Leeham News and Analysis

There's more to real news than a news release.

Boeing 3Q2025: 777X gets new $4.9bn write off as earnings results prove mixed

By Karl Sinclair

![]() Oct. 29, 2025, © Leeham News: The Boeing Company (BA) took another charge in the third quarter, to the tune of $4.9bn, on the struggling 777X program–which has yet to deliver a single aircraft to a customer.

Oct. 29, 2025, © Leeham News: The Boeing Company (BA) took another charge in the third quarter, to the tune of $4.9bn, on the struggling 777X program–which has yet to deliver a single aircraft to a customer.

Boeing released its 3Q2025 results, following the positive sentiment surrounding the second-quarter results. Despite posting the first positive Free Cash Flow (FCF) since 2023, investors drove shares down nearly 5% by midday.

Boeing’s CEO Kelly Ortberg placed the blame directly on Boeing’s doorstep when he said on the financial network CNBC Wednesday morning, “This is something (the 777X/737 Max certification) that was driven by our inability to get through the certification process as fast as we anticipated.”

Entry into service (EIS) for the 777X is now expected in 2027, rather than next year. The MAX 7 and MAX 10 are still expected to be certified next year.

Entry into service (EIS) for the 777X is now expected in 2027, rather than next year. The MAX 7 and MAX 10 are still expected to be certified next year.

Third-quarter losses from operations at Boeing Commercial Aircraft (BCA) totaled $5.353bn, deepening from the 2024 results, when the division lost $4.021bn.

Free Cash Flow was $223m for the quarter and ($2.252bn) for the first nine months of 2025. Operating cash flow was $1.123bn for the quarter, ($266m) for the year, driven by higher commercial deliveries.

Corporate net losses for the quarter totaled $5.339bn, an improvement over 2024 results, when the company lost $6.174bn.

Company-Wide Results

Cash and cash equivalents, along with short-term and other investments, dropped to a combined $22.984bn at the end of the quarter. This declined from the start of the year, when it totaled $26.282bn, a difference of $3.298bn.

Consolidated debt was $53.353bn, down modestly from $53.864bn, a $511m change.

Boeing reported 3Q2025 results of $23.270bn in total sales and a net loss of $5.339bn, along with an operating margin of (20.5%). Net losses for the year totaled $5.982bn, on company revenues of $65.515bn.

Newly minted Executive Vice-President and CFO Jay Malave expects a cash burn in the region of $2.5bn for 2025. Regarding the 777X future liquidity usage, he said, “[Boeing] expects that starting in 2029, neutrality will go to a benefit positive free cash flow for the program. The next year is gonna be a little bit heavy, but it’ll continue to improve from year over year from that point.”

Cash burn for 2026 due to the 777X program is expected to exceed previously estimated levels of $2bn.

Boeing CFO Jay Malave. Credit: Boeing.

The Boeing revenue figures are approaching the numbers it used to generate before all the setbacks it suffered, starting in 2019.

If the company matches 3Q2025 revenues of ~$25bn in 4Q2025, it will have topped the $90bn mark for the year, which begins to approach Boeing’s historical revenue range.

For comparison’s sake, in Boeing’s record-setting year of 2018, it posted full-year revenues of $101.127bn and had net earnings of $10.46bn.

This would leave the FY2025 results some ~$10bn shy of its previously reported record revenues and earnings–the difference being, of course, that earnings will fall far short of what Boeing had achieved that year.

Boeing Commercial

The division generated $11.094bn in revenues for the quarter, on deliveries of 160 aircraft. This is an improvement over 2024, when 116 jets were delivered and $7.443bn in sales were recorded. A strike from September 12, 2024, into mid-November shut down BCA and all deliveries. Losses soared, and Boeing went to the equity and debt markets to raise $24bn to avoid running out of cash.

For the first nine months of the year, BCA delivered 440 aircraft to customers, generating $30.115bn in revenue. Operationally, it has cost the company $6.447bn to do so.

While an increase in deliveries usually results in an improvement in the bottom line, this was not the case in 2024, when BCA lost just $5.879bn on 291 deliveries.

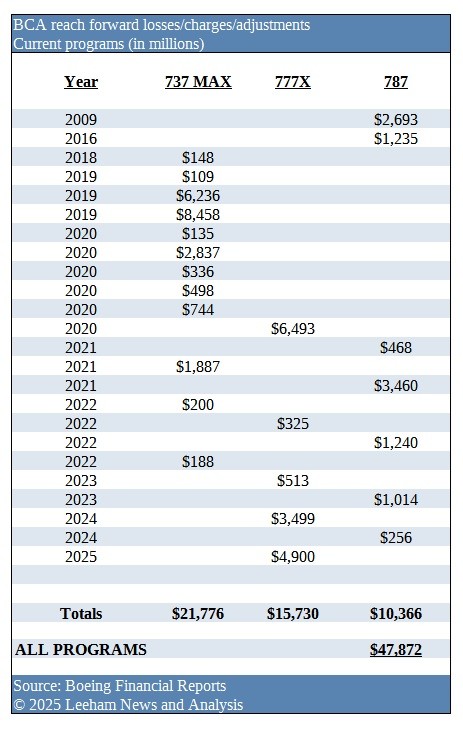

Entry into service of the 777X has now been pushed back to 2027, as previously reported by launch customer Lufthansa and confirmed by Boeing in this filing.

Launched in 2013, the aircraft was initially scheduled to enter service in 2020. Fourteen years later, the program has cost the company dearly.

While Boeing describes the current $4.9bn write-off as a non-cash charge, that description is misleading.

Yes, the current entry does not involve any cash accounts, but this is simply because those amounts have already been spent in previous periods, as LNA has reported earlier. Boeing has just waited until now to record them on the Consolidated Statement of Operations.

Total write-offs for the 777X program have now hit $15.730bn, a truly stunning amount, given that the company has no revenues on the type, to show for it.

The program will easily eclipse the $20bn loss mark, as 2026 costs the company more cash flow.

BCA still has a mild inventory build-up, with five 737 MAX and 10 787 Dreamliners awaiting delivery, which should be completed in 2026.

BCA still has a mild inventory build-up, with five 737 MAX and 10 787 Dreamliners awaiting delivery, which should be completed in 2026.

