Leeham News and Analysis

There's more to real news than a news release.

GE Aerospace FY and Q4 2025 Earnings Thrust Higher Propelled by Services Growth, LEAP Volume and Expanding Margins

By Chris Sloan

Jan. 22, 2026, © Leeham News: GE Aerospace closed 2025 with a materially larger order book than in prior years, underscoring sustained demand across both commercial and defense markets as the company continues to lean on its services-heavy business model. Chairman and Chief Executive Officer Larry Culp said 2025 marked a year of operational progress and execution. “2025 was an outstanding year for GE Aerospace as we made operational progress, delivered on our financial commitments, and continued to invest in our future,” Culp said.

Jan. 22, 2026, © Leeham News: GE Aerospace closed 2025 with a materially larger order book than in prior years, underscoring sustained demand across both commercial and defense markets as the company continues to lean on its services-heavy business model. Chairman and Chief Executive Officer Larry Culp said 2025 marked a year of operational progress and execution. “2025 was an outstanding year for GE Aerospace as we made operational progress, delivered on our financial commitments, and continued to invest in our future,” Culp said.

The fourth quarter provided a strong finish to the year, with management pointing to robust demand for both services and equipment as customers continued to prioritize engine availability and fleet utilization. For the full year, the company cited improvement across its key operating measures, supported by growth in both Commercial Engines & Services and Defense & Propulsion Technologies. Culp highlighted a backlog of roughly $190bn—nearly $20bn higher than a year earlier—as evidence of sustained demand across commercial and defense customers. “GE Aerospace is an exceptional franchise,” Culp said, pointing to the company’s installed base of approximately 80,000 engines. He added that continued deployment of the FLIGHT DECK operating model is expected to improve execution and customer support across the fleet.

Analysts said the results reinforced the durability of GE’s aftermarket-driven earnings profile. “A robust conclusion to 2025 from GE, with the engine aftermarket continuing to produce strong growth,” said Robert Stallard of Vertical Partners Research. “While this growth is expected to ease in 2026, it should be roughly similar to OEM growth, and so GE should not see a meaningful mix shift.” Similarly, Seth M. Seifman of J.P. Morgan said the fourth-quarter results were solid and that the initial outlook suggests operating profit could exceed current consensus. “It’s always hard to know how good is good enough,” Seifman said, “but we view the results as solid… and the potential for upward revisions appears to be in place.”

