Leeham News and Analysis

There's more to real news than a news release.

Airbus 3Q2025: Still on target in 2025 – gliders remain, changes in 2026

By Karl Sinclair

![]() Oct 30, 2025, © Leeham News: Airbus (AB) CEO Guillaume Faury is still confident that the commercial aircraft maker can hit this year’s target of 820 aircraft deliveries, despite the snarls it is dealing with in the supply chain.

Oct 30, 2025, © Leeham News: Airbus (AB) CEO Guillaume Faury is still confident that the commercial aircraft maker can hit this year’s target of 820 aircraft deliveries, despite the snarls it is dealing with in the supply chain.

At the end of 1H2025, Airbus had a whopping 60 aircraft sans moteurs. That number dropped to 32 by the end of the third quarter. Faury says that number will hit zero by year-end.

Engine issues at both GE and Safran, which power the workhorse A320neo family under the CFM International joint venture, put deliveries badly behind schedule. It was revealed today during the earnings call that the snags are distributed about 50/50 across the engine OEMs. Typically, Safran provides the LEAP 1A engines to Airbus for delivery to European and other non-US airlines and lessors. GE provides them to Airbus for delivery to US airlines and lessors.

Through the first nine months of 2025, Airbus delivered 507 aircraft to customers, up from 497 over the same period in 2024. That leaves a whopping 313 aircraft to be delivered over the final quarter, to meet the guidance figures.

Guillaume Faury, CEO, Airbur Group. Source: Airbus.

To put it all into context, if Airbus were to hit its future targeted rate increases, for the next three months, it would produce:

- 75/mo for the A320neo family in 2027 = 225 aircraft

- 12/mo for the A220 family in 2026 (guidance changed from 14/mo) = 36 aircraft

- 12/mo for the A350 family in 2028 = 36 aircraft

- 5/mo for the A330 family in 2029 = 15 aircraft

Airbus would deliver 312 jets to customers, one shy of the target.

It must deliver on those rates, now.

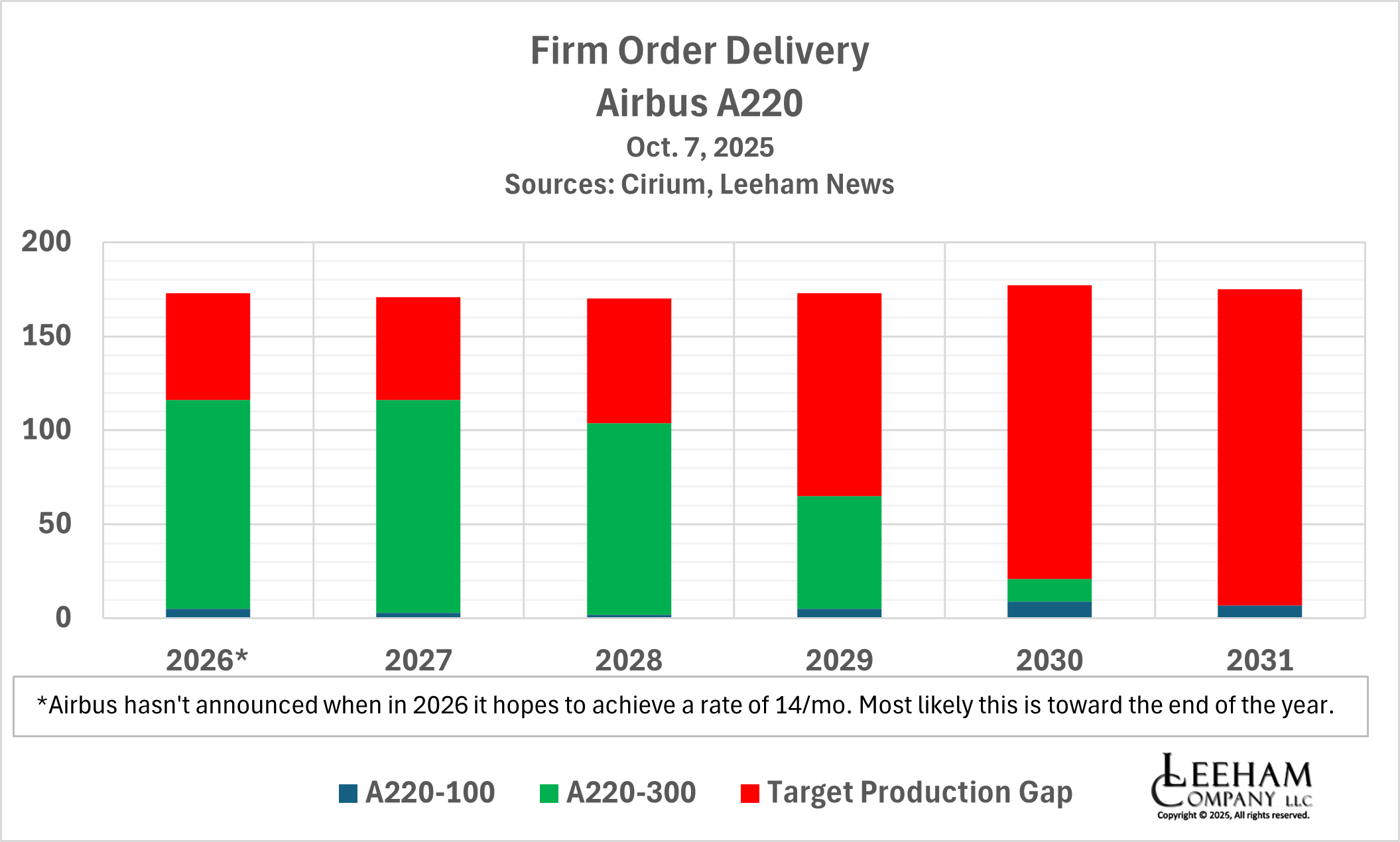

2026 Targets Modified

As indicated above, Airbus plans to increase the A220 production rate to 12/mo in 2026, down from 14/mo. However, according to the Cirium database, the A220 backlog doesn’t support a rate of 12/mo, let alone 14. LNA detailed this in a post on Oct. 20.

“We are in a steep ramp-up on the 220, and now target to reach the rate (of) 12 for next year, which is still a very steep ramp-up. But we believe this is the best balance between the different constraints we have on the A220 to get there by next year, including the integration of the wings and other work packages that will come from the integration of Spirit (Aerosystems of Wichita),” explained Faury.

In what he calls a “steep hump” for the A220 program, Faury pointed to the increased workload shouldered by both Mirabel (QC) and Mobile (AL), as a result of the wing integration and other work packages that will come with the acquisition.

While he termed that rate trim a “good balance”, Faury also addressed the future derivative A220-500. The current models are the 110-seat A220-100 and the 135-seat A220-300.

“When it comes to the third variant, which is also nicknamed the Dash 500…, that’s something we believe the program will need and benefit from. We have demand from airlines and from the airline customers for these variants, that on paper looks really good as a very competitive product. We have to say that the Dash 500 is not a question of if, but it is a question of when,” he said.

Financial Results

Airbus earnings for the nine months ended 3Q2025 were €4.1bn (EBIT Adjusted), based on reported earnings of €3.4bn (EBIT). This was up over 2024, when €2.8bn (EBIT Adjusted) and €2.7bn (EBIT) were reported.

