Leeham News and Analysis

There's more to real news than a news release.

RTX Q2 2025 Earnings: Tariff Relief, GTF Stabilization, Strong Demand, and FAA Tailwinds Lift Outlook

By Chris Sloan

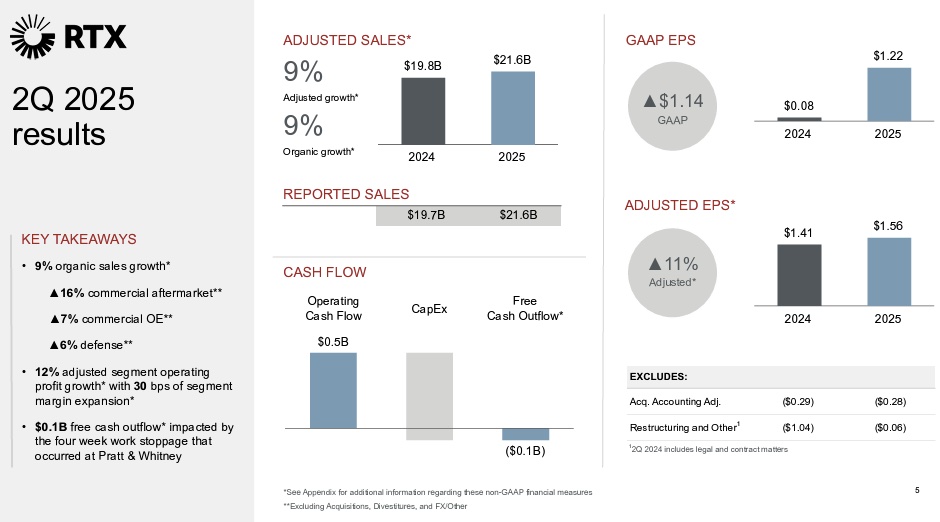

![]() July 22, 2025, © Leeham News: RTX delivered strong second-quarter results, supported by continued momentum in the commercial aerospace sector, stabilization in its geared turbofan program, and a significant aftermarket ramp across Pratt & Whitney and Collins Aerospace.

July 22, 2025, © Leeham News: RTX delivered strong second-quarter results, supported by continued momentum in the commercial aerospace sector, stabilization in its geared turbofan program, and a significant aftermarket ramp across Pratt & Whitney and Collins Aerospace.

Executives highlighted improving supply chain conditions and growing demand as key contributors, while also noting upcoming FAA modernization investments as a long-term opportunity. Despite ongoing trade friction and a sizeable tariff burden, RTX raised its full-year sales outlook and reaffirmed its free cash flow guidance. Executives said recent developments on the tariff front—including favorable exemptions and successful mitigation strategies—helped soften the impact and improve visibility heading into the second half.

“Our outlook on the impact of tariffs has improved for the year,” said RTX President and Chief Executive Christopher Calio. The company originally expected a $850m tariff headwind in 2025 but has since lowered that figure to $500m. Calio attributed half of the reduction to external developments such as the paused implementation of new rates and the UK’s decision to exempt aerospace components. The remainder, he said, came from the company’s mitigation actions, including optimizing material flows through its supply chain, taking pricing actions where possible, and leveraging trade agreements such as USMCA.

RTX has already incurred approximately $125m in tariff costs through the first half of the year, with the remaining $375m expected in the second half. Of that, $275m is expected to impact Collins Aerospace, and $225m will affect Pratt & Whitney. CFO Neil Mitchill Jr. said roughly $60m and $40m in costs have already been recorded at Collins and Pratt, respectively, during Q2. The total cash impact is expected to reach $600m for the year.

