Leeham News and Analysis

There's more to real news than a news release.

Boeing 1H2025: Turnaround underway, led by revenue jump at Boeing Commercial and positive results at Defense

By Karl Sinclair

First half 2025 financial results.

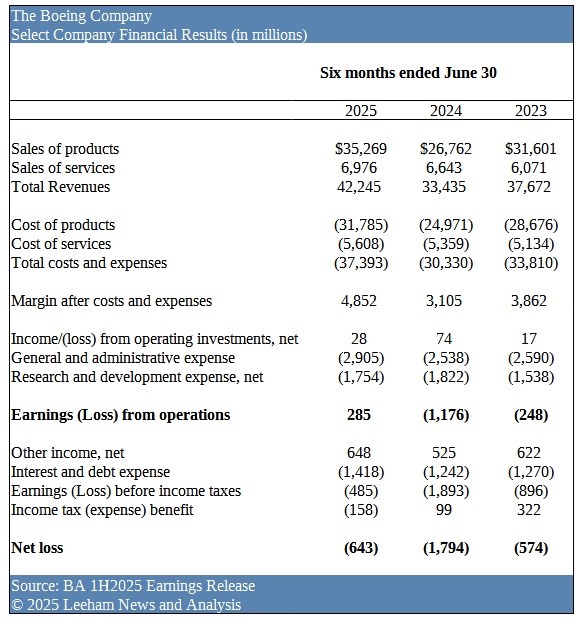

July 29, 2025, © Leeham News: The Boeing Company (BA) released 1H2025 results, and while the corporation still posted a net loss of ($643) for the first six months of 2025, strong revenues at Boeing Commercial Aircraft (BCA) indicate that the company has turned the corner and is back on track.

Revenues leapt $8.8bn, year-over-year (YoY), as did margins, which increased $1.747bn. This resulted in positive earnings of $285m for the period, a turnaround of $1.461bn.

The net loss for the period was driven by interest expense of $1.418bn, an increase of $176 YoY. However, results are a marked improvement over 2024, when the company had a loss of $1.794bn. Service revenues showed a marginal increase, while sales of products increased $8.507bn.

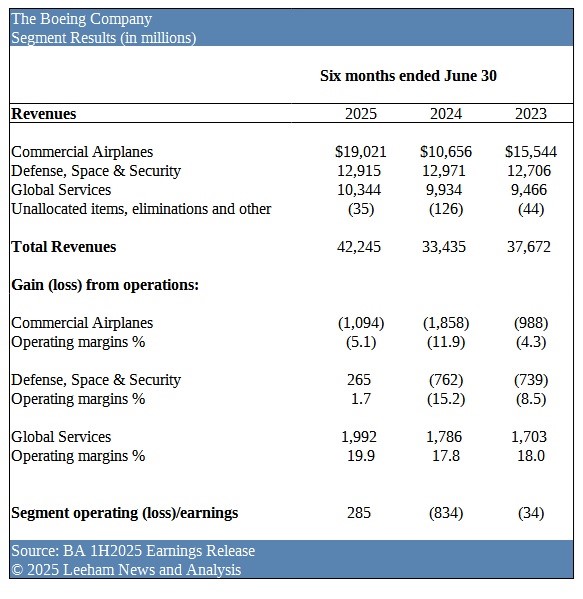

Segment Results

Strong revenues at Boeing Commercial Aircraft (BCA) drove the increase in sales, while the rest of the company posted relatively flat results for the period. While the loss narrowed at BCA, margins remained negative for the period, which was expected.

Boeing Defense, Space and Security (BDS) posted a small but positive result for the period, which was a surprising result. Expectations for the division were for negative margins throughout the year.

Boeing Global Services (BGS) continues a steady string of results, once again modestly increasing revenues for the period and delivering a 19.9% margin for the company.

