Leeham News and Analysis

There's more to real news than a news release.

GE Aerospace Q3 2025 Earning Lifts Guidance On Record LEAP Output And Strong Services

By Chris Sloan

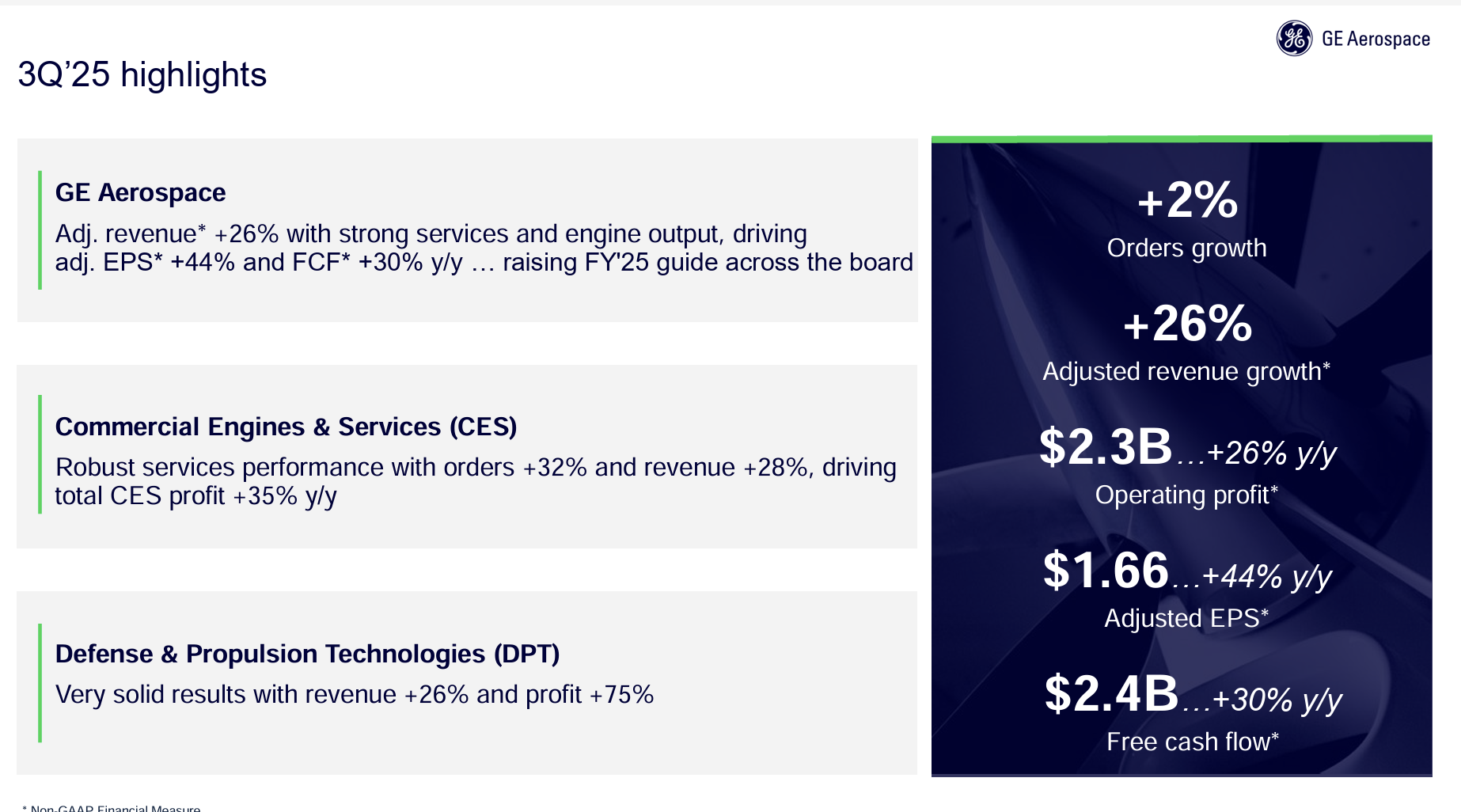

October 21, 2025, © Leeham News: GE Aerospace reported third-quarter results today, marking another period of broad-based momentum as the company raised its full-year outlook on stronger services and record engine deliveries.

October 21, 2025, © Leeham News: GE Aerospace reported third-quarter results today, marking another period of broad-based momentum as the company raised its full-year outlook on stronger services and record engine deliveries.

