Leeham News and Analysis

There's more to real news than a news release.

Boeing, once the king of freighters, falls behind Airbus going forward

Subscription Required

By Scott Hamilton and Bjorn Fehrm

April 2, 2026, © Leeham News: Boeing is no longer “freighter king.”

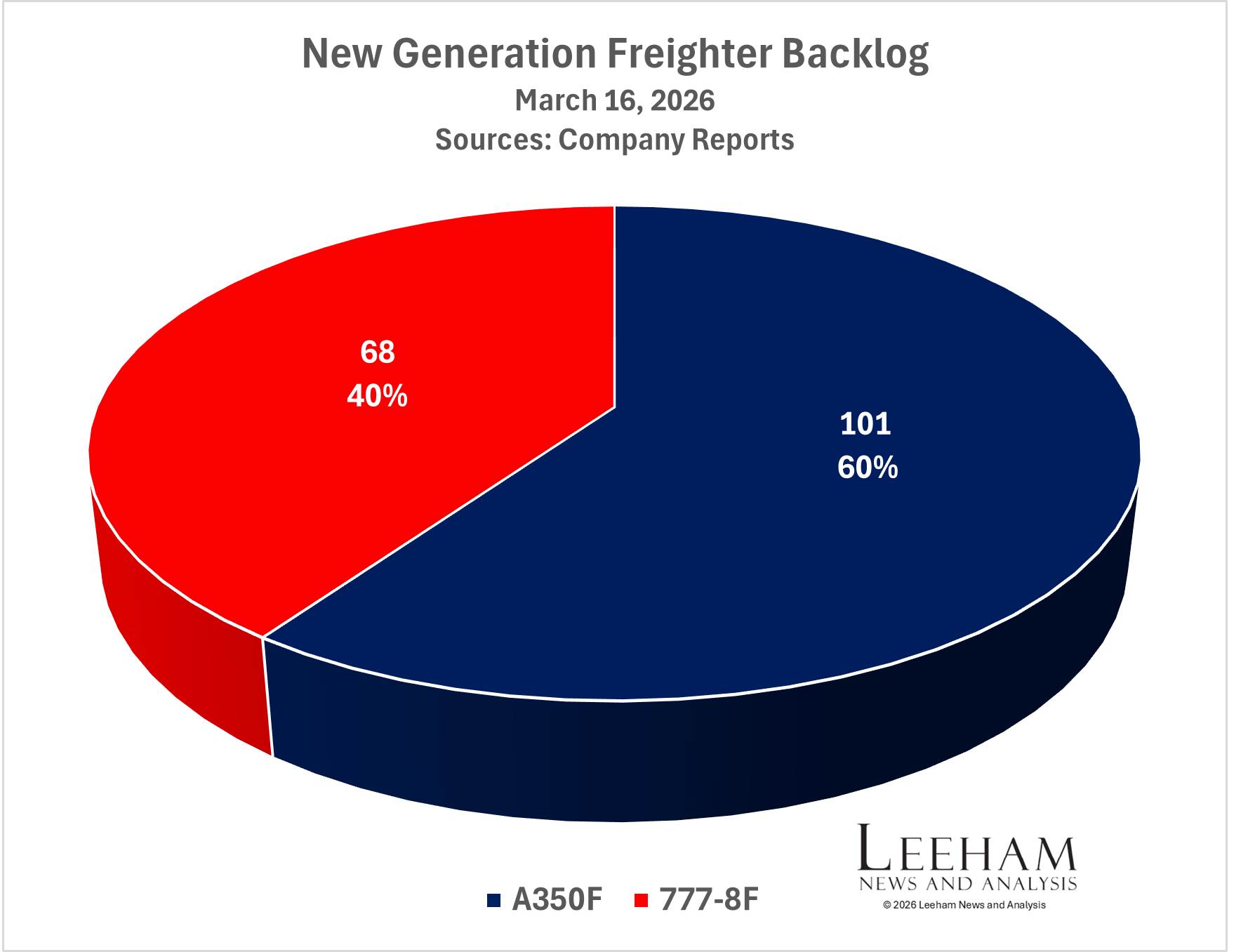

The March 16 order by cargo carrier Atlas Air for 20 A350Fs gives Airbus a 60% market share of orders for the next generation of freighters. Since the dawn of the jet age, Boeing has had a lock on jet airliner freighters. It vanquished Douglas Aircraft Co and its successor, McDonnell Douglas. Airbus had modest success with the new build A300-600F, with about 100 ordered. But Airbus bombed with the new production A330-200F; only 38 were sold.