In a spot of good news, Boeing reported that it had secured a production increase on the 737 MAX program to 42/mo, up from the current 38/mo.

“We are, as we speak, rolling at the 42 rate,” said Ortberg. He continued, “…we’ll go to the next, (which) would be the 47. I mentioned in the prepared remarks, not earlier than six months, because we need time to go to the new rate, demonstrate stability.”

The 787 program continues to work toward a stabilized production rate of 8/mo, and expansion work on the Charleston (SC) production facilities is progressing.

Boeing is investing capital in the FAL in South Carolina to double its footprint. It can reach 10/mo with the current infrastructure, but has its sights set on a production rate in the teens by 2028.

Certification Issues

On the progress being made on the certification front, Ortberg said, “The issue is solely around getting the certification work complete. We had anticipated getting TIA approval. That’s what’s needed, actually, to get CERP credit when we fly those particular tests. We have not been able to achieve the certification credit. And that’s because we haven’t gotten the TIA approval.”

Boeing underestimated the effort required to obtain the Type Inspection Authorization (TIA) certificate and lacked a realistic plan to address the issue.

At the same time, Boeing reported that it had once again secured what it calls “limited delegation authority” from the FAA. Ortberg said, “Also in the quarter, the FAA announced it will allow delegation to Boeing to issue airworthiness certificates for some 737 MAX and 787 airplanes.”

Other Segment Results

With most of the focus on BCA and the 777X woes, both Boeing Defense, Space & Security (BDS) and Boeing Global Services (BGS) had less spotlight shone on them. BDS reported relatively modest earnings of $114m on revenues of $6.902bn for the quarter.

While the results may seem relatively benign, given the division’s history, this is a welcome bit of good news, as the segment continues to post positive results.

For the first nine months of 2025, BDS earned $379m on sales of $19.817bn. This is up over 2024, when it lost ($3.146bn) on revenues of $18.507bn.

While Defense still must deal with a strike by the IAM at its St. Louis (MO) production facility, the potential for a catastrophic financial outcome for the division is not nearly as high as it was during the BCA strike.

BDS also secured a $2.8bn contract from the US Space Force, bolstering its cash position with additional deposits.

Boeing Global Services (BGS) continued its winning ways, as it posted a $934m gain on sales of $5.370bn for the quarter. Year-over-year, this is up 12% on earnings ($834m in 2024) and 10% on revenues ($4.901bn for the same period). For the first nine months of 2025, total revenues are up 6% (YoY) to $14.714bn, and earnings jumped 12% to $2.93bn.

M & A details

In the final period of the year, Boeing is expected to conduct some business on the Merger & Acquisitions (M&A) front. Plans are still in place to acquire the majority parts of Spirit Aerosystems of Wichita (KS), a former Boeing division. This transaction is expected to cost the company some $4bn in stock and to assume ~$4.3bn in debt onto the Boeing balance sheet.

There were scant details revealed regarding the upcoming sale of Jeppesen, which is still slated to conclude in 4Q2025. Spinning off that asset will net Boeing around $10bn.

The net financial effect to Boeing will leave them with some $28bn in cash and equivalents by year’s end, according to CFO Maleve.

*****************************

The Rise and Fall of Boeing and the Way Back

Boeing CEO Kelly Ortberg says one element of the company’s considerations before it launches a new airplane is Boeing’s own recovery. Boeing, too, must be ready—and there is a long way to go before it is.

Boeing CEO Kelly Ortberg says one element of the company’s considerations before it launches a new airplane is Boeing’s own recovery. Boeing, too, must be ready—and there is a long way to go before it is.

The Rise and Fall of Boeing and the Way Back, published last month by LNA editor Scott Hamilton examines how Boeing got itself into industrial disgrace and how it now is at long last on the path to recovery.

The book is available here.

“..Total write-offs for the 777X program have now hit $15.730bn, a truly stunning amount, given that the company has no revenues on the type, to show for it.

The program will easily eclipse the $20bn loss mark, as 2026 costs the company more cash flow..”

I wonder when the Boeing 777-X will actually have its EIS. I won’t mention the repeatedly-delayed MAX 737-7, MAX-10,

and the engine nacelle-heat issue on all the MAXs.

All bets are off at this point..

+1

How on Earth do you spend over $15b on developing a derivative?

Not to make this into an A v B argument, but the 330neo, a more straightforward re-engine, cost $2b. Surely (?) Boeing should have the competence to pull off a similarly simple program at similar cost. So did they just shoot themselves in the foot with the new wing?

The irony is that the 330neo’s re-twisted wing + winglets are estimated to give a ~4% efficiency gain, while the 777X’s new composite-with-folding-tips wing is estimated to give a ~7% efficiency gain. Did Boeing spend over $10 billion to improve fuel burn an additional 3%??

@Mike

Boeing has a recent history of reaching one or two steps too far on development…and in doing so underestimates technical risk.

This program is cursed. Hull rupture, engine design issues, engine mount fails, COVID, Max hangover. These are all problems that are found only in series and not in parallel.

2027 presumes that nothing of note is found in flight testing. Would you take that bet?

The B787, 747-8 and Max programs are all development failures as well.

What you did not mention is that when the 777X was launched was during peak program deliveries. The market has fundamentally shifted to smaller aircraft with all the necessary range. That accounting block of 500 might be optimistic (it made sense at program launch), And the more operators that are flying the A350 creates the inertia that will ultimately doom the 777X to the same scrap heap as the A380.

+ 1

“The program is cursed.”

Need an exorcist?

Given the extraordinary losses the 777X program has suffered and given that it appears that it will never make money for the company what are Boeing’s options? If they cancel the program today do they go bankrupt this year? And if they continue the program and deliver the aircraft, but not enough to make any money, do they also go bankrupt, but not for another 15 years? Or maybe something positive happens during those 15 years and they don’t lose money on the program. Is this a case of the “sunk cost fallacy” in reverse? Have they invested so much in the program that they can’t afford to cancel it? Same question applies for Max -7 and Max -10, although the -10 appears to have a better chance at eventually turning a profit.

All valid and interesting questions.

And now a non-financial consideration: if they pull the plug on the 777X, then they cede that market to Airbus…and concurrently lose their tradtional lead in widebodies overall.

