Leeham News and Analysis

There's more to real news than a news release.

The state of alternative propulsion aircraft? Part 8.

Subscription required

By Bjorn Fehrm

March 19, 2026, © Leeham News: In our series on the state of alternative propulsion projects, we have analysed electric hybrid projects and found that these do not make for an operationally acceptable airliner. They are more expensive in production, thus in purchase, and their operational costs are not lower than the aircraft they shall replace.

Projects analyze hybrids after realizing that battery-electric airliners are too limited in range. But soon, the problem areas of hybrids become clear. The studies then swing to hydrogen propulsion systems.

Figure 1. The Airbus ZEROe hydrogen-fueled concepts for a future airliner. Source: Airbus.

These have new technical challenges but produce aircraft with operationally acceptable range. We now examine the various concepts for hydrogen-fueled propulsion and outline their challenges and capabilities.

Change Incorporation, Configuration Control, and the High Cost of Getting It Wrong

Editor’s note: Boeing spent years doing rework on the 737 MAX and the 787 after the former’s grounding following two fatal crashes and the latter’s production flaws. “Shadow factories” began the 737’s rework after the 21-month grounding was terminated in November 2020. The last of 450 airplanes was delivered in 2025. Deliveries of the 787 were suspended in October 2020; 110 aircraft needed rework. The last of this inventory was cleared in 2025. This work is also known as “Change Incorporation.” Thirty-five 737 MAX 7s and 10s have been built and await certification, which idepends on design changes that must be retrofitted once the Federal Aviation Administration signs off. Change incorporation took 3-4 months for the 787s and was measured in months for the 737s.

More than 30 777-9s have been built while this program awaits FAA certification. This, too, will require Change Incorporation. Boeing has not revealed what changes the FAA will require, although revised flight control software is known to be one element. Nor has Boeing revealed how long Change Incorporation for the 777-9s will take.

LNA’s news team explains what Change Incorporation is, how it is undertaken, and the implications for the 777-9s in inventory.

Subscription Required

By the Leeham News Team

March 18, 2026, © Leeham News: In the commercial aviation industry, building aircraft before the type certificate is formally issued is not unusual. It is an economic necessity.

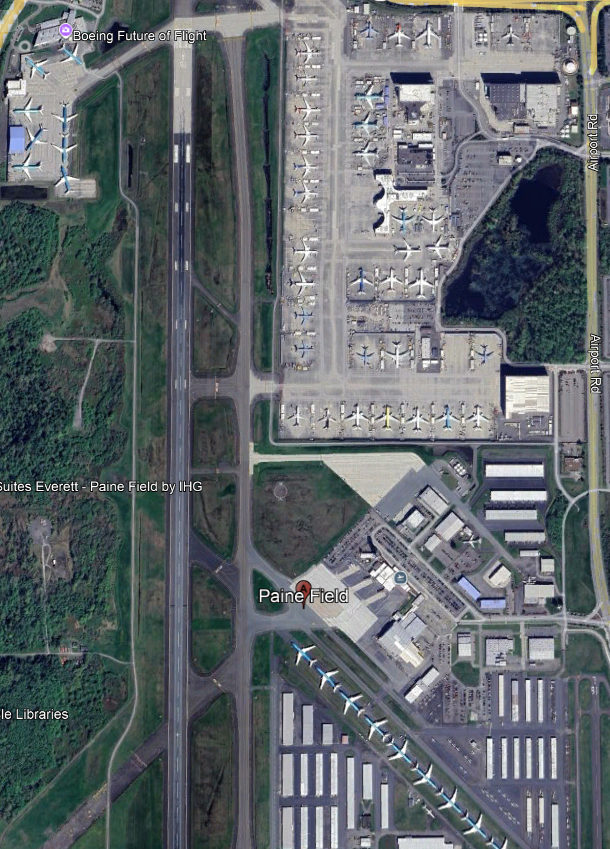

Undelivered Boeing 777-9s (among other aircraft) are lined up in open-air storage in this undated 2025 Google Earth photo of Paine Field, Everett (WA). The 777s are the “green” airplanes, though more are also painted in other colors.

Launching a production line months or years before final regulatory approval allows manufacturers to meet early delivery commitments, recoup development investment more quickly, and maintain customer relationships. But this strategy carries a profound and often underestimated technical liability: when the approved design specification continues to evolve through flight test, the already-built airframes must be brought into conformance with the final certified configuration. This is the essence of the Change Incorporation process.

