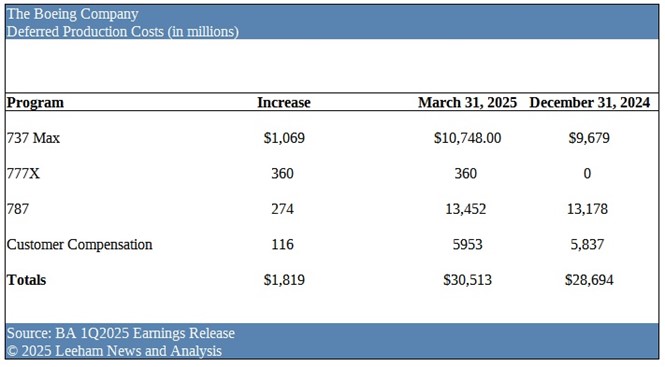

Deferred Production Costs

The breakdown of capitalized costs stored using program accounting is detailed in the Boeing 10-Q SEC filing for the quarter.

Deferred production costs and customer compensation rose once again, during the quarter, adding $1.819bn to the Balance Sheet value of Inventory, which are expenses.

This relates to the $2.4bn difference between reported program accounting margins ($537m) and actual unit-cost figures ($2.933bn).

As of March 31, 2025, 35 737 MAX aircraft produced prior to 2023 are in inventory, 25 of which are for customers in China.

There are 20 787 aircraft in inventory, produced before 2023 and that require rework, four of which are for customers in China.

For comparison, Boeing reported this in previous filings:

Commercial aircraft programs inventory includes approximately 335 737 MAX aircraft and 110 787 aircraft at December 31, 2021 as compared with 425 737 MAX aircraft and 80 787 aircraft at December 31, 2020. – 2021 Annual Report.

We have approximately 250 aircraft in inventory as of December 31, 2022, including approximately 140 aircraft in inventory that are designated for customers in China. We are remarketing some of these aircraft to other customers. – 2022 Annual Report.

At the end of 2021, Boeing 737 MAX inventory had a total of 425 aircraft, with 140 destined for China.

At the end of 2024, 40 aircraft for China still remained. That was drawn down to 25 aircraft during 1Q2025, due to an increase in deliveries to Chinese customers.

Lots of good info to digest in this article- thanks for it.

Also, definitely looking forward to buying Scott H’s new book around September.

Yes, indeed.

Huge compliment to Karl Sinclair for excellent reporting 👍

“This is really gonna be just a short-term challenge for us to either have China reverse course and take the airplanes or get us in a position to re-market those airplanes.”

I think the solution might not be China reversing course, but Trump & his MAGA boys withdrawing their silly crusade, again. I always thought the 787-10 is the perfect platform for Asian domestic & regional mass transport, lots of potential. Now we are seeing another A330 revival..

Competition is good 👍

@Kesje:

All spot on

And now we know how committed Boeing is to this project. Not the full aspect but more than enough.

https://theaircurrent.com/feed/dispatches/boeing-shelves-plans-nasa-x-66-flight-demonstrator-ttbw/

I saw studies that airlines did not like it. So off with its head.

The other take is if a fairly conventional looking aircraft gets dissed, then one with props is going no where as well.

Its one of those conundrum . Public does not like different, but the only way for a significant jump in shapes to get improvements is required.

You can get a bit out of a composite wing, a bit more out of a GTF using the unused capability (aka the PW1000 conservative in its specs).

Not sure how a blended wing is perceived. More modern or to be avoided as well.

The penny has finally dropped…though it took long enough 😅

Didn’t you proclaim earlier this month that reports of Boeing’s diminished interest in the X-66 were fake news? 🙈

Fake? I did not believe it was accurate. Fake is when someone is trying to smoke you. KAC and her alternative facts.

Logic said they would continue, so obviously that logic does not apply.

It makes no sense to start something and invest in it just to dump it.

But yea, that is the reality.

I would have no issue with it, so unlike Jet Zero that has investment occurring, airlines are not looking at this as the appeal forward.

As long as it passes all the tests I am good with that but then I am not an airline trying to sell seats nor the public.

I am disappointed as I thought it was an interesting direction.

Unlike RISE which I think is a dead end.

“Fake? I did not believe it was accurate. Fake is when someone is trying to smoke you. KAC and her alternative facts.”

Looks like you have a selective memory 🙈

Here you go:

“TransWorld

April 1, 2025

Well you won’t. Abalone nee Bryce has told us Boeing laid off its workers on the project. Granted if you believe that I have a bridge I want to sell you.

“He is getting worse, throwing a lot of spaghetti at the wall, his references are other areas and he swings them over to an area they don’t apply in.

“note he does not supply any link to what he thinks is what is going on.”

🙂

One set of rule for thee!

> “But yea, that is the reality.

I would have no issue with it,”

Sounds like bargaining, isn’t it? 🙈

Really?

Ahh well, that nails it.

I admit anything from certain sources gets dismissed.

I guess sooner or latter if you threw enough stuff something sticks.

So yea, I was flat wrong on that one.

It’s a shame Boeing shelved the experimental X-66 prototype. I question its true value anyway. The core technologies it was meant to test – high aspect ratio wings and high bypass engines – are already quite mature. Accurate simulations could have likely predicted their performance and environmental impact effectively.