Tariff risks remain

Mitchill emphasized that the current $500m estimate represents the company’s best view of full-year tariff costs net of mitigations. “We’ve incorporated these impacts into our updated full-year outlook,” he said. Notably, that figure assumes no further rate increases. However, with U.S. trade policy potentially shifting as early as August 1, RTX acknowledged that some risk remains. “We haven’t contemplated something going up on August 1 or anything that might transpire after that,” Mitchill admitted. Should new rates take effect, only a portion would hit the income statement this year, with the remainder captured in inventory balances. Mitchill said the company has built flexibility into its guidance ranges to absorb such volatility. “That’s why we’ve got a range around those two particular metrics,“ he added, referring to EPS and free cash flow.

Additional upside is expected from improved operating performance at Raytheon and more substantial volume drop-through at both Pratt & Whitney and Collins, contributing approximately 10 cents of EPS benefit. That helps offset the 30-cent drag from tariffs. On the tax front, Mitchill welcomed the restoration of full R&D expensing under new U.S. legislation, which is expected to offset about 25%–30% of the tariff-related cash impact this year. RTX continues to project a full-year effective tax rate of 19.5%. “Our intent here is to continue to aggressively mitigate these headwinds so that we don’t see a larger year-over-year headwind coming into 2026,“ Mitchill said.

Commercial demand stays strong despite trade volatility

RTX reported continued strength across its commercial aerospace business, with both Collins Aerospace and Pratt & Whitney posting solid growth in original equipment (OE) and aftermarket sales, despite uncertainty surrounding tariffs and geopolitical trade pressures.

“At a macro level, we’re not seeing any bleed-through into demand,” said the CEO. “You just look at the commercial aftermarket here in the first half—again, really strong, 18% organic growth,” Calio said global revenue passenger kilometers (RPKs) are expected to rise more than 5% this year, supporting low retirement rates and sustained shop visit activity across key engine platforms. The V2500 fleet, for example, has seen just a 1% retirement rate so far in 2025.

Pratt booked more than 1,000 geared turbofan (GTF) engine orders during the quarter, including orders supporting up to 177 aircraft at Wizz Air and 91 aircraft at Frontier Airlines. Calio said OE production remained in line with expectations through the first half and that RTX remains confident in the second-half ramp. “Countries want to get deals done,” he said. “Even with some of the more difficult negotiations… people want stability, they want predictability.”

Vice President of Investor Relations Nathan Ware noted commercial OE sales rose 1% year-over-year, with lower 737 MAX deliveries offset by increased volume on platforms like the 787. Aftermarket sales increased 13% overall, driven by a 20% rise in modifications and upgrades, a 12% growth in parts and repairs, and a 9% rise in provisioning.

Calio also pointed to rising consumer sentiment and stable employment levels as supportive of continued airline capacity growth. “The airline commentary has been around a more stable environment, which provides a good platform for continued strength in the aftermarket,” he said.

On the cash side, the CFO said second-half growth will be driven by segment profit and working capital improvements, including recovery from the Q2 work stoppage at Pratt.

Stabilizing GTF program gathers strength with Advantage upgrade, MRO ramp

Pratt & Whitney’s GTF program is showing clear signs of momentum as operational stability improves and the company pushes ahead with a significant maintenance ramp and the rollout of its next-generation Advantage configuration. Executives stated that the program’s outlook is strengthening, with rising shop throughput, easing AOG levels, and a significant retrofit offering on the horizon.

“AOGs have stabilized and we’re expecting them to come down meaningfully here in the second half,” said Calio. The key driver, he said, will be continued expansion in MRO output, which is targeted to grow more than 30% for the full year. “That’s going to be the instrumental piece of this,” he added. “That’s what’s going to move this down meaningfully.”

Despite a four-week work stoppage at Pratt, MRO output for the PW1100 rose 22% year-over-year in the second quarter, supported by higher material velocity and improved turn times across key facilities. “Think MTU. Think Pratt. Think Delta,” said the CEO. “Those are the shops that continue to drive output.” The company reaffirmed its plan for over 800 shop visits on the V2500 this year and continues to see ongoing strength in the program. “That platform continues to perform exceptionally well,” Calio said, noting demand has remained stronger than expected. “Even if shop visits eventually decline, we think content will continue to rise.”

