Leeham News and Analysis

There's more to real news than a news release.

RTX Posts Steady Q3 2-25 As GTF Stabilization, Collins Strength, And Tariff Headwinds Define Results

By Chris Sloan

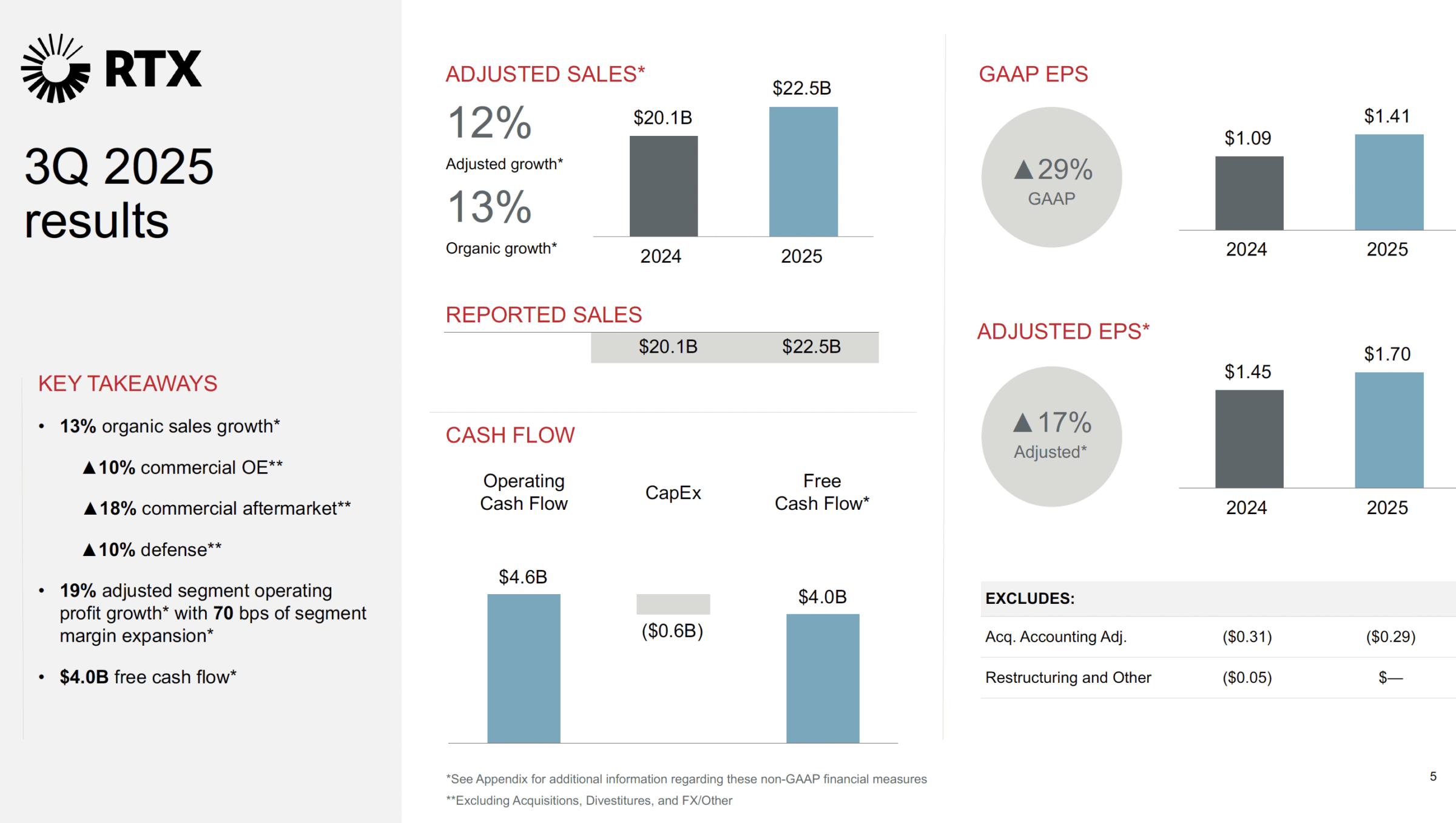

![]() October 21, 2025, © Leeham News: RTX delivered a solid and steady third quarter, marked by broad-based growth, improving GTF maintenance output, and continued strength at Collins Aerospace—even as tariff headwinds persisted. Company sales rose 12% year-over-year to $22.5bn, or 13% organically, while adjusted segment operating profit increased 19%, marking the sixth consecutive quarter of year-over-year margin expansion. Net income attributable to common shareholders climbed to $1.9bn, up from $1.4bn a year ago.

October 21, 2025, © Leeham News: RTX delivered a solid and steady third quarter, marked by broad-based growth, improving GTF maintenance output, and continued strength at Collins Aerospace—even as tariff headwinds persisted. Company sales rose 12% year-over-year to $22.5bn, or 13% organically, while adjusted segment operating profit increased 19%, marking the sixth consecutive quarter of year-over-year margin expansion. Net income attributable to common shareholders climbed to $1.9bn, up from $1.4bn a year ago.

Chairman and CEO Christopher Calio credited strong execution across all three segments for the performance, citing double-digit growth in commercial OE, aftermarket, and defense. RTX booked $37bn in new awards during the quarter—$23bn in defense and $14bn in commercial—lifting total backlog to $251bn, up 18% since the end of 2024.