Image courtesy: GE Aerospace

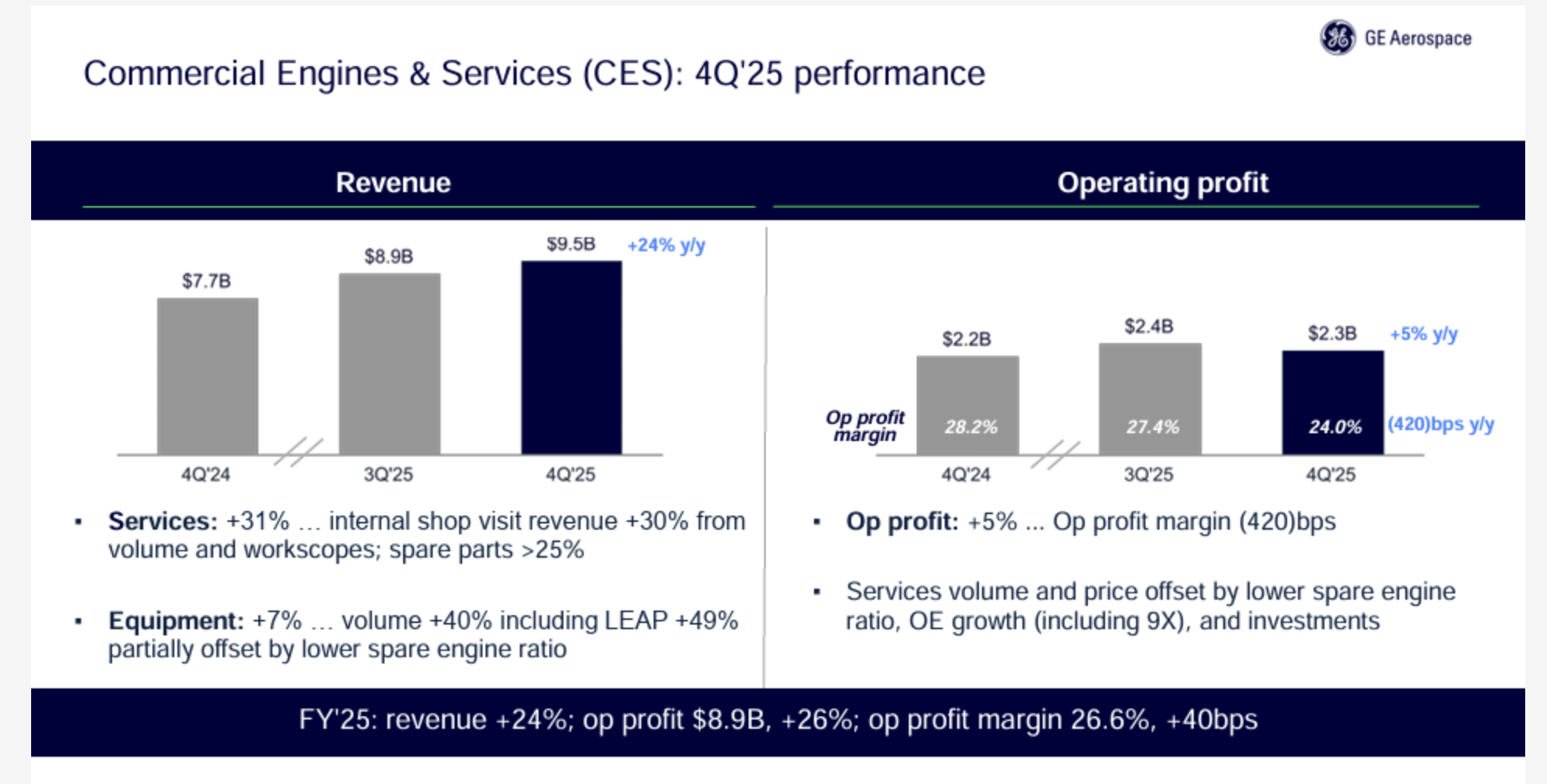

CES Books Big Orders as Services Lead Growth

Commercial Engines & Services remained the primary growth engine in 2025, supported by higher engine output, strong services demand, and a surge in new engine commitments. Commercial unit deliveries increased 25% for the year, including a 28% increase in LEAP deliveries, taking total LEAP output above 1,800 engines—the highest annual level for the program. At the Dubai Airshow, the company recorded more than 500 engine wins across narrowbody and widebody platforms. These included Riyadh Air’s commitment for 120 LEAP-1A engines, flydubai’s selection of 60 GEnx engines, and Pegasus Airlines’ commitment for up to 300 LEAP-1B engines for its future Boeing 737-10 fleet. GE Aerospace also added Delta Air Lines as a new GEnx customer, with the carrier selecting the engine to power and service 30 Boeing 787 aircraft.

The company said CES orders increased 35% for the year, with services revenue and engine output both rising by roughly 25%, reflecting higher internal shop visit activity and improved throughput. GE predicts CES is expected to continue growing in 2026, with mid-teens revenue growth driven by services. That outlook includes mid-teens growth in internal shop visit revenue and spare-parts sales, supported by low double-digit engine removals, higher work scopes, and pricing. Ghai added that LEAP internal shop visits are expected to increase about 25%, while equipment revenue is expected to grow at a mid- to high-teens rate, including LEAP deliveries up about 15%, with higher growth coming from widebody programs.