At the center of the GTF recovery strategy is the phased introduction of the GTF Advantage engine. Production has already begun, with initial deliveries scheduled by the end of 2025. Calio said the cutover from the current configuration will span several years to preserve supply chain maturity and reduce risk. In parallel, RTX will begin offering its “Hot Section Plus” kit—a retrofit package comprising approximately 35 parts from the Advantage engine—to MRO starting next year.

“These comprise the overwhelming majority—almost 90%—of the durability improvements from the GTF Advantage,” Calio remarked. While pricing will be determined on a customer-by-customer basis, he emphasized the expected fleet benefit. “It’s going to have a significant time-on-wing benefit,” he said, estimating the kit will deliver 90–95% of the full Advantage time-on-wing gain. “We do expect it to be a significant shot in the arm for the program and the fleet.”

Calio reiterated that the GTF program remains profitable over the life of its contracts. Margins are positive. When you average the last couple of years, they’re in the double digits,” he said. “We continue to be measured in our approach… we don’t want to get ahead of ourselves.” Future margin uplift tied to the Advantage and Hot Section Plus packages will materialize later in the contract cycle.

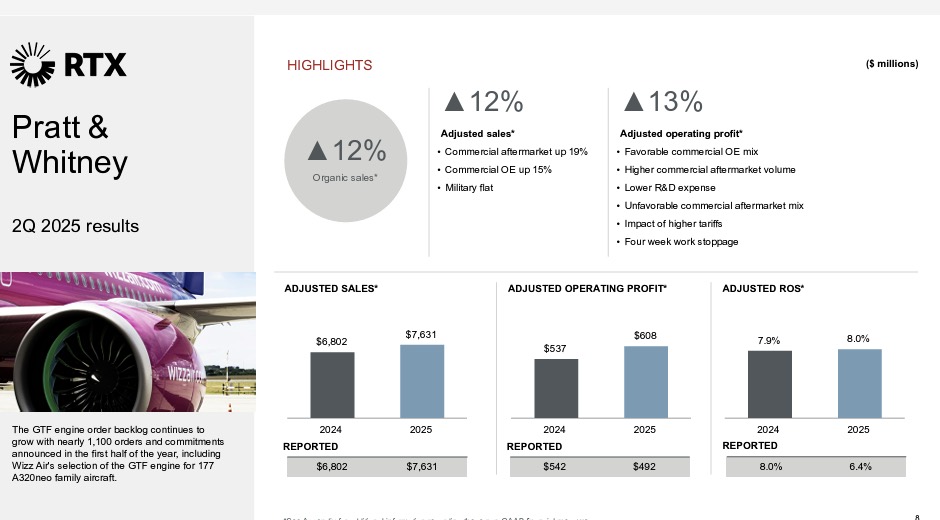

The CFO pointed out Pratt sales are now pacing up low double digits for the year, contributing roughly $800m of RTX’s projected $1.6bn topline increase at the midpoint. About half of that growth is from aftermarket, which is now expected to rise in the mid-teens for 2025. “We’ve been working to balance our deliveries between installs, spares, and MRO,” he said, and sees continued momentum in the back half of the year.

Pratt manages production ramp and shifting mix amid near-term headwinds

Pratt & Whitney continues to balance its narrowbody engine production ramp with aftermarket support as it recovers from a second-quarter work stoppage and adjusts to the impact of a customer bankruptcy. Executives said they remain confident in meeting full-year delivery and profitability targets, supported by robust aftermarket strength and an improving long-term margin profile.

On the A320neo program, RTX is continuing its planned production increases, though the four-week strike at Pratt during the quarter temporarily disrupted output. “We’re going to make that up in the balance of the year,” CEO Calio pledged. He emphasized the need to carefully allocate structural castings and isothermal forgings between MRO and new engine production. “We work closely with Airbus… because we’ve got to make sure that we balance the continued ramp there with what we need on the MRO side,” he said, reiterating the company’s priority to support the in-service fleet and reduce AOGs in the second half.