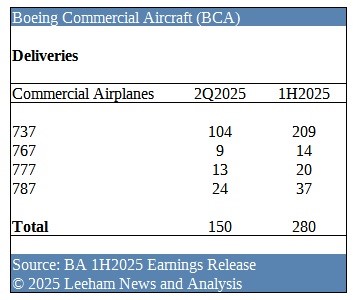

Boeing Commercial Aircraft (BCA)

Boeing Commercial Aircraft (BCA)

While deliveries remained flat for the 737 line, wide-body deliveries drove the jump in revenues, as 777 handovers jumped from seven in 1Q2025 to 13 in 2Q2025. 787 production handed over 24 aircraft during the quarter, an average of eight per month. While Boeing has declined to offer guidance on commercial aircraft deliveries for 2025 previously, results indicate a target of ~600 aircraft is an attainable goal for the division.

BCA was also able to trim the operating loss for the period, with an operating margin of (5.1%), less than half of what it was last year at (11.9%). The BCA backlog stands at 5,900 aircraft valued at $522bn.

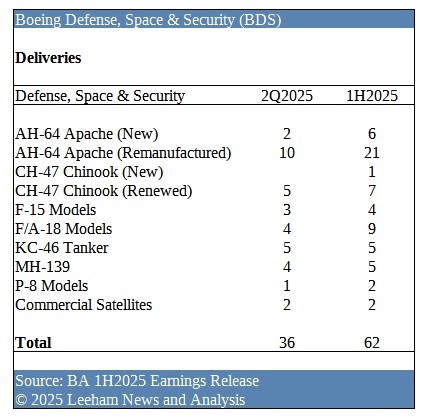

Boeing Defense, Space and Security (BDS)

The surprise result for the period is surely BDS, which was expected to drag company results down throughout the year.

Revenues were aided by deliveries of the KC-46 tanker aircraft and the MH-139 Grey Wolf helicopter during the second quarter. BDS posted a modest margin of 1.7% and while revenues decreased slightly over the same period last year, the result is undoubtedly a welcome change at the division. The $265m operating profit is a step in the right direction, as the company attempts to pivot away from fixed-price contracts, which hampered results in previous years.

The BDS backlog grew to $74bn at the end of 1H2025.

Boeing Global Services (BGS)

Services quietly continued its strong financial performance for the company, delivering revenues of $5.281bn for the quarter (an 8% increase over 2024) and margins of $1.049bn (a 21% increase over 2024).

This resulted in an increase of 210 basis points to 19.9% for the 1H2025 earnings margin.

While sales will dip at BGS, as non-core assets like Jeppesen are spun off over the coming 12 months, expectations are that the division will continue to add more than $3bn in earnings to the bottom line.

Company-wide

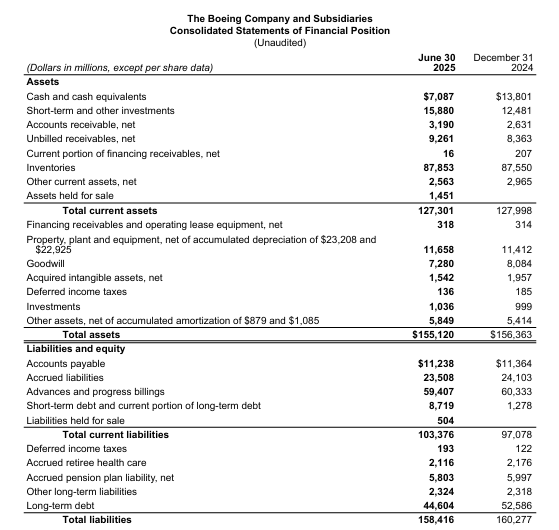

Interest expense is a growing concern for Boeing, with the combined debt load sitting at $53.3bn.

Source: The Boeing Co.

BA is expected to add ~$4.3bn to that amount, when it closes the deal to acquire portions of Spirit Aerosystems in 3Q2025. Cash and equivalents of ~$23bn will decrease in 2H2025, as $8.719bn of debt is expected to be retired by the company. Liquidity decreased by ~$3.2bn during 1H2025. The cash position will be ameliorated with the sale of Jeppesen and ForeFlight, to private-equity firm Thoma Bravo, for $10.6bn. The deal is expected to close by year-end, subject to regulatory approval.

Company results will be updated after the 1H2025 earnings call.

Good to see Boeing making progress and not having major program write-downs this quarter. Even on the fixed cost defense programs.

Fully on board with that.

The one caveat (to my very non financial view) is the 5 x KC-46A. Sudden burst of delivery reflects the crack issues.