Image courtesy: GE Aerospace

CFM LEAP: Volume Ramps as Market Share and Fleet Maturity Drive the Next Phase

Deliveries of the LEAP accelerated in the fourth quarter as GE Aerospace continued to ramp production while advancing durability and services initiatives tied to the program’s maturing fleet. The company delivered 562 LEAP engines in the fourth quarter of 2025, up 10% sequentially and 49% year over year, bringing total LEAP deliveries for the year to 1,802 engines, an increase of 28% from 2024. Management said the higher volumes reflect improving production cadence alongside sustained narrowbody demand.

The LEAP holds an exclusive position on the Boeing 737 MAX, serving as the sole engine option across the MAX family. On the Airbus A320neo family, the LEAP-1A continues to hold a market share edge over the competing Pratt & Whitney GTF, benefiting from airline preference following durability challenges that have constrained the GTF fleet in recent years. With production rates for both the 737 MAX and A320neo expected to increase further in 2026 and 2027, LEAP output will need to continue scaling to support higher airframe build rates, placing sustained pressure on manufacturing, supply chain execution, and aftermarket readiness. The CEO boasted that the company remains on track for LEAP original equipment profitability. “Yes, we expect LEAP OE to be profitable in 2026 as per our prior plans,” Culp said.

Culp also pointed to progress on durability as a key driver of improving economics. He said the LEAP-1A durability kit is expected to improve time on wing by more than two times, bringing performance in line with the industry-leading CFM56. The durability kit has now been incorporated into all new LEAP-1A engine deliveries and shop visits, with nearly 1,500 kits shipped since certification. In addition, the company has expanded its LEAP repair catalog, which it said is expected to lower the cost of ownership and improve turnaround times.

On services, Culp said the number of LEAP parts certified for repair increased 20% in 2025 and is expected to continue growing in 2026, as the company works to meet customer expectations on the program. Ghai disclosed that LEAP services’ profitability continues to improve as more repairs are performed internally and through external channels. He said the number of certified repairs is expected to continue increasing, and that higher shop visit volumes should drive additional productivity gains. “All those points to the LEAP services tailwind kind of continuing here,” he said.

The LEAP entered service nearly a decade ago on the A320neo and on the first flight of the 737 MAX. Image courtesy: CFM

GE9X and GEnx: Widebody Programs Diverge as Volume, Durability, and Market Share Evolve

Progress across GE Aerospace’s widebody engine programs continued in 2025, with the GE9X and GEnx following different trajectories as one ramps toward higher volumes tied to aircraft certification and the other benefits from long-term durability gains and market share leadership. Ghai said losses on the GE9X program ended in 2025 in line with expectations. “We said a couple of hundred million bucks of losses in 2025, and we’ve ended right about there,” Ghai said. Looking ahead, he said shipments are expected to increase in 2026 as volumes continue to grow, with losses on the program expected to double year over year.

The GE9X, the largest commercial aircraft engine ever produced, exclusively powers the Boeing 777-9, which has faced multiple delays but is now moving toward certification. Entry into service is planned for next year. As the aircraft program advances, GE expects engine shipment volumes to rise accordingly. Order activity continues to build around the program. At the Dubai Airshow on Nov. 17, Emirates announced a deal to acquire 130 GE9X engines to power 65 new Boeing 777-9 aircraft. The total value of the aircraft and engine order was placed at $38bn. The agreement makes Emirates the largest GE9X customer globally, with more than 540 engines now on order to support the airline’s planned expansion of its 777X fleet.

On the GEnx program, the CEO highlighted continued progress in durability in service as the engine approaches a significant milestone. The GEnx powers the Boeing 787 Dreamliner and will mark its 15th year in service later this year. The company confirmed that the upgraded high-pressure turbine blade engine achieved a new milestone in November, surpassing 4,000 cycles. The upgraded blade has improved time-on-wing by more than 2.5 times in hot, harsh operating environments. The durability gains have supported the GEnx’s strong position on the 787 platform. GE Aerospace commands roughly two-thirds of the 787 fleet in service with the GEnx, and more than 90% of recent orders. While Rolls-Royce’s Trent 1000 was initially competitive on the program, reliability and durability issues that emerged around 2016 shifted operator preference toward the GEnx.