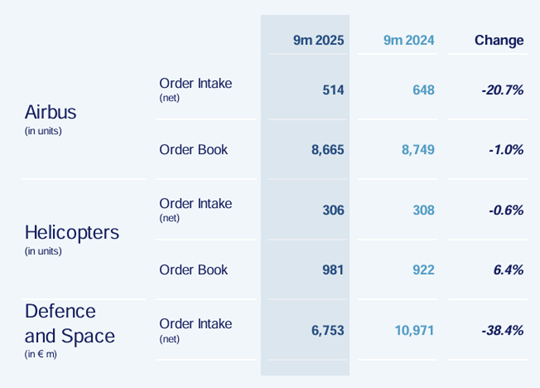

Company revenues were up €2.9bn to €47.4bn for the first three quarters of 2025, with Airbus Commercial gobbling up a 70% share. Defense and Space accounted for 19% with Helicopters bringing up the rear at 11%.

Airbus Group CFO Thomas Toepfer. Credit: Airbus.

Free Cash Flow (FCF) for the period was (€0.9bn) before Customer Financing. Airbus had an additional €2.3bn in Industrial Capex during the period, which accounted for the negative FCF. Airbus declared a net cash position of €7.0bn at the end of 3Q2025, after starting the year with €11.8bn.

As highlighted during the earnings call, the cumulative R&D spend for 2025 was €2.1bn, a drop off from 2024, when the company spent €2.4bn.

“We’re up to ~200 million (Euros) below the 2024 numbers for the first nine months of the year,” Airbus CFO Thomas Toepfer said. “That is mainly a function of our lead improvement program, where we’re focusing on the things that really matter. But we have the courage to also terminate some projects where we think they’re simply not yielding the results that we feel they should, and that means less external consultants [and] less spending on all kinds of things. It’s not trimming R&D with a lawnmower approach, but it’s really very specific and focused with the program where we focus on the things that matter most to the company.”

Airbus Commercial’s positioning saw almost universal drops across the board compared to the same period last year. Only the Helicopters order book maintained positive momentum in the first nine months of 2025.

The most significant declines were in Airbus and Defense and Space net order intake, which dropped 20.7% and 38.4%, respectively, year-over-year (YoY).

Segment Analysis

Commercial Aircraft

Commercial Aircraft

Airbus delivered 507 aircraft to customers by the end of 3Q2025. This included:

- 62 A220 – 12%

- 392 A320 Family – 77%

- 20 A330 – 4%

- 33 A350 – 7%

The higher revenues (€33.886bn versus €32.879 in 2024) were detailed as a function of increased deliveries and a growth in services. Services revenues are not broken out into a separate division at Airbus.

EBIT Adjusted jumped 8%, YoY, earning the company €3.27bn and a margin of 9.7%.

The supply chain was reported to be improving, but some concerns remained.

“On the supply chain, the main areas of attention and concern are engines, as we mentioned earlier. The rest of the supply chain is actually doing much better than in 2024 and previous years. Significantly better. The number of missing parts and the depth of delays is significantly better than it was before. We continue to have issues and delays on cabin equipment, interiors, seats, and that’s probably more of a mid-term issue than a short-term one,” said Faury.

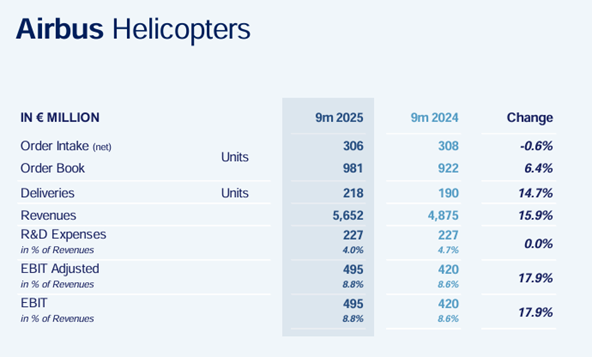

Helicopters

Airbus Helicopters had an external revenue split of 53% in Defense and 47% in Civil, for the period ended 3Q2025.

Deliveries, revenues, and EBIT and EBIT Adjusted all grew during the timeframe, climbing 14.7%, 15.9% and 17.9% for both EBIT and EBIT Adjusted, respectively.

One of the better showings was in the order book and deliveries. Both increased through 3Q2025, 6.4% and 14.7%, respectively.

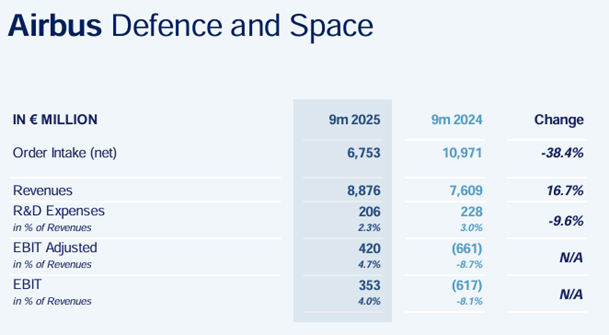

Defense and Space

The biggest news coming out of Defense and Space was that Airbus was forging ahead with the creation of a new European corporation, along with partners Leonardo and Thales. The recently signed MOU will entail breaking up parts of Airbus to form the new entity, ~35% of which will be owned by Airbus. This gives Airbus slightly more ownership than the other companies.

“On the Space consolidation, what we have to do is go from an MOU to signing, and then from signing to closing. Closing means that in order to be ready for that, we have to carve out the business. The business is spread over many legal entities and countries. We have the task as Airbus to create an operationally and legally standalone separate business until 2027, which can be then put into the new legal entity. That will come with not insignificant separation costs,” detailed Toepfer.

For comparison, it cost Embraer more than US$100m to carve off Embraer Commercial Aircraft in 2015-2016 for the proposed Boeing Brasil joint venture with Boeing. After Boeing walked away from the JV during the 21-month 737 MAX grounding and the beginning of the COVID-19 pandemic, an arbitrator eventually awarded Embraer US$140m in a break-up fee for its costs.

For the first nine months of 2025, the division reported a 16.7% increase in revenues, which climbed to €8.876bn. Revenues were split 34% to services and 66% to platforms.

EBIT and “EBIT Adjusted” both clawed their way back into the black, posting small but meaningful earnings of €420m and €353m. It was meaningful in the manner that the results were no longer negative and dragging down the company.

Order Intake, however, dropped precipitously to €6.753bn.

Airbus maintains a full-year guidance of 820 commercial deliveries, ~€7bn in EBIT Adjusted and €4.5bn in free-cash-flow, before customer financing.

It estimates that the Spirit Aerosystems deal will close in 4Q2025 and the impact of the integration remains broadly in line with projections.

Liquidity at the company remains strong, with some €30bn available. During September 2025, Moody’s upgraded the Airbus credit rating to A1, with a stable outlook.

*****************************

The Rise and Fall of Boeing and the Way Back

Boeing CEO Kelly Ortberg says one factor in the company’s considerations before launching a new airplane is its own recovery. Boeing, too, must be ready—and there is a long way to go before it is.

Boeing CEO Kelly Ortberg says one factor in the company’s considerations before launching a new airplane is its own recovery. Boeing, too, must be ready—and there is a long way to go before it is.