Figure 1. The backlog of new generation freighter orders gives Airbus a 60% market share. Sources: Airbus, Boeing.

However, Airbus now has 101 orders for the A350F. Boeing has just 68 for the competing 777-8F. This is a far cry from the 359 777F Classics, based on the 777-200LR, that have been ordered. There are 47 in the backlog. Production will conclude at the end of next year due to emissions standards that the old generation 777F does not meet. Boeing asked the Federal Aviation Administration (FAA) for an exemption to build 35 more. It requested a decision by May 1.

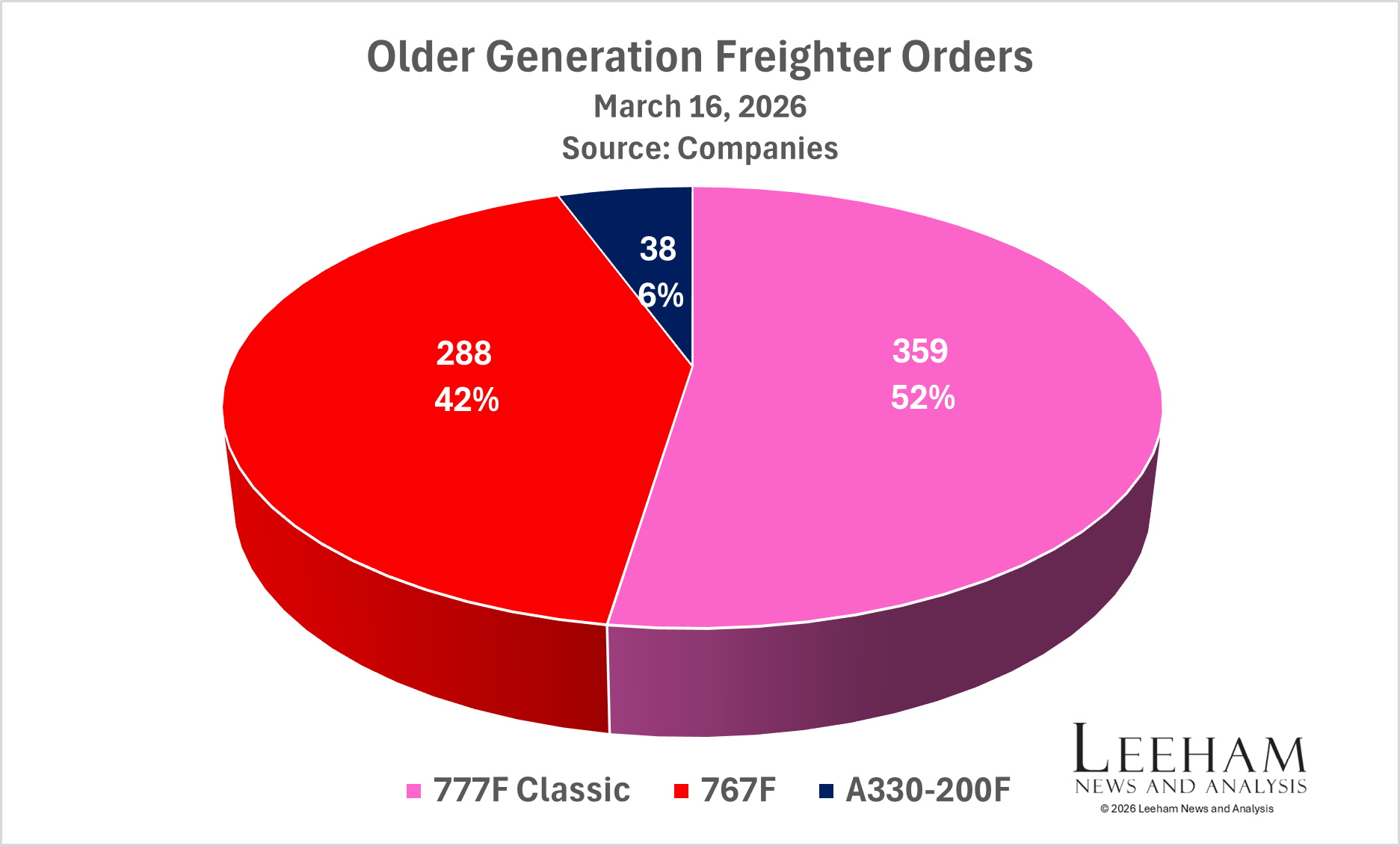

Figure 2. Boeing dominated the jet freighter market from the 1960s. The recent, old generation freighter market was still overwhelmingly owned by Boeing. Sources: Airbus, Boeing.