So, BA now has no new aircraft program in the pipeline.

One way or another, it doesn’t have the money for such a program.

It’s stuck now with the archaic 737…up against more modern competition from multiple OEMs (Airbus, Embraer, COMAC, Yakovlev…all with FBW and modern CAS, and very attractive pricing in the case of the newbies).

The usual suspects will, of course, auto-deride the Chinese and Russian offerings, but they’re just instinctively beating a tired old drum that they got at school.

The aviation industry is heading into an interesting era.

They would not let me near a drum at school, I would just break them.

It should be pointed out, that the newest viable desing for sale is the A320NEO and the MAX is just as good as the A320 in its economics.

CAS adds nor has proven to add anything to safety. One of Abalone oft loved institution flipped that into a bill. Like voice alarms, its not been researched, Airburs just decided it fit in with computer screens.

Metour pilot has done an excellent comparison.

I have mixed feelings on the X-66. Not being an engineer, I have no way to even get a hint of its complexity and cost vs just a thin wing. It was one of two ways to get a serious aerodynamic gain (BWB the other)

It seemed Boeing was committed to the test and clearly they changed their mind (or Ortberg changed Boeing commitment to it). I felt they were very committed to the X-66 if not it as a future possible. Under Calhoun they were but always suspicious of bait and switch with that guy.

The big question is do you jump in with unproven tech or stick with what works. Airbus and UAC , COMAC have all gone with conventional. MC-21 went advanced composite route, much like an A350.

I had hoped to see the MCC-21 in service, it was a jump ahead albeit conventional its pushing conventional to the MAX (pun intended). Sadly its not going to get international certification (at least in the foreseeable future, Russia did have the system in place to do so unlike China)

An in service MC-21 with all Russian content is at least 5-10 years away. How certifiable its system will be is a good question.

C919 is a standard and most probably ok design tho0ugh I hate hidden cert factors. Open is far better but we never will see open from China.

As long as the playing field is leveled by China, then its a matter of how reliable it is. Airlines take what they are told to and then park it as much as possible if not reliable.

A lot depends on where it all goes with the Maniac at the helm of the US.

China can and will ramp up if things sort out, otherwise they its a stop program while they develop Chinese systems. At least 5 if not 10 years away for that to occur.

I would put my money into an all new design. See if EASA would try to establish a cert path.

By the time a fully Chinese C919 is flying and in series production (one off does not count) it too is very dated.

“An in service MC-21 with all Russian content is at least 5-10 years away.”

Aeroflot will be receiving its first all-Russian MC-21 in 2026. Serial production of the aircraft has already started.

https://interfax.com/newsroom/top-stories/108483/

You really just make this stuff up as you go along, don’t you?

***

If the Russians can remove western content in 3 years, then the Chinese will do it even more quickly. Seeing as they’ve already started that process, we won’t have to wait too long. The CJ-1000A is slated for certification this year. So, an all-Chinese C919 won’t be “dated” at all.

@Abalone

You know there must be one at the bottom and it can’t be the fallen titan, right? If it were the Russian, who else could it be?

What kind of mental gymnastics have to be performed to fit into the distorted reality?

An emperor who never accepts he is dethroned; a champion overindulges in his former glory.

@TW

There are a few things to unpack on the X-66. I really did not hear that the design would not work…it was rather evasive.

Some of this work was likely funded through NASA and right now maybe that funding was subject to withdrawal. All the same, this was not really an EIS plan. Boeing has no EIS plan. From what I can tell, they have no Max7 or Max10 plan either. I am less concerned about the X-66 going away as I am that there is no real plan in the background.

I can think of other reasons this may have been cancelled. One of them is simple produceability…the modification of MD-90 may have revealed that this was going to untenable to produce. Some of it may have been lack of supplier enthusiam. Parternering for Succcess has not left a lot of suppliers ready to pounce. Maybe I am harping, but before Boeing can think about producing a new aircraft it needs to regain the ability to certify literally anything.

Hard to see the MC-21 selling in quantity. After the last three years of sanctions it would be a bold move by an airline outside of Russia or its orbit to invest on an entirely Russian airframe. Tariffs are not the same as sanctions.

This is a classic misleading headline. Truly fake. If you read the details its no where near a fully substituted S-100.

https://archive.ph/73ftW

And of course there are people that will jump on it and not read the details.

And have you got some sort of link to substantiate your assertion that it’s “no where near a fully substituted S-100.”..?

“To expedite certification trials, a third Superjet, fully incorporating import substitutions, is planned to be brought into the testing regime. This prototype aircraft is scheduled to join the flight test programme in April. Certification of the PD-8 engine is anticipated this autumn.

“The Superjet’s import substitution programme involves replacing approximately 40 imported systems and units, including the engine, avionics, undercarriage, and other key components. The aircraft also features a new domestically-produced fuselage.

“Two further prototype engines are scheduled for delivery before the end of March for flight testing. UEC (United Engine Corporation) General Director Alexander Grachev noted that the PD-8 engine had demonstrated excellent results and fully validated its technical specifications.”

https://ruavia.su/russian-built-superjet-100-with-pd-8-engines-completes-maiden-flight/

The Russians develop things gradually.

One thing I found quite interesting is that they added an Airbus-style curved winglet to the wing.