The Boeing 777X program offers the most current illustration of this challenge. As of early 2026, Boeing has assembled more than 30 777-9 airframes, all built to early-production standards, while the aircraft’s type certificate is still in progress.

At the same time, the January 2024 in-flight separation of a door plug from Alaska Airlines Flight 1282—an event traceable directly to failures in Boeing’s parts removal and reinstallation process—has thrown the Change Incorporation process into the spotlight.

These two stories are connected by a single systemic thread: the consequences of inadequate configuration discipline in a complex, multi-stakeholder manufacturing environment.

Air Lease merger this year creates new lessor powerhouse

Subscription Required

By Karl Sinclair

March 16, 2026, © Leeham News: Aircraft lessor giant Air Lease Corporation (ALC) of Los Angeles (CA) closed the books on 2025 and reported record figures.

March 16, 2026, © Leeham News: Aircraft lessor giant Air Lease Corporation (ALC) of Los Angeles (CA) closed the books on 2025 and reported record figures.

In early 2026, the company will cease to exist. The Sumitomo Corporation, SMBC Aviation Capital, Apollo, and Brookfield funds are expected to acquire Air Lease Corporation for $7.4bn in the early part of this year and rebrand it the Sumisho Air Lease Corporation (SALC). SALC will be a new powerhouse lessor that Airbus, Boeing, and the engine makers will be dealing with.

According to ALC, Air Lease Class A common stockholders will receive $65 in cash for each share of Class A common stock of Air Lease held immediately prior to the effective time of the merger.

SMBC will then service most of Sumisho Air Lease Corp.’s fleet, significantly expanding its service portfolio.

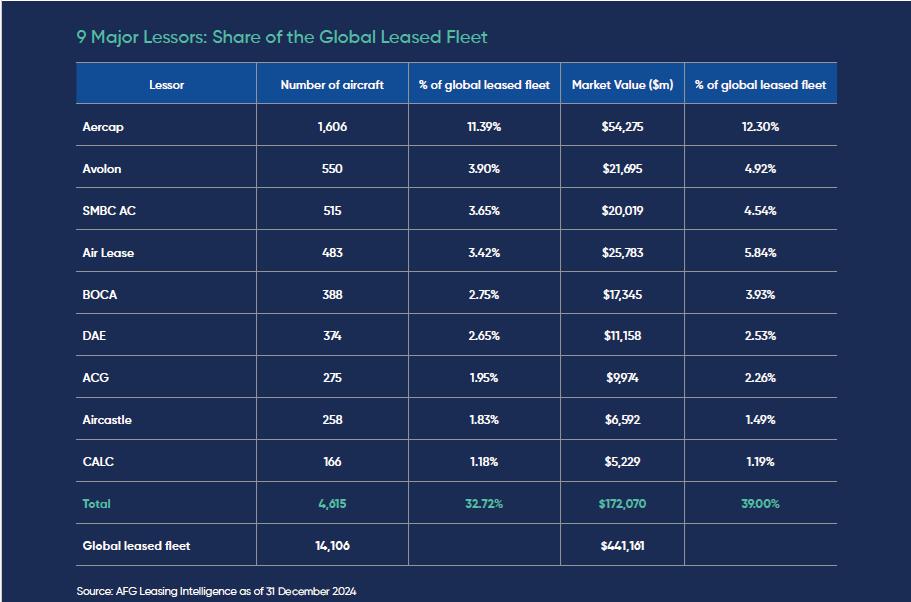

Thus, the world’s second-largest commercial aircraft lessor will be born, as the third and fourth largest lessors merge (by fleet size in the 2025 Airfinance Global annual lessors analysis), second only to Aercap of Dublin (IR).

Source: Airfinance Global 2025 Annual Lessor Report.

The state of alternative propulsion aircraft? Part 7.

Subscription required

By Bjorn Fehrm

March 12, 2026, © Leeham News: In our series on the state of alternative propulsion projects, we are analysing where the electric hybrid projects are and how parallel hybrids work and perform.

Figure 1. The Pratt & Whitney Parallel Hybrid DH8-100 test aircraft, presently under preparation. Source: Pratt & Whitney

We summarized the status last week and compared it to the serial hybrids that we analyzed before Christmas. Serial hybrids are motivated in special cases, but in general, they make an aircraft more expensive to produce and operate.

