Leeham News and Analysis

There's more to real news than a news release.

At long last, Boeing appears near certification and EIS for 777X

Subscription Required

By Scott Hamilton

July 14, 2025, © Leeham News: Boeing is still months away from receiving certification of its newest, largest jet—the 777-9—and the company didn’t bring one of the test airplanes to the Paris Air Show last month. However, officials showcased the passenger and freighter models in an experience center during the major international event.

Justin Hale has the imposing title of Customer Leader & Senior Product Marketing Director for 777X and Production Freighter aircraft

The 777X comes in three models: the 465-seat 777-9; the 777-8F cargo airplane; and the 777-8 passenger model, which is an ultra-long-range (ULR) aircraft. The program was launched in 2013 at the Dubai Air Show (even though the first order, from Lufthansa Airlines, was placed earlier). Entry into service (EIS) was planned for the first quarter of 2020 with an unofficial goal of December 2019.

Flight testing revealed some technical issues with the 115,000 lb thrust GE9X engines. These required engine removal and return to GE Aerospace for redesign, delaying the program by nine months. Further flight testing revealed some uncommanded nose-down flight anomalies, requiring software redesign.

Then two fatal crashes of the Boeing 737 MAX in October 2018 and March 2019 revealed design and certification problems with the MAX. Scrutiny by the Federal Aviation Administration (FAA) of the MAX program expanded to include a comprehensive review of the work done up to that point on the 777X. The COVID pandemic further stalled flight testing and certification work. The engine-mounted thrust links developed cracks during further flight testing, adding to the delays.

Now, Boeing sees the program is finally on track for certification this year and EIS next year.

Related Story

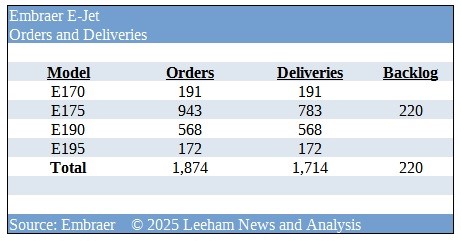

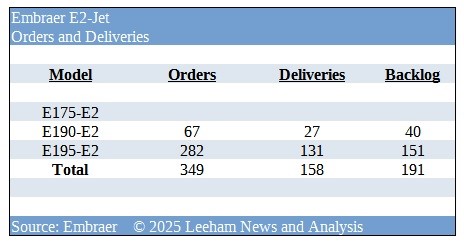

Embraer E2: Where will the orders come from?

Subscription Required

By Karl Sinclair

July 10, 2025, © Leeham News: At a subdued Paris Air Show, Brazilian aircraft manufacturer Embraer announced a firm order from US regional carrier SkyWest Airlines for 60 E175-E1 commercial aircraft, with purchase rights adding 50 planes to the order.

Embraer won a big order from SkyWest Airlines during the Paris Air Show. The E175-E1 is the mainstay of the carrier’s fleet. Credit: Embraer.

This brings the total SkyWest backlog to 74 aircraft, for a total backlog of 220 E1 jets for the variant; 211 of those aircraft are for American carriers.

While the recent SkyWest order is undoubtedly welcome news, the problem is that the rest of the commercial aircraft division is selling and producing the follow-on variant, the Embraer E2 line.

While the recent SkyWest order is undoubtedly welcome news, the problem is that the rest of the commercial aircraft division is selling and producing the follow-on variant, the Embraer E2 line.

The smallest variant of the E2 family, the E-175 E2, was placed on hold by the company until 2027-2028. This was due to the inability of American carriers to utilize the aircraft in service, resulting from the Scope Clauses with the various pilots’ unions. SkyWest once had a conditional order for 100 E175-E2s. The condition was that the unions would alter the Scope Clause restriction on the aircraft’s weight. The E2 exceeds the allowed weight by a few thousand pounds. The E1 complies.

Scope caps the maximum takeoff weight of an aircraft at 86,000 lbs, or 76 seats. The heavier and more fuel-efficient Pratt & Whitney geared-turbofan engines powering the type put the variant out of reach of US operators.