With passenger traffic holding firm and OEM production trending higher, Collins and Pratt both benefited from robust aerospace demand. Calio said the company is raising its full-year outlook for adjusted sales and operating profit, supported by the ongoing production ramp and a stabilizing supply chain.

The conversation around the GTF program has shifted: improved MRO throughput and material flow replaced the usual focus on compensation and grounded aircraft, and for the first time in recent memory, the familiar “powdered-metal” refrain was absent from the call—an indication that Pratt’s recovery is turning a corner.

Tariffs still on the radar

Tariff headwinds continued to weigh on RTX’s margins in the third quarter, though executives said mitigation efforts are making gradual progress. Chief Financial Officer Neil G. Mitchill Jr. said both Collins Aerospace and Pratt & Whitney faced about $90 million each in year-over-year tariff impact. “If you put that aside, the team’s doing a great job making that a smaller number as we move forward,” he said. “A number of mitigations have been identified—that’s really the key driver of what’s been dragging down margins.”

Mitchill added that RTX is continuing work to support product qualification for USMCA treatment, improve re-export procedures, and manage costs through pricing adjustments. “You’ll see that again in the fourth quarter for both Collins and Pratt,” he said, noting that the headwinds are expected to persist but at a manageable level.

The Chief Executive said both businesses have been “appropriately aggressive” in pricing given the market environment. “We’ll continue to be aggressive on catalogue pricing because of the value we bring and the demand that’s out there,” he said.

