Leeham News and Analysis

There's more to real news than a news release.

Does an A220-500 need a new wing and engines? Part 3.

Subscription required

By Bjorn Fehrm

May 29, 2025, © Leeham News: We are writing an article series about stretching the A220 to a capacity in the A320neo range. The idea is to replace the A320neo over time to make room in the A320/321 production lines for more A321s and extend the A220 family with a larger variant.

We analyzed what we need to change to bring the capacity to the level of the A320neo. We could achieve this with a fuselage stretch, but then the Maximum TakeOff Weight (MTOW) would need to increase to keep the A220 range. The wing and engines would then have problems, the takeoff run would get longer, and the climb to an efficient initial cruise altitude would be affected.

We now examine the potential fixes for these problems.

Figure 1. A rendering of an A220-500. Source: Leeham Co.

Summary:

- The A220-300 wing is not highly loaded compared to other Airbus single-aisle aircraft. With some modifications, it should be sufficient for an A220-500.

- The A220 engine is the mid-sized Pratt & Whitney geared turbofan, the PW1500G. It has limited thrust stretch capability. An alternative for a long-range (and thus heavier) A220-500 would be the CFM LEAP-1B from the 737 MAX.

Services are driving revenues and profits in difficult times, Part I

Subscription Required

By Karl Sinclair

May 15, 2025, © Leeham News: The aerospace industry is a maintenance-intensive operation, where strict regulatory rules drive many requirements.

Assets must be constantly maintained, governed by the time or usage an airline derives from them.

This goes for airframes, engines, and human resources.

Services account for a large part of aerospace corporate profits. Boeing’s Global Services division is the most profitable part of the company. Photo credit: Boeing Global Services.

Some equipment manufacturers derive little or no profits from product sales, but they make lucrative and long-term revenues from attached maintenance contracts.

Political factors are also coming into play in the services segment.

As airlines are forced into a difficult and expensive decision regarding the payment of tariffs on new aircraft they acquire, many could opt for a different strategy.

Older aircraft that were due for replacement with newer, more fuel-efficient jets will be sent into MRO facilities for an additional heavy-maintenance check.

With falling fuel prices playing less of a factor in the acquisition decision, airlines will be tempted to defer deliveries (thus avoiding the payment of tariffs) using their current assets in their installed fleets.

Extending an aircraft’s useful life by another six to seven years will allow carriers to simply wait out the tariff threat when things return to normal.

LNA looks into the growing services revenue segment among various companies in the aviation industry.

Does an A220-500 need a new wing and engines? Part 2.

Subscription required

By Bjorn Fehrm

May 5, 2025, © Leeham News: We started the articles series about stretching the A220 to a capacity in the A320neo range last week by going through the development of the A220-100 and -300, how it’s designed and compares to the competition in the 100 to 140 seat segment.

Now, we analyze what we need to change to bring the capacity to the level of the A320neo and whether changes to the wing and engines, in addition to prolonging the fuselage, are necessary when we increase its capacity.

We use the Leeham Aircraft Performance and Cost Model (APCM) to look at the design data for the A220-300 and discuss what it will mean to make the different changes.

Figure 1. A rendering of an A220-500. Source: Leeham Co.

Summary:

- The A220-300 has field and range performance that matches an A320neo.

- As we increase the length of the A220 fuselage to match the seating capacity of the A320neo, we run into tricky trade situations regarding range and field performance for an A220-500.

Airbus 1Q2025 results: So far, so good, but US tariffs make future results unpredictable

May 1, 2025, © Leeham News in Toulouse: Airbus CEO Guillame Faury and CFO Thomas Toepfer presented the Airbus 1Q2025 results yesterday. All Airbus divisions performed to plan, producing a group EBIT Adjusted of 0.6bn Euro.

![]() The company delivered 136 aircraft, which was to plan. The lower deliveries than last year (142) were due to CFM’s extra delivery efforts in 4Q2024, leading to fewer LEAP deliveries for 1Q2025. EBIT at €0.5bn and Free Cash Flow at -€0.3bn were also as planned.

The company delivered 136 aircraft, which was to plan. The lower deliveries than last year (142) were due to CFM’s extra delivery efforts in 4Q2024, leading to fewer LEAP deliveries for 1Q2025. EBIT at €0.5bn and Free Cash Flow at -€0.3bn were also as planned.

The big unknown going forward is the effect of the US tariffs and the trade war it has caused. Airbus CEO, Guillaume Faury, said, “Airbus will not cover tariffs applied to Airbus aircraft that are imported to the US for US customers (read A330 and A350). For A220s and A320s produced in Mobile for US customers, tariffs apply for parts that must be imported to produce these aircraft. The effects are here less clear as the tariff situation can change at any time”.

Does an Airbus A220-500 need a new wing and engines?