The commercial aviation industry is undergoing a transformation.

The commercial aviation industry is undergoing a transformation.

Carriers are opting for larger variants in a segment, as evidenced by the shift in orders at Airbus, away from the A320 to the larger A321 variant, and at Embraer, where the E170 is no longer in production. The dominant aircraft is the largest E195-E2, which accounts for 81% of all orders, compared to 9% previously.

US Transpo Secretary supports zero tariffs on aerospace, but change isn’t assured

Subscription Required

By Scott Hamilton

![]() July 7, 2025, © Leeham News: US Transportation Secretary Sean Duffy wants to return to aerospace’s zero-tariff agreement, dating to 1979, but cautioned that doing so requires a larger trade agreement between party governments.

July 7, 2025, © Leeham News: US Transportation Secretary Sean Duffy wants to return to aerospace’s zero-tariff agreement, dating to 1979, but cautioned that doing so requires a larger trade agreement between party governments.

Currently, the US has a minimum 10% to 25% tariff on aerospace imports from the European Union and Canada, with much higher fees in some cases. The EU is prepared to impose reciprocal tariffs on the US.

Tariffs have major implications for Airbus and Boeing. Although Airbus assembles A220s and A320/321s at its US Mobile (AL) plant, fuselages, wings and other components are imported into the US from Canada (A220s) and the EU (A320/321s).

Boeing exports planes to the EU, which includes 28 countries. Boeing has more exposure than Airbus.

Components imported by Airbus or Boeing for inclusion in the airplanes are also subject to tariffs.

A Boeing spokesperson told LNA that it can recapture tariffs on important components that are on aircraft subsequently exported. But this ignores the overarching tariffs the EU may apply to the completed airplane.

Related Articles

Christian Scherer, CEO of Airbus Commercial. Credit: Airbus.

In advance of the Paris Air Show, Airbus said that it’s going to adjust to US-imposed tariffs.

Responding to a question if it “made sense” for the Mobile plant to assemble A220s and A320/321s at the present rate given the impact of the tax, Christian Scherer said there will be no change. Airbus will live with the situation as it evolves. Scherer is the CEO of Airbus’s commercial operations.

Does an A220-500 need a new wing and engines? Part 4.

Subscription required

By Bjorn Fehrm

July 3, 2025, © Leeham News: We are writing an article series about stretching the A220 to a capacity in the A320neo range. The idea is to replace the A320neo over time, making room in the A320/321 production lines for more A321s and extending the A220 family with a larger variant.

We can increase the capacity to that of the A320neo by stretching the A220 fuselage. The next discussion was about how much we could increase the Maximum Takeoff Weight (MTOW) to accommodate more passengers and additional fuel, thereby maintaining the A220-300 range with a longer, heavier, and, therefore, draggier aircraft. We would need to find wing lift improvements and more thrust to keep the field performance close to the A220-300.

We now utilize the Leeham Aircraft Performance and Cost Model (APCM) to evaluate various changes to an A220-500 to optimize its performance.

Figure 1. A rendering of an A220-500. Source: Leeham Co.

Summary:

- An A220-500 can be designed to have close to the same fuel seat-mile economics as the A320neo. Our article series explains why beating the A320neo would be a challenge.

- It also looks into what a CFM LEAP-engined A220-500 would look like and how it would perform.

GE testing of giant GE9X engine aims for maturity at entry into service

Subscription Required

By Scott Hamilton

June 30, 2025, © Leeham News: GE Aerospace developed a huge engine for the Boeing 777X, the most powerful engine ever created. The GE9X tops out at 115,000 lbs of thrust.

The giant GE9X engine for the Boeing 777X generates 115,000 lbs of thrust. The human scale of the engine is illustrated here at a display at the Paris Air Show. Credit: Leeham News.

It’s had its development challenges. The 777-9, the first of the X family, was supposed to enter service in early 2020. Technical issues with the GE9X required removal of the engines from the test airplanes and a return to GE for fixes. This delayed flight testing by nine months. By then, certification of the 777X got caught up in the Boeing 737 MAX crisis; the 777X still is awaiting certification, which parties hope will come this year. Deliveries are now expected to begin next year.