The Rise and Fall of Boeing and the Way Back, published last month by LNA editor Scott Hamilton, examines how Boeing got itself into industrial disgrace and how it is now at long last on the path to recovery.

The book is available here.

Airbus plans to increase the A220 production rate to 12/mo in 2026, up from 14/mo.

Huh? Is that new math???

@Rodney: LOL, thanks. Fixed.

I’m afraid I don’t share Mr. Faury’s optimism as regards reaching this year’s 820 delivery target.

The October figures (so far) have been tepid, which puts an even bigger emphasis on November and December.

Not impossible, but I’ll believe it when I see it.

Things are picking up:

As of this morning, 54 A320/A321neos delivered in October…up from 41 just two days ago.

And, as of this morning:

A320/321neo: 57

A220: 4

A350: 8

A330neo: 2

B737 MAX: 36

B787: 7

(Legacy 777/767 not counted).

AB thus got 71 frames delivered in October (going by this data), which means that it will have to average 121 p/m for Nov and Dec if it wants to reach 820 for the year.

That’s a tall order.

Oct 6

https://www.aerotelegraph.com/flugzeuge/emirates-fordert-dass-airbus-und-boeing-groessere-versionen-von-a350-und-777x-bauen/vc0p3s6

“Malaysia Aviation Group, the owner of brands Malaysia Airlines, Firefly, and MASwings, is “seriously” considering aircraft from the Commercial Aircraft Corporation of China for its future fleet, as part of its long-term development plan through 2035 to 2040, the group’s managing director told Yicai in an exclusive interview.”

Malaysia Aviation Group: We want cheaper single aisle aircraft!

A and B: No.

Malaysia Aviation Group: We will buy C!

A and B: Good luck.

Malaysia Aviation Group: “Like the rest of ASEAN, we’re tired of the neo-colonial, geopolitical drama from western countries.”

COMAC: “Aha! We can help you with that, and also offer attractive financing packages. Yuan interest rates are much lower than USD rates, and you’ll pay via CIPS”.

Malaysia Aviation Group: “Cool! Let’s talk!”

You would be well advised to talk to the neighbors.

Rob put it pretty well me thinks.

You mean the Indian neighbors, who are going to be buying ca. 300 Russian SJ-100s, to be manufactured in India?

https://ruavia.su/hal-and-uac-to-localize-production-of-sj-100-regional-jet-in-india/

Big shock — the world’d 4th largest economy doesn’t seem to be put off by the lack of FAA/EASA cert 😉

Rob? The poster who believes Europeans should support the US even after the US wants to annex Greenland, started a tariff war, blew up…?

How the US surrenders its influence:

Members if the ASEAN are rapidly seeking to reduce trade with the US after they are saddled with sky-high tariffs. They are recognizing that in the medium to longer term, they *really need to reduce their dependence on the US because the US is not a reliable partner*.

Another fig leaf like no one would buy/fly aircraft not certified by the West. Haha.

ABALONE wrote

Big shock — the world’d 4th largest economy doesn’t seem to be put off by the lack of FAA/EASA cert 😉

Just a note on that. The Airplane was EASA certified in 2102 and the Certification was revoked in 2022 as a result of Russian Sanctions.

Certification shouldn’t be an issue @Hindustani, just refile the docs with a new manufacturer on the TCDS. This is the same process the Romainians used with the ROMBAC111.

Not the same aircraft. One is fully domestic (Russian).

@Pedro

Why would India be interested in FAA/EASA cert for a regional aircraft that can’t reach Europe or the US from India..?

this shows the US has already lost its global leadership with Donnie’s protectionism

“Xi, who did not directly mention the U.S. or tariffs, shared five suggestions for cooperation at the APEC summit: safeguarding the multilateral trading system, creating an open economic environment, maintaining supply chain stability, promoting green and digital trade and fostering inclusive development.”

China is clearly the adult in the room!

Who would have thought? Leave the couch and go to see the real world outside.

> Countries who would favor China over the US if the region were forced to choose (Not many want to be Ukraine II in the Asia Pacific):

Indonesia (72.2%)

Malaysia (70.8%)

Thailand (55.6%)

Brunei (55.0%)

Laos (51.0%)

A trend of growing preference for aligning with China over the US. The poll was *conducted in early 2025 before reciprocal tariffs were introduced*…

“Certification shouldn’t be an issue @Hindustani, just refile the docs with a new manufacturer on the TCDS. This is the same process the Romainians used with the ROMBAC111.”

I don’t know that the MC21 was ever certified. Could be wrong but never heard it got TIA even. It would have, cert was killed between Russia and the West for sure in an administrative action.

That does not count all the so called Russian systems that supposedly have been installed.

If like the other area of Russian mfg, they will be using ad hoc parts acquired from China and other places.

Engines alone would be an issue. Marginal ops in Russia let alone India with the heat.

As for collaboration, well there is a border dispute going on as well and seized territory.

Hahaha

> China’s share in India’s industrial goods imports rose to 30%

> India’s reliance on critical Chinese supplies has deepened

> India’s imports from China rose more than 16% to more than $11 billion in September, with imports touching $91 billion in the first nine months

This SSJ-100 built under license in India has a lot of potential. Hindustani has a long history of success in manufacturing aircraft. The Indian workforce is loaded with a class of technicians trained and trainable to build and, most importantly, support the SSJ. Lack of a support network at scale has been the Achille’s heel of the SSJ export program. I can imagine that India could build that network domestically and then export it along with the SSJ. I wonder whether these SSJs will be the ‘Russified’ version or the current version made with western subsystems?

ABALONE wrote Big shock — the world’d 4th largest economy doesn’t seem to be put off by the lack of FAA/EASA cert 😉

ABALONE also wrote Why would India be interested in FAA/EASA cert for a regional aircraft that can’t reach Europe or the US from India…?

Notice the flipping here. First, he has no clue that the Sukhoi Superjet was certified by EASA, that a few were operated by Interjet THEN after finding out it WAS certified, he questions why India would be interested in an EASA cert completely ignoring the fact that export sales matter. Must be difficult living in the spin cycle

Note our commenter’s confusion here:

– First, he confuses the legacy SSJ-100 with the Russified SJ-100…the latter of which has never been certified in the west.

– Second, he thinks that India is going to be exporting these SJ-100s…when India has actually ordered them for domestic use.

Must be difficult living in the muddle cycle.

ABALONE SO INCORRECTLY WROTE.

– First, he confuses the legacy SSJ-100 with the Russified SJ-100…the latter of which has never been certified in the west.

– Second, he thinks that India is going to be exporting these SJ-100s…when India has actually ordered them for domestic use.

First no confusion. You said the aircraft was never certified. You were wrong.

Second, you maintain that the Indians will not be building these for export. I never restrict the future business plans for aircraft. I’m sure that when BAC was creating the BAC111 they gave no consideration to future licensing agreements that would eventually find the aircraft remarketednas a ROMBAC111. You may limit the aircraft to India in your mind, but I’m not so presumptuous to think I know more than Hindustani. They may be building for domestic use today, but as others have posted here, and as history has shown, discounting domestic distribution is a pretty good possibility.