Indeed.

If you look at the RuAviation link that I posted and click on the “civil aviation” tab, you’ll see a sub-tab devoted to the MC-21 — featuring detailed monthly updates and other interesting articles.

The most recent article discusses an update program for the PD-14 engine.

Both China and Russia seem to be following a similar approach, i.e. get a basic model certified and flying, and then come with a relatively fast succession of incremental upgrades.

In this case they are gradual because most of their capability is going into military equipment.

It never was intended as an all Russian though the engines were highly likely if not a given.

It had a world competitive intent, now its a Russia only aircraft. They can’t even sell it to China.

There’s that tired old drum…right on cue

Who says it’s a “Russia-only” aircraft? There are loads of countries aligned to Russia — in the ME, Africa, South America and Asia.

Didn’t you similarly tell us that COMAC planes would be “China-only”? Yeah, well, that’s turning out differently, isn’t it?

How do you know they “can’t even sell it to China”? Just because no orders have been announced doesn’t mean that the Chinese aren’t interested.

If you look at the latest 737 MAX pages on Planespotters, you see that a huge majority of frames are for US carriers. So, looks like the MAX is becoming “US-only”, doesn’t it? If it were’t for Ryanair, it would have negligable presence in Europe.

People hold on to their pictures of the world. Only the most introspective revise their pictures in light of incoming data. That’s why there’s this fervor of “revival of manufacturing” — what manufacturing? T-shirt? Sneaker? iPhone?? No one knows. How about tea? How about coffee?

It’s all performative, it’s a show, a kabuki. Kool-aid peddled as solution.

@ Pedro

Just consider these (annual) production targets for 2025/2026:

C919: 75

C909: 36

MC-21: 36

SJ-100: 18

That’s 165 aircraft…enough to start taking a noticable slice out of the western aviation cake.

What will the situation be like in 3 years? 5 years?

Airbus and Boeing aren’t selling to Russia since the Ukraine War began. The SJ100 is a regional jet and irrelevant to Airbus and Boeing (and Russia couldn’t support it outside Russia pre-war anyway). The C909 is a regional jet that has not been certified outside China. Good luck on the C919 hitting rate 75 (6.75 a month). Ain’t going to happen this year or next.

There is an inflection point from producing a few aircraft per month to large scale.

The biggest is supplier diversification; avoiding single points of failure in your ecosystem. That is one reason why aircraft supply chains tend to go global.

The other objective to rate-level production is quality confidence. Producing only a couple aircraft per month gives a lot of time to swap out non-conforming components or to rework them. It is not an assembly line as much as it is a job shop. I wish COMAC and Irkut the best on their journeys. They are attempting to do on a national basis with a new supply chain that which Boeing and Airbus do a global basis with an established basis.

AW:

“VietJet Air plans to commence Comac C909 operations starting April 19 after the LCC sold tickets for flights on Hanoi-Con Dao and Ho Chi Minh City–Con Dao routes.”

FG Apr 20:

Comac’s C909 begins commercial service in Vietnam

I wonder how the efficiency will be, given the (small) size of those cowls.

The all-Russian PD-8 has the same bypass ratio (4.4) as the previous Franco-Russian SaM146 engine.

Further:

“The PD-8 is a complete analogue of its predecessor, the Russian “Frenchman” SaM146, but in almost everything is a little better. The specific consumption has been reduced from 0,63 kg/kgf•h to 0,61 kg/kgf•h, while the thrust has been increased by 20-180 kgf, depending on the modification. The Russian engine fits into the engine nacelles of serial Superjets with virtually no modifications.”

https://en.topwar.ru/208162-polnyj-forsazh-tempy-razrabotki-pd-8-sdvigajutsja-vlevo.html

https://engiru.com/engines/pd-8/

Thanks. Ab.

SaM146 has a French core (hot section). The Russians replaced the French core with a Russian one, keeping everything else, and called it a PD-8.

Looks like it’s you that missed what’s in the article.

Tap the sign

“Reality is the thing that doesn’t go away even if you don’t like it.”

Real news vs “fake” news

> Engine maker Safran says China is exempting aerospace parts from tariffs

> Company CEO says deliveries of engines and other parts are being let in without import taxes

How come there’re like hundreds of reports & analysis based on a “fake” report but no one dare to ask those from the industry??

Oh are there a flood of posts coming that say it’s because China needs foreign engines?

Here’s a link to that story:

“We learned last night that China has taken the decision not to tax engines or landing gear or nacelles (engine housings), in other words a certain number of aerospace equipment parts,” CEO Olivier Andries told reporters on a first-quarter results call.”

“”It demonstrates that the situation is very fluid,” he said, adding that finished aircraft were not included in the decision.

“China is considering exempting some U.S. imports from its 125% tariffs and is asking businesses to identify goods that could be eligible, business groups in China said on Friday.”

https://www.streetinsider.com/dr/news.php?id=24687665&gfv=1

It should be noted that Safran has 20 different plants in China, employing 2500 people.

Is BA going to pocket the $400m plus from NASA? Are there any claw backs?

This is not going to end well:

Donnie made it clear today:

He wants the tariff revenue taken in by the ‘External Revenue Service’, to replace tax dollars from income tax, by the Internal Revenue Service.

