Leeham News and Analysis

There's more to real news than a news release.

Safran raises full-year guidance on record LEAP output and booming engine aftermarket

By Tom Batchelor. October 24, 2025, © Leeham News:

A strong civil engine aftermarket and a record number of LEAP deliveries saw Safran achieve a stronger-than-expected set of results for 3Q25 and the first nine months of the year.

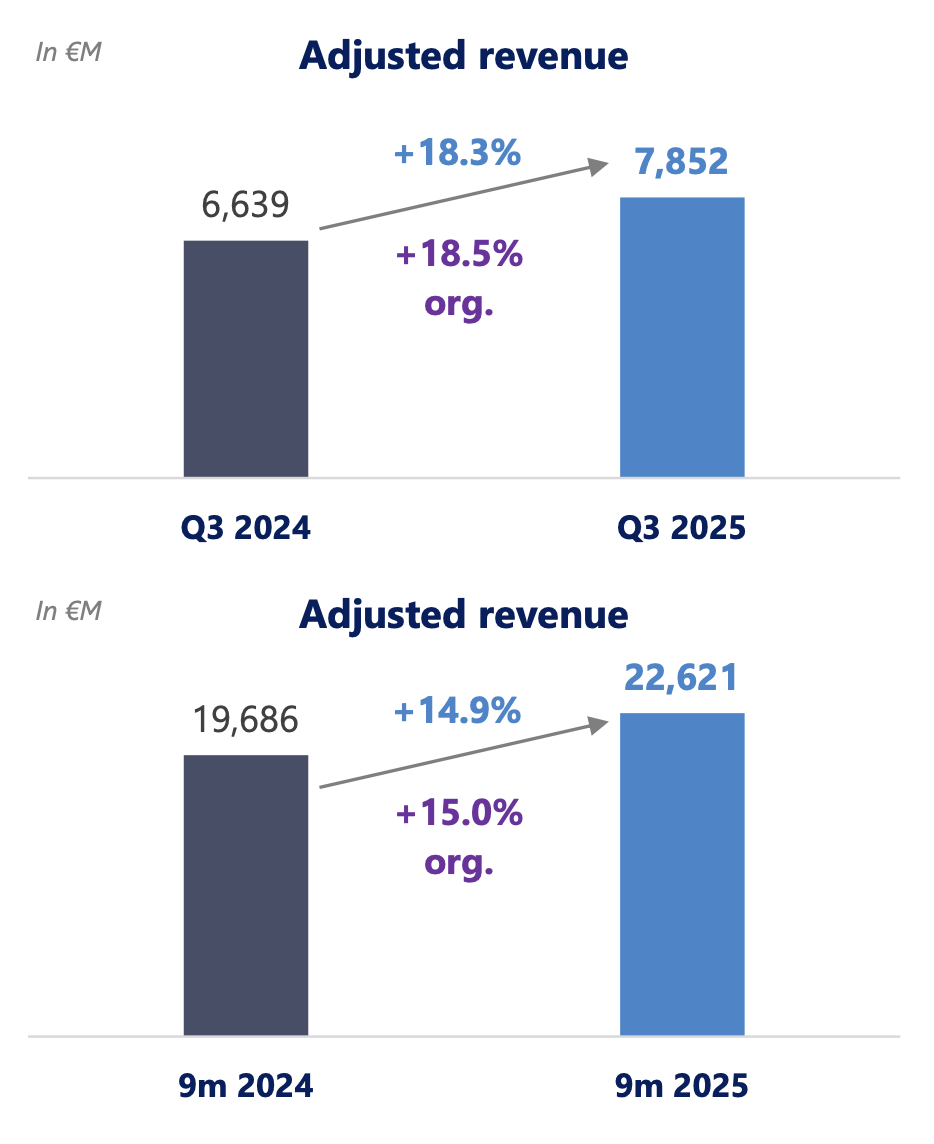

![]() Q3 2025 revenue stood at €7.85 billion ($9.13 billion), up by 18.3% compared to Q3 2024 – and an increase on the €7.59 billion-average Q3 revenue analysts had been expecting.