Perhaps we should stick to what I said. You said it was not certified. I showed you to be in error. You then say that there are 2 versions, one EASA certified, which is correct. Neither of us know if Hindustani wants to source Russian or western components. Hindustani is in the business of making airplanes profitably and I leave that window open for them. Maintaining that you know what is best for Hindustani AND that they will not have export sales is quite a stretch for somebody not on their BOD.

This gos back to your agenda of diversion from the actual conversation to cover your errors. My suggestion is that when you critique somebody. Work on what they wrote as opposed to how your imagination sees it.

“You said the aircraft was never certified. You were wrong”

Our commenter is *STILL* confusing the legacy Sukhoi SSJ-100 with the Russified UAC SJ-100.

The latter hasn’t even been certified by the Russians yet, not to mind by anyone else.

It’s the latter that the Indians will be producing — not the former.

My starting comment above explicitly referenced the SJ-100…not the SSJ-100.

***

With regard to domestic use in India — I’m going by what’s being discussed in Indian media.

And, even if the Russians contemplate export from India once India’s 200-300 orders have been filled, that still doesn’t necessitate western certification — per the growing list of countries operating COMAC aircraft without western cert.

# Better_Reading

ABALONE WROTE

November 1, 2025

“You said the aircraft was never certified. You were wrong”

Our commenter is *STILL* confusing the legacy Sukhoi SSJ-100 with the Russified UAC SJ-100.

The latter hasn’t even been certified by the Russians yet, not to mind by anyone else.

It’s the latter that the Indians will be producing — not the former.

My starting comment above explicitly referenced the SJ-100…not the SSJ-100.

First the airplane was certified. Thats a point of fact.

Second, we are discussing the same airplane. It has gone through a few name changes starting as the RRJ95 and being renamed the Sukhoi Superjet 100 at Farnborough in 2005. It was debuted at the 2009 Paris Airshow. So far, they delivered 206 of them. There is a version of the Superjet100 being made with “russafied” components. The airframe is the same Superjet100 with limited changes for component swaps. Trying to say a change to components on the aircraft equipment list makes it a new airplane doesnt make it one. Its just a re-engined airplane. Your position that there is a legacy airplane and a new airplane is incorrect. Its the same airframe with equipment changes.

PEDRO said it was a different airplane, how can it be if its a russiafied version of the Superjet. The fact that its a version means it is a Superjet100 with russian equipment. Its still a Superjet in the TCDS.

EXPORT SALES? You were the one saying it will not be for export. I was silent on that until you dragged the subject up by saying that you don’t need a certified airplane to fly domestically. I pointed out it was certified, and was silent on exports, you started that line of conversation being quite clear that they didn’t need to be certified for Indian domestic use.

read write and remember, you’re not too good at that

Now, you were wrong about the airplane being certified, it was, by EASA. Otherwise Maleev wouldn’t have been the launch customer.

“First the airplane was certified. Thats a point of fact.”

#Hopeless

“Certification testing is expected to be completed by the end of this year, with deliveries to Russian operators scheduled to begin in spring 2026.”

https://ruavia.su/first-production-sj-100-aircraft-completes-maiden-flight/

🙈

AB has a net cash position of 7 billion Euros at the end of the

third quarter. Nice.

Wonder when the A220-500 will be started in earnest.

I guess in case the A220 really hits the production of 14 aircraft per month. According to some sources the A220 will then be profitable and also available.

Or when AIRBUS has the way to lower cost of production.

The most expensive part of an aircraft (other than engines) is the wing.

AIRBUS is almost ten year into the WoT program, and is buying out the SPIRIT factory making the wing for A220.

Time to reap the rewards?

New wing costs them billions.

And another wing building center that duplicates existing.

You would get very little SFC benefit as the A220 has a very good wing.

Will Boeing keep the facility or sell it for cheap?

But duplicating the existing capacity is needed to get to 14 a month

A220 wing factory tour

https://www.youtube.com/watch?v=tDDrgGSiW3A

Vincent

This is surprisingly low. I would have thought ABs net cash position would be better as Boeings q3 net cash, unless reported differently was a bit north of 23 billion USD

For decades I could hear, look how good Boeing is financially performing vs. Airbus. I don’t care anymore.

Net cash = cash on hand minus debt.

Boeing’s *cash on hand* = $23B.

Boeing’s debt = $53.353B.

So, Boeing’s net cash = *minus* $30B.

Summarizing:

For Airbus, net cash is plus €7B.

For Boeing, net cash is minus $30B.

The word “net” says it all:

“Net, adjective:

– Remaining after the deduction of all charges, outlay, or loss”

🙈

BA’s cash position is “inflated” by begging customers to pay early and delaying payments to suppliers around the closing of the reporting period as vividly reported by D Gates. The cash will disappear once the payment floodgates open.

I wonder if AB have the same timeframe as Boeing for a new

single-aisle, or if they will move first.

I’m betting AB will move first.

They know that BA can’t countermove, due to lack of funding, engineering knowhow and organisational wherewithal.

Airbus have said EIS of 2040. So no launch this decade

The A321 is outselling the -10 by like 6 or 7 to one. AB dominates the market… BA is taken to the cleaners.

Vincent.

I pondered this as well. Theres nothing in it for Airbus to invest in a new airplane. The money question is this, why replace a known good product with great margins by adding billions in cost to the balance sheet to build fewer airplanes until you get to rate, and then make around the same margins. If Boeing moves first for real, Airbus is in far superior shape and can overrun an effort by Boeing. I see no need to cannibalize their profitability

While I agree, no new aircraft and how do you keep your design operation able to do one?

Send them home (for good). That’s what happened to BA engineers without active assignments.

If AB were run by those who are/were running BA:

they’d sit on their hands — “no moonshot”,

declare big bonuses for themselves,

see no need to “reinvent the wheel” since their aircraft are selling like hot cakes.

How to run an aerospace company to the ground!

This is my view of how and when Airbus will be introducing a new single aisle plane. I think it will start with the anticipated A220-500 to be announced by end of 2026, and I don’t think it will be a simple stretch. I think it will be the platform for Airbus to

1. Solve the cockpit compatibility issue between the A220 and the othe Airbus A3xx series of planes. Solution I think will revolve around change the A220 cockpit to reflect the Airbus A3xx series layout and ergonomics but no change to underlying software controls of the A220s, but a definite change of the interface (A3xx series

“Skin”). This change in the A220-500 will then form the basis of the A220NEO revamp for the exist dash 100/300.

2. I expect the introduction also of a second engine option to the A220 via this new plane the dash 500, which then becomes available in the A220NEO update of the exist dash 100/300. I expect RR to be that second engine option, a strategic move by Airbus to insulate itself a bit from American OEM uncertainties, and also the political uncertainties being ushered in my the Trump and Republican regimes.

I expect the dash 500 to be available EIS 2031 or thereabouts.

Following that I expect announcement of the A320 series replacement in the 2033-2035 period with EIS for this in the 2040 time frame

Makes good sense, and I also think RR will be in the NB mix.

Your A220 delivery gap story is a very interesting one. I’m curious how Airbus thinks it will bridge the gap. Faury mentioned customers were holding back orders until the engine problems get sorted, which suggests an imminent Advantage upgrade to the PW1500, similar to the A320 family. It may also signal an expectation of a quick development of the 500 model so they can bring production forward.