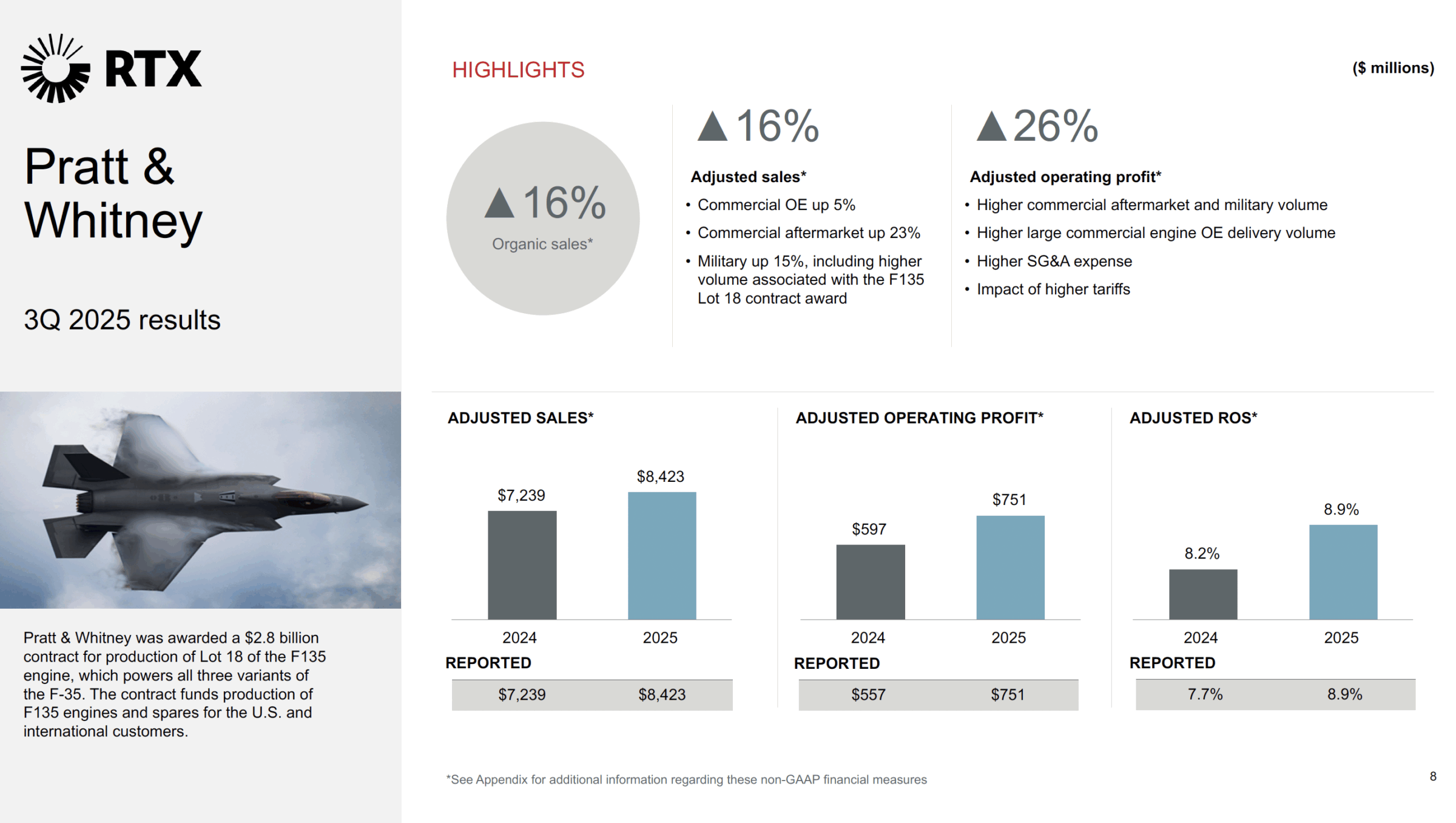

Pratt & Whitney: throughput improves as execution steadies

Pratt & Whitney continued to build operating momentum in the third quarter as production and MRO throughput improved across key programs. Calio said the business “executed well through the production ramps,” maintaining close coordination with Airbus and other OEMs to meet delivery schedules while balancing material allocation to the in-service fleet.

Production levels are now more than 50% higher than in 2019, supported by steady increases in large commercial engine output and stabilizing supply-chain flow. Calio said the company will “continue to work very closely with Airbus to make sure they have what they need down the stretch of the year,” while keeping the focus on fleet support and throughput.

Chief Financial Officer Neil G. Mitchill Jr. said the outlook for Pratt’s negative engine margin remains unchanged—still within the $150–$200m year-over-year headwind, expected to end near the midpoint of that range. New GTF deliveries are projected to grow 8–10% this year, consistent with earlier expectations.