Tim Clark, the president of Emirates Airline, has 205 Xs on order, more than any other customer, out of 521 in total. He’s publicly complained about the initial test results of the GE9X and demanded engine maturity before he’ll accept delivery.

GE has used the six year delay in the program to attempt to satisfy this demand.

Parent agency, FAA often at odds as politics outweighs safety

Subscription required.

By Colleen Mondor

June 26, 2025, © Leeham News: On March 12, 2019, then-Secretary of Transportation Elaine Chao and her staff flew from Texas to Washington (DC) on a Southwest Airlines 737 MAX. It was two days after the crash of Ethiopian Airlines flight 302, the second devastating accident involving the 737 MAX.

June 26, 2025, © Leeham News: On March 12, 2019, then-Secretary of Transportation Elaine Chao and her staff flew from Texas to Washington (DC) on a Southwest Airlines 737 MAX. It was two days after the crash of Ethiopian Airlines flight 302, the second devastating accident involving the 737 MAX.

In taking the flight, Chao showed not only her support for Boeing and Southwest, but even more so the Federal Aviation Administration (FAA), which steadfastly refused to ground the aircraft. As the pressure mounted, the agency stressed the importance of its methodical data-gathering process, which had begun months earlier with the October crash of Lion Air.

Chao also reassured the public, telling reporters “I want people to be assured that we take these accidents very seriously. We are reviewing them very carefully.” The day after her flight, President Trump announced that after conversations with Chao, the CEO of Boeing and Dan Elwell, the FAA’s acting administrator, his administration was grounding the aircraft. Elwell told reporters later that day, however, that the decision rested with the FAA. “So the decision is an emergency order to ground the airplanes,” he said, “and that is authority rested in the FAA with me.”

Chao’s flight centered her in yet another chapter of the ongoing saga between the Department of Transportation (DOT) and FAA. This was familiar territory for DOT which, since the FAA lost its independence in 1967, has often portrayed itself as the crucial, agent of flight safety in the U.S.

The most recent example was when current transportation secretary Sean Duffy captured media attention after the January 29 midair collision over Reagan National Airport. The FAA, which again had an acting Administrator, was relegated to secondary sound bites as Duffy declared, “We are going to take responsibility at the Department of Transportation and the FAA to make sure we have the reforms…to make sure that these mistakes do not happen again and again.”

Engine makers tout “Plan A” but have “Plan B” backups in R&D

Subscription Required

By Scott Hamilton

June 23, 2025, © Leeham News, Paris: CFM International touts its Open Fan RISE engine as the wave of the future. (CFM is a 50-50 joint venture between GE Aerospace and Safran.)

Rival Pratt & Whitney says evolution of its Geared Turbo Fan is the best engine choice going forward.

CFM’s Open Fan engine design called RISE. Credit: CFM.

Neither company will admit that it is also researching and developing a Plan B engine. For CFM, this is a conventional turbofan. For PW, this is a new Open Fan. But during the Paris Air Show, LNA confirmed that both have a Plan B engine in development.

PW has gone out of its way to dismiss the very idea of an Open Fan engine. Rick Deurloo, the president of Pratt & Whitney Commercial, won’t even talk about the “competitor.” Deurloo makes it clear—publicly, at least—that an evolution of PW’s Geared Turbo Fan (GTF) is the best solution for the next generation engine for the single aisle market, in its view.

Mike Winter, RTX’s Chief Engineer, dismissed the Open Fan as “sub-optimal” on a successor to the Airbus A320neo and Boeing 737 MAX families. It involves too many installation compromises on this size aircraft, he says. RTX is the parent of PW.

But, says one person with direct knowledge, PW fully understands that if CFM is successful in solving all the challenges of an Open Fan and meets the publicly stated goal of improving fuel consumption by 20% compared with today’s GTF and CFM LEAP engines, PW’s gain of an evolutionary GTF won’t be competitive.