PW has been madly inserting upgrades to the GTF on the A220 and the E2-195 for a while. That is why so many grounded is they have to get those upgrades.

The new package will probably be implemented on those other two GTF but its not needed to get them up to commitment specs.

Trans

Pure fiction. Lack of parts and slow turnaround in MRO shops.

“Korean Air becomes new customer for Airbus A350F”

“The carrier has converted seven of its existing A350-1000 passenger aircraft orders into the A350F freighter version.”

https://www.stattimes.com/air-cargo/korean-air-becomes-new-customer-for-airbus-a350f-1356962

***

That’s 2 orders for A350s in a week, both from Asia — 13 firm and 3 options.

Conversions from one type of A350 to another . No nett gain in orders

Fewer future sale of 777-8F. Koreans are hedging their bet in case, you know… ?

“No nett gain in orders”

It’s a net gain in A350F orders, which now stand at 78.

That’s compared to ca. 50 for the B777-8F.

This is a loss for Boeing. Korean Air has 20 777-9 and 777-8F on order and also a fleet of 12 777F. Now Airbus will enter the cargo fleet.

It seems that Korean Air needs new freighters but they don’t expect Boeing to deliver some modern freighters soon. When would you expect an 777-8F delivered to a costumer?

Korean Air already sent some A380 to a D-check. They won’t retire such an aircraft in 2026 as once announced.

Airbus’ A321neo or A321XLR?

Why does Qantas use the A321XLR for domestic routes??

It seems Qantas likes the flexibility to also operate e.g. Perth – Auckland and routes to Indonesia (Bali) with smaller aircraft than their A330s/787s.

But Qantas probably will have a subfleet with lie-flat seats, ordered in August 2025. The rest, I believe, will settle for mainly domestic service.

https://www.qantas.com/content/dam/qantas/pdfs/qantas-experience/onboard/seatmaps/airbus-a321xlr-seat-map.pdf

180 economy and 20 business ( 4 across)

3 rear cabin seats aren’t allocated on international and ‘long haul domestic’.

That points to them being cabin crew rest

The international routes would be ‘regional’

My favourite seating check site seatguru has closed and they say go a travel site

Pls update yourself in order not to spread misinformation:

> Qantas ordered an additional Airbus A321XLR aircraft with lie-flat Business seats to be used both on transcontinental and medium-range international flights.

The domestic A321XLR:

The cabin and seats of the new Qantas A321XLR have been designed with a focus on maximising passenger comfort. Customers can expect:

A more comfortable Economy seat that’s wider than the 737 seat with extra comfort seat cushioning

The largest overhead bins of any single-aisle aircraft that allow for 60 per cent more bags than the 737.

A sense of spaciousness in the long cabin with higher ceilings and large windows, and a wider cabin than the 737.

Fast, free Wi-Fi allowing all customers inflight to stay connected across multiple devices, as well as the improved Qantas Entertainment App for streaming content to their own device.

Seats for 197 passengers across two cabins, with 20 Business seats in a 2-2 configuration and 177 Economy seats [except the first three aircraft]

Airbus is gonna sell a jillion of those 321XLRs.

“Focusing on maximum passenger comfort customers can expect”..

😂😂😂

You can’t be serious.

2 toilets for 180 passengers in economy..

One of the worst ratios in the industry, even topping Ryanair for that dubious honor..

I got to hand it to you Pedro..

One thing you never fail to do.

Is dishing out ludicrous claims about how comfy a 5 hr.plus flight will be with that kind of privy ratios..

Well done again lad.

Comedy Gold..😆

> Qantas International CEO Cam Wallace confirmed the airline was “looking at the layout right now” for a sub-fleet of A321XLRs “with a lie-flat product” to tackle international routes.

More Airbus News ;

With the merger of Air Asia X into the unified Air Asia Group, the unit will operate narrow body aircraft only.

Leaving the A3330 neo order, which many speculated would be terminated ,came to fruition today. Once numbered a staggering 78

units ordered, reduced to 15, and finally the remainder cancelled today , ending all hopes of getting a new widebody type into service.

https://www.flightglobal.com/airlines/airasia-confirms-a330-exit-in-5-or-6-years-as-airline-sale-nears-completion/165103.article

I call it kicking the Plane down the runway. Leeham has assessed Air Asia as questionable.

I believe the progression was A330CEO, then A350, then A330NEO and now nada.

Airbus is not stupid, they had this operation as a flaky one and don’t count on it.

https://www.airbus.com/sites/g/files/jlcbta136/files/2025-04/Airbus-A330neo-Customer-List-April-2025.pdf

Its still there. Flakey Airbus accounting policies mean it would still be ‘listed’ until the last minute. Doesnt work under US accounting rules

Nice try.

List is valid as of April 2025.

Duke..

Garuda cancelled the sole outstanding A330- 800 neo order last year..

You really think they’re going to let that order go by the wayside..

False pretense as if the program actually has a backlog of orders.

So really,no surprises it’s still on the books and will continue to be for months as usual.

There is a new A330-800 order from Royal Thai Air force.

All orders will be on the books as long as Airbus will receive nothing more than a press release.

Good overall stasis on the 777X

https://archive.ph/dMJ8j

from your link regarding the 777X 3Q reach forward loss

“The charge amount includes additional customer concessions, the cost of incremental rework on built aircraft, learning-curve adjustments and the carrying cost of production operations spread out over a longer period of time,” says CFO Malave.

All because FAA moved the goal posts and no longer authorizes TIA in a single approval, but step by step

All because Boeing made changes to MCAS without notifying the FAA that resulted in almost four hundred lives lost!

Who’s at fault? Why no one is held accountable??

All because BA suffered a crippling braindrain of engineering talent, and no longer has the wherewithal to submit the required engineering analyses to the FAA.

Indian news sites are indicating that SJ-100 production in India may be starting as soon as 2027-2028.

So, early slots for Indian carriers.

@Thomas Benedict

Per your query above:

The news releases clearly indicate that India will be producing the Russified UAC SJ-100…not the legacy Sukhoi SSJ-100.

Makes sense, since it completely rids India of western geopolitical trickstering.

Interesting that, before it’s even certified by Russia, and despite the lack of western cert, the SJ-100 is now attracting hundreds of orders.

“starting as soon as 2027-2028.”

probably send subassemblies (aka Airbus style) for FAL at HAL Could be a couple phases, then move into drill and fill fuselage and wings production It will take a few years to duplicate the automatic fastening systems and tooling for production in India Probably change to moving FAL in India

Video of SSJ 100…India to Manufacture SJ-100 Aircraft in Partnership with Russia

https://www.youtube.com/watch?v=Efm–pcc_wk

Yes, Indian/Russian media are indicating that initial manufacture will use kits / sub-assemblies.

Early slots = nice selling point.

Domestic manufacture = even nicer selling point.

“extraordinary messaging” from the WH [Wink wink remember who stayed up all night waiting by the phone!]

https://x.com/WhiteHouse/status/1984273347187032079

this is why you don’t leave the party early

“China’s Xi pushes for global AI body at APEC in counter to U.S.”

“Chinese officials have said the organization could be based in the commercial hub of Shanghai.”