The CFO revealed the strike represented a roughly $1bn impact to RTX’s second-quarter results, most of which is expected to recover in Q3. “We’ll see a recovery from the Pratt strike… that’s about a billion dollars,” he said.

Separately, Mitchill acknowledged that Spirit Airlines had filed for bankruptcy during the quarter, creating some uncertainty for Pratt. “We are continuing to work with that customer as you’d expect,” he said. “Over time, I believe they will continue to utilize our assets, and in the long term, we will likely realize some recovery there.”

Despite these near-term events, Pratt posted strong top-line results. Second-quarter sales were up 12% year-over-year on both an adjusted and organic basis, driven by growth in both commercial OE and aftermarket. Aftermarket revenue rose 15%, aided by favorable mix in large commercial engines and increased volume at Pratt Canada.

Outlook

Looking ahead, RTX expects Pratt sales to grow in the low double digits for the full year. Mitchill forecasts OE volume will continue to climb, creating some temporary margin drag as new engines are placed on wings. However, the aftermarket is expected to grow faster and more profitably than Pratt’s current composite margin, creating margin tailwinds over the next several years. “Certainly, the ingredients are there,” he said, noting strength in the V2500 shop visit outlook. “Those are much heavier [work scopes] on the V, so I see sustained revenue and profit from those visits.”

Over the longer term, RTX expects sequential margin expansion at Pratt through 2025, 2026, and 2027. “Pratt is a low-to-mid-teens business,” Mitchill said. “We’ve seen those kinds of margins in the past.” He cited several contributing factors: the GTF Advantage development cycle is largely complete, V2500 shop visit content is increasing, and both Pratt Canada and the military engine business are profitable and growing. “Those will continue to grow in volume, contributing to improved margins in the Pratt business,” he said.

As the GTF Advantage fleet expands later this decade, it is expected to overtake the V2500 in aftermarket scale and profitability eventually. “We’re really confident about the GTF Advantage,” Mitchill declared.

Collins sees ramp in second half, pushes forward with internal restructuring

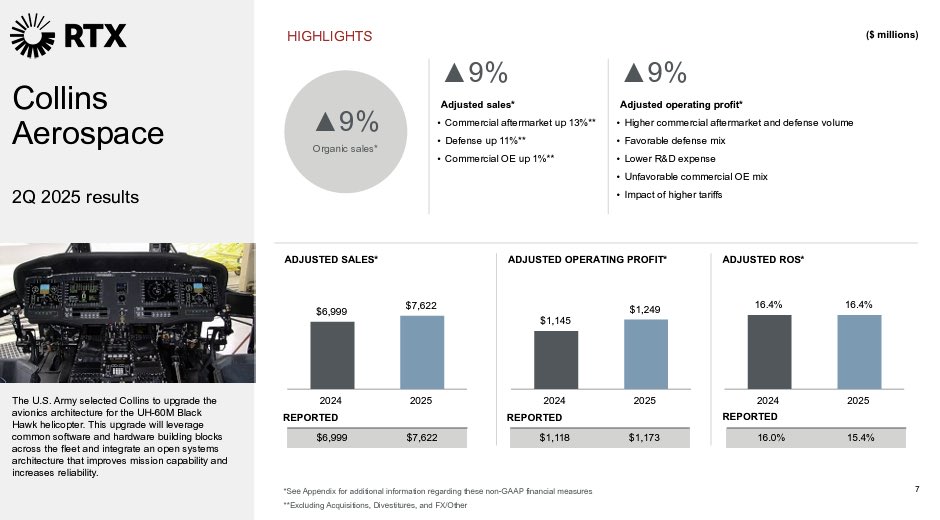

Collins Aerospace is positioned for stronger growth in the second half of the year as Boeing production stabilizes and demand for both OE and aftermarket services improves. RTX executives reiterated their confidence in the long-term outlook for the segment, while noting that continued transformation efforts are underway within the Collins business.