“GE Aerospace delivered an exceptional quarter with revenue up 26%,” said Chairman and CEO Larry Culp Jr. “Given the strength of our year-to-date results and our expectations for the fourth quarter, we’re raising our full-year guidance across the board.”

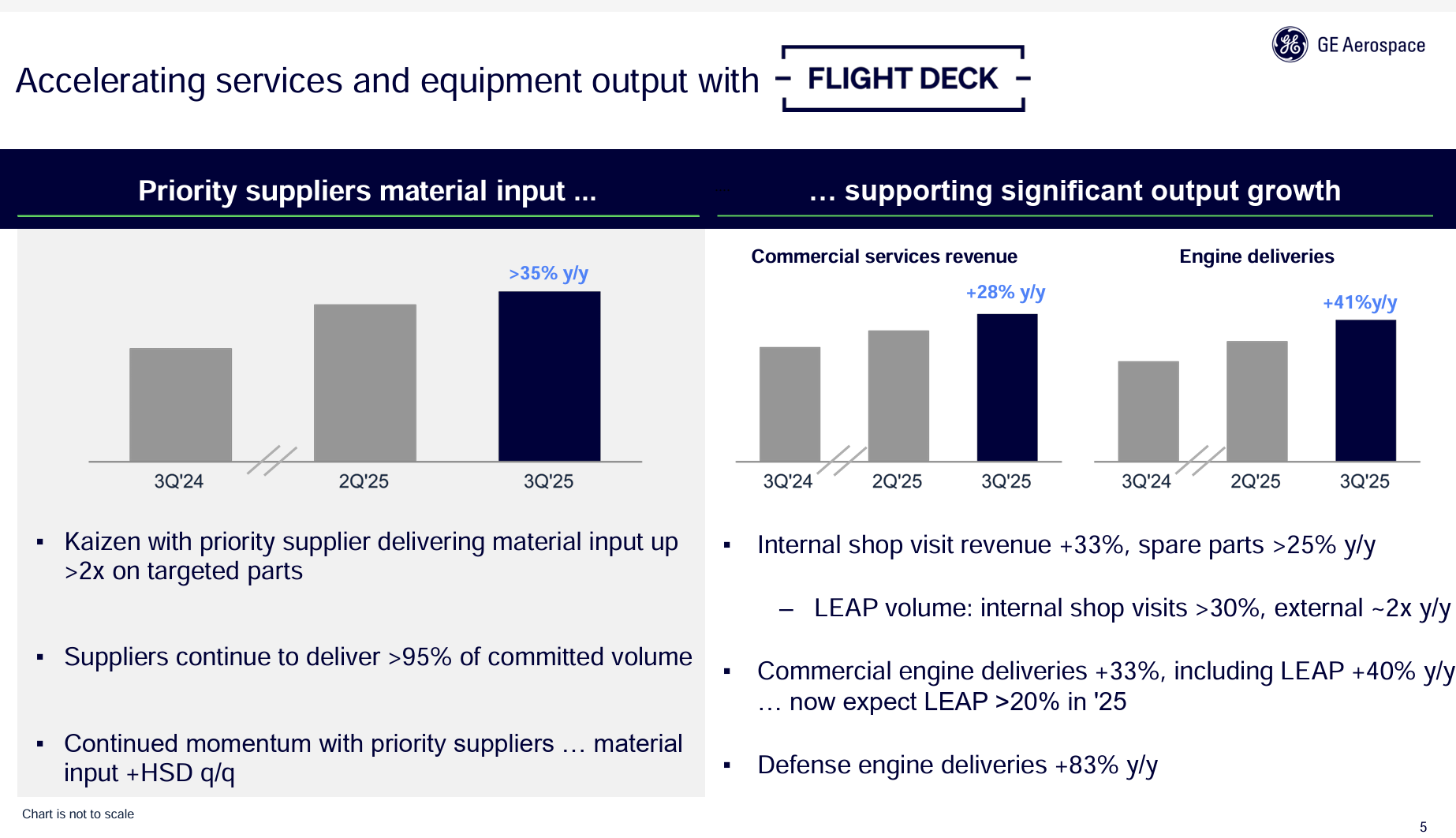

Improved material flow from key suppliers—up more than 35% year-over-year—helped drive the surge. Services revenue rose 28%, while engine deliveries climbed 33%, including record LEAP production up 40% from a year ago. Culp said the company’s operational rhythm continues to compound in the right direction reflecting both supply chain stability and persistent demand for narrowbody powerplants.