So, says the person with direct knowledge of PW’s activities, the development of an Open Fan alternative engine is being worked on as PW’s Plan B.

Furthermore, PW’s sister company, Pratt & Whitney Canada, publicly disclosed its development of an Open Fan engine in a briefing on Tuesday this week. This engine is for a new 70-100-seat aircraft designed by the start-up company MAEVE. PW is following PWC’s development.

Airbus sees Boeing as medium-term competitor, with Comac next

By Scott Hamilton

![]() June 14, 2025, © Leeham News: Airbus and Boeing forecast a significant production gap during the next 20 years of more than 2,000 aircraft per year in their current outlooks released in conjunction with the Paris Air Show. The event begins Monday.

June 14, 2025, © Leeham News: Airbus and Boeing forecast a significant production gap during the next 20 years of more than 2,000 aircraft per year in their current outlooks released in conjunction with the Paris Air Show. The event begins Monday.

Neither company can fill this gap given their current production rates and the goals they have for the rest of this decade.

This means other manufacturers must step up. The question is who?

China’s Comac is current producing a competitor to the Airbus A320neo and Boeing 737 MAX, the C919. But the production rate is excruciatingly low.

Comac also has plans for a widebody airplane to compete with the Airbus A330-900 and Boeing 787. If past is prologue, development of this aircraft will be much longer than the target entry into service of 2029.

Embraer currently is the world’s third largest airliner manufacturer. However, its jets seat between 76- and 144 seat. The company is studying whether to enter the mainline jet sector, but the decision seems a year or more away.

Start-up JetZero wants to develop a Blended Wing Body aircraft for the 250-300 seat sector. But it has little money, no engine and, LNA believes, little hope of meeting the ambitious timeline of having a demonstrator aircraft by 2027.

In a media briefing on June 13, Airbus named Boeing as its medium-term competitor; China is most like to become one; Embraer is a question mark; and JetZero appears to be making little progress, in its view.

Airbus Canada CEO: Airbus is here to stay in Canada

Subscription Required

By Karl Sinclair

June 14, 2025, © Leeham News: Airbus Canada President and CEO Benoit Schultz is quietly confident that the A220 program has turned the corner and put the worst of its recent problems in it rear-view mirror.

Hosting the official opening of the Mirabel Delivery Centre (CDL), where airline representatives arrive to inspect and formally accept possession of their aircraft, he was definitive in how committed the company is to the program. “I want to say Airbus is in Canada, in Quebec, to stay. We’ve made that investment in the program now seven years ago with the view of the long-term partnership and with the view of the value that we can bring to our customers building our aircraft here in Canada.”

Credit: Airbus Canada

Credit: Airbus Canada

In addition to the pandemic and tariff hurdles that all OEMs have had to grapple with, the A220 was hit with engine snags, due to a problem with the Pratt & Whitney geared-turbofan (GTF) powered-metal coating.

This limited the time-on-wing (ToW) interval, which is getting resolved. Current engine deliveries, fresh from the factory, are approaching 10,000 hours before heavy maintenance checks, according to Schultz – with further improvements forthcoming.