Q3 2025 revenue stood at €7.85 billion ($9.13 billion), up by 18.3% compared to Q3 2024 – and an increase on the €7.59 billion-average Q3 revenue analysts had been expecting.

Revenue for the first nine months of 2025 amounted to €22.62 billion, up 14.9% year-on-year.

As a result, the French aerospace group said on Friday as the results were published that it was raising its full year guidance across all metrics.

Growth across the board

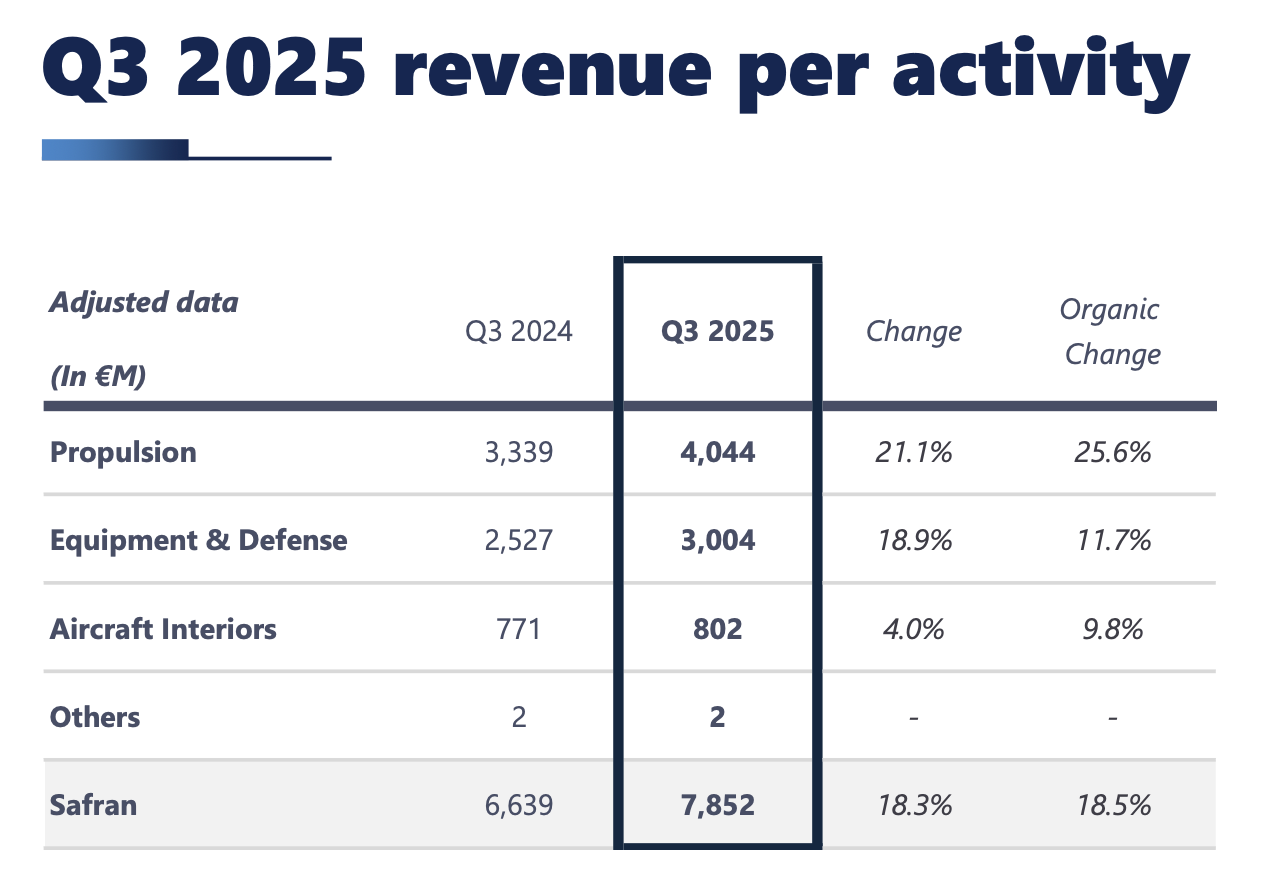

Safran said there was growth across all divisions in Q3, but its propulsion division stood out, with revenue up by 25.6%.