The quarter also brought several high-profile commercial wins. Korean Air announced the largest fleet commitment in its history—103 Boeing aircraft powered by a mix of GE9X, GEnx and LEAP-1B engines—along with a long-term services deal. Cathay Pacific expanded its GE9X order, adding 28 engines to bring its total to more than 70 for 35 Boeing 777-9 aircraft. The GE9X program continues to advance testing and durability work even as Boeing’s 777-X certification slips further into 2026.

Culp emphasized GE Aerospace’s depth of experience and installed base, noting that the company now supports 78,000 engines in service and has logged more than 2.3 billion flight hours. “With seven commercial engine certifications in the last two decades, this is an experience-based business that keeps us close to our customers,” he said.

Chief Financial Officer Rahul Ghai said GE expects roughly 2,000 LEAP engine shipments in 2025 and steady GE9X deliveries. “Our volume assumptions for 9X have not changed since July,” he said. “We do expect 9X losses to more than double year-over-year as we think about 2026, which will offset some of the positive growth we’ll see from Services.”

LEAP output hits record pace as durability upgrades advance

GE Aerospace’s LEAP program continued to set the pace in the third quarter, anchoring the company’s growth across both the Airbus A320neo and Boeing 737 MAX families. Engine deliveries surged 41% year-over-year and 18% sequentially. Commercial shipments climbed 33%, led by record LEAP production, up 40% from a year earlier — a clear sign that supply chain recovery is translating directly into output.

The CEO said progress on the LEAP durability roadmap remains a top priority. “We continue to advance on our durability roadmap,” Culp said. “With our next iteration of the LEAP-1A high-pressure turbine blade now in production, that will further enhance output.”

Durability has been a lingering issue for LEAP operators, especially those flying in hot, sandy climates where blades experience accelerated wear. Culp said the new LEAP-1A durability kit, centered on the redesigned turbine blade, is showing encouraging early performance. “We’re very pleased with the performance of the durability kit on the LEAP-1A — the new blade, which is at the heart of that kit,” he said. “We think that will drive a two-times improvement — think 8,000 cycles in harsh environments, 17,000 cycles in neutral environments. So far, so good — no surprises in that regard.”

Development work on the LEAP-1B equivalent, which powers the 737 MAX, is running on schedule. “We’re expecting to see that come through the pipeline in the first half of next year,” Culp said. “It’s probably a multi-year effort to upgrade the installed base. Having the LEAP-1A durability kit already in production helps, and we’re tending to the aftermarket now. We’ll do the same thing with Boeing once we’re on the other side of certification.”

The CEO called the early field data “fundamentally encouraging,” noting that the upgrades will pay off in longer time-on-wing, better reliability, and ultimately stronger customer economics. “No surprises to date — a lot of work still ahead of us — but fundamentally we’re encouraged by the impact this will have on durability and, in turn, on performance for our customers,” Culp said.

LEAP services surge as shop throughput and MRO capacity expand

Momentum in LEAP aftermarket operations gathered pace through the third quarter, reflecting stronger engine throughput and a maturing global maintenance network. The CEO said two priorities continue to guide the program: improving turnaround times and expanding capacity to match customer demand.

“For example, we’ve made progress with LEAP turnaround time at our Malaysia MRO shop,” Culp said. “Our team there improved flow and delivered a 30% reduction in engine disassembly time.”

That kind of operational improvement is starting to ripple across the network. Total internal LEAP shop output grew by more than 30% during the quarter, and GE is adding new capacity to sustain the trend. “This quarter, our ZEOS MRO facility in Poland completed its first LEAP shop visits,” Culp said. “Our LEAP third-party MRO network also continues to grow rapidly, with external shop visits up roughly twofold.”

The CEO described the roadmap to 2028 as one built on several reinforcing levers: better field performance, stronger material flow, and continued cost discipline. “We’ve been making improvements in the supply base, in the field, and in our shops,” he said. “The durability kit on the 1A is now in service, and material flow is starting to unlock additional productivity. There’s a lot of work to do between now and 2028, but the underlying product improvements give us real conviction in the roadmap.”

Ghai said the steady progress on LEAP’s field performance is key to sustaining that momentum. “All those things are helping, and durability is kind of hanging in there,” he said. “With the introduction of the durability kit, we’re very confident of getting to CFM56 levels of performance on the LEAP-1A — and soon on the 1B — as we look forward to 2028. That’s what gives us confidence about the trajectory we have on LEAP.”