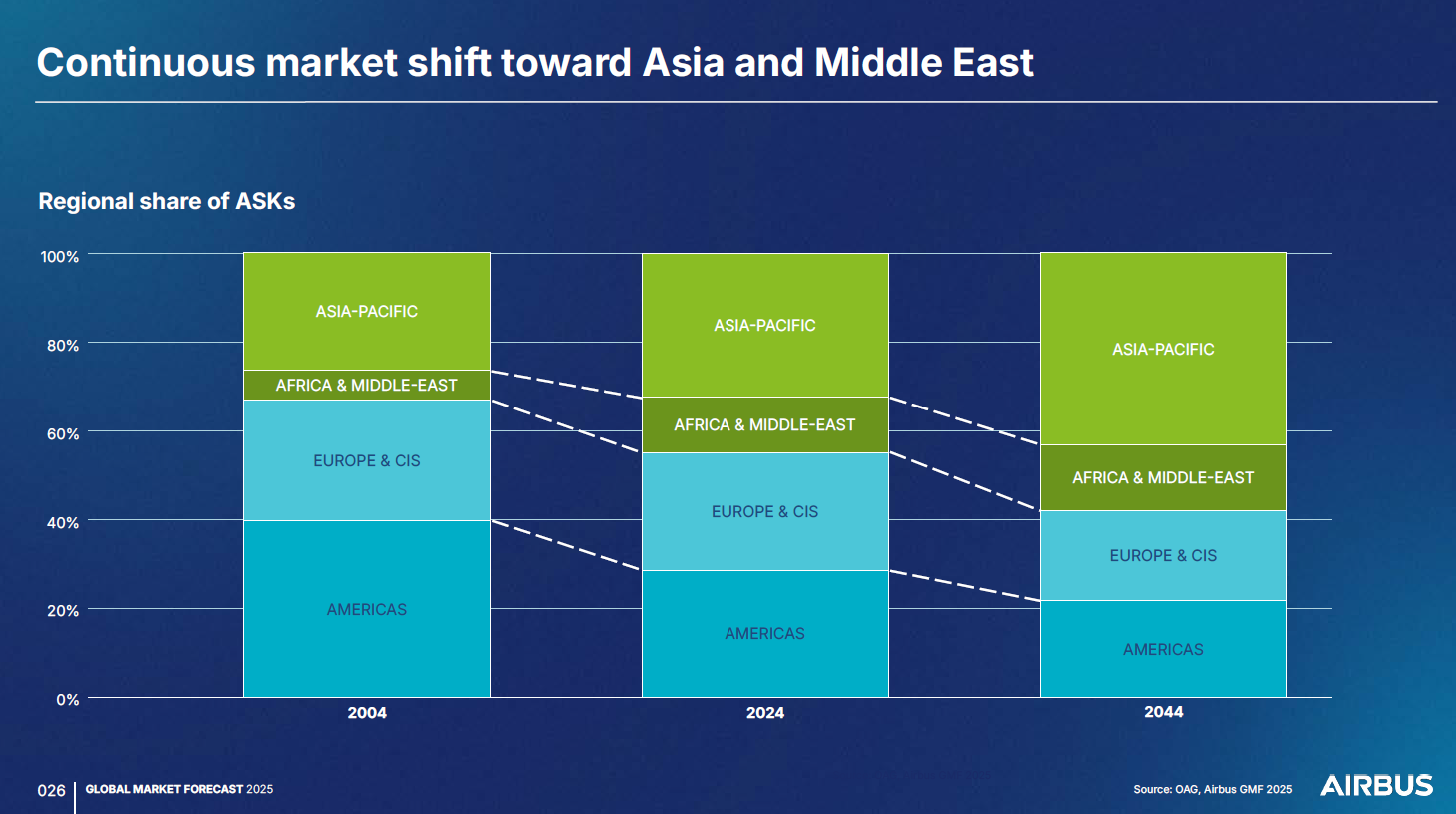

Airbus forecasts that almost three times more aircraft needs to be produced by year 2044

Subscription required

By Bjorn Fehrm

Thursday, 12, 2025, © Leeham News: Airbus has released its forecast for new airliners needed between 2024 and 2044. The forecast says there is a need for 43,420 new aircraft over the next 20 years. It means we need to produce and deliver an average of 2,170 aircraft per year during the period.

During 2024, the world deliveries were 1,200 airliners. To meet the Airbus-predicted demand, production and deliveries of aircraft by 2044 must almost triple.

We examine what this means for the existing OEM structure and the opportunities it presents for new players in the commercial aircraft industry.

Figure 1. The Airbus predicted shift in air travel from Europe and Americas to Asia-Pacific. Source: Airbus.

Summary:

- The growth in air travel and, consequently, the demand for new aircraft is expected to continue unabated over the next 20 years.

- With 1,200 aircraft delivered in 2024 and the need for more than 3,000 aircraft by 2044, there are opportunities for new players to enter the market.