For those who react, “But hybrid work very well for cars”?, let’s summarize: The car thermal engines are energy hogs, and you brake away all the acceleration energy at the next stoplight. Hybrids reduce this waste by recovering energy during braking. Aircraft and aircraft engines are wonders of efficiency by comparison, and there are no energy-recovery phases in an airliner mission.

We now use our Aircraft Performance and Cost Model (APCM) to go deeper into the parallel hybrid. Can it avoid the negative verdict of the serial hybrid?

Supply chain is improving, but the light at the end of the tunnel could be a train

Subscription Required

By Scott Hamilton

Kevin Michaels, AeroDynamic Advisory. Credit: PNAA.

March 9, 2026, © Leeham News: Every year since the end of the global COVID-19 pandemic, everyone associated in whatever capacity with aerospace has complained about the supply chain.

There is a workforce shortage.

Suppliers are unable to meet contractual deadlines.

Airbus and Boeing haven’t been able to deliver their airplanes on time. Sometimes the aircraft are months later.

Engine makers are to blame.

Interior suppliers are to blame.

The little supplier making the widget is to blame.

Delays still plague the industry, but at long, long last, there seems to be a light at the end of the tunnel.

“I don’t want to focus just on the negatives. The bottom line is that the supply chain is improving. You talk to most executives at OEMs, they’ll tell you that supply chain is in better shape today than it was a year ago or two years ago,” said Kevin Michaels, managing director of the supply-chain consulting firm Aerodynamic Advisory.

Nevertheless, there’s a very real possibility that the light is from another set of oncoming trains.

“We’ve had some very interesting dynamics this year,” Michaels said during an appearance last month at the annual Pacific Northwest Aerospace Alliance (PNAA) conference.

What’s on those trains?

Regulatory bottlenecks and rare earth production concentration and shortages are just two of the overarching areas continuing to face the aerospace industry. Engines and interiors remain challenging.

“Resilience is key” to Airbus production ramp-up

Subscription Required

By David Slotnick

March 5, 2026, © Leeham News: Airbus’ head of procurement shared a rallying cry for both OEMs and suppliers at the Pacific Northwest Aerospace Alliance (PNAA) in suburban Seattle on Feb. 10, ahead of the European planemaker’s plans to increase production to record-breaking rates.

Florian Seidel. Source: Florian Seidel.

In a speech at the annual conference, Florian Seidel, the chief of strategic procurement at Airbus Americas, urged the entire supply chain from top to bottom to focus on working “like Swiss clockwork” as manufacturing increases and airline customers continue to require support throughout each aircraft’s operating life.

The call for continued close collaboration and efficiency comes as Airbus sets its sights on production rates that exceed even peak pre-pandemic levels. While Airbus plans to increase rates on all of its commercial programs, Seidel described the target on the A320-family — 75 per month in 2027 — as “the most impressive” ramp-up, requiring a “huge effort across the entire supply base.” (Update: A week later, during the Airbus earnings call for 2025, this target has shifted to 2028.)

Additionally, Airbus plans to grow the A220 to 12 per month this year, the widebody A330 to 5 per month by 2029, and the flagship A350 to 12 per month in 2028.

“Resilience is key” to making that ramp-up successful and sustaining those rates, Seidel said.

“This is a ramp-up that’s unprecedented, and that we require the resolve of the entire supply base to make it happen,” he added.

The state of alternative propulsion aircraft? Part 6.

Subscription required

By Bjorn Fehrm

March 5, 2026, © Leeham News: Before Christmas, we started a series examining the status of alternative propulsion projects. We finished on December 18 by looking at Series Hybrids, often as battery-electric aircraft with range extenders (Figure 1).

The range extender is the natural next step when a project realizes that a pure battery-electric aircraft won’t be able to fly the missions the market is asking for.