Cutaway image of the GE9X – the world’s largest and most powerful commercial turbofan, delivering over 134,000 lbs of thrust for the Boeing 777X, the world’s largest twin-engine jet. Image courtesy: GE Aerospace

CFM56: Stronger for Longer as Utilization and MRO Support Sustain the Fleet

The legacy CFM56 program continues to generate meaningful revenue for GE Aerospace, supported by high utilization, sustained airline demand, and a slower-than-expected pace of retirements. The engine family has been in service since 1982, with more than 30,000 engines delivered to over 550 operators worldwide, making it the most widely owned and operated commercial aircraft engine in service.

Culp said retirements of the CFM56 fleet remained muted in 2025, at about 1.5% of the installed base, broadly consistent with 2024 levels. Looking ahead, he said retirements in 2026 are expected to remain relatively modest, likely around 2%, below the 2%–3% range previously anticipated. As a result, GE now expects shop visit demand to remain strong, with approximately 2,300 to 2,400 CFM56 shop visits annually through 2028, before a gradual decline later in the decade. Culp said utilization trends and airline demand point to the program being “stronger for longer.” The propulsion maker credits independent MRO providers with giving operators greater flexibility in servicing their aircraft, supporting higher asset values, and lowering the cost of ownership. GE continues to expand access to OEM materials to support CFM56 longevity, including a materials agreement reached last quarter with FTI Aviation to support service of its growing CFM56 fleet.

Reorganization Aims to Tighten Integration and Lift MRO Output

GE Aerospace announced an organizational restructuring intended to accelerate execution in 2026 by further integrating engineering, supply chain, and customer-facing functions within Commercial Engines & Services. Under the changes, CES has been expanded to include T&O, which will be led by Mohamed Ali. The revised structure brings product line, engineering, and supply chain teams under a more unified organization, a move the company said is designed to improve end-to-end engine lifecycle management and decision-making.

Customer-facing teams have also been elevated and will now report directly to the chief executive, led by Jason Tonich. The company said the change is intended to reinforce a customer-driven operating model and improve responsiveness as demand across services and equipment continues to grow. “These changes will enable greater cross-functional problem-solving, agility, and alignment to deliver for our customers,” Culp said. The reorganization builds on the FLIGHT DECK operating model and is expected to support higher delivery volumes in 2026, particularly across the MRO network. The company said it is removing waste across repair operations to improve shop visit output and reduce turnaround times.

GE Aerospace also said Russell Stokes, president of Services, will retire from the company in July after 29 years of service.

Aftermarket Momentum Builds as MRO, Shop Visits, and Spare Parts Drive Growth

Aftermarket performance was a central contributor to GE Aerospace’s results in 2025, supported by higher shop visit volumes, improved turnaround times, and strong spare-parts demand across both mature and newer engine programs. The company said a shift from batch to flow production improved execution across its MRO network, with turnaround times for LEAP, CFM56, and GE90 improving by more than 10% year over year in the fourth quarter. At the Wales facility, CFM56 turnaround time improved by 20%, while at Selma, the company sustained turnaround times below 80 days, enabling its highest LEAP shop visit output of the year.

Utilization of mature engines remained strong, with airlines continuing to keep aircraft in service to meet demand. Management said aftermarket growth in 2025 was driven less by the demand environment and more by execution, particularly the ability to move spare parts through the system to support both internal and third-party shop visits. “We’re not particularly concerned about the demand environment,” Culp said. “It’s really all about our ability to move spare parts out to third parties to complete our own internal shop visits. While we were pleased with the sequential and year-over-year numbers in the fourth quarter, there’s much more to do here in 2026.”