Segment sales rose 16% to $8.4bn on both an adjusted and organic basis, with adjusted operating profit up $154m to $751m. Growth was driven by stronger commercial OE volume and productivity improvements, which offset higher SG&A costs and ongoing tariff impacts.

On customer compensation payments related to the GTF fleet, Mitchill said the financial outlook “remains consistent” with prior guidance. “We’re right on track with where we expect to be this year—between $1.1bn and $1.3bn, with a slightly heavier fourth quarter and the residual carrying into next year,” he said.

As of mid-2025, 700 to 800 GTF-powered aircraft remained on the ground, mostly A320neo-family jets, along with several dozen A220s and Embraer E-Jets. The issue drew little focus on the call, with management instead emphasizing tangible improvement in material flow and shop throughput—signaling that Pratt’s recovery is shifting from crisis management to sustained execution.

GTF MRO and Services: throughput gains mark a turning point

Pratt & Whitney’s GTF maintenance and repair operations continued to improve in the third quarter, marking a key milestone in the engine family’s stabilization. Calio said the company’s financial and technical outlook “remains on track,” with PW1100 MRO output up 9% in the quarter and 21% year-to-date.

“We saw another quarter of solid progress,” he said. “Isothermal forgings were up 16% and structural castings up 29% year-over-year.” Those material flow improvements supported a record number of Gate 3 starts—the reassembly and test phase of an engine overhaul—putting Pratt on pace to deliver about 30% MRO output growth for the year.

Calio added that repair network performance has also strengthened. “Our repair network was up about 30% year-over-year, which helps lessen demand for new parts and improves flow earlier in the process,” he said. “We exited the quarter with roughly 80% of GTF MRO completions averaging a 110-day turnaround time, even on heavier work scopes.” He called higher MRO throughput “the key to continuing to push down AOG levels,” and said the company is “in a good position to reach that 30% level for the full year.”

V2500: strong, steady aftermarket runway

Mitchill said demand for the V2500 continues to run stronger than expected. “We talked about 800 shop visits for the full year, and we’re right on track,” he said. “It’s been pretty linear through the first three quarters, and we expect a similar level in the fourth.” Those shop visits are trending heavier, he added, contributing directly to top-line and margin growth.

The fleet’s age profile continues to support a long aftermarket tail. “It’s still a relatively young fleet—average age about 15 years,” Mitchill said. “Fifteen percent haven’t had a first shop visit, and forty percent haven’t had a second. There’s significant aftermarket runway ahead, and demand is stronger than we thought a year or two ago.”

Aftermarket momentum drives Pratt performance

Commercial aftermarket sales rose 23% year-over-year, driven by heavier shop visits in large commercial engines and a strong contribution from Pratt Canada. Mitchill said much of RTX’s overall profit increase in the quarter came from Pratt’s aftermarket. “About $1.1bn of the $1.6bn increase in segment profit sits at Pratt & Whitney, and the majority of that is in the aftermarket,” he said.

He also emphasized that Pratt continues to maintain balance across production channels. “We’re not heavily discounting spares,” Mitchill said. “We’re balancing installs, spares, and material to the MRO network. There’s strong demand across all of it—whether engines are going to Airbus, directly to airlines, or into MRO.”