Similar story as regards the 737-10…alhough the 737-9 would sort-of take its place, and sort-of limit the damage.

At this rate, BCA will never return to profitability: it will remain a jobs program, and a market prop-up for GE and RTX engines.

@Benedict

What happens if they cancel the program today? All deferred production costs are written off.

The nature of the loss is not COPQ but development errors. The Max has been reworking through the shutdown inventory. The 777X has a small measure of that…but now awful. This is not a “terrible” program if it stands on a clean slate.

Also keep in mind…sometimes you maintain a product line to stay in business. Boeing does not have a Plan B if the 777X fails.

“On the progress being made on the certification front, Ortberg said, “The issue is solely around getting the certification work complete. We had anticipated getting TIA approval. That’s what’s needed, actually, to get CERP credit when we fly those particular tests. We have not been able to achieve the certification credit. And that’s because we haven’t gotten the TIA approval.”

“Boeing underestimated the effort required to obtain the Type Inspection Authorization (TIA) certificate and lacked a realistic plan to address the issue.”

***

Unfathomable.

Confirms that BA no longer has a clue how to get a plane certified.

🙈

They’re not receiving TIA because they haven’t complied with the regulations. Comply and you’ll get the TIA Mr. Ortberg.

Don’t forget EASA is driving the certification rules for the FAA. No more rubber stamp from the FAA after what happened with the Max.

+1

Kelly prefers to complain about the “mountain of work” involved in certification.

Perhaps he was assuming/hoping that his buddy in Washington would arrange a “golden pass” for fast-track cert…or, better still, a return to the good old days of self-cert.

Who knows? A hefty donation to that new ballroom might, as yet, work a wonder 😉

Chump change for Ortberg/BA:

> Initially announced at a cost of $200 million, the Trump ballroom is estimated to cost $300 million

+1

This statement is false. The 777X is fully compliant with the regulations, the issue is meeting new documentation requirements that didn’t exist before.

FAA will not permit the transition to the next phase of TIA until all the documentation is approved. It will take time for Boeing to work through the new requirements.

A: “The 777X is fully compliant with the regulations,”

versus

B: “the issue is meeting new documentation requirements that didn’t exist before. ”

If B is not met A can’t be true, right?

additionally:

“fully compliant” : to what set of requirements (dated) ?

“fully compliant” : has this been checked/proven? lack of docs is telling.

Haha that poster is a wordsmith.

> “Boeing must demonstrate through its own testing and analysis that the aircraft meets regulatory requirements” before the FAA greenlights

No, this is another false statement. If you can point to a regulation deficiency in the 777X, you are welcome to do so. But you can’t.

@ Pedro

Indeed!

Unwillingness to accept that the 777X still doesn’t meet certification requirements –> requires smokescreening to avoid blame.

Rob

Why don’t you talk with Ortberg? That’s from a report interviewing with Ortberg.

@ Chris

Absolutely true.

BA hasn’t bothered to (properly) do the engineering analyses required by the FAA.

That’s a failure of engineering and math — not a bureaucratic glitch.

Less complaining, more engineering modelling.

This is absolutely a false assertion, intended to mislead and malign. Made without factual evidence of any kind. Just pure hatred.

Utterly disgusting that this continues to be allowed here.

Yawn. broken record.

push the picup a bit forward.

What “factual evidence” did you provide to support your assertion? None.

Utterly disgusting you’re allowed to continue this evidence-free practices.

PEDRO

This is an exceptionally complex subject full of interdependence that most are unaware of. You cannot break a soundbite into an answer because of these relationships in the subjest

The certification problems with the 777x are caused by BOTH the FAA and Boeing. The act formally set boundaries on delegation, completely redefined the classification of Major and Minor changes and how they are handled. The Certificarion process of old and the ability of previously flown hardware to be used as proof under the “same as except” logic was basically done away with. The process of doing a derivative aircraft today is completely different than in past programs. We went all over that a couple weeks ago.

Here we go again. This is Boeings first airplane after the end of the commonly understood old style derivative cert process. That’s the fact unrealized in the conversation. It has actually caused a mountain of new work. The FAA actually has to perform a far larger segment of the work. There is friction between the FAA and Boeing on the finer points on how the data is being submitted, it starts with Boeing having an analysis proof method based on their experience that in many times is different than the FAAs new proof methods. It’s slowing down things that used to be very simple processes. When you combine Congress’s restrictions on delegation in the Air Safety act along with not passing an FAA Reauthorization Act, lots of time gets used up accomplishing nothing. Is this Congress’s fault, yes but they are not the only reason. As I have said before, Boeing has not adapted to the changing landscape but they are not the only reason either. The FAA was instructed to make a sea change in the certification process and was never funded properly by Congress to accomplish their revised mission.

Remember the delays in certifying. the single skin Airbusb fuel tank and the last minute delays in its certification? There were points that needed to be redone and all you said about it was that they worked their way thru it ok and its not a big deal. THIS ACTUALLY IS A BIG DEAL.

Congress enacted hundreds of pages of new laws, The FAA with no more budget took on a far larger portion of the work in the past AND the entire set of definitions of how a change is evaluated for Certification impact and how much of the certification basis was invalidated by it. Some of us here that worked in the industry doing just these kind of things understand the scope of the changes.

This is why your fingerprinting sound bites are so disingenuous. You only put the small pieces that support your narrative into print. You do not do your work in anywhere near the context required for a true conversation. Are you wrong…. No. Do you mislead by concealing facts of consequence…… ABSOLUTELY

@ Pedro

Well said!

Ortberg has admitted that BA hasn’t provided proper analyses to the FAA…and he then tries to cover his ass by suggesting that the FAA is somehow to blame for that.

When the A321XLR required modifications to its RCT, Airbus listened, Airbus modified, Airbus provided the required analyses and documentation…and, lo and behold, it promptly got its certification in the mail.

# Scapegoating

As I’ve said previously, BA lived through more than a decade of self-cert, that’s why it’s so painful for BA to adjust/re-adapt to the new reality when an independent third party takes over the review.

Everyone nowadays are going through the same revised FAA certification process, so the process is not particularly demanding for airframers, but the one who stumbled the most is the one which enjoyed the most during the self-cert era.