To support longer-term aftermarket demand, the company is expanding capacity across its global MRO network as the LEAP installed base grows. The LEAP fleet is expected to roughly triple between 2024 and 2030. In 2025, GE Aerospace added MTU Dallas as its sixth premier MRO partner, with third-party shops now accounting for about 15% of total LEAP shop visits. GE is dedicating roughly $500m of more than $1bn of planned MRO investment to LEAP, including capacity expansions in Malaysia, Selma, and Dallas, as well as a new on-wing support facility in Dubai. These investments are expected to roughly double internal LEAP capacity over time.

Taken together, the company said these actions drove meaningful progress in services output in 2025. CES services revenue increased 26%, with internal shop visit revenue up 24%, including a 27% increase in LEAP internal shop visit volume. Spare-parts revenue grew more than 25%, supported by higher volumes, expanded work scopes, and improved material availability. Looking ahead, Chief Financial Officer Rahul Ghai said both shop visits and spare-parts revenue are expected to grow at a mid-teens rate in 2026, broadly in line with overall services growth. Spare-parts demand is expected to be driven primarily by narrowbody engines, reflecting continued growth in LEAP external channels and ongoing strength in the CFM56 fleet. Third-party shops now perform more than 15% of LEAP shop visits, while CFM56 shop visit demand is expected to remain in the 2,300–2,400 range as retirements stay muted.

“Our customers want more, and they want it faster, without any compromise with respect to safety or quality,” Culp said. “It’s a fair ask, and one this team is committed to delivering on in the new year.”

Technicians conduct work on a legacy GE CF6. Even ancient programs continue contributing to the company’s bottom line. Image courtesy: GE Aerospace

Next Generation and R&D

GE Aerospace recently completed a ground test campaign demonstrating its first hybrid-electric narrowbody engine architecture, a milestone the company said validates system-level integration and advances the technology from concept toward a scalable application. “Nearly $3bn in annual R&D expenses,” Culp said, underscoring the scale of the company’s investment. R&D spending remains focused first on improving customer experience through enhancements to engines in service or entering service, including continued durability improvements to LEAP aimed at improving time on wing and reducing total cost of ownership. Investment is also supporting newer programs as they move toward entry into service and ramp-up phases, including the GE9X under the 777X.

At the same time, the company continues to invest in longer-term propulsion technologies. “We’re very hard to protect and expand the size of the R&D envelope because we know this business is led through product cycles,” Culp disclosed. He pointed to work on future propulsion concepts, including the RISE program, as central to positioning the company for the next technology transition in the 2030s.

GE’s next-generation RISE Open Fan Architecture engine is pegged for service entry in the 2030s. Image courtesy: GE Aerospace

Supply Chain Improvements

GE Aerospace said supply chain performance improved through 2025, with greater visibility into the supplier base and further out in time, supporting both aftermarket demand and new-engine production. “No one can really isolate the new-make demand and invest for that without being mindful of the aftermarket demand as well,” Culp professed. He said the company now has better insight into supplier readiness to support airlines and airframers across both service and delivery requirements.

The engine-maker said supplier performance improved sharply in 2025, citing roughly a 40% year-over-year improvement from priority suppliers, a pace he said is unlikely to be repeated annually but reflects the impact of process improvements and capital investment across the supply base. “There’s work to do,” he said, but added that the progress made last year positions the company to step up again as demand continues through the decade.