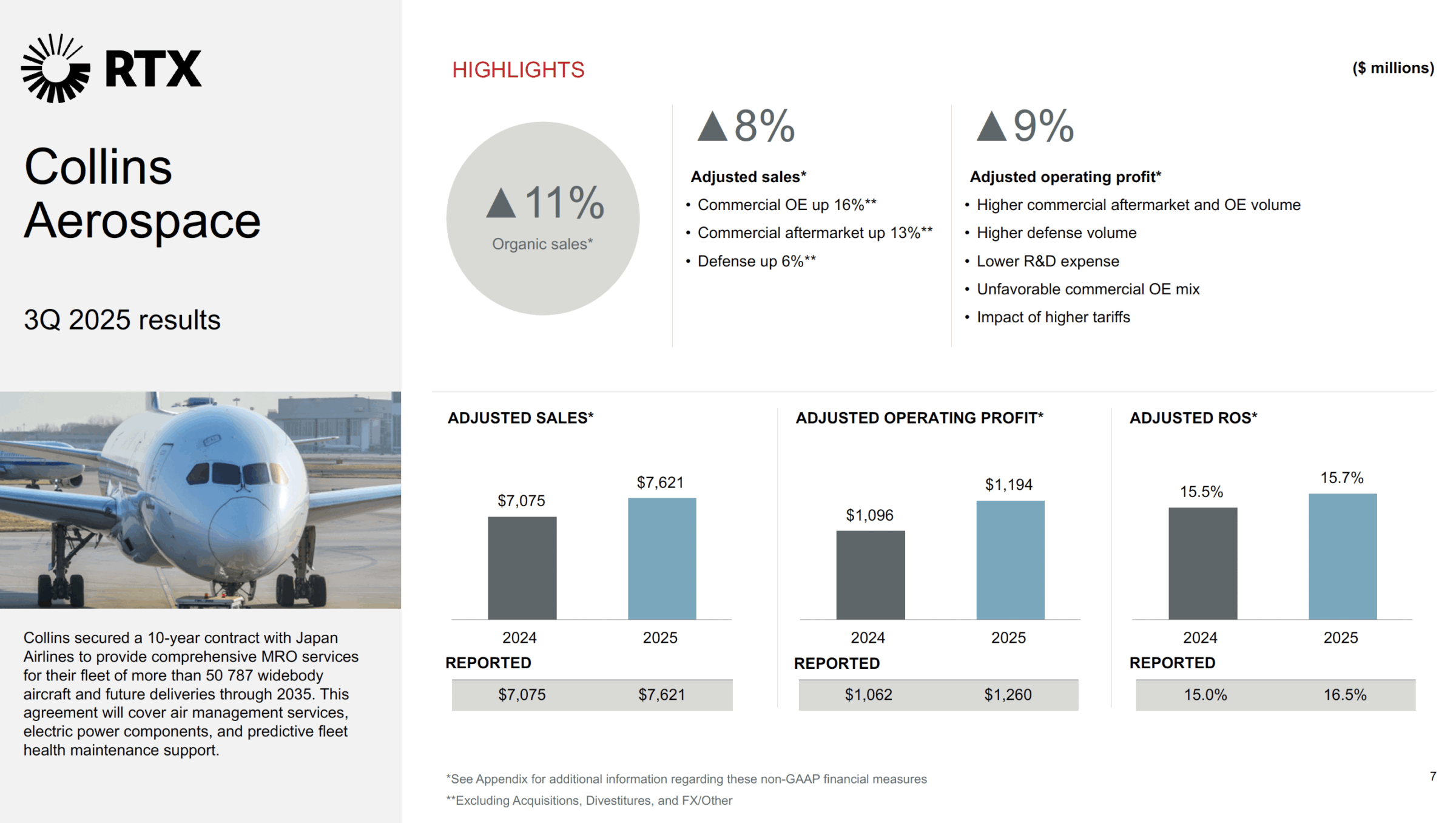

Collins Aerospace: leveraging deep installed base, ready for ramp-ups

Collins Aerospace entered the final stretch of the year with a strong operational footing and a deep base of recurring work. Calio said the business’s $100 bn in out-of-warranty installed equipment gives it “an incredibly strong position to work from,” sustaining long-term aftermarket growth.

He added that Collins is nearing final certification of its next-generation braking system for the Airbus A321XLR, which uses proprietary carbon technology designed to extend brake life and improve profitability within the company’s maintenance support portfolio.