Tariffs are here to stay.

We’ll see. 11 states have sued over their legality.

How did that work out for that judge in Wisconsin? Is the Trump admin noted for following the rule of law and adhering to rulings?

Not that they could be right and win in court – but what if he thumbs his nose at them and gets Kash Patel to round them up?

Trade tariffs cannot replace income taxes – UBS

Trade tariffs cannot replace income taxes, said UBS’ chief economist, after President Donald Trump tied tariffs to potential tax cuts for middle-income earners.

Trump said on Sunday that revenue from his tariffs could allow him to lower income taxes for Americans earning under $200,000 a year, even as concerns about the direction of his economic policies continue to grow.

“Trade tariffs cannot replace income taxes—to suggest otherwise either raises questions of policy competence or implies a deficit-financed tax cut. Neither is likely to shore up waning faith in the safety of the US dollar,” UBS Chief Economist Paul Donovan said.

And I think it is pretty obvious what the endgame here is.

When Donnie says “everyone making under 200k will benefit”, he really means “everyone earning over $5m a year, will benefit, the most.”

@ Frank P

Just wait until shortages start to bite — then the tune will probably change.

The Port of Los Angeles expects a 35% drop in sea traffic arriving from China, and other Asian countries, starting to manifest itself in the coming 2 weeks. The shortfall amounts to ca. 30,000 sea containers per week — and that’s just at LA. You can pack a *lot* of goods into 30,000 sea containers — electronics, spare parts, appliances, medical supplies, clothing, toys…and that’s all going to be missing from US shelves.

https://www.latimes.com/business/story/2025-04-24/traffic-at-the-port-of-los-angeles-set-to-plunge-amid-tariffs-disruption

On top of that, there’s also the rare earth embargo to consider.

Donnie has his head in the sand.

And 30,000 less containers to move.how many truckers will be out of work

…and those truckers will, accordingly, be making less use of diners, motels and gas stations.

But tariffs will make the USA rich Donnie says.

At the top of my tl today:

> Trump’s China tariffs are about to unleash a supply shock on the US economy, with shoppers likely to see empty shelves and higher prices. “We are paralyzed,” said Jay Foreman, CEO of toymaker Basic Fun in Boca Raton, which supplies big retail customers such as Amazon.

> There were 4 national polls released today. All of them show the same thing. Trump’s approval is crashing and it’s directly tied to how Americans feel he is handling the economy, and particularly tariffs. The economy went from his strongest issue to his weakest due to tariffs.

For those who peddled the idea that “we don’t need cheap Chinese toys!”, time for reality-check. It’s American jobs and American businesses on the line. Have fun. Time to “reshore” toy manufacturing! Enjoy.

The NYTimes runs a piece about Your Home without China, check it out. I think for many small appliances and others, there’s a perfect supply chain there. What a pity. It’ll be gone for no reason.

More

> • 46% of Toy Companies in the US say they expect to go out of business within “weeks”

• Shoes expected to go up 87% in price

• Apparel expected to go up 65%

• US Exports expected to drop 18%

• Tourism to US down 20%

Don’t forget spare parts!

All those little knick-knacks for your vacuum cleaner, printer, lawn mower and air conditioner…they come from China (or used to, until they stopped coming).

I simply cannot believe that this is not mentioned

more here in the Exceptional Nation: 80% or more

of what one buys here [including DoD] comes from China..

#weird/cognitivedissonance

We’ve been told that we’re ‘exceptional’, ad nauseum. Baloney and hubris.

“Embraer goes to China to seek orders for its aircraft”

“Planemaker participates in Airshow China 2024, in Zhuhai, and says it wants to explore opportunities for collaboration with the Chinese supply chain”

“…While Pratt & Whitney’s GTF engines are the main reason for the delays, there are also problems with structural parts, the executive said.

“Therefore, a possible collaboration with Chinese companies could create an alternative source of supply and perhaps open the door to orders from the country’s huge aviation market.”

https://www.airdatanews.com/india-france-sign-deal-to-acquire-26-dassault-rafale-naval-fighters/

***

Makes sense — two BRICS buddies seeking mutual benefits…

Three BRICS make regionals. China needs to diversify the C909 away from the Big 3. When you look at the historical deliveries…that is where most have gone…and most of the forward backlog is elsewhere. Not sure that leaves room for many E2 orders.

Hard to know if China is the best place to try this. If you are going to go down the path of BRICS collaboration…I have to think India would be the better option since they are not supporting their own domestic airframes.

India:

“Govt to set up SPV to create ecosystem for India-made aircraft”

“The government plans to set up a special purpose vehicle to develop an ecosystem for aircraft manufacturing over the next five years, aiming to scale up the manufacture and export of locally made planes, the civil aviation minister said on Wednesday.”

““We want to inform the industry that the government is strongly pushing into the idea of India manufacturing their own planes,” he said on the sidelines of the 10th PHD Chamber of commerce and industry Global Aviation and Air Cargo Summit 2024 in New Delhi.”

https://www.livemint.com/companies/aviation-ministry-spv-aircraft-boeing-airbus-make-in-india-dornier-hindustan-228-11725450578175.html

After already finding alternatives for US LNG and oil, China has also got alternative sources for grains:

“Business News: China Says It Won’t Be Affected by Loss of U.S. Grains and Oilseeds”

https://www.agriculture.com/china-says-it-won-t-be-affected-by-loss-of-u-s-grains-and-oilseeds-11723074

Even if the trade war ends tomorrow — which it won’t — there’ll be a big dent in US exports.

