Leeham News and Analysis

There's more to real news than a news release.

Boeing FY2025: Company posts small profit on Services division; BCA still losing money

By Karl Sinclair

Jan. 27, 2026, © Leeham News: The Boeing Company (BA) released its full-year 2025 results, and indications are that the company is headed in the right direction. However, some monumental tasks face the corporation in the short-to-medium term.

Jan. 27, 2026, © Leeham News: The Boeing Company (BA) released its full-year 2025 results, and indications are that the company is headed in the right direction. However, some monumental tasks face the corporation in the short-to-medium term.

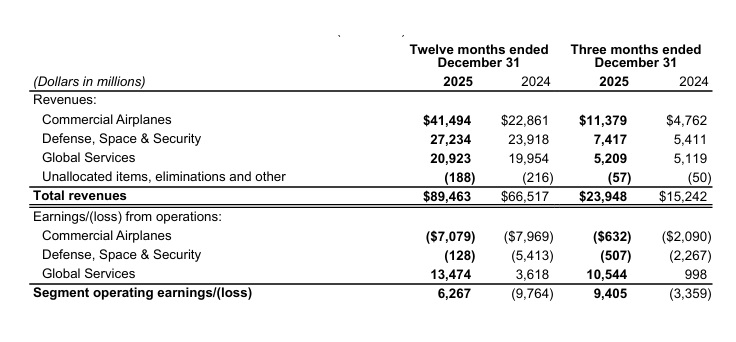

Boeing Commercial Aircraft (BCA) is still in a loss-making position. BCA lost $7bn, compared with $8bn in 2024. Boeing Defense, Space and Security (BDS) was near break-even. Boeing Global Services (BGS) was the only profitable division, boosting the corporation to an annual profit on the back of the $10.6bn sale of part of its business.

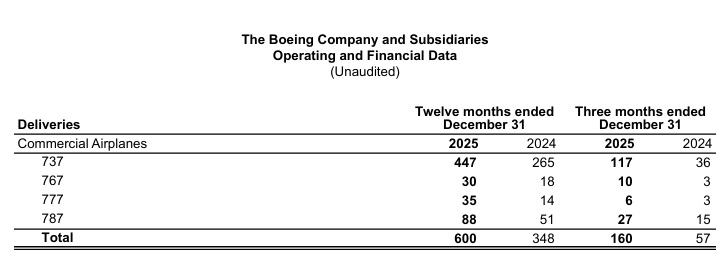

BCA delivered 160 aircraft during 4Q2025, including 117 of the cash-cow 737 MAX series and 27 Dreamliners.

This boosted BCA revenues in the final quarter to $11.379bn, up from $4,762bn, year-over-year (YoY). Full-year revenues hit $41.494bn, almost doubling 2024 sales of $22.861bn.

Source: All tables and images via Boeing.

The company is adamant about demonstrating stability in production and the supply chain at rate 42/mo, before making the leap to 47/mo by mid-2026.

787 rates are expected to stabilize at 8/mo, as investments in the Charleston (SC) production facilities begin to take shape, boosting output into the double digits in 2026.

Company-wide results

Strong results at BCA boosted revenues to $89.463bn, a whopping gain of $22.946bn over FY2024.

BDS also reported decent gains of $3.316bn, while BGS added $969m over last year.

Boeing earned $6.267bn in FY2025. However, this was bolstered by a $9.6bn gain on the spin-off of Jeppesen from BGS, which will undoubtedly reduce revenues at the division, moving forward.

Boeing earned $6.267bn in FY2025. However, this was bolstered by a $9.6bn gain on the spin-off of Jeppesen from BGS, which will undoubtedly reduce revenues at the division, moving forward.

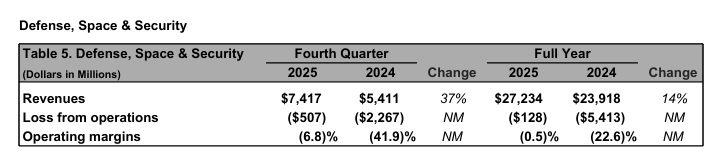

BDS essentially broke even in FY2025, a nice change from FY2024 when it cost the company $5.413bn. This includes a further $565m write-off on the KC-46 program, which CEO Kelly Ortberg termed “a bad contract for the last decade, this existing contract.” Boeing entered into the contract during the former CEO Jim McNerney’s tenure. Total write-offs now are more than $7bn.

BCA trimmed it losses from last year, but still is operating in the red, to the tune of $7.079bn.

The built-up inventory unwind is fairly complete, with aircraft requiring re-work down to one 737 MAX and a further five 787s from previous years’ production remaining.

As such, traveled work has been cut by a further 30%, with all Key Performance Indicators (KPI) in the green.

Boeing is looking to leverage significant investments in production facilities, most notably the new North production Line in Everett (WA) and the Charleston 787 assembly plant expansion, to produce its way back into the black.

Airplanes don’t make profits, do they?

Boeing CEO Kelly Ortberg.

On the FY2025 earnings call, CEO Ortberg was asked by Ron Epstein from Bank of America, “…it seems like on a very fundamental level that [OEM airframe manufacturing is] just not a very profitable industry…. It seems like everybody else is making money on planes from guys doing seats, faucets, engines, aftermarket parts. Can that change on a future airplane?”

Ortberg was diplomatic in his response, now having worked both sides of the Tier 1 and OEM equation. He replied, “I know how you can make a really good margin in this aerospace market. And I see how you can not make a very good margin in the aerospace market.”

This alludes to the critical investments in plant and manpower that Boeing is currently making, which were shunned by previous management teams. These capital injections into key components of the company will bear fruit over time.

However, there is also some cleaning up of the previous mess, which requires attention.

Boeing is carrying $54.1bn in consolidated debt, with significant payments coming due in the short-to-medium term, most notably a balloon payment of ~$8bn in 2026 to lenders.