Broken down further, aftermarket revenue was up by 21.1% and OE sales rose by 34.4%.

Aftermarket momentum in the first half of the year continued into the third quarter, with civil engine spare parts sales up 16.1% year-over-year in USD terms.

Safran Q3 and 9m 2025 revenue. Credit: Safran

Growth was led by the CFM56 and high-thrust engine segments, while LEAP engines – which it co-produces with GE Aerospace through CFM – also made a positive contribution to the aftermarket results.

Civil engine service revenue rose 24.2%, driven by stronger LEAP rate-per-flight-hour (RPFH) contract volumes and continued demand for high-thrust engine maintenance.

LEAP engine deliveries spike

Notably, the number of LEAP engine deliveries saw a dramatic increase of 40% to 511 units, compared to 365 in Q3 2024, and Q3 deliveries were up 25% versus Q2 2025.

“Our output has improved quarter after quarter this year,” CEO Olivier Andriès told analysts on a call. “After a slow start, we have been able to catch up on delays.”

Andriès added that recent investments, including in a new LEAP-1A assembly line in Casablanca, Morocco, would enable Safran to “meet the high rate increase for the assembly” of the engine, referencing Airbus’ ramp up towards a rate of 75 aircraft per month in 2027, as well as Boeing and Comac, which he said was also “willing to increase.”

He added: “We have, let’s say, a joint vision [with Airbus] on the number of engines they need for 2026 and 2027, and we are discussing now 2028 and going forward. Are we going to catch up this year? I’m confident we will.”

Elsewhere, Safran’s military aircraft engine revenue declined versus the previous year, notably due to what the company said was a softer level of aftermarket activity.

Equipment & Defense

On the Equipment & Defense side, revenue rose 11.7% year-over-year, supported by solid performance across both aftermarket and original equipment activities.

Aftermarket services were up 11.5%, with broad-based growth led by landing systems, including spare parts, landing gear services, and carbon brake operations, alongside gains in electrical systems and A320neo nacelles.

OE sales increased 11.9%, driven by higher production volumes for landing gear on the 787 and A320neo, as well as stronger demand for electrical systems and nacelles across single-aisle, business, and regional jets.

Aircraft Interiors

Aircraft Interiors saw 9.8% revenue growth in Q3, with aftermarket activities up 6.8% and OE sales up by 11.7%.

CFO Pascal Bantegnie, also on the analysts call, noted there was “steady growth in the cabin business benefiting from aircraft ramp up.”

However, business class seat deliveries, he said, “face headwinds from certification, which remains a key challenge in the sector.”

Safran’s Q3 2025 revenue per activity. Credit: Safran

Tariff impact

Safran estimates the impact on recurring operating income from tariffs to be €100-150 million in 2025.

Bantegnie said: “Going forward for 2026 up to 2030, I would expect, given what we know today, and of course this may change…the net impact to be no more than €100 million per year on EBIT.”

The company said that while the trade deal between the EU and the US – and the eligibility of its products under the United States-Mexico-Canada Agreement – had “significantly reduced the amounts at stake”, a “residual impact” remains, primarily related to flows between China and the US, and products not eligible under bilateral agreements.

“In this fluid environment, Safran remains agile and actively continues to implement mitigation measures and commercial actions,” the company said.

Improved full year guidance

On its full year guidance, Safran said it was now expecting revenue growth of between 11-13%, versus a previous forecast of low-teens.

Recurring operating income is expected at €5.1-5.2 billion, versus €5-5.1 billion, and free cash flow of €3.5-3.7 billion, compared with €3.4-3.6 billion.

The improved guidance is underpinned by the uptick in LEAP engine deliveries, spare parts and services revenue and exchange rate effects.

“On its full year guidance, Safran said it was now expecting revenue growth of between 11-13%, versus a previous forecast of low-teens.”

two weeks versus a fortnight 🙂

Interesting that SAFRAN claims they’ll be able to keep up with

increasing demand. We’ll see how it goes.

Safran indicated 2 months ago that it expected to have worked-off this year’s LEAP-1A shortfall by the end of October (i.e. a week from now).