Additionally, Boeing sold 288 767-300ERFs. There are 18 in the backlog. Production concludes at the end of next year.

How did Boeing lose its overwhelming dominance in the freighter market? How did Airbus overtake Boeing, as it did in the early 2000s in the passenger airplane arena?

The answers about Boeing rest in a combination of negative fallout from the 737 MAX crisis, a suspension of production of the 787, shifting priorities and Boeing’s inbred arrogance.

For Airbus, the answer lies in the tortoise-and-hare analogy and a willingness to listen to potential customers more than Boeing did in key campaigns.

Fuel prices up sharply, but not sustained at record levels–yet

Subscription Required

Now open to all readers

By Scott Hamilton and Karl Sinclair

March 28, 2026, © Leeham News: Oil prices skyrocketed this month with the beginning of the 2026 Iran War.

Yet, as sharply as prices spiked, they are not yet a record relative to inflation-adjusted prices since the 1973-1974 OPEC-inspired oil embargo and other regional or global events, an analysis by LNA shows.

West Texas Intermediate Crude oil prices topped $100/bbl. Brent crude briefly hit $197/bbl on March 20. On March 27, Brent topped $100.

Some airlines worldwide hedged fuel against dramatic price hikes. Our detailed analysis is below.

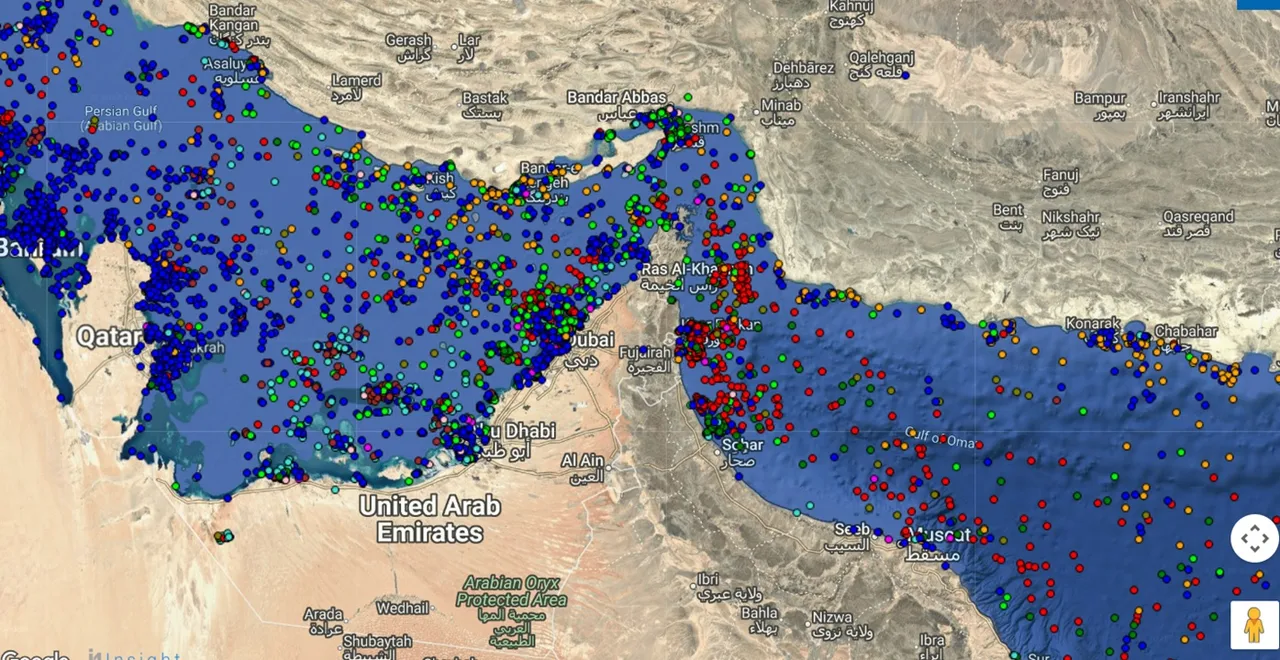

There are dire predictions that the prices could reach $170 or even $200/bbl if the Iran War continues. Bombing of Iran by the United States and Israel began on Feb. 26. Shortly after, tanker traffic through the Strait of Hormuz all but ceased. Twenty percent of the world’s oil transits through this bottleneck. Some countries, such as Japan and China, obtain more than 90% of their oil via the Strait.

More than 300 tankers are trapped. Some were attacked by Iran. Hundreds of ships of all kinds are blocked on both sides of the 35-mile-wide Strait.