Boeing is carrying $54.1bn in consolidated debt, with significant payments coming due in the short-to-medium term, most notably a balloon payment of ~$8bn in 2026 to lenders.

Interest and debt expense rose slightly to $2.771bn, up from $2.725bn in FY2024.

Operating cash flows rose during the year, a welcome sign, with additions to Charleston (787 program), Everett (737 program) and St. Louis (BDS programs) reducing that by $956m.

Operating cash flows rose during the year, a welcome sign, with additions to Charleston (787 program), Everett (737 program) and St. Louis (BDS programs) reducing that by $956m.

Management was pressed by analysts on free-cash-flow (FCF) expectations for the future.

Projections but no guidance

Boeing CFO Jay Malave.

CFO Jay Malave was upbeat about projections, despite some short-term headwinds that need to be addressed. He elaborated:

“2026 is a big, big year for us, as Kelly mentioned. We have to get through our certification programs. We also have rate ramp increases as well…I went through this in the fourth quarter, and I’m very comfortable with our ability to achieve $10bn (in FCF). Again, it’s a little bit of a repeatable sequence of events, but we have to get through the certification programs. We have to ramp up on our BCA production rates. We need to see the improving performance at BDS related to our margin profile as well as burning off the prior charges, and in continued performance at BGS.”

Segment Analysis

BCA

Boeing Commercial has a lot on its plate in 2026.

Chief amongst the tasks is ensuring that the 737 MAX 7 and 10 variants get certified and into service with airlines during the year. Built up inventory on those types remains at around 35 units. The Max 10 is currently going through expanded flight testing, granted by the FAA with TIA-2, with a permanent design fix completed on the engine cowling issue. The reintegration of Spirit Aerosystems into the Boeing family will cost the company ~$1bn, but will also bear fruit in the future.

The 787 program is expected to hit rate 10/mo in 2026, which is the maximum capacity with the existing infrastructure. However, management expects no supply-chain constraints with the program on the ramp-up.

Touched upon in the earnings call was the short-term burn off of customer compensated aircraft, also a leftover from previous management, which will affect cash flows moving forward.

The 777-9 is still expected to receive certification in 2027, with durability issues on the General Electric GE9X engines identified. The program continues with TIA-3 testing ongoing, which involves the engines, avionics, and CPU.

The cost is estimated to be ~$3.5bn spent on the 777X program, with a drag on FCF expected to continue until 2029.

All of this is ongoing, as the company ramps up from rate 42/mo on the 737 program to 47 by mid-year. A good portion of the ramp-up will be borne by higher-than-normal inventory levels, which will aid suppliers in getting accustomed to the new rates.

Moving beyond 42 to 47/mo will be a bigger endeavour.

Increasing Production

Ortberg detailed the production horizon:

“[The] Supply chain on that ramp [is] not a big issue for us right now, and we projected that. As you know, we’ve got a lot of inventory there. I actually don’t think supply chain is going to be a big challenge for us in the next rate ramp from 42 to 47. But that’s where we start to normalize with the supply base in terms of burning off the excess inventory. As we’ve said, going from 47 to 52 will be where we’ll have to see improved performance from the supply chain. We’ve got time. We’re working that diligently with the supply chain.”

It seems as though the relationship is much improved in the supply chain, as Boeing works with its suppliers, with little mention of the previous “Partnering for Success” program.

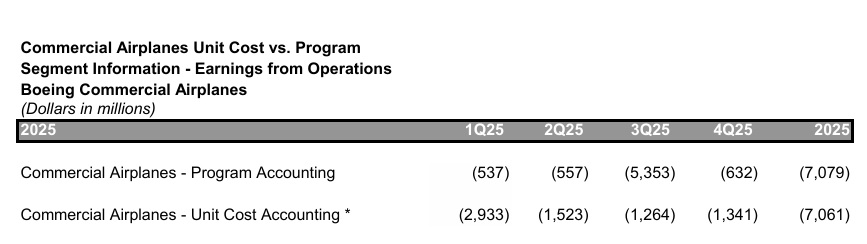

In 3Q2025, Boeing took a $4.9bn charge against the 777X program, which had the net effect of increasing the Program Accounting loss from ~$2.2bn to $7.079bn for FY2025.

In 3Q2025, Boeing took a $4.9bn charge against the 777X program, which had the net effect of increasing the Program Accounting loss from ~$2.2bn to $7.079bn for FY2025.

This brings it in line and mirrors the unit-cost accounting loss figures for the year. In order for the division to contribute positive results to the company, it is imperative that the unit-cost numbers reach positive integers moving forward. It is unclear if that will happen in 2026.

BDS

Boeing Defense made some positive strides during the quarter, yet was held back by another write-off on the KC-46 program.

This time around, it cost the company $565m, as total losses on the program began to reach double-figures. This has been offset by another order for 15 tankers, as the company hopes to put those losses in its rear-view mirror.

Crucially, the company has signed an agreement with the IAM union local in St. Louis (MO) and will avoid any work stoppages there with labor peace in place for the next five years.

Crucially, the company has signed an agreement with the IAM union local in St. Louis (MO) and will avoid any work stoppages there with labor peace in place for the next five years.

BDS revenues were up 7% over FY2024, to $19.817bn, and generated a modest margin of 1.9% or $379m, a welcome change over the $3.146bn loss of the previous year.

The KC-46 write-off was detailed as a “discrete charge,” specific to the program and indicative of higher production costs associated with the 767 commercial aircraft, on which the tanker is based.

Once again, management is going to produce its way into positive territory, as it projects to deliver 19 tankers in 2026, versus 14 in FY2025.

A highlight for BDS during the year was the first operational delivery of the T-7A Red Hawk to the US Air Force at Joint Base San Antonio-Randolph. A welcome indicator that revenue streams will begin on another Boeing defense program.