2025 Financials Beat on CES While DPT Trails Expectations

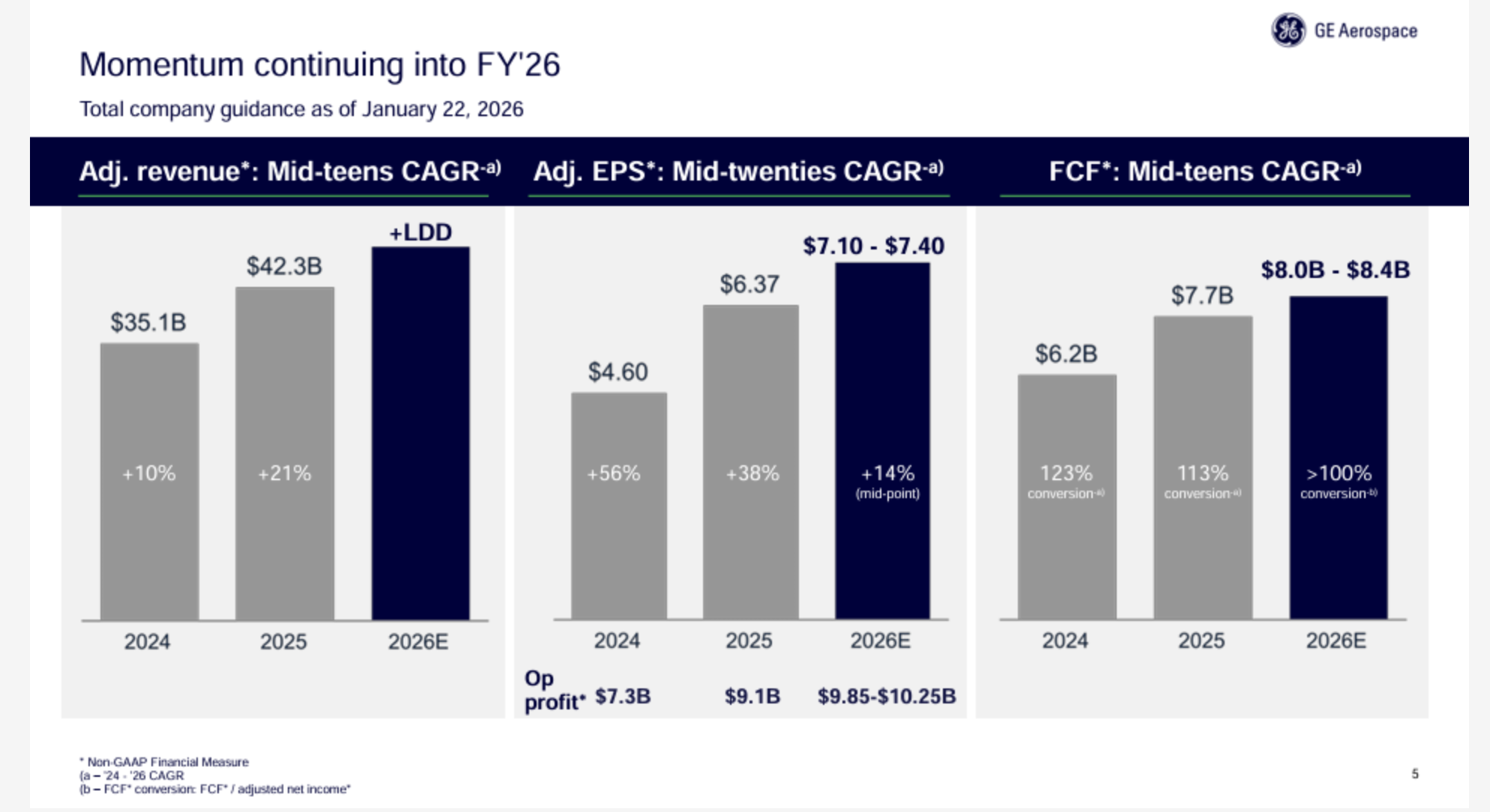

Overall, GE Aerospace delivered strong results in the fourth quarter of 2025, with total orders reaching $27.0bn, a 74% increase year-over-year. The company reported total revenue (GAAP) of $12.7bn, up 18% from the prior year. Profit (GAAP) increased 24% to $2.9bn, while the profit margin (GAAP) expanded to 22.4%, reflecting a favorable mix and strong services performance. For the full year 2025, total orders increased 32% to $66.2bn. Total revenue (GAAP) rose 18% to $45.9bn, with profit (GAAP) growing 31% to $10.0bn and profit margin expanding to 21.8%, supported by operating leverage, productivity gains, and a higher contribution from services.