Figure 1. Source: About 750 ships were trapped at the peak. Iran is allowing limited traffic through. Seatrade-Maritime magazine.

The price of oil is being whipsawed as President Donald Trump mixes messages about the war’s progress, sometimes within minutes. Sometimes the war is “won,” but more troops and ships are being sent to the region. Trump threatened to increase bombing, attack Iran’s power stations, invade an island, and then take it back. Allies are needed to reopen the Strait, and then they are not.

Air Lease merger this year creates new lessor powerhouse

Subscription Required

By Karl Sinclair

March 16, 2026, © Leeham News: Aircraft lessor giant Air Lease Corporation (ALC) of Los Angeles (CA) closed the books on 2025 and reported record figures.

March 16, 2026, © Leeham News: Aircraft lessor giant Air Lease Corporation (ALC) of Los Angeles (CA) closed the books on 2025 and reported record figures.

In early 2026, the company will cease to exist. The Sumitomo Corporation, SMBC Aviation Capital, Apollo, and Brookfield funds are expected to acquire Air Lease Corporation for $7.4bn in the early part of this year and rebrand it the Sumisho Air Lease Corporation (SALC). SALC will be a new powerhouse lessor that Airbus, Boeing, and the engine makers will be dealing with.

According to ALC, Air Lease Class A common stockholders will receive $65 in cash for each share of Class A common stock of Air Lease held immediately prior to the effective time of the merger.

SMBC will then service most of Sumisho Air Lease Corp.’s fleet, significantly expanding its service portfolio.

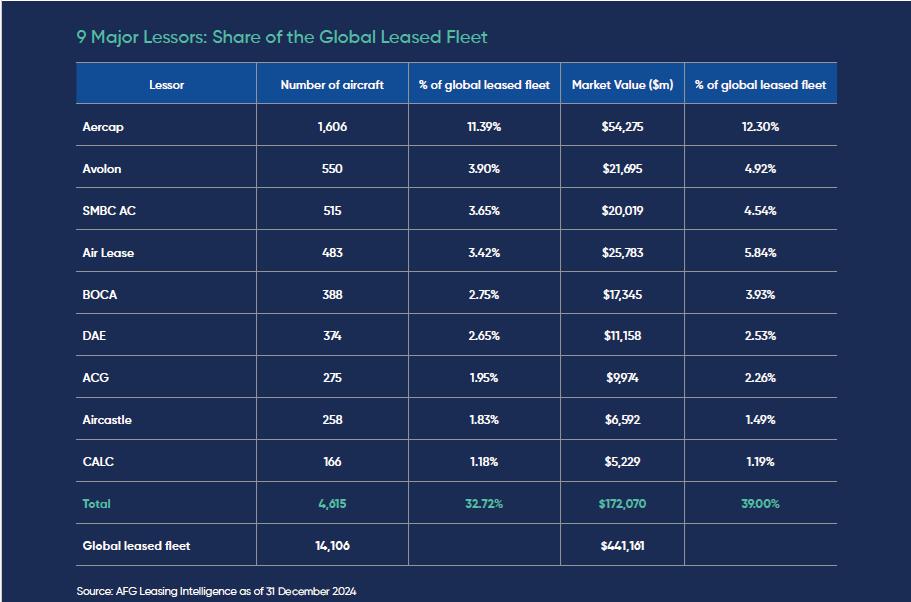

Thus, the world’s second-largest commercial aircraft lessor will be born, as the third and fourth largest lessors merge (by fleet size in the 2025 Airfinance Global annual lessors analysis), second only to Aercap of Dublin (IR).