The issue here many posters ignored is the mentality of the leaders at BA, building optimized schedule based on their hopes, not planning in accordance with the new reality. So who should shoulder the blame here??

Karl, is there any way we can estimate from these non-cash write-offs how much the compensation to customers for late 777 EIS is?

Alternativly, do you have an idea how much clane purchsse contracts typically promise for such delays?

How painful it is because BA survived on self-cert.

More from the AW:

> Approval for the new widebody is being sought via a phased TIA, which breaks the required certification tests into batches. *Boeing must demonstrate through its own testing and analysis that the aircraft meets regulatory requirements before* the FAA will greenlight the related batch of tests which, in many cases, involve the agency’s test pilots.

> “We very much underestimated how much work it was going to take for us to get the TIA approvals and for the FAA to have the opportunity to review all the data submissions that are required.”

> Boeing was granted authority to begin TIA in mid-2024 and is currently in the latter stages of TIA Phase 2. Its previous plan, which envisioned first deliveries in 2026, saw TIA Phase 3 starting “in the third quarter” of this year, CFO Jay Malave said on the call. “However, this authorization has been delayed as Boeing and the FAA work through the supporting analysis,” he said. Boeing now sees the next TIA phase starting late this year or in early 2026, he added.

The revised and still uncertain timeline means customers at the front of the delivery line must adjust their network plans. Lufthansa’s recently announced move to schedule its 777-9 debut in the 2027 summer schedule foreshadowed Boeing’s ongoing challenges.

The new schedule also means a slower production ramp-up—and likely more headaches—for suppliers.

“We just have to flow the new, revised schedule out to our suppliers, and then we’re going to have to negotiate on a case-by-case basis the impact that has to the various suppliers,” Ortberg said when asked about the supply-chain ramifications. “Depending on the commodity, the impact might be significant or might be fairly insignificant. So, we’re going to have to work through that.” [More compensations are coming]

[Other than a new anti-ice system, there are futher works that BA has to complete before the MAX 7/10 certification. ]

> “If you take the engine anti-ice out of it, there is still work to be done to complete the certification, probably a little more work on the -10 than the -7,” Ortberg said

Translation: further slippage of EIS to 2028 (at the earliest) for all three models.

Imagine that: Boeing actually has to show that its models are certifiable! Who’d have guessed that?

Further work on the MAX…what a shocker! 🫣

I agree it’s likely that none of the three aircraft- 777-X, 737-7, 737-10- will have EIS before 2028, if then.

That prediction is unfounded and unlikely in the extreme.

In fact Ortberg said in the earnings call that the 737 certifications are still on track for first half of 2026.

It’s only the 777X that’s been delayed, and that’s due to new documentation requirements.

Ortberg said that Boeing has already completed the certification testing of the 777X, to ensure compliance when the FAA is finally ready to transition to the next phase of TIA. They have more than 4,000 flight hours on the aircraft.

That not the truth, the whole truth or nothing but truth.

“Ortberg said that Boeing has already completed the certification testing of the 777X”

Factually false!

The certification testing is now progressing in phases. Boeing is stuck without approval moving to the next phase testing.

Yet another false statement. Ortberg specifically said Boeing had flown the FAA certification profiles to ensure there are no regulatory violations in certification. But FAA will not fly them until the documentation is complete.

That is the new FAA policy for phased TIA. And the documentation standards are evolving as certification proceeds. All of this is in the earnings call.

“Ortberg specifically said Boeing had flown the FAA certification profiles to ensure there are no regulatory violations in certification.”

That’s not what Ortberg said, stop your disinformation campaign.

Who said the MAX are still on track for the first half?

Who said it’s due to the new documentation requirement? That are all your inventions!

@ Vincent

Indeed.

Ortberg hinted at some other gremlin in the MAX, without specifying what is was. That doesn’t bode well at all 🙈

Does anyone attach any importance any more to timelines given by Boeing?

Tim Clark could write a book on that, couldn’t he?

Another openly false statement. There is no “gremlin” in the MAX, nor did Ortberg make any such reference.

What he said was there was still certification work to be completed, related to documentation since TIA is almost complete for both versions of the MAX.

The anti-ice is the only open technical issue remaining.

@ Vincent

Ortberg’s quote was:

““If you take the engine anti-ice out of it, there is still work to be done to complete the certification, probably a little more work on the -10 than the -7,” Ortberg said”

More work on the -10 than the -7?

Suggests the new gremlin may have something to do with the -10’s telescoping landing gear…what do you think?

No reasonable or logical person would conclude there is a “gremlin” from that statement. Which explains your commentary quite well.

Yet there are more to be done by BA before the FAA certification, contrary to what many here said previously.

Regarding the 767 commercial program, Boeing’s latest Form 10-Q states that “during the nine months ended September 30, 2025, we recorded further reach-forward losses of $241 million primarily driven by higher production costs.”

During 2024, Boeing had recorded “reach-forward losses of $580 million” for the 767.

In previous years, Boeing had not recorded losses on the 767 commercial program, but starting in 2020, it stated in its annual filings that the 767 commercial program had “near break-even gross margins.”

Based on these data, it would appear that the 767 commercial program is overall unprofitable and that the low production levels of recent decades have ended up wiping out all the profits that had certainly been accumulated during the first two decades of 767 production.

From 1982 to 2003, Boeing delivered 916 767s (an average of 3.6 deliveries per month). From 2004 to 2017, however, deliveries were only 190 (1.1 per month). Since 2018 (with the start of deliveries of the 767-2C/KC-46), the monthly average has risen to 2.5, but this has not been enough to make 767 production profitable again.

Considering that Boeing also incurred in more than $10 billion of losses on KC-767 and KC-46 programs, perhaps it would have been better for Boeing to have ended 767 production in 2004 (as it did for the 757). The money saved would have been enough to fund much, if not all, of the development of a brand-new airliner.