Services momentum builds across fleets, with CFM56 seeing extended life

GE Aerospace’s services engine kept humming in the third quarter as operational momentum accelerated across the commercial fleet. Improved material flow and rising shop throughput are powering record aftermarket activity, led by the LEAP family — with a clear spillover effect benefiting older engine lines such as the CFM56.

The CEO said the company’s legacy narrowbody program continues to deliver well beyond its expected life cycle. “While CFM56 continues to fly for longer, and with the fleet size expected to triple by 2030, we’re also expanding capacity and capabilities to reduce turnaround times and improve shop-visit output,” Culp said.

Material input from key suppliers increased more than 35% year-over-year and by high single digits sequentially, helping unlock output across GE’s global network. Those gains are feeding directly into higher engine inductions, better parts flow, and stronger recovery in spare-parts fulfillment — long-standing constraints for the business.

Chief Financial Officer Rahul Ghai said the combination of improved material flow, heavier work scopes, and resilient demand has pushed services well ahead of plan. “We had a really strong quarter on services,” Ghai said. “We were expecting high double-digit growth for the year, and year-to-date results are at about 25%. So now we’ve raised the outlook to mid-20s growth. The improved outlook is both in our shop-visit revenue and in spare parts, driven by the strength we observed in the third quarter.”

Ghai said engines across the fleet are now entering more intensive shop visits as they mature in service. “Worldwide shop visits have still not recovered from 2019 levels, so there’s a lot of pent-up demand,” he said. “We’re beginning to see on the GE90 that the second shop has come through — and that can be 60% to 70% heavier than the first. The same trend is happening on the LEAP and on GEnx.” Larger work scopes are adding depth to the services backlog and increasing average revenue per visit as fleets age.

The durability upgrades now being introduced are extending time-on-wing for the LEAP, easing some near-term pressure on capacity, but overall demand still outpaces supply. “Our output has been increasing, but we are still behind on meeting demand,” Ghai said. “Even with the spare parts we have, there’s still a gap. As we look forward into 2026, we expect departures growth in the 3–4% range, but the number of engines coming off wing will be up double digits. That difference between departure growth and spare-parts demand will persist for a while.”

Backlog levels remain unusually strong. “Ninety percent of the spare parts we need to ship in the fourth quarter are already in the backlog — about 15 points higher than historical levels,” Ghai said. He described the commercial environment as “better than three months ago,” noting that air-traffic growth has stabilized and that both narrowbody and widebody fleets are feeding a healthy pipeline of future shop visits. “We don’t expect 2026 to match the pace of 2025, but we should normalize toward the double-digit growth we’ve projected over the medium term,” he said.

Supply chain steadies as collaboration deepens

GE Aerospace’s manufacturing system showed further signs of stabilization in the third quarter, as sustained process discipline and closer coordination with key suppliers helped ease production bottlenecks. The CEO said the company’s cross-functional teams are now working more seamlessly with partners to address constraints and lift output.

“Our team is working better cross-functionally to deliver improved outcomes, and in turn, accelerate the same type of collaboration with our supply base,” Culp said. “For example, this quarter we partnered with a critical supplier to address several key constraints utilizing Flight Deck tools, This resulted in the supplier improving first-time yields meaningfully and, in turn, delivering more than a twofold increase in output.”

Culp said the company’s hands-on approach at supplier sites is driving steady improvement in throughput and yield quality. “The common denominator is where we’ve been able to go in around these priority suppliers — which are either current constraints or anticipated bottlenecks — and really get out on the factory floor, staring down a problem at a machine or an assembly line,” he said. “It’s truly collaborative — our best engineers working alongside their best engineers, not negotiating on the factory floor but identifying the problem, containing it in the short term, and putting in permanent corrective action going forward.”

He acknowledged that progress remains uneven, but said the underlying system is more resilient than a year ago. “There are fits and starts we manage every day, every week,” Culp said. “But we’ve gotten better at it, and going forward, we want to be not just excellent at near-term problem solving but also ensure we’re investing time and talent to get ahead of those issues in the medium and long term.”

For the third consecutive quarter, GE’s priority suppliers shipped more than 95% of their committed volume — a sign that supply chain rhythm is beginning to hold.