Source: Airfinance Global 2025 Annual Lessor Report.

Middle East conflict impact on Airbus, Boeing

By Scott Hamilton

March 10, 2026, © Leeham News: The end of the war in the Middle East appears to be on a path of continued uncertainty and confusion, with no end in sight.

Middle Eastern airlines and lessors have 1,710 airplanes on order. The Mideast represents 9% of Airbus’ backlog. It represents 14% of Boeing’s backlog. Airbus has a 43% share of the Mideast backlog, while Boeing has a 57% share. Embraer is a fractional player.

Although President Donald Trump has already said the war has been “won” and could be over soon, he’s also provided mixed messages. Trump says that a cessation will be done with the concurrence of Israeli Prime Minister Benjamin Netanyahu, a notoriously anti-Iranian leader who urged Trump to engage in the first place, according to multiple media reports.

Trump also said that bombing may continue despite hinting that the war’s end is near.

For the airlines, the continued conflict means vastly reduced service. More of the current fleets are grounded than in service. For lessors, many have airplanes with Middle Eastern carriers, and a few whose home is in the region, some have outstanding orders with Airbus and Boeing. Lenders may face requests to restructure debt payments the longer the conflict continues.

Here’s a snapshot of the backlog exposure Airbus and Boeing have with the Middle East.

Figure 1. The Airbus-Boeing firm order backlog market share in the Middle East. Sources: Airbus, Boeing.

“Resilience is key” to Airbus production ramp-up

Subscription Required

By David Slotnick

March 5, 2026, © Leeham News: Airbus’ head of procurement shared a rallying cry for both OEMs and suppliers at the Pacific Northwest Aerospace Alliance (PNAA) in suburban Seattle on Feb. 10, ahead of the European planemaker’s plans to increase production to record-breaking rates.

Florian Seidel. Source: Florian Seidel.

In a speech at the annual conference, Florian Seidel, the chief of strategic procurement at Airbus Americas, urged the entire supply chain from top to bottom to focus on working “like Swiss clockwork” as manufacturing increases and airline customers continue to require support throughout each aircraft’s operating life.

The call for continued close collaboration and efficiency comes as Airbus sets its sights on production rates that exceed even peak pre-pandemic levels. While Airbus plans to increase rates on all of its commercial programs, Seidel described the target on the A320-family — 75 per month in 2027 — as “the most impressive” ramp-up, requiring a “huge effort across the entire supply base.” (Update: A week later, during the Airbus earnings call for 2025, this target has shifted to 2028.)

Additionally, Airbus plans to grow the A220 to 12 per month this year, the widebody A330 to 5 per month by 2029, and the flagship A350 to 12 per month in 2028.

“Resilience is key” to making that ramp-up successful and sustaining those rates, Seidel said.

“This is a ramp-up that’s unprecedented, and that we require the resolve of the entire supply base to make it happen,” he added.

Airbus: Repeatedly Missing the Mark on delivery guidance

Subscription Required

By Karl Sinclair

March 2, 2026, © Leeham News: With the closing of the 2025 financial year, Airbus SE (AB) estimated how many commercial aircraft it expects to deliver to customers in the coming 12 months.

March 2, 2026, © Leeham News: With the closing of the 2025 financial year, Airbus SE (AB) estimated how many commercial aircraft it expects to deliver to customers in the coming 12 months.

Along with guidance on expected revenues, profits, and free cash flow (FCF), investors and analysts use delivery metrics to assess not only Airbus’s success but also how the heavily integrated supply chain beneath the OEM is functioning.

It only takes one missing part to keep an aircraft glued to the tarmac, and as the old adage goes, “When a supplier has a problem, Airbus has a problem.” Even when it is buyer-furnished-equipment (BFE), like interiors.

Airbus has missed its aircraft delivery guidance in each of the last three years. The company had to reduce its guidance as the lack of engines, BFE, other parts, and quality control issues combined to cause Airbus to miss its early guidance.

Related Article

How close do the estimates provided by Airbus, some 12 months out, come to reality at year-end?

Are the projections pie-in-the-sky numbers or can they be safely relied upon to provide a clear picture of the short-term future?