+1

2012: FAA Aircraft Certification reform act pushed by Boeing Congress

https://www.faa.gov/media/32711

2014: Congress Pushed FAA to speed up reform by re-authorization budgets

https://www.gao.gov/products/gao-14-285t

2014 FAA pushed into to Fast Tracking Boeing 777X Certification, changed product rule. To speed up certification process, reduce costs.

https://www.frequentbusinesstraveler.com/2014/05/faa-to-fast-track-boeing-777x-certification/

2020-2021: Objective review of 737 MAX and general FAA certification process by independent group of international specialists. Exposing critical process weaknesses, FAA adjusts and become less dependent and cooperative. https://www.faa.gov/sites/faa.gov/files/2021-08/Final_JATR_Submittal_to_FAA_Oct_2019.pdf

As explained earlier, the current circumstances have nothing to do with “becoming less dependent and cooperative”.

That is a false narrative that has been called out here many times before. It doesn’t become more true by repetition. There are no statements by the FAA that support that conclusion.

The true story is as explained here many times, that the certification process has been slowed and serialized, in order to prevent the details slipping though the cracks, as occurred in the 737 MAX certification.

With the 777X, TIA has been phased and FAA will not authorize the transition to the next phase, until Boeing completes the new documentation regime. That new regime is being defined as it’s being implemented, and thus is difficult for Boeing to anticipate in advance.

There is recognition by both Boeing and the FAA that the current delays are unsustainable. The question is whether the wrinkles will naturally iron out with learning and experience, or whether the process requires adjustment. Probably a combination of both.

False narrative alert!

It’s because Boieng fails to “demonstrate through its own testing and analysis that the 777-9 meets regulatory requirements”

Ortberg made no such statement, nor did the FAA. Again you are welcome to point to the alleged regulatory violations or exception. But you cannot, because there is none.

Not true. You should have emailed Ortberg to find out.

It’s been reported by AW and I quoted them.

The FAA didn’t give TIA to Bo0eing because BA failed to “demonstrate through its own testing and analysis that the 777-9 meets regulatory requirements”. You can ask Ortberg, BA or the FAA.

@ keesje

You’ve hit the nail on the head.

In the earnings call, Ortberg admitted that BA hadn’t done the technical analyses required by the FAA. That’s not “paperwork” — it’s engineering math.

There is a false narrative being pushed that FAA bureaucracy is somehow to blame for BA’s inability to get planes certified. However, the public record clearly shows that ineptitude at BA is — and continues to be — the problem.

No evidence provided for either assertion, just allusions to the “public record”.

A tactic well recognized and called out hundreds of times for this commenter. No credibility can be attributed without evidence, and no value can be attributed to openly false statements.

Neither do you, Rob!

Not necessary to disprove a false assertion. The burden of evidence rests with you.

We’ve been over this countless times, but your entire line of argument rests upon the false assertion and demand for disproof. Which would flunk an elementary school class in debate, but it’s really all you have.

@ Pedro

Indeed!

The pot pointing at the kettle 😆

But you’re backed up by copious published evidence…whereas the poker faces have an empty hand 🙈

It better starts with you, Rob. Fiction writer can’t afford the truth.

If you accuse others, you also have to provide proof, but you can’t. That’s the hard truth.

Selling the family silver so as to fix the roof — some cash on its way to BA:

“Jeppesen, Foreflight Sale To Close Next Week: Report”

“The Air Current is reporting that the sale of Foreflight and Jeppesen to software investment fund Thoma Bravo will be finalized as early as Nov. 3. The news came out of Boeing earnings call earlier this week according the Air Current. The sale was announced last April and was estimated to be done by the end of the year. Boeing said it was selling the two units, along with OzRunways and AerData, for $10.55 billion in cash to raise money and to further its new leadership’s focus on Boeing’s core businesses.”

https://avbrief.com/jeppesen-foreflight-sale-to-close-next-week-report/

***

“…further its new leadership’s focus on Boeing’s core businesses”

Core business = burning money on never-ending certification delays.

$10.6 billion is not a small amount, what’s the impact on PBT?

Actually Ortberg said in the earnings call that the fault for the 777X certification delays was split between Boeing and the FAA.

He noted that the TIA process is very different from what it was before, and the Boeing and FAA are feeling their way through that process, as they go.

He also noted that Boeing and FAA are in discussions as to how to address the problem, as they both agree the current process is unsustainable.

And he noted that there continue to be no technical issues on either the aircraft or the engines. In fact Boeing has already completed the certification flight testing that is needed for TIA, in preparation for the FAA testing. No issues were discovered there either.

It’s unprecedented for TIA to be interrupted for a year, solely over issues of documentation. But that’s where they are now.

The failure is BA hasn’t demonstrated to the FAA through its testing and analysis that the aircraft meets regulatory requirements!!

Again that is not a factual statement from Boeing or the FAA. Nor does it become such by repetition. But I give you points for your parroting skills.

Rob

That’s according to report attributed to Ortberg. No more fictional posting or misinformation is going to solve BA’s problem. Better for those who are still stuck in Chicago to face the reality than spinning falsehood, lying is not going to save the company.

@ Pedro

Correct…it’s plain and simple, and profusely documented, but it’s not something to be squarely admitted to stockholders.

See my links ago — this failure was already clear back in 2021/2022.

Nope. That’s totally disinformation. What Ortberg said: “… there was learning in what analysis and data we had to have complete and submitted to get the TIA approval. Some of that’s for us, and I think it’s taking longer as well for the FAA to go through those submittals and get the approval.”

Remember, BA lived thru a decade (or more) of self-cert, of course it’d take longer for the FAA to do realistic review than BA’s rushed through self-cert! But that’s far different than the FAA has to take the blame!

BA stock is down 10% in 2 days, so emergency damage control measures are being enacted 😉

Lol, Pedro, I specifically said, as did Ortberg, that the blame is split between Boing and the FAA.

In addition, I explained why that is, as did Ortberg. Notably you have not addressed either of those points.

Reading comprehension is your friend, and an essential skill.

Well said Rob .

Speak your mind .

Ignore the Horde…

+1 for you.

@ Pedro

Absolutely correct.

Now that self-cert is off the table, BA just doesn’t know what to do — it’s like a deer staring into the headlights of an oncoming truck.

Ortberg predictably needs to try to shift blame onto the FAA, to shift the spotlight away from the company’s (and his) continuing failures.

Does anyone actually care what that man says?

Don’t tell us — show us!

I don’t know why we have a poster here who’s fond of putting words in other’s mouths: the latest example is what exactly Ortberg said in the 3Q25 earnings conference call, no one had said “the blame is split”, ever! Pure fiction from a poster who repeated to claim “factual discussion” but failed miserably for misleading and fact-free posts.