Next-generation propulsion: early testing, hybrid potential

Alongside its focus on near-term execution, GE Aerospace is accelerating work on its next wave of propulsion technologies. Culp said the company recently began dust-ingestion testing on next-generation high-pressure turbine blades developed for the CFM RISE compact core.

“This marks the earliest we’ve ever started this type of testing in development,” he said. “While we’re investing in compact core for RISE technologies, there could be applications of these learnings for today’s fleet as well.”

GE is also extending its reach into hybrid-electric propulsion through its collaboration with Vermont-based Beta Technologies. “Something we’re really excited about is our $100 million investment in Beta Technologies,” Culp said. “We really like the team, the underlying technology, and our collaboration to co-develop a hybrid-electric turbogenerator. We think it will yield benefits for both of us — in defense applications and, ultimately, in the commercial space.”

Financials: Another record quarter lifts full-year 2025 outlook

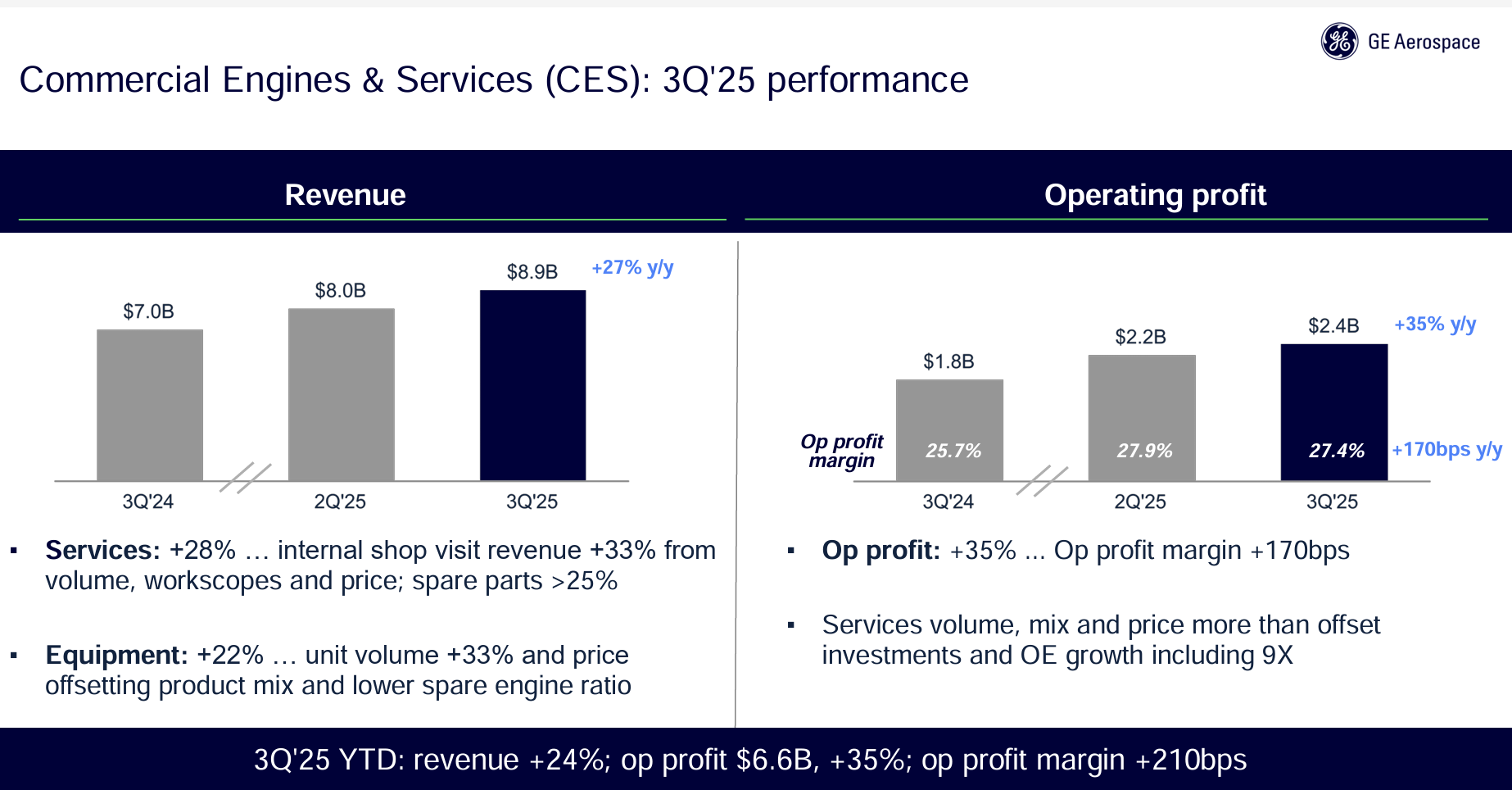

The propulsion maker delivered another strong quarter, powered by Commercial Engines & Services (CES), and lifted its full-year outlook. Total company revenue rose 24% year-over-year to $12.2bn, while operating profit increased 26% to $2.3bn. For the first nine months, revenue climbed 19% to $33.1bn, and operating profit advanced 29% to $6.8bn. The operating margin held steady at 20.3%, reflecting continued strength in services and disciplined cost control.

CES once again led the charge. Third-quarter revenue rose 27% to $8.9bn, driven by higher shop visits, strong spare-parts demand, and record LEAP engine deliveries. CES operating profit increased 35% to $2.4bn, with a segment margin of 27.4%, underscoring the sustained rebound in commercial aftermarket activity.

On the back of these results, GE Aerospace raised its full-year 2025 guidance. The company now expects adjusted revenue growth in the high teens and operating profit of $8.65–$8.85bn, up from $8.2–$8.5bn previously. CES is forecast to deliver low-20s-percent revenue growth and segment operating profit of $8.45–$8.65bn, an improvement from the prior $8.0–$8.2bn range.

Analysts were broadly upbeat on the performance and raised outlook. Seth M. Seifman, CFA, of J.P. Morgan, said GE’s quarter “should contribute to a positive stock reaction,” noting that strong services growth and higher guidance “show continued momentum in the commercial engine business.”

Karl Oehlschlaeger of Vertical Research Partners summed it up more succinctly: “GE starts the season in fine form, firing on all cylinders. Engine aftermarket continues to rock. Another cracking quarter from GE, showing the continued strength of the aero-engine sub-market.”