Offset that is it was not a severe issue and the takeup of 10 options I believe it was in the original KC-X contract as well as extension of (75?) follow up orders.

The number of commercial aircraft delivered in Q2 (150) was the highest quarterly figure since 2018. Despite this, the operating loss at BCA was $557M, corresponding to an average loss per frame of $3.71M.

Average revenue per frame was $72.49M — which is pretty meager considering that a third of the delivered frames were widebodies.

Glass is 90% empty kind of thinking, vs half full. So it goes.

Its called a recovery for a reason.

Cash and cash equivalents shrank from $13,822M on Jan 1 to $7,796M on June 30, representing a H1 cash burn of $6,026M.

Current cash on hand is $7,087M.

Short term debt climbed in H1 from $1,278M to $8,719M. This has to be paid back within 12 months — and BA currently doesn’t have enough cash to do so. This excludes the additional debt at Spirit Aero.

https://www.prnewswire.com/news-releases/boeing-reports-second-quarter-results-302516005.html

They have $15.88bn in short-term investments

BA is proudly touting: “737 production reached 38 per month in the quarter”

The party didn’t last long: Planespotters is currently putting 737 MAX deliveries in July at 21…

Hi, do you have the number for Airbus? Thanks.

Ortberg talked a lot about KPI, but forgot the reality where the rubber hits the road?

Hi Pedro,

Over at AB, I’m counting 47 A320/321neo deliveries in July (19:00 CET).

Also:

5 A220s

6 A350s

1 A330 neo

***

The 737MAX figure for July now appears to have climbed to 27.

Also: 5 787s

Data from Aviation Flights shows Boeing on 33 MAX deliveries in July with a few hours to go. I’m not counting one that’s gone to the completion centre in China this week. I don’t know when that’s officially counted as delivered.

Airbus are on 50 A320 family, 64 overall.

Official numbers may be one or two out either way.

I’m only counting MAXs delivered from the line — not bothering to look for deliveries from the parking lot, since they’re not relevant to line rates.

I believe that different sites maintain different definitions of “delivered”. Planes entering the completion center in China are not counted as deliveries by PS — they’re only counted when they leave to go to the customer.

Russell and Abalone

Thanks everyone!

Ortberg spoke to the extension on the 737 MAX deicing certification, to 2026. He said they encountered some issues in testing with the redesigned inlet cowling for engine airflow, that caused them to back up a bit.

They don’t want to submit the final design to the FAA for certification, until the testing of the design changes is complete.

He also said there are no other open issues on the MAX-7 certification, which would imply either they are confident on the SMYD waiver, or they have removed it from the certification basis

I’ve been told the MAX was “as safe as any airplane that has ever flown the skies” by BA, back in 2019; BA also said that it would take one year to redesign the engine anti-ice system in January 2024.

I learned my lessons.

BTW United has taken delivery of its 39th A321neo. United also ordered an additional 40 A321 in May.

Good to see Boeing headed in (apparently) the right direction.

We’ll see how it goes.

At least it seems they aren’t repeating the mistake of jumping on any improvement as conclusive. Instead they are waiting to see if the improvement is stable over several months.

Basically they are working to margins rather than to minimums. That’s a huge and beneficial change in culture, long needed. It requires patience and discipline. I hope that continues.

Ortberg also said they are sticking with their plan for 737 production incremental increases of no more than 5 per month, and no less than 6 months apart. So he doesn’t foresee an increase from the current 38 rate for the rest of this year.

Also he said that at the 38 rate, one KPI fell out of the green, which was total rework hour reduction of 50% from the pre-shutdown levels. So they will work on stabilizing that before requesting the increase from the FAA.

Also mentioned that the Spirit acquisition will close later this year, and the fuselages arriving at Boeing for assembly are now meeting all KPI’s.

Worth noting is that Spirit is taking attention as well as financial costs.

Integration is not going to be a oh, we are one now and no issues.

Two entities having done things differently for many years might as well be a new acquisition. Easily into 2026 for the bulk and like Boeing itself, its going to be a work on progress for years, not one quarter to the next and, oh, its all done, we are golden.

Can Spirit ramp up??

Ortberg said they are watching suppliers and right now they already have the surplus inventory for the next production increase.