It’s more than a failure of comprehension, it’s a mental illness.

“Boeing Faces Five-Year Race to Deliver All F-15EX Jets for U.S. With No Room Left for Export Buyers”

“The U.S. Air Force currently plans to acquire 129 F-15EXs, with 126 expected to be delivered by the end of 2030 already nine months behind schedule. The delays stem from software issues, supply chain disruptions, and material shortages. Future production capacity could also be limited by the arrival of the sixth-generation F-47 fighter, which will likely take industrial priority.”

“Even at the projected rate of 24 aircraft per year, Boeing will need about five years to fulfill just the U.S. order. That means any potential foreign customers will either have to wait longer or fund an expansion in production, as U.S. military demand will always come first.”

https://en.defence-ua.com/news/boeing_faces_five_year_race_to_deliver_all_f_15ex_jets_for_us_with_no_room_left_for_export_buyers-16319.html

SO…desperate times require desperate measures:

“Boeing sweetens its Polish F-15EX offer with local deals, ‘Ghost Bat’”

“To make its effort more attractive to Poland, the U.S. company is combining it with an industrial cooperation package for the country’s defense sector, and the MQ-28 Ghost Bat loyal wingman-type drone offer.”

https://www.defensenews.com/global/europe/2025/10/31/boeing-sweetens-its-polish-f-15ex-offer-with-local-deals-ghost-bat/

***

Same MO as the 777X: try to trap the fly with a honey trap as regards promised delivery date, and then continue to string him along…

Ford doing a “rope-a-dope” with Donnie

“Ford to make new engines in India with $370 million investment, Bloomberg News reports”

Good grief!

India really is stealing the show of late.

# Backfiring

An interesting “blast from the past” — BA was dragging its feet in submitting required analyses to the FAA in 2022…and it’s still dragging its feet today:

“FAA says Boeing has not completed work needed for 737 MAX 7 approval”

“The Federal Aviation Administration told Boeing it has not completed key work needed in order to certify the 737 MAX 7 by December, according to a letter from the FAA seen by Reuters.

“Lirio Liu, the FAA’s executive director of aviation safety, told Boeing in the September 19 letter that the agency had concerns about the planemaker’s submissions and sought discussion “about realistic timeframes for receiving the remaining documents.”

“The FAA told Boeing to turn in all remaining System Safety Assessments (SSAs) by mid-September “if the company intends to meet its project plan of completing certification work [and receiving FAA approval for this airplane] by December.”

“Liu said as of September 15, “just under 10% of the SSAs have been accepted by the FAA and another 70% of these documents are in various stages of review and revision.””

https://www.rappler.com/business/faa-says-boeing-has-not-completed-work-needed-737-max-7-approval-september-2022/

***

Dragging its feet…and then trying to pin the blame on the FAA 🙈

Lol, nice retro post to 3 years ago!! Now let’s try addressing the current delay with current facts. As I did above.

A bridge too far for you, perhaps?

Another “blast from the past” — this one from 2021:

“FAA raises concerns over engineers appointed by Boeing for airplane certification”

“Boeing appointed underqualified engineers to oversee its airplane certification program, according to the Federal Aviation Administration (FAA).

“In a letter to Boeing last week, the FAA complained that in interviews with recently appointed safety engineers from the company this summer it had found many “are not meeting FAA expectations,” according to The Seattle Times.

“The appointments were made to fill openings left in the company’s safety engineer ranks after Boeing offered early retirement to some of its more senior FAA-authorized personnel during the COVID-19 pandemic, the Times reported.

“At one point, more than 20 engineers from a single certification speciality left Boeing in just one week, according to an FAA safety engineer who remained anonymous because they were not authorized by the agency to speak to the Times.

“The FAA’s letter noted that of 12 recent appointees tasked with dealing with safety issues, nearly 40 percent “struggled to demonstrate an understanding of FAA certification processes,” according to Reuters.”

https://thehill.com/policy/transportation/581190-faa-raises-concerns-over-engineers-appointed-by-boeing-for-airplane/

***

Hire some cheap rookies, consequently fail to meet certification demands vis-à-vis engineering analyses, and then try to pin the blame on the FAA 🙈

# Blantant_Scapegoating

Lmao, let’s go back even further in time!!

AW

“Emirates has 35 777-8s and 170 777-9s on order, but delivery of the first 777-9 has been deferred multiple times since its planned delivery date in 2020. “The official date for our contract was this month: October 2025,” Clark said, but he had anticipated delivery in the second half of 2026, potentially slipping to spring 2027.”

And Clark isn’t buying the narrative that the delay is the FAA’s fault.

It’s Boeing that he regularly lambasts — not the regulator.

“… potentially slipping to spring 2027.”

Now based on what we know, even this looks hopelessly optimistic, 2H or Q4 is more likely.

Boeing has a long, long history now of overpromising and underdelivering.

Remember, it was *only a month ago* that

Boeing claimed the 777-X would be certified “late this year”, and delivered in early 2026.

I figure a mid-2028 actual EIS for that aircraft will be about right, given what’s written above; we will surely see.

> Emirates President Tim Clark has described himself as being “a little bit miffed” after learning about Boeing’s latest timeline for the 777X program from the media rather than the manufacturer directly. [Whoops!]

> “I was with them recently, in New York, and before that in Seattle. There was never any hint that they would make an official pronouncement that 2027 was to be the delivery year,” Clark said Oct. 30 on the sidelines of APG World Connect here in Seville. “It was all about getting the certification process done by the middle of next year.”

> “Now what happens is that I don’t know when the aircraft’s going to be delivered. When you say 2027, do you mean January or December?…

> the 777-10, which would be around 150-in. longer than the 777-9. This would equate to roughly five or six more economy seat rows.

[Six rows in 150-in.? 😱 ]

> Speaking during the company’s third-quarter briefing on 30 October, Spohr said Lufthansa “never expected” the [777-9] to be in commercial operation during 2026.

> Spohr says the *US government shutdown, which began on 1 October, is delaying deliveries*, and the carrier no longer expects to receive 10 [787-9] this year, but “probably around eight”. [How come delays caused by the shutdown of the USG was never mentioned in BA’s conference call?]