I wonder how those LEAP durability upgrades will pan out,

and how much of an drag they will be on GE.

We won’t be hearing results like this over at P&W/Raytheon…🙈

Ohh really…☺️

Ask and you shall receive..

GE revenue growth: 26%

P&W revenue growth: 16%

GE Q3 profit: $2.3B

P&W Q3 profit: $751M

P&W:

“Chief Financial Officer Neil G. Mitchill Jr. said the outlook for Pratt’s negative engine margin remains unchanged—still within the $150–$200m year-over-year headwind”

“On customer compensation payments related to the GTF fleet, Mitchill said the financial outlook “remains consistent” with prior guidance. “We’re right on track with where we expect to be this year—between $1.1bn and $1.3bn, with a slightly heavier fourth quarter and the residual carrying into next year,” he said.”

☺️

Any idea who bears the cost of CFM failing to meet its Leap engine TOW promise? Doesn’t GE/CFM entice customers with fly-by-hour service contracts??

Like Pratt, GE is paying compensation for reduced time on wing. But also like Pratt, they have the revenue stream to support it.

The durability kit should eventually lift them out of that, but as they said it will take several years to roll out across the fleet. Probably 2028.

Are there any reports that GE/Safran are paying out compensation to customers?

Just to clarify:

GE’s Q3 earnings report makes no mention of any such compensation — unlike the RTX report, which clearly references the subject.

For RTX, it’s more about the unprecedented grounding of the fleet due to its manufacturing defect(s), not the shortened WOT.

(partial)* grounding

GE doesn’t provide direct compensation to airlines for LEAP engine performance issues. But compensation can occur through contractual maintenance agreements.

When an engine issue arises, it’s managed on a case-by-case basis, according to the specific terms in these contracts, which may include a combination of credits, reduced costs, and potentially some fees depending on the nature of the problem.

An example:

https://www.geaerospace.com/sites/default/files/reimbursement-schedule_0.pdf

General knowledge of how the agreements work:

https://oat.aero/2025/01/06/who-pays-for-grounded-aircraft-with-engine-issues/

A further example, in 2022 GE lowered the time on wing allowance within new maintenance contracts, to reflect the reality and what airlines could expect in terms of costs. That lowered their exposure to the LEAP issues through compensation.

How is it booked and reflected in GE’s result announcement?

It’s reflected in the cost vs revenue of the services section, which includes maintenance agreements. The revenue is fixed by the contract, but the cost depends on engine performance. GE absorbs anomalous costs.

