Leeham News and Analysis

There's more to real news than a news release.

RTX 2025 Earnings: Commercial Aerospace Leads Growth as Pratt Advances GTF Recovery

By Chris Sloan

![]() Jan. 27, 2026 © Leeham News: “RTX is constructed to meet the moment—by the moment I mean the ramp both in defense and commercial—and to drive long-term value for customers and shareholders,” RTX President and Chief Executive Officer Christopher Calio said as the company closed 2025.

Jan. 27, 2026 © Leeham News: “RTX is constructed to meet the moment—by the moment I mean the ramp both in defense and commercial—and to drive long-term value for customers and shareholders,” RTX President and Chief Executive Officer Christopher Calio said as the company closed 2025.

The company has strong order momentum and a record backlog, driven by commercial aerospace demand and continued progress at Pratt & Whitney as the company works through the Geared Turbofan (GTF) powder metal issue.

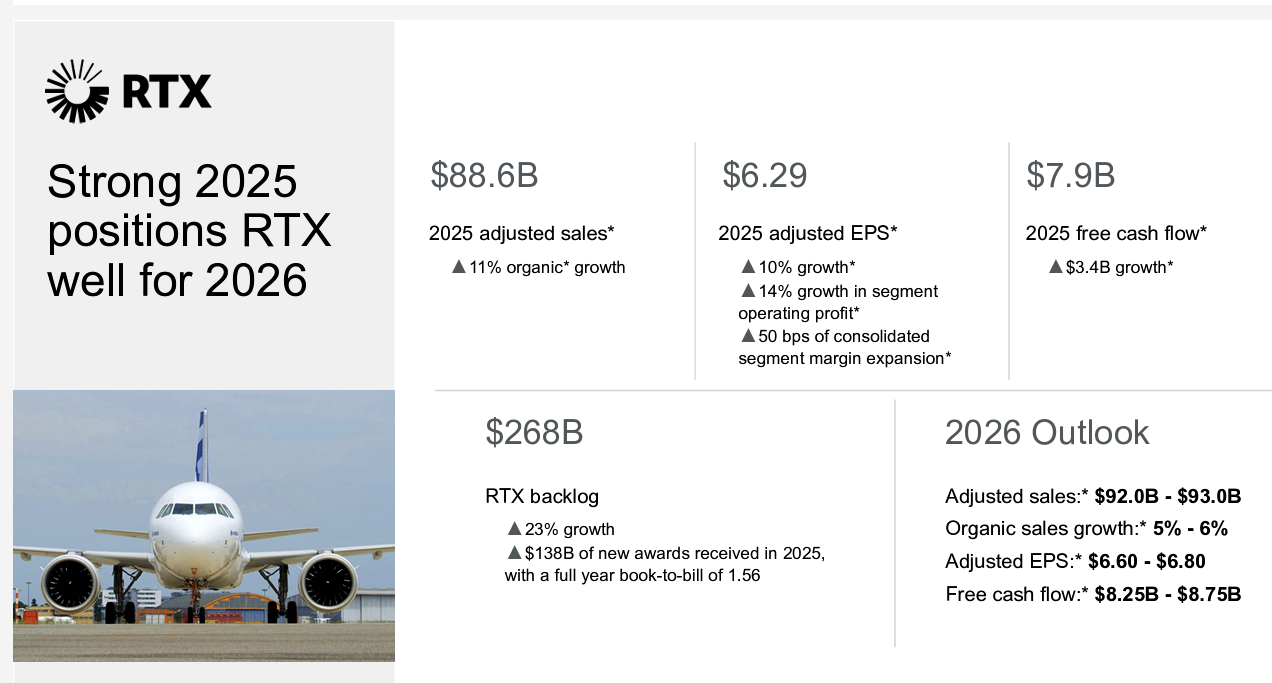

RTX ended the year with a full-year book-to-bill of 1.56 and a $268bn backlog, up 23% year over year, including $161bn of commercial orders and $107bn of defense awards. Commercial backlog rose 29%, supported by higher aircraft production rates and resilient passenger air travel, while organic growth was led by commercial OE and aftermarket.

At Pratt, management emphasized improving performance as the GTF program continues to grow and newer contracts begin to reshape the business. Chief Financial Officer Neil G. Mitchill Jr. said Pratt is “growing out of the older contracts,” with improved pricing on new work and legacy businesses remaining intact, positioning the segment for margin expansion over the next several years as backlog is executed.