The USA is now having to fight off China hegemony in the East Asia because of Trump’s and Republicans shortsightedness and eagerness, during Trump’s first term in office, to discredit and dismantle Obama policies, in the case of current Trade issues, the Obama TPP (Trans Pacific Pact). This was comprehensive free trade agreement that would have tied the ASEAN nations, Japan, South Korea and other East Asian nations to the USA to counter the China belt and road initiative.

Trump tearing that agreement up in his first term and starting trade wars with all and sundry have turned former solid allies of the USA in the region into lukewarm friends.

This is what call snatching defeat from jaws of victory in the commercial struggle against China. Trump and his Republican allies are clues on how to navigate a changing world in which demographics and technology are making post ww2 world view assumptions of the late 20th century obsolete for policy formulations be it for social or economic.

CNBC: “Dollar divorce? Asia’s shift away from the U.S. dollar is picking up pace”

“Asia is progressively moving away from the U.S. dollar, as a mix of geopolitical uncertainties, monetary shifts and currency hedging prompt de-dollarization across the region.”

“While de-dollarization is not exactly a new phenomenon, the narrative has changed. Investors and officials are beginning to recognize that the dollar can and has been used as a leverage — if not overtly weaponized — in trade negotiations. This has led to a reevaluation of predominantly overweight U.S. dollar portfolios, said Mitul Kotecha, Barclays’ head of FX and EM macro strategy in Asia.”

“”De-dollarization in ASEAN is likely to pick up pace, primarily via conversion of FX deposits accumulated since 2022,” the bank’s Asia fixed income and FX strategist Abhay Gupta said.

“Beyond ASEAN, the BRICS nations, which include India and China, have also actively developed and peddled their own payment system to bypass traditional systems like SWIFT and reduce dependency on the dollar. China has also been promoting bilateral trade settlements in the yuan.”

https://www.cnbc.com/2025/06/11/de-dollarization-in-asia-is-picking-up-speed.html

Plain in sight:

> W/ Trump leaving early, allows Xi to play the role of senior statesman. Articles write themselves– “China moves into vacuum of US leadership withdrawal from Asia Pacific region”

https://pbs.twimg.com/media/G4n_kp5bQAMFEci?format=jpg&name=large

https://pbs.twimg.com/media/G4n96osa4AAOM9M?format=jpg&name=large

So… no “massive Boeing order” from China, after all?

Not yet. Notwithstanding that suspicious report.

“The USD is down to 42% of global reserves, while gold is rapidly rising”

“The dollar is losing its reserve currency status. USD is now down to 42% of global reserves, while gold is rapidly rising. According to The Kobeissi Letter, which provides leading commentary on global capital markets, gold is quickly replacing fiat currencies as a reserve currency.”

“Gold’s share of global international reserves rose by 3% in quarter one this year alone to reach 24%, almost one-quarter of global reserves, and the highest level in 30 years. At the same time, the dollar has declined by 2 percentage points to 42%, its lowest level since the mid-1990s.”

“Beyond the uncertain macro outlook driving investors to the traditional safe-haven asset, the major driver in gold price, according to Balaji, is the BRICS.

“The sanctions imposed on Russia in the wake of its Ukrainian invasion only served to erode the store-of-value function of the dollar. It opened the eyes of nations worldwide. If their dollar holdings can be frozen at will, it is not a safe place to store wealth. Moreover, with nagging inflation, the purchasing power of the dollar is eroding.”

https://www.thecoinrepublic.com/2025/09/03/the-usd-dollar-is-losing-reserve-currency-status/

https://x.com/KobeissiLetter/status/1962235795622035767

***

Global reserve currencies usually reign for about a century, and are then supplanted.

The USD became the reserve around 1920-25, so its time is up.

We’ve already seen this 6 times before:

-Portuguese Escudo (1450-1530)

-Spanish Peso (1530-1640)

-Dutch Florin (1640-1720)

-French Franc (1720-1815)

-British Pound (1815-1920)

-US Dollar (1920-)

-Unipolar –> multipolar?

Next question:

If India is willing to order (and manufacture) substantial numbers of Russian SJ-100s, will it also engage with the Russian MC-21 … which is in the same market segment as the A320 and B737?

And, if it does: at the expense of how many A320/B737 lost orders?

***

“MC-21-310 Prototype with all-Russian Systems Completes Maiden Flight”

“Aircraft No. 73057, with manufacturer serial number MC.0013, is the first serial MC‑21‑300 with a wing made entirely of Russian polymer composites.”

“As part of comprehensive modernization, this prototype underwent replacement of cockpit panels and controls, flight control actuators, wing mechanization drives, engine pylons, stabilizer trim mechanisms, avionics suite, auxiliary power unit (APU), air conditioning system, integrated flight data acquisition and recording system (FDARS), wheel braking system, fuel system, wiring harness, wheels, and tires. All components are of Russian origin, reflecting the country’s push for technological self-reliance in aviation.”

https://ruavia.su/mc-21-310-prototype-with-all-russian-systems-completes-maiden-flight/

Anyone see anything more about the reportedly imminent “massive Boeing order” from China? I have not.

On CNN, just 4 days ago:

“Boeing reported yet another massive quarterly loss Wednesday. It could still be an extremely good week to be Boeing.

That’s because the US planemaker could finally get a huge order from Chinese airlines, a market that the company has been frozen out for nearly a decade.

“Boeing is reportedly close to reaching a deal that could result in as many as 500 jet orders from Chinese airlines in the coming days or weeks, possibly as soon as President Donald Trump meets with Chinese leader Xi Jinping in South Korea on Thursday, according to multiple outlets.”

https://www.cnn.com/2025/10/29/business/boeing-china-deal

Perhaps Ms. Morgan can clarify for us? 😉

“could”, “close”, “possibly”,

The smell of desperation in the mornin’.. but yeah, maybe we should check with Ms. Morgan

for the final word.

😉

FT: Behind the niceties, the change in the balance of power between the two leaders was unmistakable

> Its bizarre a) how long it has taken western elites to realise the extent to which China is now a peer/has surpassed the west in key areas and b) how little this has been covered in ‘mass media’ that the public sees.

[Fmr special adviser to the UK PM for science&tech]

We have a commenter who thinks that the UAC SJ-100 is “just a variant” of the Sukhoi SSJ-100 😆

From the link (also posted above):

“Transitioning the SJ-100 to domestic components is the result of extensive modernization of the SSJ100 airframe and manufacturing processes at Yakovlev’s Production Center and partner facilities. *The import substitution program has replaced 64 key systems and components, achieving 70–80% localization. Russian-made avionics, landing gear, auxiliary power unit, flight control systems, electrical power supply, air conditioning, fire protection, passenger cabin interior, and other systems have been installed.*”

And also new engines…the PD-8.

https://ruavia.su/first-production-sj-100-aircraft-completes-maiden-flight/

***

More info:

“There isn’t a single component in the SJ-100 that was used in previous versions of the aircraft. It is a completely new aircraft, Alexander Dolotovsky emphasised. “The aircraft features an indigenised electrical power system, flight control system, display systems, signalling systems, radio communication systems, radio navigation systems. Inertial systems, air data measurement systems, landing gear, landing gear brakes, the main propulsion unit, the auxiliary power unit, the fuel system, the crew oxygen system, and the passenger oxygen system have all been replaced,” he listed.”

https://ruavia.su/superjet-indigenised-nothing-foreign/

***

By that measure, the 737-7 is (even more so) “just a variant” of the 737-700…so, how come the 737-7 isn’t certified, whereas the 737-700 is? 😂

ABALONE.