This presumes the customer has purchased the maintenance agreement. I would expect that most customers do, but I don’t have that data.

This is generally true unless the problem is defined as a latent defect. Then there is usually a separate compensation program, as with Pratt and the GTF.

A latent defect is an inherent manufacturing flaw that surfaces during service, outside normal wear and tear. Powdered metal application failures with the GTF would qualify.

I don’t think the LEAP problems rose to that level. They were essentially early wear that was dependent on specific environmental conditions.

How many GE9X will GE deliver this year and next year and who is going to pay for them?

Depends on whether — and how quickly — BA can get through the “mountain of work” on the 777X about which Ortberg was recently poor-mouthing.

My guess:

(1) zero

(2) zero…or maybe a trickle, at best

It doesn’t look like GE is sitting on a bunch of undelivered customer GE9X engines or parts for building such customer engines — so a non-confidence vote of BA’s promise/plan to deliver aircraft in early 2026?

“Chief Financial Officer Rahul Ghai said GE expects roughly 2,000 LEAP engine shipments in 2025 and *steady* GE9X deliveries.”

Zero, one or a handful? It’s a mystery.

A falsifiable prediction: certificated and delivered Boeing 777-Xs will not appear

before 2027- if then. We’ll see.

+1

Tidbits from the transcript:

> **our volume assumptions on GE9X have not changed since we were together back in July.** [GE had material information of Boeing ahead of everyone??]

> the number of shop visits that will be done in 2025 globally, worldwide shop visits are still below where we were in 2019. The worldwide shop visits still have not recovered to the 2019 level. [But GE got a banner year of profit?]

> The number of engines that will come off wing are going to be up double digits [next year]. [For the airline customers, does it look healthy??]

> We just launched our second dust test on the GE9X, which will continue to mature the design pre-entry into service

“Sweden and Ukraine Sign Historic Multi-Year Deal to Supply 100–150 Gripen E Fighter Jets”

https://united24media.com/latest-news/sweden-signs-deal-to-supply-ukraine-with-100-150-gripen-e-fighter-jets-12717

The Gripen E/F currently use the GE F414 engine…though there are reports that Saab is looking for a European alternative — potentially the RR EJ230 — so as to reduce exposure to geopolitical whim.

***

In related news:

Dassault has just completed its 300th Rafale (out of 533 ordered), and is upping the production rate to 4 p/m.

https://www.slashgear.com/2003804/dassault-300th-rafale-fighter-jet-completed/

-*-*-

Germany has just ordered a further 20 Eurofighter Typhoons, to be produced in Manching, Germany. This brings the total number of recent German Typhoon orders to 58.

https://www.eurofighter.com/news/germany-places-order-for-20-eurofighter-jets

“Sweden and Ukraine Sign Historic Multi-Year Deal to Supply 100–150 Gripen E Fighter Jets”

👇👇

LOI

Financing details need to be hammered out.

All 4-4.5 gen fighters. I think Europe will have to skip 5th Gen (apart from the widely ordered F35s).

Maybe the biggest 5 euro countries + Sweden can sit around the table and reshuffle specifications around a smaller and a bigger aircraft. So European air forces can order either or both, industries can also participate in both.

All 3 European models are considered to be 4.5 gen.

There’s no interest in Europe to develop a 5th-gen fighter, and very little appetite to order more F-35s, in view of their continuing sub-spec performance issues.

6th gen will/may be the next big development…although senior officers on the ground in Ukraine are consistently saying that large numbers of “simpler” machines are far more effective — in real-world warfare — than small numbers of “more complicated” machines.

France is working on a factory to churn out 1000 attack drones per month. Go figure.

Almost all Europe Nato countries are implementing / adding F35s. There is no European stealth alternative, many are in the F35 supply chain also.

When was the last new European order for F35s? Germany’s order 3 years ago.

Spain and Portugal don’t want it. France never did.

Denmark publicly regrets it — as does Switzerland

Several NATO countries have F35 sub fleets, with bigger fleets of Eurofighters.

All users are still waiting for a whole series of promised upgrades. Many/most of the current F-35s are not optimally deployable.

There are more and more systems that can detect and target “stealth” fighters, so one can fundamentally discuss the whole use case / point of “stealth”.

Meanwhile, users have to accept lower range, speed, payload and mission readiness, as well as much higher costs.

Good to hear that GE is still interested in application of hybrid. The world is moving towards electrostate.