It seems to me that anyone who has spent the past 20 years believing, re-adopting, and defending Boeing’s statements and predictions must be exceptionally flexible, remarkably forgetful and forgiving.

IMO 777x trouble is a result of forced FAA aircraft certification reforms from 2012, FAA surprizingly approving a 777x changed product rule certification strategy for a new aircraft, combined with ODA, and exposure after the world grounded the 737MAX before the FAA in 2018 and independents audited the new streamlined certification proces.

https://www.businessinsider.com/boeing-ceo-called-president-trump-after-737-max-8-disaster-ny-times-2019-3

FAA/Boeing are now certifying the 77x via an officially approved, misplaced process. Delay: 7+ years.

+1

KEESJE

Absolutely correct.

The Boeing of today barely resembles the Boeing I worked for……. I was in Manufacturing Planning at DAC in Long Beach and was recruited to go north to staff up the 747-400. The change was illuminating. Nobody ever writes about the fundamental differences in the workforce structure between the 2 places. At Long Beach, the Planners were the highest paid hourly employees in the company. Mechanics had a place to take their skills from the factory floor and write great assembly sequences for the product. At Boeing, Manufacturing Planners were thought of as second tier of unworthy tech employees of minimal value. Very few if any had actually been airplane makers before becoming and it showed. They relied on the planning programs to make sure the parts were accounted for on the PL and that was about it. Douglas died a slow death, not because of the people, they were genuinely above average. Douglas commercial died from getting too small to matter any more. they got below a number we jokingly called the minimum economic unit. That was the size you needed to be in the market to be successful.

The concept of minimum economic unit is the battle Embraer is fighting. Great product, fabuluous people, but not enough product getting to market to thrive. This is the hill Comac must climb. Their product is improving more rapidly than anyone else and they are close to on par with the current generation of aircraft. They should make it because the government has decreed it to be so.

So what of Boeing. Boeing is shrinking and has been doing a crappy job for over a decade. They have lost their way in fighter aircraft, the F15 and F18 are legacy products being milked. They missed the F35, F22 and are relying on the f45 to stay in the fighter business, a shakey bet with no guarantee of profitability. They have the Apache and Chinook, 2 more legacy programs being milked. They missed the Blackhawk and its successor. They still build the Harpoon, yet another legacy DAC program, the bomb tail kits sell by the bushel but lack a follow on. When Boeing and McDac merged it was the world’s largest defense contractor marrying up to the biggest commercial airplane maker, because both had lost their ass on the other side of the business. Boeing got run out of defense and Dac out of airliners. IT was supposed to be a reset to make the combined company big enough everywhere to continue forward and be profitable. It hasn’t worked that way, Defense is a mere shadow of itself and Boeing Commercial hasn’t had a really profitable program of late and the programs that used to make money had huge setbacks. So where is it today, deeply in debt with a pile of borrowed cash in the bank. The program execution on the 737 has improved a lot. The 787 program execution is improving a lot. The new airplanes are continuing to slip and transparency isn’t there on why. The battle Boeing must win above all else, is to not become too small to be relevant, and they have been putting those dominos in place for 15 years. I hold out hope that at the next fleet replacement cycle that they are the winners, if they aren’t it will be difficult to continue. Comac isn’t the immediate threat. Todays threat is internal mediocrity and only a great leader demanding change is going to fix it. Is Ortberg the guy, maybe to start the change but he is too old to be there for the whole journey.

I picked a great time to get hurt and leave Boeing years ago. I can’t imagine the daily craap that gos on now.

Thnx for the story, must hurt seeing your old colleagues struggling. Hopefully the F47 & trainer get certified according to plan.

KEESJE

Yeah it hurts but not being honest about it doesn’t improve things. I post here with the hope that somebody in a change maker position might add my thoughts to his decision-making process. The good news is that Boeing is getting better, the other good news is that the industry is sort of in a detante position where the next product isnt in the cards for a decade by a lot of informed estimates. That means that when the next airplane happens, things will be completely different fabrication wise and engines will be different. This gives Airbus the chance to kill offf a large Boeing market share OR for Boeing to make a recovery move. Jurys out either way and it will be interesting if Boeing can gain a bit of humility and do a better job.

There needs to be an industry reset for certification requirements. It is nobody’s interest to see these programs drifting aimlessly. We have a conflict where there is a global desire to encourage maximum efficiency for climate and fuel purposes meeting a certification process that has exploded to a baseline 10 years. We went to the moon faster.

A lot of the explosion in cert timing is to meet a safety threshold that has evolved to the expectation that any new type will meet or beat a safety record of a program that has had decades in service. NASA is the poster child for an agency that has become so onerous in their certs that they end up accomplishing nothing at all.

None of this is a value judgment. We will all be well served if we can ask ourselves “what can be done with a five year development program” and asking ourselves “is that good enough”

Let’s first see how quickly the A350F gets certified, before we start talking about an apparent new 10-year norm.

We’ve already seen the A321XLR get certified with relatively little hassle.

Just because BA can’t generate required engineering anslyses doesn’t mean that other OEMs can’t.

“We went to the moon faster.”

In the 20th century only. It’s struggling in the 21st century, no different than BA whether you see it as a systematic issue or not.

More misery at Spirit Aero:

“Spirit AeroSystems Reports Third Quarter 2025 Results”

– Revenues of $1.6 billion

– EPS of $(6.16); Adjusted EPS of $(4.87)

– Cashflow in operations of $(187) million; Free cash flow of $(230) million

“Operating loss in the third quarter of 2025 increased compared to the same period of 2024, primarily due to higher changes in estimates charges and lower program margins on Boeing programs, partially offset by lower excess capacity charges and a reversal of accrued liabilities.

“Total changes in estimates in the third quarter of 2025 included net forward losses of $585 million and unfavorable cumulative catch-up adjustments of $14 million.”

Total debt: $4.33B

https://www.prnewswire.com/news-releases/spirit-aerosystems-reports-third-quarter-2025-results-302601403.html

***

Sounds like a wonderful investment for Boeing

Another clean house for Jay once the transaction is closed?

In 2014 FAA approved the wrong certification strategy for the 777X, which is a new aircraft really. With their backs against the wall.