Looking ahead, RTX outlined several areas that will shape results in 2026 and beyond, including continued improvements in GTF fleet management, rising MRO output, and the transition to the GTF Advantage engine. Management also pointed to alignment with OEM production ramp-ups, continued improvement at Collins Aerospace, and increased focus on defense output and capital deployment following recent comments from the Trump Administration, framing the company’s outlook as it balances near-term execution with longer-term growth across commercial and defense markets.

RTX Q4 and FY 2025 Earnings Call Slide Image: RTX

Pratt & Whitney: GTF Enters Third Year of AOG recovery

Pratt & Whitney entered 2026 marking a decade since the Geared Turbofan entered airline service, while continuing to work through the third year of elevated aircraft-on-ground (AOG) levels tied to the powder metal issue. Demand for the engine family remained robust. Orders and commitments during 2025 included more than 1,500 GTF engines and more than 2,400 Pratt & Whitney Canada engines. On the defense side, the business delivered a full-year book-to-bill of 1.31, including several significant fourth-quarter awards, Calio outlined.

Execution under the GTF fleet management plan continues largely as expected.

“On the GTF fleet management plan, our financial and technical outlooks remain on track,” Calio noted. As planned, PW1100 AOGs declined in the fourth quarter, a trend Pratt expects to continue through 2026. The improvement comes as compensation payments tied to the powder metal issue begin to moderate. Mitchill indicated cash outflows totaled approximately $1bn in 2025 and are expected to be about $700m in 2026, bringing cumulative cash usage to roughly $2.8bn by the end of next year—close to the approximately $3bn cash headwind Pratt has previously outlined for execution of the fleet management plan.

“We’ve been very prudent in our management of the compensation,” Mitchill emphasized, citing customer agreements and disciplined execution, adding that Pratt is “in good shape for 2026” as it exits 2025.

Operational progress on AOG reduction remains closely linked to shop throughput. AOG levels are down more than 20% from their 2025 peak, reflecting improving repair capacity and shorter turnaround times. “MRO output remains the key enabler,” Calio underscored, framing shop performance as central to stabilizing the in-service fleet as the GTF installed base continues to grow.

GTF Engine Cutaway Image: RTX

GTF MRO and Services: Output and Aftermarket Drive Recovery

MRO performance strengthened throughout 2025, even as shop visits became heavier and more complex. “MRO output was up 39% in the fourth quarter and up 26% for the full year, even as heavier shop visits increased 40% in 2025,” Calio reported. Pratt exited the year with fourth-quarter momentum supported by a 16% reduction in turnaround time and a significant increase in repair volume, easing pressure on new material requirements and improving fleet availability.

Looking ahead, management expects the commercial aftermarket to be the primary growth driver for Pratt in 2026. Mitchill outlined that approximately 70% of segment growth next year will come from the commercial aftermarket, which is projected to grow at a high single-digit rate. Pratt & Whitney Canada’s aftermarket is also expected to expand at a similar pace, outgrowing RPK trends. Within the large commercial engine portfolio, V2500 shop visits are expected to remain steady at just over 800 in 2026, roughly in line with 2025 levels. That stability is partially offset by retirements of PW4000 and PW2000 engines, which Mitchill characterized as a planned headwind of about $100 million, aligned with customer fleet strategies.

The GTF aftermarket continues to expand as the fleet matures. Shop visit content is increasing, adding complexity while also lifting revenue. Mitchill pointed to improving profitability across the GTF aftermarket, describing margins as “low double-digit,” with one to two points of expansion anticipated in 2026. That margin progression reflects durability upgrades, evolving contract structures, and pricing adjustments as the program moves further from entry into service.

Supporting those gains, Pratt continues to improve material flow across its manufacturing network. Calio highlighted that aged inventory has been reduced by about 45% at the Lansing, Michigan, facility that produces GTF fan blades, improving support for both OE production and aftermarket demand. Together, higher MRO throughput, improving material availability, and moderating compensation payments position Pratt to continue reducing AOG levels through 2026—a critical step toward stabilizing the fleet and restoring long-term profitability across the GTF program.