That may very well be, but I’m not *yet* seeing it on Planespotters. There are a handful of gliders being cleared (more last month than this month, so far), but the total had climbed to about 60…so there are lots more still to go.

As of this morning, line deliveries month-to-date were 32 for the A320/321neo and 26 for the MAX.

It could be that while the backlog is cleared from the manufacturer, those engines may take some weeks to reach the airframe assembler, and additional weeks/months to be installed, tested etc and ultimately delivered to airline customers.

Yes, I agree — that’s why I said “yet” and “so far”.

However, end-of-year is already a very busy time at AB, and this will make it even busier.

They may also churn out a whole bunch of finished gliders this week…who knows? There are certainly wild fluctuations in line output this year.

There is a difference between an engine OEM “bare engine” to a fully QEC’d powerplant ready to hang on wing. The QEC kit without nacelle is +$1.5M then the nacelle of a couple of million $.

Does anyone know Safran have a similar accounting policy of GE to recognize revenue from fly-by-hour service contracts?

Does GE follow different accounting treatment?

> Civil engine service revenue rose 24.2%, driven by stronger LEAP rate-per-flight-hour (RPFH) contract volumes and continued demand for high-thrust engine maintenance.

CFM international is the business that builds the Leap engines. It would be a standalone entity with 50:50 ownership. How Safran and GE deal with their share of the business is likely detailed in the annual reports

Apparently you didn’t read their annual reports before you posted!

Why would I. Surely you asked a question without consulting the reports…if any.

My answer was the generic …bleeding obvious category

My question is more for the author or one who is familiar with Safran’s accounting policies, not those who can’t bother to read the annual reports.

Take a closer look at what changes GE made that led to an SEC enquiry in 2018.

Interesting maint issue

https://www.cnbctv18.com/business/aviation/boeing-explains-sudden-rat-deployment-on-air-india-dreamliner-at-birmingham-airport-19724655.htm

Interesting BA design shortcoming:

“To address this, Boeing had earlier introduced a design change in the shuttle valve. However, 19 of Air India’s Dreamliners, including VT-ANO, do not yet have this modification.

There’s one company that can never be at fault. It’s the M.O.

Truly a hoot to read.

What did Airbus do about the Thales freeze prone pitot?

For those who actually are interested, no aircraft mfg is going to replace a working part and the AHJ would have to make a mandatory AD.

As usual, its a known issue common to all mfgs across various equipment bit and pieces.

It only fails if you don’t set it right. Its also a non crisis item, merely annoying.

Does your auto mfg update your car bits and fiddly bits when a better item is offered?

Time to get a grip on reality. No medicine for Airbus D. Syndrome.

> French investigators found that the Air France pilots had mishandled the temporary loss of data from iced-up speed sensors

> The accident to a number of technical and training changes.

If it happened to a Boeing, these same posters would argue it’s all the pilots’ fault!

So predictable

Same as ADS here in this thread.

Ventriloquism… making up words others never said…keeps those temu credits rolling in

The evidence-free squadron joins in. Truth Social is over there. 👉

> first losses in the SCS war

PLAN:USN 2:0 (PLAN didn’t come tho)

ABALONE.

Interesting AIRBUS Design Shortcoming

Upon touchdown, the RAT extended without any cockpit selection. Trouble shooting confirmed that the UPLOCK P/N: 730822B, IPC 29‐25‐03‐3A‐90 was weak and could be released by manual effort, with no obvious damage in cables/ control linkages detected. A new uplock

was ordered to replace the suspected one. Investigation of the uplock confirmed that the uplock (which was >20 years old) would not lock, and therefore could lead to the uncommanded RAT extension. “

This is from AIRBUS Maintenance Briefing Notes.

16 Pages of Rat Failures

https://skybrary.aero/sites/default/files/bookshelf/4022.pdf

PNWgeek I thought you were a professional in that domain?

( and Rob had afair linked to that Airbus document earlier, an interesting read, nothing comparable available from Boeing.)

RAT deployment as such from “packaging” issues is a nuisance.