Calio said Collins remains aligned with both major airframers as production rates increase. “We’re aligned with Boeing on the rates they’re at now and where they want to go,” he said. “Collins has delivered at higher rates in the past, and we’ve got the capacity to support the volume ramp.” He noted that Collins’ readiness depends on continued supply-chain improvement, which has been “showing steady progress.”

Mitchill added that Collins and Boeing are now operating in sync after working through earlier channel inventory. “We’re pretty synchronized with Boeing and their delivery schedule,” he said. “The higher 787 mix brings some near-term margin challenges, but as rates rise toward the levels we’ve capacitized for, we’ll see better absorption and continued margin expansion.”

Segment sales reached $7.6bn, up 8% on an adjusted basis and 11% organically, driven by strength across all three channels. Commercial OE sales were up 16% year-over-year, while commercial aftermarket grew 13%, led by a 17% increase in mods and upgrades and a 13% rise in parts and repair activity. Adjusted operating profit climbed to $1.2bn, up $98m from a year ago, with higher commercial and defense volume offsetting the impact of tariffs and OE mix.

Supply chain: steady performance, capacity expanding

RTX continued to emphasize strengthening its supply chain and expanding manufacturing capacity to meet rising demand across programs. Calio said the company is investing over $600m this year in expansion projects aimed at increasing output in critical manufacturing areas.

“We continue to focus on increasing critical manufacturing capacity to support growth,” he said. “It’s about making sure the supply chain stays healthy.” RTX recorded its 10th consecutive quarter of material receipts growth, which Calio described as a positive trend but one that must continue to accelerate. “Performance has stabilized and been good,” he said. “We need to see it keep improving through 2026 and beyond, because the demand is there.”

Next generation: hybrid-electric propulsion on the horizon

Looking ahead, RTX is channeling part of its investment toward next-generation propulsion technologies. Pratt & Whitney Canada was selected by the EU’s Clean Aviation Program to design and integrate a hybrid-electric propulsion demonstrator for regional aircraft. The system combines a 250-kilowatt electric motor with advanced propeller technology from Collins Aerospace, targeting a 20% improvement in fuel efficiency.

The collaboration underscores RTX’s longer-term focus on sustainable propulsion and its strategy to align Pratt and Collins innovation pipelines for future aircraft platforms.

Financial close: RTX raises outlook after another strong quarter

RTX capped the third quarter with another steady performance, underscoring balanced execution and firm demand across both commercial aerospace and defense. Adjusted segment margins expanded for the sixth consecutive quarter, reflecting continued operational discipline and productivity gains.

Cash generation was particularly strong, with free cash flow of $4.0bn and operating cash flow of $4.6bn, both well ahead of last year. Management said the improvement was driven by aftermarket strength, higher volumes at Pratt and Collins, and ongoing cost control.

On the back of this performance, RTX raised its full-year 2025 sales outlook to $85.5–86.25bn and reaffirmed free cash flow guidance of $7.0–7.5bn, pointing to sustained demand and improving shop throughput at Pratt & Whitney.

Analysts characterized the results as solid and confidence-building. Robert Stallard of Vertical Research Partners said RTX “delivered another broad-based beat, with all three divisions contributing,” while Ken Herbert of RBC Capital Markets called the absence of new GTF cost disclosures “a net positive,” reflecting growing program stability. Seth Seifman of J.P. Morgan noted “strong operational results across each segment,” citing improving aftermarket profitability and tight cost control.

“..As of mid-2025, 700 to 800 GTF-powered aircraft remained on the ground, mostly A320neo-family jets, along with several dozen A220s and Embraer E-Jets. The issue drew little focus on the call..”

Interesting.

Yep, that is nuttty

Its a stunning number. It should be progressing down but its a stunning number regardless.

LEAP has its issue but I don’t think its anywhere near that number (be interesting to find out what it is)

No where to go with A220 or E2 types.

I think that just means Pratt had correctly quantified the losses and costs in earlier quarters, so did not have to change guidance or accept additional loss, beyond that previously forecast.