Interestingly: the LNG, oil and grain sectors in the US are concentrated in red states…ouch.

FT: China says it can live without US farm and energy goods

But can American live without Chinese good??

A forest of olive branches seemed to be on offer from the US to get the Chinese to come back to the table to negotiate, from respect for their economic achievements to the offer of a deal to do a “beautiful rebalancing” of the world economy.

And there is a widespread view that there is no need for countries to retaliate, when the CEOs of Walmart and Target are telling the President privately that there will be empty shelves from early May.

The collapse in container traffic from China to the port of Los Angeles – the main artery of the world economy for the first quarter of the 21st century – is the one to watch. The IMF’s boffins say they can start to see the impact from space as satellites track fewer, increasingly empty ships leaving China’s ports. Of course this will be denied by the US.

https://www.bbc.com/news/articles/c4g45zp77y5o

This article puts the numbers into perspective:

“The impact of the diminished freight container traffic to North America will be significant for many links in the economy and supply chain, including the ports and logistics companies moving the freight. If each sailing was carrying 8,000 to 10,000 TEUs (twenty-foot equivalent units), that would equal a decline in freight traffic of between 640,000-800,000 containers, and lead to decreased crane operations at the ports, lower fees that could be collected, and declines in container pick-ups and transports by trucks, rails, and to warehouses for storage.”

https://www.cnbc.com/2025/04/16/trade-war-fallout-china-freight-ship-decline-begins-orders-plummet.html

***

Yes, you read that correctly — 800.000 sea containers that aren’t on their way from China to the US.

And that was the situation on April 16. Since then, there’ll have been even more cancellations.

Well that is 800,00 less trucker movements needed.

A lot of truckers meals and less diesel used.

Let alone less dockers getting overtime

From the article:

‘Whoever wins in Canada’s election will bring that G7 economy firmly back into this globally transformative debate. Could the newly elected Canadian PM start a full fat negotiation with the UK too? And then he will chair the G7 Summit in Canada in June as President Trump’s 90 day deadline expires. It is presumed Donald Trump will travel to Alberta, to the country he claims should be part of his own.’

Hard to imagine how any government official could be so immersed in an alternate reality:

“Treasury Secretary Bessent says it’s up to China to de-escalate trade tensions”

https://www.cnbc.com/2025/04/28/treasury-secretary-bessent-says-its-up-to-china-to-de-escalate-trade-tensions.html

***

First gem:

““I believe that it’s up to China to de-escalate, because they sell five times more to us than we sell to them, and so these 120%, 145% tariffs are unsustainable,” Bessent said during an interview on CNBC’s “Squawk Box.””

*No comment required 🙈

***

Second gem:

“In addition to his assessment of the situation with China and other Asian countries, Bessent charged that European nations are likely “in a panic” over the strength of the euro against the U.S. dollar since the trade tensions began. The euro has risen nearly 10% this year against the greenback after the currencies had reached near parity in early January.

““You’re going to see the [European Central Bank] start cutting rates to try to get the euro back down,” Bessent said. “Europeans don’t want a strong euro. We have a strong-dollar policy.””

*Mr. Bessent — de euro isn’t up…it’s the dollar that’s down. And Europe is delighted with that, because our imports of oil, gas and other commodities are now a lot cheaper. It’s not affecting our exports, because the euro is more-or-less flat compared to other major trading currencies other than the dollar, and exports to the US are stagnating anyway, due to tariffs. Further: the ECB has been reducing interest rates for months now, because inflation in the EU is under control — unlike the situation in the US. And, despite the lower rates in the EU, investors continue to flock to euro-denominated securities…which is a big thumbs-down for the dollar.

Please enroll for an online course in basic economics.

#TheBlindLeadingTheLame

Unless there’s something else going on at the ruling elite level.

Quiet Rebalancing going on beneath the chaos?

> BREAKING: Airbus announces definitive agreement with Spirit AeroSystems to acquire factories and A350, A321, A220 program work spread across North Carolina, France, Morocco & Belfast, NI. Spirit pays $439 million to Airbus to take the factories as it heads to market exit.

https://x.com/jonostrower/status/1916707135985168573

Cool. Wonder how Spirit will shake out for the other guys.

The other guys will be enjoying the privilege of adding Spirit’s $5.4B in debt to their own debt mountain…in addition to acquiring Spirit USA’s low-motivation workforce 🙈

Yes. I fail to understand how the Spirit acquisition in itself benefits Boeing. There is a lot on their plate without it..

@Vincent

This doesn’t benefit Boeing. It only stops insolvency of Spirit. Spirit was not making money on its own and now they can not make money as a piece of Boeing.

Maybe next time don’t spin of your business parts and shake them down for the lowest possible price.

You’re not wrong.

In the short-term, Boeing is going to have a heck of a time and it’s going to cost them some money.

This is a long-term play. For one thing, it demonstrates (perhaps to the FAA and customers) the shift in mentality. BA will have better control as it re-integrates vertically.

It was probably a necessary step in the direction of proving that.