In the quarter, the Commercial Engines and Services (CES) unit reported orders of $22.8bn, up 76% year-over-year, driven by strength in both services and equipment. Revenue increased 24% to $9.5bn, with services revenue up 31%, supported by higher internal shop visit volumes, expanded workscopes, strong spare-parts demand, and pricing. Equipment revenue grew 7%, reflecting higher engine deliveries, including increased LEAP volumes, though growth lagged services due to mix and spare-engine dynamics. Operating profit rose to $2.3bn, with an operating margin of 24.0%.

Analyst Matthew Akers of BNP Paribas credited CES with driving the majority of the earnings beat, with operating profit and margins materially exceeding expectations, largely due to stronger-than-anticipated services growth, while lower-margin equipment trailed estimates. For the full year, CES orders rose 35%, revenue increased 24%, and operating profit grew 26% to $8.9bn, supported by strong aftermarket demand, higher shop visit volumes, and record LEAP deliveries. Akers noted that Defense & Propulsion Technologies underperformed expectations, with quarterly operating profit of $252m and an 8.9% margin, reflecting mix and investment pressures.

2026 Guidance: Services Growth Offsets Some Headwinds

Looking ahead, the world’s largest aircraft engine maker is guiding for continued low double-digit growth in 2026, building on adjusted revenue of $42.3bn in 2025. Operating profit is expected to increase to a range of $9.85bn to $10.25bn, supported primarily by services growth and higher engine and shop-visit output. Ghai said the company expects a strong start to the year, with first-quarter revenue growth in the high teens, driven by higher equipment output and shop-visit activity compared with early 2025. Both Commercial Engines & Services (CES) and Defense & Propulsion Technologies (DPT) are expected to perform above their respective full-year guides in the first quarter.

Within CES, the CFO highlighted services as the primary driver of year-over-year profit growth, supported by a strong backlog and the absence of a charge taken in the first quarter of 2025. The company also expects GE9X shipments in the first quarter, which were not present a year ago. Higher deliveries and GE9X shipments are expected to weigh on mix, but this impact is expected to be offset by services growth and the absence of the prior-year charge. As a result, Ghai said overall margins in the first quarter are expected to be in line with, or slightly above, fourth-quarter 2025 levels, despite a lower spare-engine ratio and the inclusion of GE9X shipments.

Image courtesy: GE Aerospace

Looks pretty good from GE, though I wonder how much of that increase in services is due to warranty work.

@Vincent

Considering the profit growth in GE Services, the warranty impact is negligible compared to what both P&W and RR are experiencing with their warranty workload.

These companies, including the airframe OEM’s make significant profits from services which includes spare parts and MRO systems.

Its not in the story – GE is good at whitewashing its durability problems.

This is the background to GEnx ‘improvements’, ie fixes mentioned

HPT Stage 1 Blade Failures: Multiple in-flight shutdowns (IFSDs) were caused by HPT stage 1 blade failures, prompting Federal Aviation Administration (FAA) directives for inspection and removal.

Aft Blade Retainer Failure: The May 2024 uncontained engine failure on a United Airlines B787 was attributed to the failure of the HPT stage 1 aft blade retainer. A fatigue crack originated from a surface-connected cluster of Oxide/Carbonitride/Nitride/Carbide (OCNC) particles, a unique material issue in high-stress scenarios.

Environmental Degradation: Earlier issues included fan blades rubbing on the casing due to ice ingestion, causing premature wear and requiring FAA airworthiness directives to modify the casing’s abradable material.

Fan Mid-Shaft Concerns: In 2012, inspections were ordered for the fan mid-shaft following failure,, which differed from later HPT blade issues, according to CNBC and Aerossurance.

So yes GE has warranty workload too but GE and the aviation media always sing from the same song sheet

I don’t disagree. Bit of a puff piece above..

I have always wondered why GE is reporting all of CFM”s production as their own?

I was thinking the same but It seems that SAFRAN is also reporting all CFM figures in their reporting