BGS

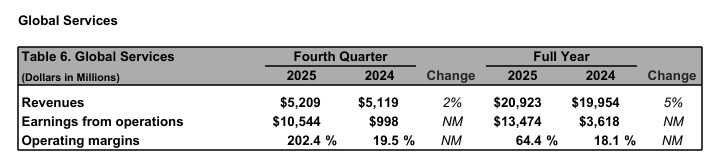

While the news is normally quite subdued at Global Services as it quietly goes about generating ever-increasing revenues and margins quarter after quarter, a portion of the division was sold, which added a net $9.6bn to Boeing’s coffers. The Digital Aviation Solutions transaction did not immediately impact revenues in FY2025.

This would naturally be expected to change in 2026, as the loss in expected revenues begins to take hold. Earnings and margins were outsized for the year, as the profits from the one-time transaction were realized. Sales in FY2025 were up 5%, over FY2024 – which mirrors previous results of a 4% gain, YoY:

This would naturally be expected to change in 2026, as the loss in expected revenues begins to take hold. Earnings and margins were outsized for the year, as the profits from the one-time transaction were realized. Sales in FY2025 were up 5%, over FY2024 – which mirrors previous results of a 4% gain, YoY:

If the $9.6bn gain is removed from the equation, BGS still earned ~$3.874bn during the year, versus $3.618bn in FY2024.

The Boeing management team seems to have focused on what tasks need to be accomplished to get the underperforming divisions back into positive financial territory, while making difficult financial decisions with divestitures to bolster the balance sheet.

Those EIS dates for the Boeing 777-X seem to continue to slip: now the reporting here is *certification* in 2027, not EIS as previously (recently) reported.

Corrections welcomed.

That may be an LNA typo.

The BA earnings report says:

“In the quarter, the 777X program began the Type Inspection Authorization 3 phase of 777-9 certification flight testing, and the company still anticipates first delivery in 2027.”

https://investors.boeing.com/investors/news/press-release-details/2026/Boeing-Reports-Fourth-Quarter-Results/default.aspx

No worries. It doesn’t seem the engine is meeting customer airlines’ expectations.

“… durability issues on the General Electric GE9X engines identified.”

GE needs more time to make sure its engine works as promised.

Are we going to hear from TC in the very near future?

There’s no mention of Jeppesen in the earnings press release. Without the sale, it’s another year of losing money and cash burn. Go figure.

If TC is dissatisfied he will order A350-1000.

TC has too much customer compensation to spend! That’s why he keeps ordering!

The delay for this program is just crazy. 7 years. Will also lower lifetime sales of the program.

In the quote above (and herebelow), CFO Jay Malave shows us how one can use lots and lots of words…and, yet, say absolutely nothing:

“2026 is a big, big year for us, as Kelly mentioned. We have to get through our certification programs. We also have rate ramp increases as well…I went through this in the fourth quarter, and I’m very comfortable with our ability to achieve $10bn (in FCF). Again, it’s a little bit of a repeatable sequence of events, but we have to get through the certification programs. We have to ramp up on our BCA production rates. We need to see the improving performance at BDS related to our margin profile as well as burning off the prior charges, and in continued performance at BGS.”

===

Note how often he says “we have to” or “we need to”. Those are just rote expressions of (obvious) goals.

Listening to meaningless, off-the-cuff goals has become tiring.

[Deleted as a violation of Reader Comment rules.]

Show us, don’t tell us.

Kind of like Airbus focusing on production increases.

The first step in a 1`2 step program is recognizing your problem

Boeing is several steps into recovery but we all know its going to take many years. Once Boeing is recovered, we will still get the complaints.

One guy I worked with was spot on with the Company issues. He ignored the fact that he too had issues he should have addressed.

Being at the pointy end of the spear and making things work is not like calling a Uber.

Abalone – good point!

If we go back on the way back meter one year ago Jan 2025 then CFO Brian West said the same “we have to, we need to” conjecture.

Meet the new boss, same as the old boss.

Cash burn for the year would have been even worse were it not for some “flexible” bookkeeping: there was a significant increase in accounts payable and accrued liabilities — to the tune of about $4.8B.

A well-worn windowdressing trick.

After all his negative sentiment toward the XWB-97 engine on the A350-1000, Tim Clark will surely be thrilled to read this:

“Boeing discovers new durability issue affecting 777-9’s GE9X turbofans”

https://www.flightglobal.com/engines/boeing-discovers-new-durability-issue-affecting-777-9s-ge9x-turbofans/166086.article

Each of these new engine generations pushes the technology to its limits and none are problem free, some worse than others. If/when they get the 9X sorted out it will likely be a long time before the next big one from GE.

The next generation in big engines is the RR ultrafan. It too will likely have issues but like the P&W GTF probably not with the gearbox.

Sure.

But TC has been acting as if the GE9X is perfect compared to the XWB-97.

Cold shower for him now.

First run for GE9X was in April 2016. First run for Trent XWB-97 was in July 2016.

The difference is about 100 A350-1000 run under real conditions on a daily base revealing real world problems.

So, as a variant of “no news, is good news”, TC seems to be a fan of “no data, is good data”.

That will work out well 👀

We don’t know what goes on behind the scenes- of which there is likely to be plenty.

Pretty sure this isn’t Sir Tim’s first rodeo, if you know what I mean.

@Dan Fuller”

Spot on. The GenX shed blades as well as the Ice Up issue (which I wonder was part of Climate change). It took two PIPS and then unofficially PIPS to get the burn rate up to spec (its now above the contract numbers))

The GP7000 had a bolt break due to Hydrogen Embritlement. HE is a well known phenomena. It had never occurred in that application.

DF is exactly right that no testing duplicates real world operations (and then it can take some time for it to manifest though some like the GE Auto Turbine shed took place almost immediately.

The Trent 1000 is bad enough that RR ran themselves out of that 787 market making the 787 a one engine aircraft.

How GE9X does in actual service we have to wait and see.

The key word used is “durability” and not “reliability”.

That implies something that is not necessarily a safety concern but more of an early wear out. The obvious candidates are premature turbine blade or combuster wear.