But they want to get away from holding that inventory so are encouraging suppliers to maintain their own, or have assured production capability.

He acknowledged supply is always a risk but they are factoring it into their estimates.

Reuters:

> Members of the machinists union at the defense division overwhelmingly rejected a four-year contract offer on Sunday.

==================

There’s an est $1.5 billion FCF headwind in Q3

Q2 FCF improvement:

> primarily driven by better PCA [BCA ??] delivery performance as well as some timing items.

Any mention of impact on EBITDA next year due to divestment of Jeppesen, etc?

I read that 2025 EBITDA of businesses sold varies from $300m to ~$660m.

Any bet when the MAX 10 is delivered to the first customer?

Unless BA has a solution within next few weeks, certification of the MAX 7 looks dicey for 1Q26

The stonk is down more than 4% today.

A few items noted regarding the 737 MAX certification:

> “We just haven’t closed the design,” he said. “We found some issues with the design implementation we had.”

Also 👇

> Boeing (BA) is working on a few items, including a redesign of the jet’s engine anti-ice system to address a safety issue

Explained above, from the earnings call.

Boeing:

“An effective engine anti-ice system requires a complex, integrated design as it touches different airplane systems,”

“The development team is maturing a technical solution that is one of the last steps* to certify the 737-7 and is important to certify the larger 737-10.”

You have to hate it when your stonk goes Down!

“The stonk is down more than 4% today.”

just a fyi

“Pakistan’s rookie carrier Air Karachi has recognized to talk to COMAC manufacturer to evaluate a possible order from C919, the most advanced commercial jet developed in China.”

Who said that the aircraft haven’t been certified by the FAA, therefore it can’t fly outside China?

It can be flown in any nation that recognizes and accepts the Chinese certification standards. Neither the FAA nor EASA does, and most nations follow one or the other.

There are exceptions, but the market outside China will remain limited.

ICYMI:

There are many flights of Chinese aircraft flying outside China. Hahaha.

Not that long ago, Chinese cars are “craps”, now BYD outsells Tesla in Europe, GM is the largest importer of Chinese vehicles in Mexico and the US automakers are hiding behind the tariff wall.

C919 is flying in China with less than 30 total aircraft. Prospective customers are Cambodia, Indonesia, Kazakhstan, and now potentially Pakistan.

A few nations have granted permission for C919 operations in their airspace. No Western country has.

Time to wake up!

According to BA ‘s commercial market forecast, the Chinese market is bigger than that of N America. Emerging market will represent over 50% of the global commercial fleet. China, South and Southeast Asia will account for 50% of the growth in the global air fleet.

Does not change anything. C919 is self certified, funny how some hate Boeing for the FAA cert issues but its just fine for a completely opaque China cert.

Trust us, we are the Chinese Dictatorship. The same ones that will not release the findings on the 737-800 suicide. And no, I don’t trust the US Administration though in the case of the FAA, we have the cross check of EASA. Both AHJ should question the other regardless.

COMAC can’t even build C919 at any serious rate. I can see the Indochinese airlines lining up and, oh, we will sacrificial ours to our Brothers in North Korea!

So in theory, China shorts itself for a publicity stunt. Then they buy more Airbus jets to back fill that (ahem) loss.

But as noted, they will not be flying into Japan, Australia or Singapore.

Oddly COMAC could apply for a Experimental Category in the US and fly it around!

Airbus results are out — time for some benchmarking.

H1 commercial aircraft:

306 deliveries, revenue €20,829M, EBIT 1,231M.

That gives average revenue per frame of €68.07M ($78.08M) and average EBIT per frame of €4.022M ($4.614M).

The correspindong BA figures posted above: $72.49M and -$3.71M (loss).

So, despite having proportionally fewer widebodies in the mix, AB is securing a higher average price per frame.

Why does BA continue the unsustainable discounting? Is it an attempt to win back market share?

Any updates?

Early 2025: Boeing removed 38 777X from backlog in recent weeks

> That document breaks out order figures by the first-generation 777 and the 777X. It says that at end-2024 Boeing held unfilled “firm” orders for 358 777X, down from 396 three months prior.

62 orders for 777X in first half 2025.

Have BA reversed those removed from the backlog? Why?