Subscription required

By Bjorn Fehrm

May 1, 2025, © Leeham News: For years, the debate has been going on about when Airbus will complement the A220-100 and -300 with a longer, higher-capacity A220-500.

In fact, the Bombardier team that designed the A220 as the CS300 already foresaw the prospect of a longer -500. The latest discussions have been around how much to stretch and whether a new wing and stronger engines are needed if the A220-500 replaces the A320neo in the Airbus lineup.

We use the Leeham Aircraft Performance and Cost Model (APCM) to examine the design data for the A220-100 and -300 and determine whether a stretched -500 would benefit from a new wing and stronger engines (which would then be the CFM LEAP-1Bs used on the Boeing 737 MAX).

Figure 1. A rendering of a possible A220-500. Source: Leeham Co.

Summary:

- The A220 started life as the CSeries, designed to compete with Embraer’s E-Jet E2.

- It has since added range through increased Maximum Takeoff Weights to enter the single aisle segment range-wise.

- A stretched A220 would expand the present A220 series upwards and potentially replace the A320neo for Airbus.

- We start by comparing the A220 to the E2, then we move on to examining whether an A220-500 can successfully replace the A320neo.

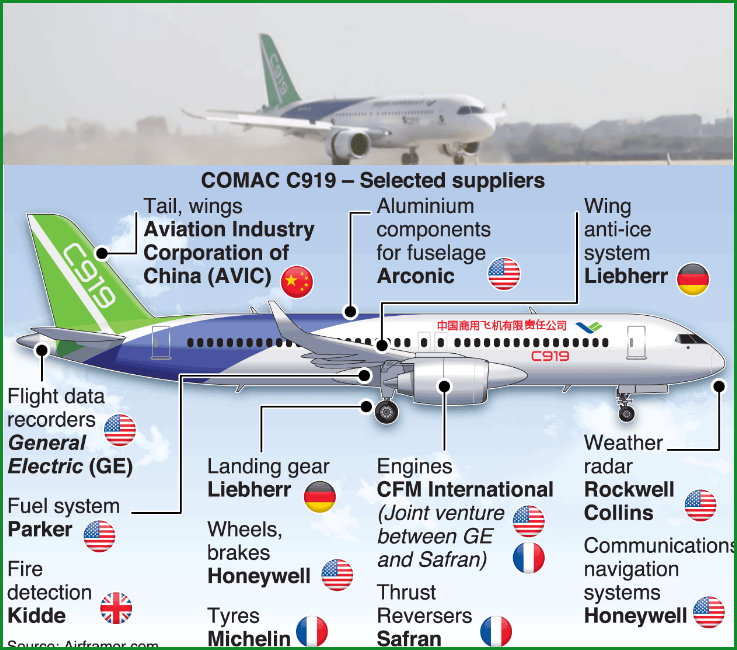

China bans Boeing, US parts imports in tariff war

April 15, 2025, © Leeham News: It was inevitable: China has banned its airlines from accepting deliveries of Boeing airplanes.

The move is in retaliation against President Donald Trump’s boosting tariffs on Chinese goods to 145%. Beijing placed retaliatory tariffs on US goods to 125%. During the first Trump administration, the president placed tariffs of 25% on Chinese goods imported to the US. Beijing has allowed delivery of very few Boeing jets since then.

Illustration of many of the systems and components COMAC sources for its C919 jet. The smaller C909 regional jet is similarly sourced. Credit: Airframer.com.

The move once more blocks Boeing from the world’s second biggest aviation trade market. Additionally, Beijing blocked the import of US-made parts, according to Bloomberg News, which first reported the actions.

Uncertainty plagues airline, aerospace, lessor industries over tariffs

Subscription Required

By Scott Hamilton

April 10, 2025, © Leeham News, Seattle: The airline and aerospace industries are plagued by uncertainty over the global tariffs announced by US President Donald Trump on April 2. The 90-day pause on nearly all tariffs announced yesterday doesn’t resolve the uncertainties. For the moment, they are only postponed.

Airbus’s A320 production plant in Hamburg, Germany. Credit: Leeham News.

Airframe and engine manufacturers, suppliers of components feeding them, and Buyer Furnished Equipment (BFE) directly to the airlines, lessors, aftermarket maintenance companies, and freighter conversion firms have many questions and no answers in chaos following Trump’s global tariff scheme.

Related Stories

Consider the unknowns:

- Will Trump tax the entire value of airplanes, engines, and components imported into the United States or just the foreign content? There is no guidance yet.

- Will other jurisdictions, notably the European Union, announce reciprocal tariffs? This is unknown because the Trump Administration hasn’t clarified what will be taxed.

- How will aircraft leased by non-US lessors be treated when US airlines are the customers? How will US lessors leasing to non-US airlines be treated? No answers.