The issue with the XWB-97 is also one of “durability” rather than “reliability”…

Yep. The Thrust Strut would be a safety of flight issue (see the MD-11 Pylon shed)

Thrust strut was a Boeing engineer and build item;

I did note that FG got its data wrong. 13 Meters is not 10 feet (3 meters at a guess, close enough).

“13m (10ft)-long titanium devices that transfer thrust from engines to airframes.”

Bodes well for TC’s 777-10 😁

It’s crazy that on both the FG piece and another one I came across are written as if BA had finally turned a profit without mentioning that’s only because BA made a profit like $9.6 billion from selling Jeppesen.

On the front page of FG web site:

Why engine reliability really matters for Asia-Pacific airlines

Paid content by GE Aerospace

I’m not making this up.

============

In other news:

https://www.flightglobal.com/engines/honeywell-settles-flexjet-engine-maintenance-dispute-after-warning-of-470m-hit/166022.article

https://www.flightglobal.com/engines/airbus-closes-on-key-milestones-for-a380-flying-testbed-as-companion-project-nears-design-freeze/166018.article

Doesn’t surprise me at all.

CNBC constantly pushes a (paid?) selective narrative on all sorts of fronts — financial, commercial, economic, political.

We’re back to the 2007 landscape, in which analysts, ratings agencies and news outlets are in other peoples’ pockets…

FG:

“This agreement places supplier accountability at center stage, and we hope it further unites the industry around a matter essential to private aviation operators both large and small,” Flexjet says. “With a *value surpassing a billion dollars* in cash considerations and service credits, it sets a powerful precedent for businesses seeking to correct similar supplier transgressions.”

“Our hope is that the litigation, and now agreement, serve as a case study reinforcing the importance of supplier relationships built on authentic commitment, principled conduct and consistent delivery,” Flexjet adds.

The latest Q4 charge on the KC-46A program now brings the total loss on that program to $7B…

“Boeing has now lost more than $7 billion on fixed-price contract for the KC-46, which CEO Kelly Ortberg acknowledged has been a “bad contract for the last decade.””

https://www.airandspaceforces.com/boeing-takes-first-kc-46-charge-since-2024/

I wonder how AF1 is doing

It’s $565M for the 4th quarter of 2025.

https://www.defensenews.com/air/2026/01/27/boeing-reports-565m-loss-on-kc-46-as-firm-looks-forward-to-repricing/

From the article

“This has been a bad contract for the last decade,” Ortberg said. “As we enter into a new opportunity where we get to reprice, we want to make sure that we ensure it’s a fair contract and we can make money.”

Boeing offered a low price in the first place to win the contract. Maybe USAF could look for a better aircraft to keep the price fair: MRTTneo.

BA executives worked too hard at “winning” orders! They have to be incentivized to make real money.

“Boeing has now lost more than $7 billion on fixed-price contract for the KC-46…”

More record-setting achievement.

BDS has delivered a total of about 100 KC-46A!

While Boeing probably means the Adamant about steady production before the next rate increase, its the FAA they have to convince they are.

Boeing can ask but it is not their decision.

Good comments, Abalone!

Boeing is trending in the right direction finally. Many hurdles to jump through though before that balance sheet goes positive.

“BCA delivered 160 aircraft during 4Q2025, including 117 of the cash-cow 737 MAX series and 27 Dreamliners”.

Cash cow? That used to be the case before the mad Max accidents in 2018. Not so much anymore.

IMHO divesting the BGS Jeppensen unit was a big mistake, the Foreflight app alone was worth it. Everyone uses it…. That’s a cash cow.

Will Boeing Wichita, formerly Spirit be worth it? Other than maybe they can control the quality aspects.

Onward and upward.

The MAX and 787 are what generates revenue and are the only two programs that can contribute to BCA recovery. The 787 is a mature program and is selling loads (very technial term).

Regardless of labels, MAX and 787 are Boeing cash cows.

No idea what Jepppensen generated a year but that is a business decision on how it fits and what you can get for it selling it. GE more than proved being spread all over is not a good thing. They did get more for it than the pundits had said they would.

I am surprised that Boeing has not divested other entities though that may be in the works. Satellites are not aircraft nor are rockets.

Helicopters are only two models in two different places. Huge sellers so that would be the same assessments as Jeppensen.

Spirit gets Boeing nothing a good contract to Spirit would not have. Having lived inside that same model of sub contracting, it does not work. You have to pay Spirit in this case more than it would cost you to do the same yourself.

My old company is gone (too late for my benefit) the company that hired them finally figured out that it was costing them and folded it back into their structure.

What happens is the main company management pushes to low cost to save money. The only way the separate company can make money is to go cheap. So they drop the very quality they need to do the job per contract.

The sales spin for outsource is saving money. When both companies need to make profits, then done right its going to cost you money. Its possible that its worth it but not on the basis of saving money.

The one I saw work for the employees was when the contract had to be union. The Main Company lost money hand over fist, the employees were rolling in the dough (which they deserved, it was high skill work).

Boeing will now have to manage the former Spirit on the same basis as their other facilities and employees. They won’t save money and it will cost them money to get back to what is needed (ask Airbus how things are going with their portion!)

Not having to save money to justify things, Boeing will work the quality to the same level as their other facilitates and overall it adds to the benefit of Boeing and saves headaches long term as they still wound up managing Spirit like one of their own facilities.

You don’t hear anything on the 787 nose so I wonder if Spirit did strike a good deal on that?

“Cash cow? That used to be the case before the mad Max accidents in 2018. Not so much anymore.”

Exactly. The only cash cow is Jeppesen, not the 737 MAX or 787 that some repeatedly bring up. How many family heirlooms can BA afford to let go to sustain it?

The sale proceeds ($9.6 bill) helped increase Boeing’s cash reserves to nearly $30 billion by the start of 2026.

Most of Jeppesen gone servicong the 2026 knock on the door……….

“Boeing is carrying $54.1bn in consolidated debt, with significant payments coming due in the short-to-medium term, most notably a balloon payment of ~$8bn in 2026 to lenders”

Loans can be rolled over when due. Its called corporate finance, even the federal government does that.