“..low-motivation workforce..”

Yea verily; and it co$ts bags of money to fix that one. Management

handwaving ain’t gonna cut it.

> Airbus takes over part of Spirit’s Belfast plant

European aircraft manufacturer may yet acquire other elements of Belfast site in €387m deal

> At the time of the deal’s initial announcement in July 2024, Airbus said it would pay $1 for the Spirit assets it was acquiring, and receive $559 million in compensation. Airbus said on Monday that the compensation amount has been adjusted to reflect revised transaction perimeters.

> The facilities that Airbus is taking over are crucial to the European planemaker’s aircraft programmes, and have struggled to keep up with Airbus’s timetables to increase output.

https://www.irishtimes.com/business/2025/04/28/airbus-to-take-over-spirits-belfast-plant-as-part-of-boeing-reintegration/

Airbus announcement:

https://www.airbus.com/en/newsroom/press-releases/2025-04-airbus-signs-definitive-agreement-with-spirit-aerosystems

The deal still needs to be greenlighted by regulators…which is not expected until July at the earliest.

Under the deal, Airbus will take ownership of the following Spirit AeroSystems sites and production lines:

Kinston, North Carolina, U.S. (A350 fuselage sections)

St. Nazaire, France (A350 fuselage sections)

Casablanca, Morocco (A321 and A220 components)

Wichita, Kansas, U.S. (A220 pylons production)

Belfast, Northern Ireland (A220 wings and A220 mid-fuselage production, unless Spirit finds a third-party buyer for the mid-fuselage activities)

Prestwick, Scotland (wing components for A320 and A350 programs)

Separately, Spirit AeroSystems plans to divest its Subang, Malaysia site to an independent third party.

“…unless Spirit finds a third-party buyer for the mid-fuselage activities…”

I found it interesting that AB apparently isn’t interested in these particular operations in Belfast — meaning that they’ve seemingly found another source for their A220 mid-fuselage sections…

Maybe Tata from India to take over production of A220 mid fuselage in NI? Seems like A220 Mid Sections made in NI and China?

video of A220 mid section production in China

https://www.youtube.com/watch?v=qp2tJUroFBE

older article with pic of A220 mid section in Belfast Northern Ireland

(looks like a NI operation is very labor intensive process)

https://www.aero-mag.com/bombardier-belfast-spirit-aerosystems-26102020

@ David

Looks like China will be the lead (or only) producer for the A220 mid-fuselage sections going forward…perhaps as a carrot to lure A220 orders from Chinese regional carriers?

Tata may, indeed, be a good candidate for the “redundant” NI operations. India wants to build a home-grown regional airliner, and this might be a useful resource in that endeavour.

> Apollo predicts a recession (and stagflation) coming to the US by June with mass layoffs in trucking and retail

> Wall Street Journal now reporting that Jamie Dimon told investors last week that the *best case outcome* is now a recession for the U.S.

This was at the same closed door meeting where Bessent told the same investors that the current tariffs on China are unsustainable.

> CNBC: Agriculture isn’t nearing trade war tariffs crisis — ‘it is a full-blown crisis already’ farmers say.

> International students rethinking US college plans amid visa policy shift

[So I guess Fortress America doesn’t need foreign students anymore]

Donnie says that the tariff money is pouring in…and, yet, the US Treasury will be borrowing $514B in Q2, which $391B *more* than announced a few weeks ago…

https://www.forexlive.com/news/us-q2-treasury-borrowing-estimate-soars-to-514-billion-20250428/

Reuters: “US aviation industry slammed by tariffs, seeks exemptions”

“Airlines have been cutting flights in response to softening bookings. They have also been scrapping their financial forecasts and trying to control costs in a bid to protect margins. They are also pushing back against price increases for aircraft and parts as planemakers and engine makers seek to pass along the tariff costs.

“Airline executives have even raised the possibility of returning leased planes and deferring aircraft deliveries.

“”It’s really difficult for us to wrap our heads around paying tariffs on those airplanes,” May said. “It just doesn’t make economic sense.””

“Boeing expects a tariff hit of less than $500 million a year. Jet-engine maker GE Aerospace has estimated its tariff bill would exceed $500 million. Its rival RTX expects about $850 million in additional annual costs.”

“Boeing is paying 10% duty on supplies from Italy and Japan. United Airlines CEO Scott Kirby this month said Airbus has had to pay tariffs on planes it is building in Alabama.”

“One airline executive said carriers could have taken the tariffs in stride if travel demand was booming. But bookings have softened in the past two months, weakening their pricing power.

“Airline fares in March posted their steepest month-on-month decline since September 2021, according to data from the U.S. Labor Department. Carriers have been lowering fares to stimulate demand.”

https://finance.yahoo.com/news/us-aviation-industry-slammed-tariffs-100328935.html

Feom the article:

“GE Aerospace (GE) estimates that aircraft departures will now decline in North America, which accounts for 25% of global traffic, as a result of cuts in flight schedules. Aircraft departures drive aftermarket services business.

The company said a slowdown in departures tends to start having an effect on its business in about four quarters.”

AW

“Comac C919 To Get European Approval In 3-6 Years, EASA Chief Say”

Oops

> The Truman lost an F/A-18 and a tow tractor at sea

https://x.com/beverstine/status/1916919761369272611

> So far this deployment, F/A-18 lost to friendly fire, a merchant vessel collides with the ship and an F/A-18 falls overboard.