- Contracts between lessors, airlines, Boeing, and Airbus don’t specifically address tariffs. Some airlines say they won’t pay tariffs because the contracts are silent. However, Boeing thinks there is a way to pass tariffs along. Airbus probably does, too.

- Over the last weekend, US-based supplier Howmet informed its customers it reserves the right to exercise the force majeure clause in its contracts to give it flexibility to suspend deliveries because of the tariffs. Other suppliers, including some engine companies, are following suit.

- At least one supplier has already billed some customers for delivered goods, including a tariff tax line item on the invoice.

- How will various jurisdictions treat aircraft converted into freighters with a mix of US and foreign content? There is no answer.

The US-based law firm Vedder Price issued its opinion and guidance on Tuesday on some issues.

Boeing at far greater risk of tariff impacts than Airbus

Subscripton Required

By Scott Hamilton

![]() April 7, 2025, © Leeham News: Tariffs against the rest of the world announced by US President Donald Trump last week threaten retaliatory tariffs against Boeing at a far greater level than Airbus faces, an analysis by LNA shows.

April 7, 2025, © Leeham News: Tariffs against the rest of the world announced by US President Donald Trump last week threaten retaliatory tariffs against Boeing at a far greater level than Airbus faces, an analysis by LNA shows.

Trump exempted no part of the world from tariffs where Boeing isn’t at risk for retaliatory tariffs. Airbus faces tariffs only in the US. Critics note that North Korea and Russia aren’t on the list; these two countries already are under steep economic sanctions. Nevertheless, the US had more than $3bn in Russian imports last year. Even Boeing’s domestic US deliveries potentially could be hit with tariffs on foreign-sourced parts, components and engines.

The situation is still fluid, and it is still unknown precisely how US tariffs will be applied to the aerospace industry. This will affect how retaliatory tariffs are applied to Boeing and Airbus, which sources much of its aircraft content (notably engines) from the US.

Accordingly, LNA’s analysis is necessarily highly preliminary. It’s also possible that more airplanes may be listed as at risk to tariffs than the final analysis would conclude.

Boeing potentially has three times more aircraft subject to retaliatory tariffs than Airbus has exposure in the US with its European and Canadian sales to US customers.

How good is the C919? Part 3.

Subscription required

By Bjorn Fehrm

April 3, 2025, © Leeham News: The COMAC C919 is finding its first customers outside China, which gives us a reason to examine the aircraft.

Last week, we estimated its efficiency versus its Western “look-a-like,” the Airbus A320neo. Now, we look at new variants that have been announced and how competitive these would be.

Figure 1. The C919 and its variants are analyzed by the Leeham Aircraft Performance and Cost Model, APCM. Source: Leeham Co.

Summary:

- The C919, sized like an A320neo, is the first variant in a family of aircraft.

- The next C919 variant is a shorter model for hot and high airfield operation.

- The following variant is an A321neo-sized aircraft.

Airbus launches Book and Claim SAF scheme

Subscription Required

By Scott Hamilton

March 31, 2025, © Leeham News: Airbus last week announced a program to boost Sustainable Aviation Fuel (SAF) called Book and Claim. Its purpose is to buy SAF credits in one location and take credit for them in another.

March 31, 2025, © Leeham News: Airbus last week announced a program to boost Sustainable Aviation Fuel (SAF) called Book and Claim. Its purpose is to buy SAF credits in one location and take credit for them in another.

The buyer can then claim in its corporate reports that it is meeting environmental goals, at least in part.

“This initiative aims to boost both supply and demand for SAF worldwide, providing a flexible and scalable solution to accelerate SAF adoption,” Airbus said at its annual environmental Aviation Summit.

“In simple terms, the book and claim approach allows a buyer to ‘book’ a certain amount of SAF and ‘claim’ the corresponding emission reduction, even if the fuel is used elsewhere. Through a pilot program running throughout 2025, Airbus will leverage this system to improve SAF accessibility for potential customers, particularly those with limited volumes and far from supply points,” the company said.

It’s an admirable effort for an industry that has so far fallen dramatically short of the SAF goals outlined by the International Air Transport Association (IATA) at its 2021 Annual General Meeting in Boston (MA).

However, LNA is skeptical about the effort. Carbon credits, which appear to be a variation, failed when airlines tried them. United Airlines CEO Scott Kirby called carbon offsets a “fig leaf” and “mostly a fraud.”

In land use regulations, Book and Claim sounds suspiciously like wetland mitigation programs. This is where a wetland is filled in for development and a new one may be created miles away, offsetting the environmental damage in the original location. At least this is the theory, and it’s essentially pencil-whipping. Nature doesn’t work this way for wetlands. LNA isn’t convinced it works this way for carbon, either.