$54 bill isnt that much compared to other large manufacturing companies . Its the credit rating that matter most- which is still investment grade and the order backlog is growing

Ford Motor Company: ~$135B+ (High debt due to Ford Credit financing operations)

General Motors: ~$115B+ (Includes substantial GM Financial automotive debt)

Dell Technologies: ~$95.47B

General Electric (GE): ~$18.81B (Following major deleveraging and corporate splits)

Honeywell International: ~$27.14B

ExxonMobil: ~$43.5B (Gross debt as of Jan 2026 reporting)

John Deere (Deere & Co.): ~$48.05B

Boeing: ~$50B+

Just a little over a year ago and now no one remembers?

> Boeing would be biggest-ever US ‘fallen angel’ if cut to junk

> Boeing at Risk of Junk Rating With S&P

There are serious implications in case BA’s debts became junk, its customers may have to consider provision for their PDPs. Lol.

@Duke

Which of those on your list was at risk of being downgraded to junk barely a year ago? I can only think of one.

Ford’s debts mostly come from auto financing it provides to dealers and customers (secured by automobiles), unlike BA. That’s why it’s irrelevant to compare with F or GM. It’s an elementary-level mistake. Don’t kid me.

It’s not just debt that matters — one also needs to consider debt servicing costs, which are determined by the interest rates applicable to the debt (in BA’s case, those are high).

One also needs to consider whether the debt holder is generating a profit or not (BA isn’t), which determines ability to ultimately pay off debt.

And, of course, one needs to look at the debt-to-equity ratio — which is extremely high in BA’s case.

As regards debt rollovers: not an attractive option when the interest rate on the new debt is (much) higher than the rate on the old debt.

@Duke:

I find it a shocking amount though with the 787, MAX and 777X issues, not at all surprising.

It does seem like a lot when Boeing was on the edge of Bankruptcy, but then I am not a big business guy nor a financial expert.

I heartily agree you have a far deeper insight into the finance end than I do. I would like to see other financial guys weigh in for a balanced view.

I don’t know if the companies you list are actually the same debt aspect relationship to Boeing’s debt.

The 54 Billion is not a surprise for what Boeing went through but it does not look at all normal.

Sum of BA’s cash, cash equivalents and short term investments per:

Dec 31, 2024: $26,282B

Dec 31, 2025: $29,400B

That’s an increase of only $3,118B.

In other words: most of the Jeppesen sale proceeds were swallowed in covering cashburn during 2025.

And, if one factors in the fact that cashflow was dressed-up by allowing accounts payable and accrued liabilities to increase by $4.8B, then one sees that the *entirety* of the Jepppesen sale proceeds were swallowed in cashburn.

There was some interesting news in this issue of Airforces. The KC46 breaks off booms with far too much regularity. They illustrated 3 instances of the receiver aircraft getting out of phase with the tanker and running the boom body into the bottom of the fuselage, breaking the boom and damaging the lower fuselage. Apparently, it’s a fairly big issue as it is a class A incident and one was reported to take 14 million to repair.

We hear almost nothing of the Small Diameter Bomb, JDAM tail kits, Chinook remanufacturing or Apache follow Ons. It used to be that these cost + fixed fee programs were golden. One would expect BDS is quietly losing its ass on the tanker and using these solid programs to fund the shortfalls.

ALSO. Where is any reference to the loss leading AirForce 1. Funny that vanished from the reporting as did any reference to F15, F18 program earnings or B2 sustainment income. Something looks suspect here. We have to be selling huge spares to the navy and to a lesser extent the Marines and AF for spares and attrition aircraft. They lost 2 Growlers we know of and perhaps 5 to 12 total, as its hard to pin it down. F15s possibly 6

Lots to question, and perhaps when these endless cash drains stop, the company wont need to be as slimy in how they report things. I cant see how BDS can be delivering all this stuff and still be showing virtually nothing in return unless they are on the serious short end of the fixed fee schedule.

It will be interesting to see what Boeing gets for the next Tranch of KC-46A (or will it be a B by then?) While the USAF can try to extend the original contract, Boeing does not have to sign on.

That is where you see if long term they could make money on the program or not by what the next contract says.

Boom breaks are an assessment of what mechanism is causing it and I have not heard what that result is. Regardless the inflation adder clauses will be kicked in full throttle, so Trump is shooting us in the foot there as well.

Boeing does have to adhere to accounting rules, so that info is in there someplace.

The Navy is going to have to buck up for a bridge order of FA-18, they don’t have enough fighters and don’t want the F-35C. Its not just the F/A-18 losses, its the retirements on old airframes that exceed any losses by some magnitude.

AF1 is back on the slow burner, El Presidente got his AF1 from his buddies in Qatar!

” While the USAF can try to extend the original contract, Boeing does not have to sign on.”

The USAF can also walk away. Maybe USAF makes a deal with AirTanker Services Limited while running KC-Y?

“While the USAF can try to extend the original contract, Boeing does not have to sign on.”

Since this didn’t happen, it is more a pipe dream bubbled up.

BTW last I checked, the Pentagon slashed its order of the F-35 by 45%. Another moment of spewing my coffee Lmao.

@MHalblaub:

No, they are going to try to extend the contract. Walking away is not an option.

100% is the enemy of having something vs nothing.

KC-46A is at least an 85% solution. Vs nothing. US needs more conventional tankers not fewer.

So no, the USAF is not going to walk and it defies all logic to portend they would.

As for the boom, the reasons I brought up mechanism, the boom is stiff per a USAF spec Boeing met (not all KC-46A problems are Boeing caused).

The US not only has far more tankers than the entire world combine, wazah, they also fuel more. Aircrat damaging booms does happen and its got nothing to do with the booms.

We need two facts.

1. What is the rate of boom damage in vs total tanks?

2. What was the mechanism of failure?

Non sequitur.