Oops

> UPDATE: A US official said that initial reports from the scene indicated that the Truman made a hard turn to evade Houthi fire, which contributed to the fighter jet falling overboard.

https://x.com/NatashaBertrand/status/1916933113026150862

“It made headlines in February when it collided with a merchant ship near Egypt; no injuries were reported. Another F/A-18 from the Truman was also “mistakenly fired” upon and shot down by the cruiser USS Gettysburg in the Red Sea in December; both pilots ejected safely.

“Other US Navy ships in the region have also come under Houthi fire. In early 2024, a US destroyer in the Red Sea had to use its Phalanx Close-In Weapon System, its last line of defense to missile attacks, when a Houthi-fired cruise missile got as near as a mile away – and therefore seconds from impact.”

Looks like the Houthis are causing as much distress as the Taliban used to — again demonstrating how effective guerilla tactics are against “old school” warfaring techniques.

The US should have asked the EU about its experiences during the ongoing ASPIDES mission in the Red Sea, rather than rushing in to a hornets’ nest…

Delta Routes New Airbus Plane to Tokyo to Sidestep Trump Tariffs

“Delta Air Lines Inc. is flying a new Airbus SE plane through Japan to skirt US import tariffs as President Donald Trump’s trade war threatens the flow of new jets to the the aviation industry.

The A350-900 aircraft is set to leave Toulouse, France, home of Airbus’s main manufacturing facility, on April 30, arriving in Tokyo on May 1, according to data from FlightAware, an online tracking provider.”

“Chief Executive Officer Ed Bastian said on April 9 that the airline “will not be paying tariffs on any aircraft deliveries” and he’d made it “very clear” to Airbus that he would defer any planes carrying a tariff. American Airlines Group Inc. CEO Robert Isom also later vowed not to pay levies. “

Delta used a similar trick during the Trump I tariffs years ago 👍

Flight “canceled”?

https://www.flightaware.com/live/flight/DAL9936/history/20250430/0910Z/LFBO/RJAA

maybe not tariff free A350 after all

“UPS to cut 20,000 jobs on reduced Amazon deliveries, as US tariffs weigh”

That’s also going to have a significant effect on air freight…

comment based on the idea of Amazon publishing tariffs on invoices

“Commerce Secretary Howard Lutnick echoed Levitt’s comments, saying it’s a hostile act if a company goes out of its way to “make it seem” like tariffs have caused prices to change.

“It’s nonsense,” he said Tuesday in a CNBC interview. “A 10% tariff is not going to change virtually any price,” he added, referring to the nearly universal baseline tariff on all countries. “The only price will change would be a product that we don’t make here, like a mango.” The 10% tariff, however, is hardly the only one in effect.”

“A 10% tariff is not going to change virtually any price,”

seems they don’t know how much is comes in from China with 145%

They really haven’t a clue, have they?

And to think that we have a commenter here who regularly suggests that all info in and from China is manipulated to suit the CCP’s agenda…🙈

😂 They aren’t going to be fooled by a dog and pony show

CBS News: 90% of Americans think tariffs will drive up prices and cost the U.S. more money than they generate, according to a new Gallup poll .

Teamsters Response to UPS Earnings Call

“The following is a statement from Teamsters General President Sean M. O’Brien on the announcement from UPS in today’s earnings call that the delivery and logistics company anticipates cutting 20,000 jobs this year:”

“United Parcel Service is contractually obligated to create 30,000 Teamsters jobs under our current national master agreement.”

So that 50K employment swing for UPS….

> UPS is warning that US small businesses are suffering more than China from tariffs

> The Atlanta-based shipping company revealed that its China-to-US trade lanes, which account for 11% of UPS’s total international revenue, are its most profitable business channels. […]

Small and medium-sized businesses appear particularly vulnerable to the brewing trade war, with Tome noting that “many of our small and medium-sized businesses are 100% single-sourced from China.”

These smaller enterprises, lacking the financial resources of larger corporations, face difficult decisions as they contend with potential tariff increases that could significantly impact their operations and profitability. […]

UPS is responding to these challenges with significant operational restructuring, with Tome announcing the company “will complete 164 operational closures, including 73 building closures by the end of June.” […]

For the second quarter, UPS forecasts… average daily volume… roughly 9%.

> Amazon will start displaying how much of an item’s cost is derived from tariffs – right next to the product’s total listed price.

> Q: “Amazon will soon display…how much the Trump tariffs are adding to the cost of each product. Isn’t that a perfect, crystal clear demonstration that it’s the American consumer….who is going to pay for these?”

Leavitt: “This is a hostile and political act by Amazon.”

> Amazon’s plan to show the extra cost of goods due to tariffs is a “hostile act,” Trump’s spokeswoman said.

> CNBC: Port of Los Angeles expects 35% slump in shipping volume next week

> Adidas warns it will raise prices on all U.S. products due to tariffs

BW: “On his 100th day in office in 2017 Trump headed to a PA wheelbarrow factory to launch his trade policy and put the US on the path to today’s tariffs.

Eight years on that factory is closed. The wheelbarrows are now made in China.”