RAT deployment from issues in the regular deployment path is of much higher interest. ( and indicating a major system problem. )

UWE

I did that to juxtapose ABALONES comment on Boeing Rats, which are an annoying mechanical anomaly with upgraded parts available to cure the issue. The fact that Indian Airlines chooses not to purchase them is not a problem with Boeings design. ABALONE for whatever reason seems to post insignificant off topic items and I thought he might like to see what they look like.

I do agree that aircraft System issues causing Rat deployments would be of far greater interest, but as of now, none seem to driving the rat deployments in the news of late.

Hopefully none appear

Have a great evening.

I wonder what progress has been made on the Leap-1A35A.

This engine, specified for the A321XLR would offer ~10% more take-off thrust and significantly enhance the XLR’s performance. As well as opening the door for possible heavier A321 stretch, freighter, MPA developments.

https://07185918574543712684.googlegroups.com/attach/c2bb917e3d4c/Airbus%20A321%20MPA%20concept%20keesje.jpg?part=0.1&view=1&vt=ANaJVrH-gl8hJXJ12CHNyTmxSXFxeAqexaYlq1e-G_Aj5MOINDUu0VhWB79C9tzwfCmfbTPxB_urCE-NYozw9q3VNU3ktOl7zaUGrZbTqacaJxSp69fvXRU

The Leap-1A35A seems delayed at least 2 years. Maybe CFM doesn’t want to push up engine temperature, pressures loads while MTBF / time on wing is not on target?

What’s the latest datasheet of the LEAP-1A?

> CFM partner Safran confirms to FlightGlobal that “all the Leap-1A thrust ratings” – up to 35,000lb (156kN) – have been certified by EASA, adding that they are “available through a software update, without design change”.

> The modifications, which were incorporated into the TCDS on July 10th and published on August 6th, included the models LEAP-1A32X, LEAP-1A33X, LEAP-1A33B2X and LEAP-1A35AX in the engine family certificate.

I think 32k lbf is the highest certified Leap-1a power rating in operation.. The A321 XLR is also limitted to 97t MTOW at this stage.

Thanks you for posting the possible option, had not heard of it.

That said, 10% thrust increase on an already hot engine?

They just released what was called a Pip at one time, so they probably need time on wing to see how that pans out.

I put this under several sub posts as to not hi jack the main thread on the root. Found it most interesting

https://www.politico.eu/article/ursula-von-der-leyen-new-plan-break-china-critical-materials/

Talk is cheap. Pundits have no idea of what they’re talking about. Too bad, there’re few who do know.

Porsche operating loss in Q3 wipes out nearly all profits this year. Decoupling is a two-way street. VW is in crisis, faces a €11 billion liquidity shortfall next year.

Read this

https://x.com/ThinkFinance999/status/1982116217511924105

CFM will play a role in any new NB development. Their RISE engine would need a new wing at least for a NB. Interesting RR seems focussed on re entering the market and Pratt hasn’t used the GTF’s full potential yet.

It seems Boeing position of not introducing a new NB before 2040 indicates they are financially restrained and waiting to see what others (Airbus, Embraer, Comac, ??) do. For Boeing increasing deliveries (quality), producing the backlog, reducing debt restoring confidence is more important. As discussed a few weeks ago:

https://leehamnews.com/2025/09/30/perspective-on-boeings-737-replacement/

In Europe I see R&D programs on new production technologies (ultrasonics, laserwelding), thermoplastics making progress, being completed. Upper and lower NB fuselages have been produced, tested, lessons learned in European programs like Cleansky2.

E.g. MFFD assembly research platform in Germany (High Res, no final design, but interesting details.. 😉 )

https://www.ifam.fraunhofer.de/en/technologies/final-assembly-mffd/jcr:content/contentPar/sectioncomponent/sectionParsys/textwithinlinedimage/imageComponent1/image.img.4col.large.jpg/1743657931574/Figure-1.jpg

It seems thermoplastic fuselage and production technology is pushing TRL-8 after 20+ years of R&D..