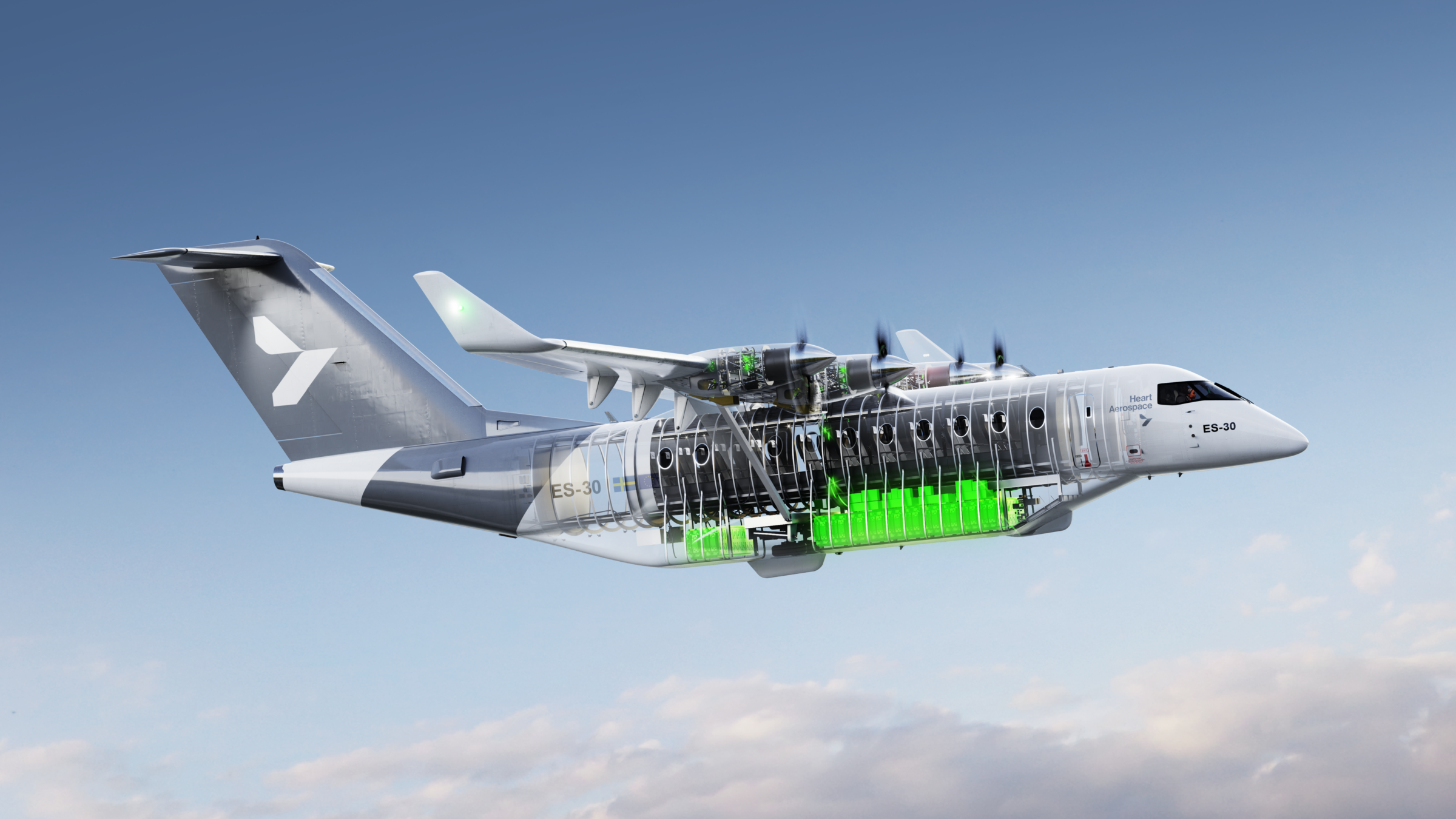

Figure 1. The Heart Aerospace Battery-Rlectric ES-30 with dual range extending turbo-generators in the back. Source: Heart Aerospace.

After a while, analysing the range extender, the drawbacks become increasingly obvious. Charging the battery system in flight or directly feeding the electric propulsion system from a turbogenerator is inefficient. The losses along the path from the gas turbine through a generator, an inverter, and then to a motor that drives a propeller or fan are much higher than when the gas turbine drives the propeller directly.

A series hybrid can’t compete on operational economics with the aircraft it shall replace (for example, the Cessna Caravan or the SAAB 340). Projects then turn to parallel hybrids, the subject of today’s article.

Airbus: Repeatedly Missing the Mark on delivery guidance

Subscription Required

By Karl Sinclair

March 2, 2026, © Leeham News: With the closing of the 2025 financial year, Airbus SE (AB) estimated how many commercial aircraft it expects to deliver to customers in the coming 12 months.