Sales at Collins are now expected to grow in the mid-single digits on an adjusted basis and in the high single digits organically, said Ware. Original equipment growth was modest in Q2, up 1% year-over-year, as expected. “We expected the first half of the year to be a little bit lighter,” opined Mitchill, citing a difficult year-over-year comparison driven by the Boeing strike in 2024. “The compares get a lot easier as we get into the second half of the year.”

Mitchill revealed RTX expects about $800m in full-year sales uplift at Collins, with $200m tied to OE volume and $250m from aftermarket growth. RTX is particularly encouraged by the ramp at Boeing, especially on the 787. “We’re expecting a mixed headwind as the 787 ramps up in the second half.”

Calio said Collins is focused on maintaining stable delivery performance to support Boeing’s output goals. “We are seeing stability in the rates at Boeing,” he said. “For Collins, it’s just making sure that we stay out of their way and continue to deliver at the rates that they need.” He added that RTX has capacity for a much higher production rate at Collins and is focused on ensuring constrained material is in place to meet second-half requirements.

Alongside its commercial recovery, Collins is undergoing a more profound internal transformation aimed at streamlining operations and improving long-term efficiency. The company recorded a sizable restructuring charge in Q1 and is continuing with a broader organizational realignment. “We’re rightsizing the business—sizing the back office, reducing our footprint, increasing our automation,” Mitchill emphasized. “Those are all projects that Collins is aggressively undertaking right now.” He said additional actions are likely.

Supply chain shows signs of relief as RTX maintains pressure on throughput

RTX continues to see steady gains across its supply base, with structural improvements in castings and backlog reductions at key divisions. Executives emphasized that while challenges remain, the first half of 2025 marked measurable progress.

“Supply chain overall, I would say, continues to see improvements,” Calio noted. He pointed to more than 20% growth in structural casting output at Pratt and a 25% reduction in overdue line items at Collins as tangible examples of stabilization.

Calio credited RTX’s internal operating system and hands-on collaboration with suppliers for driving better visibility and throughput. “Sitting side by side with our suppliers, making sure they understand our demand… if there are producibility or specification changes we can make, we’re doing it,” he explained. “That core has been instrumental in helping us get to this level of stability.”

While acknowledging that the effort remains ongoing, Calio conveyed confidence in the direction of progress. “We’re not taking our foot—by any measure—off the pedal,” he remarked. “But we feel good about the progress so far in the first half of the year.”

FAA modernisation creates runway opportunity for Collins

Collins Aerospace stands to benefit significantly from the recent One Big Beautiful Bill Act, part of the U.S. budget reconciliation package signed on July 4, which allocated $12.5bn for FAA modernization. RTX executives stated that the funding is a major catalyst for upgrades across radar systems, control towers, automation, and aircraft equipment.

“FAA modernization is critical… we play in some very specific areas,” Calio observed, referring to Collins’s strong market share in radar systems installed at FAA facilities. He also highlighted automation upgrades in towers and runway ground control equipment, where Collins holds a significant presence.

He added that the $12.5bn “is a pretty good down payment on what’s needed to overhaul the air traffic system.” Calio noted the segment’s involvement in upgrading automation in FAA towers, enhancing runway control packages, and working closely with the agency on system modernization.