” While the USAF can try to extend the original contract, Boeing does not have to sign on.”

I thought what you meant is BA can walk away, not the other way round!! 🤣

Which types of USAF aircraft the RAAF KC-30A is not allowed to refuel? (“100% is the enemy of having something vs nothing.”)

Why are there no 737NG tanker aircraft? Airbus could offer now an A321XLR tanker.

Can someone provide data about the use of KC-46? How many flying hours are for refuelling and how many hours are for other missions like cargo? Maybe USAF should use this data for the next competition.

There is no such creature as a KC-30, the comment makes no sense.

The RAAF tankers can not refuel any USAF aircraft, they are all boom receptacle types.

They can refuel all USN aircraft.

A Single Aisle tanker does not have enough off load capacity to make it remotely worth it.

Squint a bit and maybe a drogue type would have some use. Tanking tends to be larger amounts for a group of fighters or lots of fuel for a C-5 or C-17.

USAF will have its internal records on what the KC-46A is being used for. You can be sure its vastly biased to tanking. The US does not use its tankers heavily in the freighter business, it has other and better options for freight and it does not have enough tankers.

MHalblaub is correct in his statement. The Australian KC30A has a boom and can, and has, refueled ALL USAF aircraft. You forget that the RAAF has F35A as it current primary combat aircraft and therefore made provision for boom capable refueling on its tanker. See picture in link provided

https://www.af.mil/News/Photos/igphoto/2001296618/

Trans Wrote

A Single Aisle tanker does not have enough off load capacity to make it remotely worth it.

Squint a bit and maybe a drogue type would have some use. Tanking tends to be larger amounts for a group of fighters or lots of fuel for a C-5 or C-17.

My Friend. You are missing the fact that 2 “single aisle” Tankers are currently in service. The Lockeed KC-130 and the Embraer KC390. Lockeed has made close to 200 c130 based tankers and the KC130J, fleet is at 79 aircraft for the Marine Corp alone, there are 18 export customers ovet the history of the program. The KC390 is going to Brazil, Portugal, Sweden and Hungary, so far, Israel is sniffing around for local theater ops for rotary wing gas to replace their 130s Bedek built. The Marines would like to acquire the KC390 to replace the KC130. There is a BIG need for Theater sized Gas Passers to keep smaller strike packages fueled by smaller players, Remember how many Blackhawks have probes and how many smaller operators of refuelable aircraft are out there

Trans

“A Single Aisle tanker does not have enough off load capacity to make it remotely worth it.”

Exactly! BA sold like 800 nevertheless! It must be the “scam” of the century. And the USAF will continue to fly them well into the 2040s! Another great start of the day. [Edited.]

I thought F/A-18 was close to termination. In fact it is, no more F/A-18.

https://www.twz.com/air/last-new-f-a-18-aft-fuselages-built-as-super-hornet-production-end-approaches

I guess USN has to start taking F-35C

Trans.

Im expecting a bridge purchase to occur. The naval F35 sux, the Navy knows it and they are flying the F18 fleet in excess of plan consuming airframe life faster than replacements are scheduled to appear

Cash cows. We have to wait for the 2025 annual report in 1 months time for the detailed data on the various BCA product lines.

Does not matter. They are still Boeing BCA revenue generators.

The input is short term exceeded by the output to add mfg for both, Charleston expansion, Spirit buy out, Everett line build.

Now the excess inventory has mostly gone but BA is still stuck with $54 billion of debts. The myth of “investory is as good as cash”! Another one that can’t survive the reality test.

777X (35) and 787 (around 5) excess inventory remains

the Max 7 and Max 10 still in inventory is said to be around 30

The normal use of ‘inventory is as good as cash’ is for the planes that are certified and built for a customer and rolled out but delayed delivery ( and payment) short term for some reason. could be financing issues, or engines or cabins etc

How many months and years did BA take to clear its excess “planes that are certified and built for a customer and rolled out but delayed delivery” after the 737 MAX was grounded??

Apparently you underestimated the damage caused by building up the excess inventory in the first place. Of course, BA’s fake FCF would pop when BA’s “FCF” is built on delayed payments to its suppliers, That’s why BA was so reluctant to lower its production.

Thats irrelevant and past history. [Edited]

Your claim of ‘no more’ excess inventory isnt matched to the actual numbers I quoted.

Those planes stored during Max grounded included 120 or so that after much huffing and puffing were eventually taken by the original customers

1. Those aren’t “excess inventory”.

2. BA has another write-down of its 777X inventory. Anyone who went thru BA’s earning releases can remember that. How much cost of the 777X is carried on BA’s book, [Edited]?

3. [Edited] 😀

@Duke:

The excess build up is almost gone so for all practical purposes, it is no longer relevant.

Pre builds are not excess inventory. It may look the same but the financial aspects and status are totally different.

They have a liability aspect as they may well need to have changes implemented. We know the -7 and -10 will need program changes as well as new inlet cowls.

It will not be as bad as the 787 fixes, but its also not nothing. 777X may be pretty well off but all of those will be finalized status when their respective programs are finalize and we get the data for when they will be cleared from inventory.

The 777X and Max 7 & 10 are ‘undeliverable’ inventory until the certifications are done

Theres the normal month by month inventory of course that have been rolled out and are on course to be delivered to the order customer

Airbus might have 60 planes in inventory at any time, plus some airframes like A350F which isn’t certified- and seems to have struck issues with the cargo door design

Boeing hasnt written down 777X that have been built, it was recorded as deferred production costs

Go back to Q3 2024, the deferred production cost of the 777X was fully written off to zero. A big zero! Another $5 billion was written off in 2025. Anyone who read BA’s 10Q/10K would be aware of these major items.

See this chart from LNA:

https://leehamnews.com/wp-content/uploads/2025/02/BA-Customer-Comp-12-31-24.jpg

Notice the deferred production costs of the 777x program as of December 31, 2024: zero. A big, fat zero.

Without the sale of Jeppessen, BA would have suffered cash burn over $10 billion in FCF! Cash cows? What cash cows?