The SSJ100 and SJ100 are the same airplane. When IRKUT (the Sukhoi name holder) was absorbed by Yakolev, they renamed the SSJ100 to SJ100 to remove the Sukhoi Branding.

This has been clearly covered in the press from both Russian and Western sources. One particularly clear statement is from Flight Global (August 15, 2023), which states that Irkut, now Yakovlev, has renamed the former Sukhoi Superjet 100 as SJ-100, removing the Sukhoi association following the aircraft’s integration under the new company. The rebranding includes all company materials and documentation.

Rusaviation article dated August 31, 2023, reports on the Yakovlev presentation held after Irkut’s renaming and describes the renaming of the Russian regional jet from SSJ-100 to SJ-100. It explains the historical context of the Yakovlev design bureau reclaiming its name and integrating the Superjet under it.

THAT is why the new SJ100 VARIANT is undergoing removal of foreign components. Same airplane, different equipment list.

The Russian component SJ100 is not a new aircraft, it’s a new variant. Those are 2 very different things. New airplanes get new TCDS, New ICAO designators but most importantly, new airplanes demonstrate the 150% max load wing break test. They didnt do that.

Lastly, because you seem even more clueless than I had thought possible, the answer to your last question.

By that measure, the 737-7 is (even more so) “just a variant” of the 737-700…so, how come the 737-7 isn’t certified, whereas the 737-700 is?

The answer is quite clear; each variant of an aircraft must prove conformity to FAR part 25 before its designator may be added to the Aircraft Models Type Certificate Data Sheet. Each separate variant of an aircraft model is listed in the TCDS. The TCDS entries for each variant generally list the variant or model name/number (e.g., Boeing 737-100, 737-200, 737-800, etc.)

Different configurations or versions within that model line (e.g., extended range versions, freighter versions)

The applicable regulatory compliance details for each variant

Any notes on particular restrictions or special equipment fitting requirements

Related model designations included under the same certificate for military or civil use, if applicable

Each aircraft variant entry on the TCDS thus serves as an official record identifying which specific model variants meet the type certification standards, outlining their regulatory compliance and any special conditions attached to those variants. This allows manufacturers, operators, and regulatory authorities to identify exactly which versions of an aircraft are covered by the type certificate and under what conditions they are certified to operate

What else would you like to learn today?

“The SSJ100 and SJ100 are the same airplane. ”

vs

““There isn’t a single component in the SJ-100 that was used in previous versions of the aircraft. It is a completely new aircraft, Alexander Dolotovsky emphasised”

Q.E.D.

🙈

Fuselage diameter still is the same therefore we could apply 777 logic.

Your use of the word “logic” in this instance is an oxymoron 😉

ABALONE.

From another Russian source. This one states the number of foreign components exchanged and the dubious claims of the scope of work….. I tend to trust Flight Global, The Manufacturer and The Russian version of the insider. Here’s the excerpt

The Insider.ru article from April 2025 discusses the development status of the fully localized version of the Sukhoi Superjet 100, now referred to as the SJ-100 or “Superjet New.” It highlights that the fully Russified version aims to replace about 40 foreign-made systems and components, including avionics, landing gear, auxiliary power units, control systems, power supply, air conditioning, and fire protection systems with Russian-made alternatives.The article notes that in March 2025, a 2018-built Superjet was re-engined with the Russian PD-8 engine, marking the first flight of this configuration. However, certification of the PD-8 engine and the fully imported-substituted aircraft remains ongoing, with type certification expected by fall 2025. Only after engine certification can the full import-substituted aircraft certification proceed, requiring hundreds of test flights over several years before commercial operation.The Insider article expresses skepticism about the certification timeline and readiness of the aircraft despite state media presenting the flights as a major advance and a key achievement reducing reliance on Boeing and Airbus. It suggests the full replacement with Russian parts will take years to finalize despite some progress made by early 2025.In summary, the Insider article paints a cautious picture of the SJ-100 development progress, confirming the target of a fully localized aircraft but emphasizing the challenges remaining in certification and deployment of the Russian-made components across the aircraft systems

ABALONE.

GOOD TRY

but did you note the prototype of the Russiafied SJ100 was built in 2018?? How can that be unless it’s the same airplane

You kill me sometimes

Unreal

🙈

“There isn’t a single component in the SJ-100 that was used in previous versions of the aircraft. It is a completely new aircraft, Alexander Dolotovsky emphasised”

I suggest that they meant to say “There isn’t a single foreign made component used in previous versions of the aircraft.” Perhaps a translation oversight? Over exuberance?

THOMAS Wrote

“There isn’t a single component in the SJ-100 that was used in previous versions of the aircraft. It is a completely new aircraft, Alexander Dolotovsky emphasised”

I suggest that they meant to say “There isn’t a single foreign made component used in previous versions of the aircraft.” Perhaps a translation oversight? Over exuberance?

I agree with you. ABALONE in his haste to try to discredit me lost track of the fact that the Russianized version SJ100 airframe was manufactured in 2018, predating the Ukrainian invasion and the resulting sanctions. Their prototype of the Russianized SJ100 by definition cannot be 100 percent new. The reference sources I used were quite specific in noting the laundry list of replaced components.

THANKS FOR BEING THE VOICE OF SANITY

@Thomas Benedict

The Russians have indicated in detail that — while replacing western parts — they’re concurrently taking the opportunity to revise other parts of the plane, leading to what is effectively a major re-design.

They’re doing the same with the MC-21, Il-114-300, and Tu-214. The Tu-214 cockpit is, for example, being converted from 3-person to 2-person, even though the component replacement work doesn’t require this.

For those who are actually able to read, there’s a wealth of information on this website, divided into useful sub-categories:

https://ruavia.su/

Some commenters just don’t seem to be able to cope with the speed and extent to which the Russians are modifying five civil programs concurrently…including development of multiple new engines. And, unlike Boeing, there telling us in detail about what they’re doing, and the timeline involved.

The new SJ-100, with its PD-8 engines, and a whole plethora of other new systems, is expected to be certified at the end of this year, with volume production starting in 2026.

@Abalone

A link with .su – really?

I don’t care about their lies or anything else from .ru or .su.

@ MHalblaub

I don’t like our eastern neighbors either, but that doesn’t mean they’re only spreading lies.

Ask the Indians — they’re evidently impressed/satisfied by the SJ-100 and Su-57 programs.

In the same way that various customers in SE Asia are impressed by COMAC — despite western misgivings about “the reds”.

As a benchmark: ask yourself how accurate is the information that we’ve received from Boeing in recent years.