“President Donald Trump’s effort to revitalize U.S. manufacturing with sweeping tariffs on Chinese goods may hit a snag: American factories depend on machines from China to make everything from cars to electronics.”

https://x.com/NorthropKatrina/status/1916791400244408455

WaPo: Tariffs on Chinese-made machinery drive up costs for U.S. manufacturers

“It appears Newark Airport in NYC is suffering from yet another major equipment (radar) outage that has forced a ground stop.”

https://bsky.app/profile/willguisbond.com/post/3lnvkdmltic2q

Airbus to U.S. Airlines: We Won’t Pay Your Tariffs

“Airbus Chief Executive Guillaume Faury has set the stage for a tussle with U.S. airline customers, saying the planemaker won’t cover the cost of tariffs for imported aircraft.

“We will not, as far as Airbus is concerned, pay tariffs for planes that are going to the U.S.,” Faury told reporters after the company announced its first-quarter earnings. “We are sitting with them to find ways to deal with it in the short term.”

“Airbus Reports Healthy First Quarter 2025 Results”

“Airbus kicked off 2025 with solid top-line growth and a healthy order book, despite supply-chain pressures tempering its delivery cadence.

“In the first quarter ending on March 31, Airbus reported revenues of €13.5 billion, a 6% year-over-year increase, and an adjusted EBIT of €624 million, an 8% increase despite delivering six fewer commercial jets than in Q1 2024 (136 vs. 142).

“Guillaume Faury, Airbus CEO, highlighted the “progress we are making on our priorities across the business,” while cautioning that “specific supply chain challenges” have back-loaded deliveries. Indeed, Airbus delivered 17 A220s, 106 A320 Family jets, four A330s, and nine A350s, aiming to ramp up the A320 line to 75 aircraft per month by 2027 and the A220 to 14 per month by 2026.”

https://airwaysmag.com/new-post/airbus-healthy-q1-2025-results

***

“Airbus says keeping 2025 forecasts despite US tariff uncertainty”

“Paris: European plane maker Airbus said Wednesday that it was sticking to its full-year forecasts for now, including delivery of around 820 aircraft, even though uncertainty over US tariffs has roiled supply chains worldwide.”

https://thepeninsulaqatar.com/article/30/04/2025/airbus-says-keeping-2025-forecasts-despite-us-tariff-uncertainty

Lutnick

“You go to the community colleges, and you train people!” he says, before listing two universities—Arizona State University and Grand Canyon University—that are decidedly not community colleges.”

“You know, this is the new model where you work in these kinds of plants for the rest of your life and your kids work here and your grandkids work here.”

https://x.com/i/status/1917275438319129082

Well, if these “plants” are attractive enough to keep whole generations of families working there for life, then they must be giving *stunning* pay and other benefits…right?

And that’s going to be reflected in the price of the goods they produce…rendering them uncompetitive with products from developing industrial economies. So, these goods won’t be for export.

Moreover: more expensive goods + stunning remuneration = domestic wage-price spiral, which is inflationary.

***

It really is a three-ring circus there in DC.

Lutnick being worth $3 billion, wonder if he was ever on a factory floor much less work on one Guess not, “After graduating, Lutnick worked at Noonan, Astley & Pierce as a broker for the United States dollar–Japanese yen exchange” but that said, “At Haverford College, Lutnick became captain of the tennis team.”

Exclusive: Ryanair threatens to cancel Boeing order if tariffs impact price

“Ryanair would consider cancelling planes it has on order from Boeing if U.S. tariffs materially affect the price and look at alternative suppliers, chief executive Michael O’Leary said on Thursday.”

this is new tactic from the US government (security concerns on commercial aircraft)?

US lawmaker warns Ryanair against buying Chinese-made planes

“A senior U.S. lawmaker has warned Ryanair against purchasing Chinese-made aircraft due to security concerns, following comments by the CEO of the low-cost Irish airline that he would consider buying Chinese jets at the right price, according to a letter seen by Reuters.”

“Ryanair responded to the letter by saying it would consider cancelling planes it has on order from Boeing if U.S. tariffs materially affect the price and look at alternatives, including Chinese planemaker COMAC.”

…”security concerns”…?

Rather childish.

Also rather desperate.

The “invisible” hand, from working behind the curtain to the centre of the stage.

auto industry tariff work arounds

“Subaru’s Canadian division will stop importing the popular Outback model from the U.S., CEO Atsushi Osaki revealed last week.

Instead, Canadian dealers will now source their Outbacks directly from Japan, thanks to a free trade agreement that allows Japanese vehicles to enter Canada tariff-free”

“Mazda Canada announced it would pause production of CX-50 crossovers destined for Canada from its Alabama manufacturing plant.”

“Hyundai’s Canadian division is also shifting strategy, sourcing most of its Tucson lineup from Mexico rather than the U.S.”

“Meanwhile, Nissan scrapped plans to build electric sedans in the U.S., officially citing “industry market conditions.””

CNBC: L3 Harris tapped to modify Qatari jet as potential new Air Force One after years of Boeing delays

CNBC: Microsoft raises prices of Xbox video game consoles due to ‘market conditions’

Bloomberg: “Japan’s Finance Minister Katsunobu Kato said that the country’s US Treasury holdings could be a card in its trade negotiations with the US”