Isn’t FCF king?

GEN9X:

For those who used up their access limit to Flight Global, this should get you the article.

https://archive.ph/qeGsp

Ackhually Alaska placed the massive 737 & 787 order with BA in Q4 2025, not January 2026!

Everyone is tricked.

Does it really matter?

Its a nice order for Boeing and goes to future producible and revenues which is what counts.

Truth matters, in my opinion.

Announcement was Jan 7. But Boeing has included the numbers/airline in 2025 calendar year

Alaska now has a new livery – Northern Lights- replacing the Eskimo

Yea, not going to make Alaskans happy. AK forced Alaska Airlines to retreat once before on the Logo thing.

Me, shrug. The NL thing is a bit glitzy and they will keep the Inupiat Logo (which would be correct for Northern Alaska Indigenous peoples – note some of their preseences wraps around on the Alaska West Coast ) .

Eskimo is wrong. There are a number of Northern Indigenous groups, Eskimo is a contrived word we try to avoid out of respect.

Kind of like referring to Scots as British. Out come the Claymores.

on another note…here we go again!

article title “Trump says he’s decertifying Canada-made aircraft and threatens 50% tariffs”

“It would be a transportation disaster,” Aboulafia said. “If it’s only the Global Express, it’s not that big of a problem. But if it’s all Canadian-made jets … the (US air travel) system would be seriously impacted.”

https://www.cnn.com/2026/01/29/business/trump-canada-aircraft-tariff

remind again, why would China put in a new order for Boeing aircraft?

Maybe Canada has a point about Gulfstream aircraft the FAA didn’t caught. It already happened with a Boeing model. Therefore other regulators are more consciousness or woke about FAA certifications.

The threat of doing harm to yourself should not be underestimated. On the other side the Gripen is now a flight hour closer to Canada.

See my de-icing comment below.

We’re all living in an interesting time!

> FR24: There are currently more than 400 Canadian made aircraft operating to/from a US airport right now. [Last evening]

> The team from @theaircurrent is seeking more information on this statement from the President. A massive amount of the U.S. fleet of mainline, regional, helicopter and military aircraft are “made in Canada.”

https://x.com/jonostrower/status/2017032007415714046

> Rasmus Jarlov, a prominent Danish Member of Parliament and chair of the defence committee, expressed regret over Denmark’s decision to purchase F-35 fighter jets, citing security risks and potential,U.S. leverage.

I guess many would underestimate the long-term consequences of such an act, whether Trump’s wish is fulfilled or not. Look back in two or three decades, or maybe as short as ten, or fifteen years:

We’d better understand why Trump did what he did (is it tantrum over anxiety about America’s decline?), and the consequences.

Today, it’s Greenland and Canada, which countries will be the target tomorrow?? It’s mask off.

That person may be the best “agent” Putin could buy and his grandkids are learning Chinese.

Is it true that the Gulfstream G700 and G800 havent even been certified by FAA in regard to fuel icing. They were given temporary exemption by FAA in 2024 and required to demonstrate compliance by end 2026?

What exactly are “world recognized Certification standards” being peddled by some here?? 😂

“This is too much winning. We can’t take it any more”

“Trump’s ‘Bombardier War’ Threatens To Sink 14.2B F-35 Deal; Will Canada Pull the Plug on U.S. Stealth Jets?”

“The Swedish defence giant SAAB has offered 72 Gripen E/F fighter jets and 6 GlobalEye surveillance aircraft to the Canadian Armed Forces, which would generate thousands of jobs in the country, as EurAsian Times recently reported.

“The big question remains: will US-Canada tensions sink the F-35 deal, worth a whopping $14.2 Billion?”

https://www.eurasiantimes.com/trumps-bombardier-war-threatens-to-sink-14-2b-f-35-deal-will-canada-pull-the-plug-on-u-s-stealth-jets/

===

Meanwhile:

“Rasmus Jarlov, head of the Danish parliament’s defence committee, has voiced his concerns about that country’s decision to have the F-35 as its only operational fighter jet. Those concerns have only increased as the Trump administration recently threatened Denmark and talked about seizing control of Greenland from the NATO nation.

“In his interview with CBC, Jarlov had a message for Canada about the F-35: “Choose another fighter jet.”

“They’re in for repairs about half the time or even more,” Jarlov said. “The Americans have all the power of actually destroying our air force just by shutting down (parts) supplies.”

https://ottawacitizen.com/public-service/defence-watch/us-ambassador-canada-f35-order#:~:text=Rasmus%20Jarlov%2C%20head%20of%20the,down%20(parts)%20supplies.%E2%80%9D

TACO is the answer to that. Too many are credulous over anything Trump says- well what his ventriloquists say as Trump wouldn’t know anything about planes origins

from another article…more info

“”Based on the fact that Canada has wrongfully, illegally, and steadfastly refused to certify the Gulfstream 500, 600, 700, and 800 Jets, one of the greatest, most technologically advanced airplanes ever made, we are hereby decertifying their Bombardier Global Expresses, and all Aircraft made in Canada, until such time as Gulfstream, a Great American Company, is fully certified, as it should have been many years ago,” Trump railed.”

from Flight Global in 2024

“The Federal Aviation Administration has temporarily exempted Gulfstream’s in-testing G700 and G800 business jets from certain fuel-icing airworthiness rules, seemingly bringing the company one step closer to achieving the jets’ certification.”

“A three-year exemption issued by the FAA on 17 January means the agency can certificate both the G700 and G800 – and Gulfstream can start delivering them, and customers can start operating them – despite the jets not complying initially with some fuel-icing rules.”

https://www.flightglobal.com/airframers/faa-exempts-g700-and-g800-from-fuel-icing-certification-rules/156570.article

Gulfstream needs to get its de-icing systems in order, and stop looking for exemptions (like Boeing):

“Gulfstream’s newest models have yet to be certified in Canada due to tests still pending on a crucial fuel icing system. In the US, the Federal Aviation Administration gave Gulfstream a time-limited exemption on the G700 and G800 models until the end of 2026, allowing the planemaker to deliver the model to customers even as tests are done to ensure the fuel system is safe from tiny droplets of water freezing and blocking flow of fuel to the engines.