KEESJE

Boeing hasn’t been standing still either. In the past 4 years they have reduced to practice and implemented 22 different Thermoplastic fabrication process specifications. Thermoplastic composite parts are being installed in Boeing aircraft by the literal millions today.

https://www.compositesworld.com/news/atc-manufacturing-boeing-expand-long-term-thermoplastic-composites-agreement

@keesje:

I also go with PNWgeek on Boeing is not sitting still and also keep in mind the military side (which means Tech can cross both ways)

That said, PW is not doing a new GTF because there is no market for it.

Airlines are not happy with the grounded aircraft problem and I agree, its atrocious. More than half is PW.

No airline would buy a new engine now. And in affect it would be a NEO on top of an NEO.

CFM is not doing a new engine either (RISE stuff aside and you know how I feel about that one). They have 2/3 of the Market. They did the same Pip 1 that PW did.

PW would only do a fully upgraded/new GTF if the desire was there and I don’t see it happening.

All the major and miner updates then have to fit into the existing form.

RR in a way is an example of what happens. The Trent TEN parts don’t fit the Trent 1000 parts. If you want an RR 787 engine, you buy the TEN.

Fixes for the 1000 are being implemented though its still having an affect.

As far as I know, no one is buying Trent TEN. Switching to GE. I don’t know what the old customers are all going to do, case by case basis. Might as well stick with the 1000 as to buy a whole new engine, let alone one that has few if any customers.

The TEN was the basis for the A330NEO, so its not abandoned but the TEN itself is an orphan.

Few common parts, no service experience, small pool of spares. You might as well switch to GE and get the better engine (the TEN does not match GE in that choice).

Only if there is a new aircraft and then CFM, PW and RR will throw their hat in the ring. I would favor PW and RR as the ones committed to the GTF and in PW case, gobs of experience on it.

“No airline would buy a new engine now.” Lol. What do you mean by “now”? 2025? 2035?? How do you know? Which airlines have you talked with? What’s from the military side is relevant at this moment? What do you know??Wish is *not* a plan.

@Pedro:

Lighten up. I’ve written many times that customers don’t want a new airplane, new engines, or new technology “now.” They just want their effing airplanes on time with effing engines that work before they are willing to consider tomorrow’s airplanes and engines.

But no one has a “new engine” available “now”. No one is saying they are selling a new engine today or tomorrow. If you order a new aircraft from the airframer *today*, you aren’t expecting to take delivery this month or next year. You are around the very end of the line.

There are orders placed every year, if there’s a credible option that emerge in a few years’ time, who can say there are no willing customers??

Me thinks Scott has vastly better fingers on the Airline pulse than Pedro!

Trans

Let’s have a bet, okay. Are you willing to bet? (Open to everyone on this site.)

Bet: whenever a major airframer (Airbus or Boeing) launches an all-new aircraft with a new* engine, there are customers (airlines/lessors) willing to place orders.

I’m also willing to bet you aren’t going to take the offer.

“new airplane and/or new engine”

After hawing and hemming everybody will take it.

you could follow the mechanics in scope of the A320NEO.

Obviously some parties with existing investment will try to deflate the offer. ( sample in kind: After having ordered 787 obviously the same entities would have down talked any (counter)offer from Airbus )

PSA: My offer lapses by 10:30 pm EDT

Scott. Today Hindustani announced a license production agreement to build the SJ100. That airplane would be for domestic service. How would that new entrant potentially change the engine supply landscape. Thanks

“RR in a way is an example of what happens. The Trent TEN parts don’t fit the Trent 1000 parts. If you want an RR 787 engine, you buy the TEN.”

That whole line of thinking you have essentially made up. As there’s no validation for that. You have this idea that they are totally different engines yet the certification as them all under the same type certificate.

In fact type certificates dont mention ‘Ten’ version at all as its just a marketing name for a Trent 1000 version.

This has all been pointed out for you before in detail.

If you knew actual aircraft engine maintenance in detail, there wouldn’t be these ‘wide’ claims

“Few common parts, no service experience, small pool of spares. You might as well switch to GE and get the better engine (the TEN does not match GE in that choice).”