LNA takes a deep dive into Airbus guidance accuracy by analyzing the original projections for the previous three years, any changes that it has made to those targets, and how well those prognostications held up at year-end.

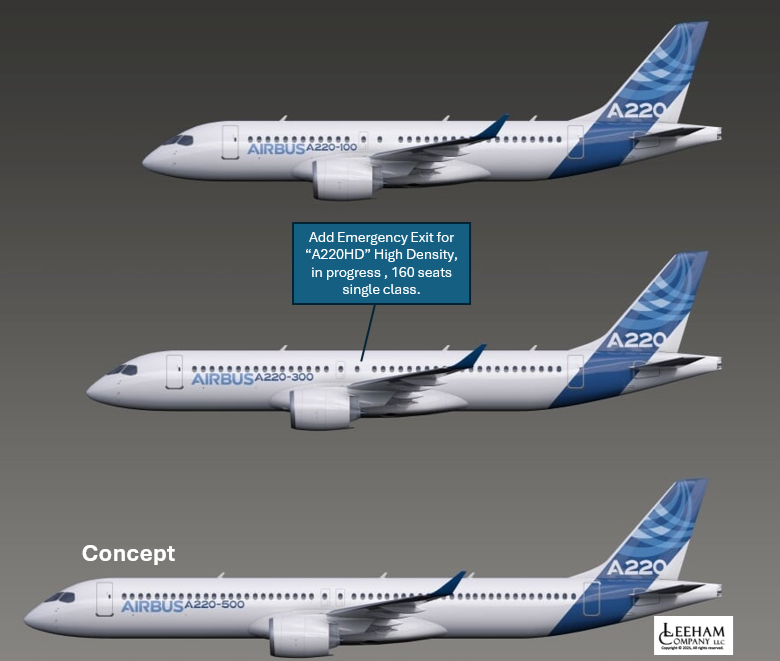

Airbus leans toward launching “A220-500”, but faces challenges

Subscription Required

By Bjorn Fehrm and Scott Hamilton

Feb. 19, 2026, © Leeham News: Airbus appears likely to launch the long-discussed stretched version of the A220-300, nominally called the -500, as early as the Farnborough Air Show in July.

Figure 1. This illustration, created years ago by Leeham News, shows the concept of a “simple stretch” for the “A220-500.” This illustration does not include some aerodynamic improvements LNA believes are necessary. Airbus is already planning a high-density version of the A220-300. Credit: Leeham News.

Lars Wagner, the new CEO of Airbus Commercial Airplanes, told Reuters in January that he favors the new aircraft, which would seat 165 passengers in single class configuration. Wagner assumed the position on Jan. 1. His predecessor, Christian Scherer, had long favored the stretch.

Wagner didn’t provide Reuters with any details about the new airplane. But Scherer told LNA last year that the debate within Airbus was whether to pursue a “simple” stretch or one with a larger wing and more powerful engines. A simple stretch trades range for capacity. Scherer told LNA that customers told Airbus they were more interested in capacity than range.

Figure 2: The ranges of the A220-300 and the proposed A220-500, using airline rules and calculated by LNA’s Aircraft Performance and Cost Model (APCM). Air France (CDG) and Delta Air Lines (ATL) have expressed interest in a stretched A220-300. Credit: Leeham News.

LNA confirms that a simple stretch is the preferred option. However, this does not mean that Airbus won’t tweak aerodynamics to improve operating and take-off performance and maintain as much range as possible. LNA has a good understanding of the likelihood of these tweaks and of the current proposed configuration of the A220-500. Using our proprietary Aircraft Performance and Cost Model (APCM), the -500 should have a range about 13% lower than the -300.

LNA’s APCM analysis is based on today’s information. The data is subject to final details when Airbus completes the design freeze.

Here’s our analysis.

Net Zero by 2050 is beyond reach, but R&D, SAF work continues

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Feb. 2, 2026, © Leeham News: When the International Air Transport Assn. (IATA) adopted its carbon Net Zero by 2050 policy at the October 2021  Annual General Meeting, it included milestones for increasing the use of Sustainable Aviation Fuel (SAF). The outline also included the adoption of alternative energy technologies like hydrogen, batteries, and hybrids.

Annual General Meeting, it included milestones for increasing the use of Sustainable Aviation Fuel (SAF). The outline also included the adoption of alternative energy technologies like hydrogen, batteries, and hybrids.