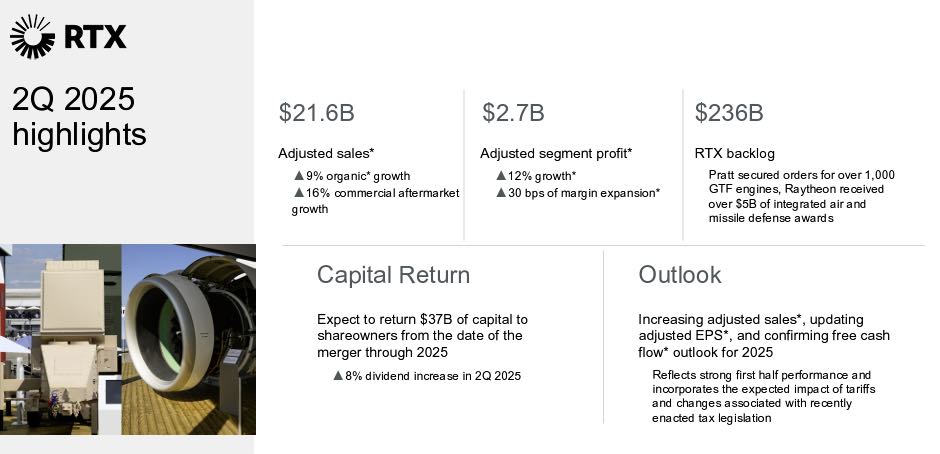

RTX raises full-year revenue target after strong Q2 showing

RTX posted second quarter sales of $21.6bn, a 9% increase over the same period a year ago. Net income attributable to common shareholders rose to $1.7bn, up from $111mn in Q2 2024. Pratt & Whitney generated $7.63bn in revenue during the quarter, representing a 12% year-over-year gain. Adjusted operating profit for the segment increased 13% to $ 608 million. Collins Aerospace reported $7.62bn in sales, up 9% from the prior year. Adjusted operating profit improved 9% to $1.25bn.

RTX raised its full-year 2025 sales outlook to a range of $84.75bn to $85.5bn, up from the prior estimate of $83bn to $84bn. The company now expects organic sales growth of 6%–7%, compared to the previously forecasted range of 4–6%. Adjusted earnings per share were revised downward to $5.80–$5.95 from the earlier $6.00–$6.15 range, reflecting the anticipated impact of tariffs and recent tax law changes. Free cash flow guidance was reaffirmed at $7.0bn to $7.5bn.

Analysts broadly viewed the updated guidance as a balanced reflection of strong operational momentum and external headwinds. Karl Oehlschlaeger of Vertical Research Partners noted the tariff impact was less severe than feared and called it a “positive” that RTX maintained its free cash flow guidance while nudging up its top-line outlook. “Underlying core operations are progressing well, and we think this is what investors are likely to be focused on,” he said.

Ken Herbert of RBC Capital Markets pointed to the recent work stoppage at Pratt & Whitney as the primary factor behind the $72m free cash outflow in the quarter. He added that strong engine results at Pratt echoed trends seen at GE and suggested continued strength for the broader engine market. “For a sixth straight quarter, Pratt & Whitney led the revenue growth,” Herbert said, citing 12% organic growth at Pratt, 9% at Collins, and 6% at Raytheon. He also flagged the potential for upside in Collins’ OE business in the second half as Boeing build rates stabilize above supplier expectations.

It would be good to see some mention of the sale of part of RTX controls to Safran. I think Safran divested some stuff.

Have to go dig some, I don’t understand either move?

I continue to wonder how P&W can use the Advantage (or would) While RR has the Advance label, too close and easily confused. Poor word selection to me.

@TW

I believe that was one of the conditions of the Raytheon / UTC merger from regulatory review for anticompetitive concerns.

Safran has bought the Flight controls and actuators business. [4,000 people across eight main facilities in Europe (UK, Italy and France) and Asia, and has activities in Poland, USA and India.]

The merger between Raytheon and UTC specifies the divestiture of Raytheon’s military airborne radios business as well as the optical systems and military global positioning systems (GPS) from United Technologies.

BAE bought the military GPS .

Elevators and A/C was also sold for unrelated reasons

The Collins segment was sold outside of the merger requirements

Makes my head spin.

It may have the European regulators condition to divest the Flight Controls and actuators

Originally the business was BF Goodrich, bought by UTC in 2011, which merged with its existing Hamilton Sundstrand division.

Goodrich had bought some of these business segments from TRW in 2002, and they had taken over the original european business Lucas aerospace- centered mostly in France and UK

Good history lesson.

Lucas was known over here as the Prince of Darkness!