“The planemaker had previously sought to use the certification of its older models as the basis for the analysis that was safe. But it was later determined that because of changes in the routing of the system, fresh testing was required. Canada hasn’t granted a similar exemption, delaying certification of those models.”

https://finance.yahoo.com/news/trump-threatens-decertify-levy-tariff-042840400.html

While we are pointing fingers, we should look at two other jets that have been inflicted on the US.

Challenger that went down in Bangor Maine that has an extraordinarily picky wing (high speed don’t you know rules all). It has no latitude for even a bug on it before it stalls. Funny how the real world has water, snow, ice and bugs.

The other is the Hawker Bussiness jet that has killed two crews in the last year due to mandatory flight testing.

Another picky design that if you touch the leading slats, you have to do a full stall re-certification.

What has been left out is how dangerous that is and that it should be flown by an experienced test crew, not line pilots.

In other news:

Airbus to start sales drive for larger A220 jet, sources say

Estimating without too much pressure there could be 400-500 orders. More if they do a simple stretch with the same wing;

And also offered a 4th length with an updated wing.

Both options with a choice of either of 2 engines.

So Lufthansa isn’t about to retire their A380s anytime soon?

> BREAKING Lufthansa introduces refurbished #A380 with new C Class Thomson seats in 1-2-1 config from April

https://x.com/SpaethFlies/status/2017191418989539487

[Oh I’m repeating what I said before: would the A380 outlasts the 747-8 in passenger service? 😄 ]

Is not AF-1 carrying passengers?

The one flying is not a 747-8. Okay let me change that to commercial passenger services.

@All

Comparing the A380 to the 747-8P is not going to end well.

I could only find where 36 747-8 were ever delivered for commercial service (LHT / Air China / Korea). The 747-8 was an even worse disaster than the A380 in sales.

Edit: outlast*

> A couple of weeks ago the NTSB issued an update on the UPS MD11 crash and I wanted to use the graphs of flight data in a visualization combined with the ADS-B data and surveilance videos. This is what I ended up with, one hard part about this is the flight is so close to the ground the viewpoint needs to account for the pitch of the aircraft raising and lowering the cockpit.

https://x.com/DJSnM/status/2016025651049103706

let’s not forget about Embraer

article title Embraer and Adani partner on Indian manufacturing facility

“The planned manufacturing facility, along supporting operations including development of supply chain, aftermarket services and pilot training, aims to tap into India’s travel boom, reports Reuters.”

https://macaonews.org/news/lusofonia/embraer-adani-india/

info from Wiki

“Adani Enterprises Limited (AEL) is an Indian multinational publicly listed holding company and a part of Adani Group. It is headquartered in Ahmedabad and primarily involved in mining and trading of coal and iron ore. Through its various subsidiaries, it also has business interests in airport operations, edible oils, road, rail and water infrastructure, data centers, and solar manufacturing, among others.”

My guess, this venture go no further MOU…bad choice by Embraer

US aluminum prices surge above those in overseas.

“This is too much winning. We can’t take it any more”

https://pbs.twimg.com/media/G_1CrV6WgAAm94v?format=png&name=medium

how does Spirit (Boeing) lock in the aluminum prices for 737 fuselage production?

Thats a ‘spot’ price on the LME.

Large users will have most of their supply on fixed or semi variable longer term contracts

The underlying real issue is the US $ has ‘deflated’ a lot . Gold has jumped as well in $US

Another lmao moment!

> In April 2025, aerospace supplier Howmet Aerospace declared force majeure on certain contracts, citing significant cost pressures from new U.S. tariffs on steel and aluminum, potentially impacting deliveries to Boeing. This legal move allows suppliers to pause obligations due to uncontrollable circumstances…

When your suppliers die, you won’t survive for long.

> “Upper Midwest manufacturing down for third year in a row”

https://t.co/kFm63fhi7J

“The takeaway from this is the biggest impact of tariffs has been on the cost of doing business”

https://pbs.twimg.com/media/HAFeR72WsAAfEo4?format=jpg&name=900×900

“They’re passing a lot of that tariff cost pressure onto their customers.”

A commenter said:

“There is no such creature as a KC-30, the comment makes no sense. The RAAF tankers can not refuel any USAF aircraft..”

https://www.airforce-technology.com/projects/kc-30a-multi-role-tanker-transport-mrtt-aircraft/

From the above link:

“..The KC-30A’s cockpit is equipped with 2D and 3D screens, and accommodates a pilot, co-pilot, an air refuelling officer, one mission coordinator, and up to eight crew attendants. The air refuelling officer controls two air-to-air refuelling systems.

>> The tail section of the aircraft is mounted with the aerial refuelling boom system (ARBS), which is around 12m long when retracted and up to 18m when extended. The flow rate of the ARBS is 8,040lb/min.

The ARBS consists of a fly-by-wire boom refuel system, remote air refuelling operation (RARO) console and a boom enhanced visual system (BEVS). The RARO console is used to control boom, pods, video systems, mission planning system, communications systems and fuel offload quantities. <<

The KC-30A aircraft is fitted with a pair of all-electric refuelling under-wing pods and a 90ft hose-and-drogue system to refuel probe-equipped aircraft at a flow rate of 2,810lb/min. It also features a universal aerial refuelling receptacle slipway installation (UARRSI) with a flow rate of 8,040lb/min.."

Boeing’s FY2025 results show a mixed bag: while BGS drives profit, BCA’s losses remind us how capital-intensive the aerospace sector remains. For smaller aviation ventures or suppliers looking to stabilize cash flow during such turbulent periods, securing funding can be crucial. Services like Crawfort Loans offer a simple loan process that can help companies manage short-term financial pressures while positioning for long-term growth.