Tim Clark, president of Emirates Airline. A voice of reality when it comes to eco-aviation. Credit: Emirates Airline.

Some, including LNA, quickly concluded that the timeline and some of the technologies were unachievable. Tim Clark, the president of Emirates Airline, attended the IATA AGM. Don’t make promises you can’t keep, he told the assembly.

Since then, airlines across the globe have relaxed or even abandoned the IATA goals for their internal efforts.

SAF remains an elusive alternative. So does hydrogen. Battery-powered eVTOLs appear just around the corner for certification. However, developers of battery-powered commuter and regional airliners hit the reality that the weight of the batteries needed for even flights of a few hundred miles weighs more than is feasible. Some hybrid technologies appear to have promise, yet likely are technologies that appear to have promise for certain aircraft architectures, but need higher-performance batteries, which pushes these into the next decade.

Still, Europe continues to place a priority on sustainable aviation. Airbus, engine manufacturers and key suppliers continue their drive toward more sustainable aviation. However, Airbus backed off its 2035 target for a hydrogen-powered airplane. Rolls-Royce, key engine supplier MTU, and components supplier GKN, and others, strive for improving fuel efficiency and reducing emissions. Safran, a partner with GE Aerospace in the 50-50 joint venture CFM International, and an interiors manufacturer, likewise seeks environmental improvements to their products.

Related Article

In Asia, China is making a big bet on eVTOLs (and solar and automobile electric power). Its eVTOL industry is already flying in China. The country is the biggest producer in the world of solar panels and high-performance battery cells. China’s auto industry has a line-up of electric cars from small to luxury based on its battery technology.

GE 2026 Outlook: From LEAP Momentum to 777X Certification and the Rise of RISE

Subscription Required

By Chris Sloan, Tom Batchelor and Charlotte Bailey

January 22, 2026, © Leeham News: After a strong 2025 marked by rising output, expanding services, and improving execution, GE Aerospace enters 2026 with momentum building across four major programs that define its near- and long-term outlook: the GE9X and the long-delayed Boeing 777X as certification advances toward a 2027 entry into service; the LEAP program as record production levels combine with durability improvements that are beginning to take hold; the widebody GEnx franchise steadily growing its installed base and aftermarket contribution; and the RISE Open Fan as a high-risk, high-reward investment in next-generation single-aisle propulsion.

Throughout the year, strengthening supply-chain performance, rising engine deliveries, and robust services growth translated into improved financial results, reinforcing confidence that GE Aerospace’s operational recovery is gaining traction. Further detail was revealed when the company reported full-year 2025 earnings on Jan. 22. The company will test whether this momentum can be sustained—converting higher volumes, maturing reliability initiatives, and disciplined investment in future technologies into durable earnings growth, even as certification timelines stretch and the industry remains cautious about launching the next clean-sheet aircraft.

GE Aerospace’s latest engine application. Credit: GE.

Related Article

Dissecting Boeing’s 2025 orders and deliveries

By The Leeham News Team

![]() Jan. 16, 2026, © Leeham News: Boeing won more orders than Airbus last year. Airbus delivered more airplanes, given its higher production rates and Boeing’s long, slow path to recovery.

Jan. 16, 2026, © Leeham News: Boeing won more orders than Airbus last year. Airbus delivered more airplanes, given its higher production rates and Boeing’s long, slow path to recovery.

But a dissection of the numbers also shows positive results for Boeing.

Boeing 737 MAXes awaiting delivery at Boeing Field. Credit: Leeham News.

On top of Delta Air Lines’ breakthrough order for the 787-10, its first for any 787, United Airlines converted 56 787-9s to the 787-10. The 787-10’s seat-mile costs are the lowest in its class. If an airline doesn’t need the longer range of the Airbus A330-900, the A350-900, or the 787-9, the extra passenger and cargo capacity of the -10 is a winning combination.

The total twin-aisle passenger aircraft deliveries were 179 (91 Airbus A330 and A350, 88 Boeing 787s). It is far below the peak of 2015 (362), at the level of 2011 (179), and below the peak of the late 1990s cycle (227 in 1999). Boeing needs the 777-9 certification to reclaim its historical lead in twin-aisle passenger aircraft deliveries. Boeing handily dominates the twin-aisle order book.