March 2, 2026, © Leeham News: With the closing of the 2025 financial year, Airbus SE (AB) estimated how many commercial aircraft it expects to deliver to customers in the coming 12 months.

Along with guidance on expected revenues, profits, and free cash flow (FCF), investors and analysts use delivery metrics to assess not only Airbus’s success but also how the heavily integrated supply chain beneath the OEM is functioning.

It only takes one missing part to keep an aircraft glued to the tarmac, and as the old adage goes, “When a supplier has a problem, Airbus has a problem.” Even when it is buyer-furnished-equipment (BFE), like interiors.

Airbus has missed its aircraft delivery guidance in each of the last three years. The company had to reduce its guidance as the lack of engines, BFE, other parts, and quality control issues combined to cause Airbus to miss its early guidance.

Related Article

How close do the estimates provided by Airbus, some 12 months out, come to reality at year-end?

Are the projections pie-in-the-sky numbers or can they be safely relied upon to provide a clear picture of the short-term future?

LNA takes a deep dive into Airbus guidance accuracy by analyzing the original projections for the previous three years, any changes that it has made to those targets, and how well those prognostications held up at year-end.

Boeing defects and rework fell due to better supplier relations: exec

By Justin Bachman

Feb. 26, 2026, © Leeham News: Boeing has seen quality rework hours on aircraft production drop 40% over the past year as its supplier base has trimmed defects, aiding the company’s recovery, Boeing’s supply chain head said.

Ihssane Mounir, the head of the Boeing Commercial Airplanes supply chain, at the 2024 PNAA conference. Credit: Leeham News.

The rework decrease through 2025 is “incredible and very significant,” Ihssane Mounir, senior vice president of Global Supply Chain and Fabrication for Boeing Commercial Airplanes (BCA), told supplier partners, speaking Feb. 11 at the annual Pacific Northwest Aerospace Alliance (PNAA) conference in suburban Seattle.

“When you think about how that happened, it’s a whole slew of things that had to happen to drive the number down that way,” Mounir said in a talk that touted Boeing’s recovery to its supplier partners after six years of crisis and production problems.

Mounir assumed the role of SVP, Supply Chain and Fabrication, in December 2022, following six years as BCA’s top sales executive.

“It’s you paying attention to quality. It’s us augmenting our quality in our engineering teams, our fabrication teams, and our support teams, and putting them with you and helping you,” he said. “It’s us increasing our engineering support and being more responsive to the changes and to the asks and the analyses that come our way.”

The prevalence of supply-chain defects and Boeing’s need to rework incoming parts and subassemblies during production had become a source of deep conflict between the company and many of its 1,200 suppliers for several years.

When does Boom go boom; military goes green and loses the battle

Subscription Required

By Scott Hamilton

Feb. 23, 2026, © Leeham News: “How long until Boom goes boom?”

“eVTOLs, the perfectly mediocre over-priced helicopter.”

“We lost the battle, but we had a lower carbon footprint.”

These are just a few of the pithy comments to come out of the annual Pacific Northwest Aerospace Alliance (PNAA) conference this month in suburban Seattle.

Boom, the 88-passenger supersonic transport program, was founded in December 2014. Ten years later, it flew a demonstrator aircraft that bears no similarities to the Overture SST that the company is developing as the first passenger SST airliner since the Concorde.

The Boom Overture SST has many, many skeptics. Two were speakers at the annual conference of the Pacific Northwest Aerospace Alliance. Credit: Boom.

No established engine maker agreed to power the Overture. Rolls-Royce had an exploratory contract for a time, but bowed out. Boom cobbled together three companies to make an engine. More recently, the company is going to use the engine, whenever it works, to power energy plants.

There are few believers in aerospace who think Boom will be successful, despite raising a reported $600m-plus in funding, building a production facility and winning conditional orders from Japan, United and American airlines.

Richard Aboulafia, a managing director of Aerodynamic Advisory, said he would just “write off” Boom. Kevin Michaels, also an MD at the same consultancy, was just as direct. “We have a bet in our office going how long until Boom goes boom?”

They were no more kind toward the prospect of eVTOLs, especially the possibility of the US military using battery-powered eVTOLs on the battlefield.