ABALONE completely misses the point of the changes of components to completely russian system parts on their aircraft. Sanctions are working. They must replace parts en mass from their domestic suppliers because they have no other choice. If they wish to produce commercial aircraft today in this time of sanctions, they must create their own supply chain for the replaced western components. The news from the Russian Manufacturers is being portrayed as a masterstroke of marketing instead of what it is. A response by Putin to counteract the debilitating results of a successful sanction program……. Anybody with modicum of knowledge of the workings of aircraft assembly understands the integration fiasco this creates. ABALONEs viewing this soviet response as anything other than desperation is fulfilling an agenda instead of accepting the obvious truth about sanctions and how russia has been forced into this position. They must source from within, or not at all…..

@ Abalone

November 4, 2025

I have doubts about “Indians”.

“Ask the Indians — they’re evidently impressed/satisfied by the SJ-100 and Su-57 programs.”

I’m not impressed by some Indian being “impressed” or “satisfied”. Sukhoi failed to support Superjets already delivered to airlines. India is looking for the Su-75 and not the Su-57. Su-75 hasn’t flown yet. I’m not impressed.

“As a benchmark: ask yourself how accurate is the information that we’ve received from Boeing in recent years.”

In addition to Boeing’s flowery language directed at the stock market, Boeing also had to publish hard data. Since the 7-8-7 roll out, I know what Boeing is trying to sell. Boeing isn’t any longer the benchmark for aircraft manufacturing.

“I don’t like our eastern neighbors either, but that doesn’t mean they’re only spreading lies.”

They just lie. That’s it. Even the name the Kremlin designated for its territories and the occupied territories is a lie: “Russia”. The Kingdom of Russia was located around Lviv and the duke of Moscow just took that name to rebrand its duchy to distract from its heritage as tributary state to the Golden Horde. – Excursion to politics: Kremlin even won’t keep its treaties (Budapest Memorandum,…). So why should Ukraine bother with peace talks for another treaty Kremlin won’t keep? Do you know another language with 3 separate words for a lie? They themselves know that they are lying their a. off.

ABALONE

Note the term VARIANT is freely used by Bjorn in his article comparing the A321NEO, A312LR and A321XLR, all of which were certified seperately as they emerged.

“To get the answer, we look into the different A321neo variants and compare their capacities and operational costs in this article using the Leeham Aircraft Performance and Cost Model, APCM.”

An aircraft variant is a specific version of an aircraft model that has differences requiring recognition or special consideration compared to the base aircraft. Variants can differ in size, engine type, range, configuration, or other performance and design characteristics. The term variant often refers to aircraft within the same general model family but with distinguishing features such as extended range (ER), freighter versions (F), or special cargo doors (SCD). Pilots may require difference training when switching between variants within the same aircraft type rating due to these differences.

In summary, an aircraft variant is a distinct form of a base aircraft model, differentiated by modifications or features that impact performance, configuration, or operational use.

In addition to manufacturing domestic-use SJ-100 passenger aircraft under license, HAL may also be lining up to manufacture Su-57 5th-gen fighters for India:

“According to Asian News International, citing a source within India’s Ministry of Defence, Indian and Russian specialists are jointly assessing the investment required to establish Su-57 production at Hindustan Aeronautics Limited (HAL) facilities in Nashik. This plant currently manufactures the Su-30MKI under license, providing an established production base and experienced workforce for Su-57 assembly. Additionally, Indian enterprises already produce components for the Su-30MKI using Russian technology, which could help reduce costs through localized production of the fifth-generation fighter.”

https://ruavia.su/india-considers-su-57-production-partnership-with-russia/

ABALONE WROTE

In addition to manufacturing domestic-use SJ-100 passenger aircraft under license, HAL may also be lining up to manufacture Su-57 5th-gen fighters for India:

That’s good news. It has nothing to do with the systems changes in the SJ100 removing western components to produce the Domestic Version of the SJ100 , but shows the Hindustani workers are a good group and fully capable of advanced aircraft building

If I recall right, HAL has been producing A320 doors since the early 1990s

My post was to illustrate the extent to which India is increasingly embracing Russian tech exports, and the extent to which Russia is happy to allow India to self-manufacture…all going against Donnie’s policies.

Some commenters are already well aware of this tendency, of course. For many others, the penny isn’t dropping at all.

I’m never understood why US hasn’t over many years supported India more robustly in defense and economic development. I dont’ know the full history, but it seems we chose Pakistan over India 75 years ago. Seems ironic, India being a democracy and Pakistan being less than a democracy. Maybe Great Britain persuaded US to avoid India. I dunno..Geopolitics…

Anyhow, India has some savvy leadership now and they certainly have a skilled workforce to do pretty much anything. Human capital to spare. I wish them well building the SJ-100. I agree with PNWGeek that they will do it well.

ABALONE.

I might suggest that as opposed to adopting Russian Technology Exports, the Indians are playing the long game here. They have already produced license built airliners in the past, but now, they are taking advantage by purchasing licensing rights from Putins regime due to Putins need to raise cash in the face of sanctions and oil export curtàilment. This is a great, smart move by the Indians and illustrates the Putin regimes weak negotiation position. The SUKHOI 57 is the crown jewel of soviet aerospace development. The fact it is available to India shows the cracks in the Soviet economy….. Attributing this to anything other than sustained international sanctions over the Ukrainian invasion would be wide of the mark

Has anybody noticed the Russians took an airplane built in 2018 striped it of western components calling it a russianized variant??Why did they cobble together a flyable airplane using lower performing Russian domestic products and go thru all the propaganda machinations to make it look like some marketing genius move. The clear headed among us see it for what it is a desperate move to get the money coming in. They couldn’t license it to the Indians until they could overcome the parts shutoff caused by the Ukranian Invasion Sanctions. T his is Putin and the command economy trying to generate cash to offset oil exports……

The marketing masterstroke was keeping people from saying this out loud

Even after all that the Indians will do well with it, because I’m sure they bought it at a very favorable price structures…..

“Ful of sound and fury, … ”

NYTimes:

> many companies have found that “in no place has it been possible to replicate the manufacturing ecosystem and cost efficiencies that you get in China.”

> Companies “doubly hesitant about expanding supply chain networks outside of China.”

https://t.co/aldfaIqNyH

Who’s being played?

Shock! Horror!

Who’d have guessed? 👀

Although countries like Vietnam and India probably offer a relatively good proxy, there won’t be many companies voluntarily onshoring in the US.

Dubai Airshow starts 2 weeks from today — 17 to 21 Nov.

COMAC is going to participate with the C919 and C909, 4 frames in total, including flight displays.

Airbus will be bringing an A350-1000, A220-300 and an ACJ 320, plus military/helicopters.

Embraer is bringing the E195-E2 and an E2 freighter, as well as the KC-390.

Not yet known what Boeing is bringing.

https://www.dubaiairshow.aero/en/visit/visiting/aircraft-list-2025.html

https://aerospaceglobalnews.com/news/comac-first-dubai-airshow-2025/

***

It will be interesting to see if Emirates orders anything.

Air India may also top up.

The winning continues?

WaPo: Some South Korea firms pulled projects after Hyundai immigration raid

> Despite reassurances from the Trump administration, South Korean investors remain cautious, according to three people who represent South Korean and East Asia-based firms in the United States that paused or retreated from U.S. investment plans.

As of early this week, at least two companies with projects in development had decided against investing in the U.S. and at least four companies have extended pauses on projects put in place after the Hyundai raid in September, according to two consultants and one lawyer with clients in East Asia.