Now the chickens come home to roost. Launching customer Lufthansa & their authority EASA are watching closely.

Haven’t we seen this movie before?

> UK RAF E-7 Wedgetail: the most expensive aircraft ever bought by the UK! Originally just over £2bn for 5, now £2.28bn for 3, making each cost £760m! And not a single useable aircraft has yet been delivered, with no prospect of such.

IOC end of 2025?

Dream on! Of note, E-7 is now known either as “the RAF’s Ajax” (not a compliment to Ajax, either…), or “Voldemort”, which in Harry Potter jargon equals, “he who shall not be named”.

“When the aircraft were ordered in 2019, the MoD set the total programme cost of £2.15 billion, which included buying simulators and building ground infrastructure. This broke down at £430million per aircraft, but under the new budget, the RAF is buying three jets at a unit cost of £760 million, which represents a 76% cost increase.”

https://t.co/PApyPjgcNG

South Korea recently decided not to buy more E-7s:

“South Korea’s air force to receive four Global 6500 AEW&C aircraft by 2032”

“The Republic of Korea Air Force is set to receive its new Bombardier Global 6500 airborne early warning and control (AEW&C) aircraft in the 2030-2032 timeframe.

“The initial two aircraft will be integrated by prime contractor L3Harris in the USA, with the two follow-on examples to undergo work by Korean Air in South Korea, according to Korean Air. ”

“The four jets will add to South Korea’s fleet of four Boeing E-7 Wedgetail AEW&C platforms. Additional E-7s – a derivative of the 737NG – and the Saab GlobalEye; also based on the Global 6500 airframe, were also considered by Seoul for the follow-on AEW&C order.”

https://www.flightglobal.com/fixed-wing/south-korea-to-receive-global-6500-based-aewandc-aircraft-by-2032/164973.article

France recently chose the Saab Global Eye.

Germany and Denmark are also considering it.

Sweden and the UAE already have it.

It seem the Saab-BBD Globaleye is rapidly gaining populairity in Europe, like the KC-390.

Multiple powerfull AESA radar systems that can be fully operated from ground stations if required.

Combined with the Global 650s long range, a compact but powerfull system, to be combined with Eurodrone (Which passed CDR a few weeks ago)

I have always believed the RAF made a big mistake choosing the B737NG platform for its MPA and AWACs solution. My reasoning ring the obsolete nature of the B737NG flight control architecture in a digital age.

In my view the Japanese Kawasaki P1 aircraft is a better platform first for the MPA role, and secondly I think the Wedgetail radar would be easier to integrate onto the P1 aircraft whose flight control architecture and avionics are fully digital.

The illusion of the B737NG airframe purchase price being cheaper than the P1 hides the additional cost of essentially adapting an analog system to carry a complex digital “payload”, and also adapting what is essentially an airliner to undertake roles that it was not designed for, especially in the MPA role. France with the A321 is going to have some of the same flight regime problems in the MPA role, but less so using the same aircraft in the AWACs because of the digital architecture of the A321 which makes plugging in a digital “payload” such as the wedgetail or Erieye radars and modifying the flight controls to account for the heavy aerodynamic disrupting loads on the “roof” less arduous/ complicated compared to the obsolete A737NG frame.

I stand to be corrected by experts in the forum.

KEESJE

Agreed. The 777x being to be certified using the old same as except concept (cert by similarity) is laughable today. How anyone caould say with a straight face …….. Here’s my new plastic wing with floppy wingtip mounted to a larger fuselage using the largest engines ever mounted on our airplanes with a new fbw system AND it’s SO SIMILAR to the old plane that I can use the certification by similarity process……… That’s amazing

So analyses and testing come in. Now doing that using an integral, top down approach when you are years down the similarity certification road and prototypes are build already..

This is interesting — and separate from the federal, criminal case currently under consideration by the court in Texas (which hasn’t yet ruled on the NPA between BA and the DoJ):

“Boeing Trial to Begin Monday in Chicago Federal District Court”

“Two of five designated cases are set for trial this Monday, Nov. 3, in the 2019 crash of a Boeing 737 MAX8 jet in Ethiopia. U.S. District Court Judge Jorge Alonso will be hearing two cases at a time before a jury of eight people.”

“Jury selection is scheduled to begin on Tuesday morning, and opening statements from all parties are expected to commence on Tuesday afternoon. The trial for all five of these victims’ families is expected to take about 10 days during the federal government shutdown.”

““Boeing accepted full responsibility for the senseless and preventable loss of these lives,” Clifford said. “We are determined to achieve justice for every one of them.””

https://eturbonews.com/boeing-trial-to-begin-monday-in-chicago-federal-district-court/

***

So, these are just the first 2 of 5 cases that will be prosecuted.

It’s worth noting that civil penalties in the US can reach into hundreds of millions of dollars per plaintiff.

Potentially far worse for BA will be all the dirty laundry exposed in the coming weeks.

Emergency damage control:

SF published this article a few weeks ago…and now it’s being published again.

One wonders who’s paying? 😉

“Why Might The World’s Most Advanced Long-Haul Widebody Airliner Have Airbus Worried?”

https://simpleflying.com/most-advanced-long-haul-widebody-airliner-airbus-concerned/

As reported by TAC:

> “acceleration plan to be ready to *roll out* [737 MAX] at 42 per month by the end of October”

Oh yeah?

It will be interesting to see how long that takes to actually materialize 😉

They still have to stabilize at rate 38…

This is the future?

AW:

> the B-21 will be crewed by one pilot and one weapon systems officer

For a flight of 36 hours?

============

AW:UK Lawmakers Unimpressed by F-35 Fighter Shortfalls

> The UK’s Public Accounts Committee says the UK Defense Ministry is being “complacent” in its approach to resolving issues with its Lockheed Martin F-35 force. In its report on the UK F-35 program, published Oct. 31, the lawmakers said the fleet “faces significant capability gaps.”

BA stonk fell 11% last five days.

Must be good news for traders.

CNBC:

> Retailers are raising prices to meet tariffs. Amazon is hiking more than others

> Taser maker Axon plunges 17% after earnings fall short due to tariff hit

Bloomberg

> “US companies announced the most job cuts for any October in more than two decades…”

I heard the economy is doing great. Oops.