It’s still costing them about $2B per year, but they have the revenue to support the loss.

I asked AI (google) what are the main technical reasons for this MRO drama, instead of setting up my own research 😉 :

“The main technical reason that hundreds of Pratt & Whitney Geared Turbofan (GTF) engines have caused mass groundings is a manufacturing flaw involving contaminated powdered metal. This defect affects critical rotating components, which can lead to premature cracking and requires mandatory, expedited inspections and replacements. The scale of the inspections, combined with other durability issues, has overwhelmed the engine maintenance network, leading to extensive delays and aircraft groundings.

*** The contaminated powder metal defect ***

– Source of the problem: Between October 2015 and September 2021, a “rare condition” of contaminated powdered metal was used to manufacture key engine parts.

– Affected components: The flaw primarily affects high-pressure turbine (HPT) and high-pressure compressor (HPC) disks, hubs, and air seals.

– Safety risk: The metal impurities can cause microscopic cracks to form and grow much earlier than expected. If left unaddressed, this could lead to a catastrophic, uncontained engine failure.

– Affected engine models: The issue is most pronounced in the PW1100G engine, which powers the Airbus A320neo family, but accelerated inspections also apply to the PW1500G and PW1900G engines used on the Airbus A220 and Embraer E2, respectively.

*** The ripple effect of mandated inspections ***

The technical issue has been compounded by severe logistical problems in the aviation maintenance and supply chains.

– Mandatory inspections: Following Pratt & Whitney’s disclosure in 2023, aviation authorities like the FAA and EASA mandated accelerated inspections of affected engines. Initial estimates projected around 1,200 engines would need to be inspected.

– Overwhelmed maintenance facilities: The influx of engines needing complex, unscheduled inspections has overwhelmed maintenance, repair, and overhaul (MRO) facilities. As of 2025, inspection times have ballooned from a normal 60 days to over 300 days per engine.

– Chronic aircraft on ground (AOG): Because of the long maintenance times, airlines have run out of spare engines, forcing them to ground aircraft until inspected and repaired engines are available. As of mid-2025, between 700 and 800 GTF-powered aircraft remained grounded worldwide.

– Parts shortage: The need for replacement parts, particularly forgings and castings, has also strained supply chains, which Pratt & Whitney is still trying to ramp up in late 2025.

– Durability and wear issues: In addition to the metal defect, some GTF engines have also experienced other durability issues, including premature wear and corrosion, particularly in harsh operating environments.

*** Consequences for airlines ***

The GTF issues have created a domino effect for airlines operating GTF-powered aircraft.

– Lost revenue: Airlines face significant financial penalties from operating fewer aircraft, with some receiving compensation from Pratt & Whitney.

– Spare parts sourcing: In a desperate attempt to find working engines, some airlines have resorted to “parting out” and scrapping nearly new Airbus A320neo and A220 jets to use their engines on other grounded aircraft.

– Flight cancellations: To cope with the reduced fleet capacity, carriers have had to cut routes and frequencies, causing disruption for travelers. For example, in October 2025, one report indicated that 22% of the global Airbus A220 fleet was grounded”

This was in the earlier LNA report on A220

A handful of A220s have been scrapped to monetize for parts rather than be stored indefinitely, running up storage fees, awaiting new engines.

This is misleading as it should have also pointed out the same has happened to 5-6 yr old A321neos

‘As a result, more than a dozen recently produced A320 family aircraft have now been torn down for spares. ”

https://airinsight.com/parted-out-for-engines-young-aircraft-retired-early/

I gotta think that resorting to such extreme measures means that this episode is expected to last a very long time. If these scrapped airframes had a chance of becoming revenue producing resources in a few (3-5) years it would make less sense to scrap them. It also means that the values of engines and other cannibalized components will remain high for many years. One would think that this situation would also, eventually, drive up new aircraft prices. However, the long order fulfillment cycle may dampen this kind of inflation.