Completely untrue

Forgetting that Genx has a family of variants too, apart from the 787-747 change

Notice that there will variation between GEnx‐1B78/P2 and the much earlier GEnx‐1B54

The thrust ratings are a clue from 54k to 78k

There is a lot of ‘real’ information on GE fixes to the reliability and power upgrades of Genx engines on AIN, sister site to LNA

The high power 1B76/P2 is clearly related to the 787-10 from its 2018 certification date and of course the 787-10 EIS

https://www.ainonline.com/aviation-news/air-transport/2018-07-12/ge-delivering-new-genx-durability-upgrade

Safran is heavily involved in Genx series

@Duke:

With all do respect, I made up nothing. Per Av Week, 75% of the Trent Ten is new.

You can guess that parts like starter, gens etc stay the same.

Yes GENX has variations in PIP. I believe they quit calling it a PIP after 2 but continue to fix or improve things (mostly improve as they to were on the short end of SFC to start). Unlike Ten, all parts are backwards fitable.

RR did a PIP 2 of the Trent 1000, then moved to the TEN. They were trying to get away from the blade crack issues (they repeated it).

Going from memory so its iffy but I don’t think the TEN got any increase of SFC past spec, I think it met spec but by then GE had superseeded spec.

RR like PW on the GTF, laid an egg. The GTF could be fixed.

Some big Airline names (BA included) have dropped the Trent and gone with GE.

The Trent 10 was the developmental engine for the A330NEO (7000). The main reason the NEO A330 was late.

So please feel free to access the Parts manuals for both engines and do a part number by part number breakdown.

You can find a Plethora of airlines with problems, this is a year old but matches some of the latest I have seen in Av Week.

https://aviationweek.com/air-transport/airlines-lessors/british-airways-drops-flights-over-rolls-trent-engine-issues-787s

Or you can read this though I am not sure who it is, it matches other sources.

https://www.facebook.com/FlightDramaa/posts/a-quiet-shift-is-underway-among-boeing-787-operators-faced-with-long-term-reliab/122238569234064089/

No I do not log every web link though I suspect even hard proof from RR would be ignored.

The 75% ‘new or changed’ comes from Wikipedia not Aviation Week

Wiki source is dead link so cant be checked. Dubious at best claim

“The 75% ‘new or changed’ comes from Wikipedia not Aviation Week”

Whoops whoops. From AI hallucination to human hallucination. Must be some good stuff.

Damn autocorrect

*Whomp whomp*

One wonders if this is just plain ignorance…or paid PR / misinformation:

“Quantum Tech Moves From Lab to the Factory Floor: How Ford, TSMC, and Boeing Are Already Using It”

“…At Boeing , engineers turned to quantum models to study corrosion in aircraft materials. The new process helped the team identify longer-lasting coatings faster, saving time and improving safety”

https://www.tipranks.com/news/quantum-tech-moves-from-lab-to-the-factory-floor-how-ford-tsmc-and-boeing-are-already-using-it

Meanwhile, over in the real world:

“Practical Quantum Computing Five to Ten Years Away: Google”

(and even that estimate is highly optimistic)

https://thequantuminsider.com/2025/02/13/practical-quantum-computing-five-to-ten-years-away-google-ceo/

I think the believe Boeing will introduce no new aircraft before 2040 might based on a few assumptions that may be questionable:

– Boeing with the 737-7 is fine in the 130-165 seat category, its a small segment anyway. (It isn’t)

– Offering no AKH options is fine, because bulkloading is the standard in the US. (Look at ROW).

– 200+ Seats is satisfactory covered by 737-9 and 737-10. (Now look at market share).

– Customers fly Boeings for decades and will stick with their commitments no matter what. (Look what happens)

– 737 Dated cockpit systems and grandfathered requirements are irrelevant for airlines (Are they?).

-Airlines will keep ordering 737 MAXs while new bigger versions of NEO, A220 and C919 become available over the years.

-Trump & Tarriffs politics play no role in these developments. (GOOGLE Trump Boeing order 2025).

– Boeings supply chain in the US is just fine with the 737 for the next 15 years, they’ll wait & see.

I think Boeing will always deny there is an issue until they have solution.

Just before 737-10 launch: https://www.flightglobal.com/boeing-reaffirms-737-max-9-strategy-despite-slow-sales/119575.article