GTF’s at a Pratt & Whitney MRO Facility Image: RTX

GTF Advantage: Closing the Durability Gap

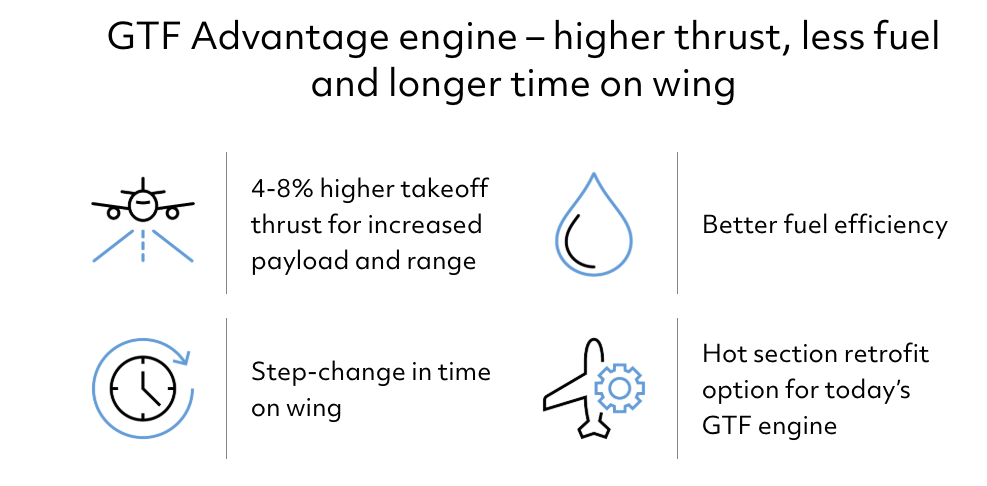

Pratt & Whitney took a key step in resetting the GTF program’s long-term operating profile with certification and production ramp-up of the GTF Advantage, the next evolution of the engine designed to restore Time on Wing performance to original expectations while delivering incremental efficiency gains. The Advantage configuration incorporates a redesigned Hot Section and other enhancements intended to improve durability and reduce maintenance burden across the fleet, while increasing fuel efficiency by up to 1.5% compared with today’s production standard.

Progress accelerated late in the year. “In the fourth quarter, we received the EU certification of the GTF Advantage (GTFA) engine and expect aircraft certification soon,” Calio outlined. Pratt has already begun Production Cut-In of the Advantage engine and expects Entry Into Service later this year. Certification is also expected for the first installations of the associated Hot Section Plus Upgrade Package for MRO customers, extending many of the Advantage benefits beyond new-production engines.

Pratt views the retrofit pathway as a critical element of the Advantage strategy. Calio emphasized that the Hot Section Plus Upgrade Package delivers “90 to 95% of the durability benefits of the GTFA” and will be incorporated into the Installed Base through MRO later this year. That approach allows Pratt to improve On-Wing performance across the existing fleet rather than waiting for full turnover to new-build engines. Together, Production Cut-In, Entry Into Service, and Retrofit Availability position the GTF Advantage as a central lever in stabilizing fleet operations, supporting higher MRO throughput, and improving long-term aftermarket economics as the GTF program matures.

Key upgrades to: GTF Advantage Image: RTX

Aligning With OEM Production Ramps: Balancing Installs and the Installed Base

Management framed Pratt & Whitney’s OE outlook around a measured but sustained production ramp across its core GTF-powered platforms, while continuing to prioritize support for the growing in-service fleet. Analysts questioned whether Pratt’s 2026 guidance appeared conservative given Airbus’ plans on the A320neo and A220 programs, prompting management to emphasize the trade-offs between new installs, spares, and MRO capacity.

Mitchill characterized the approach as deliberate. Large commercial engine deliveries rose about 6% in 2025, and Pratt expects output to grow at a mid-to-high single-digit rate in 2026 on top of that base. Rather than chasing maximum OE volume, the company continues to balance installs with support for the flying fleet, particularly as MRO demand rises. “We’re really trying to make the right balancing decisions between MRO and install,” Mitchill noted.

That balance comes as Airbus continues a gradual ramp on its narrowbody programs. Airbus is expected to produce the A320neo family at roughly 55–60 aircraft per month in 2025, reflecting uneven progress as supply-chain and engine-availability constraints persist. Output is projected to rise further in 2026 as stability improves, with Airbus maintaining its ambition of reaching around 75 A320neo family aircraft per month by 2027 across its global final-assembly network. For the A220, current production remains in the high single digits per month, with the program now projected to reach about 12 aircraft per month this year, a level increasingly viewed as a sustainable medium-term rate rather than a stepping stone to significantly higher output.

Outside Airbus, Embraer’s E-Jet E2 family is also regaining momentum. While Embraer does not publish a formal monthly rate, recent delivery performance and management guidance point to a recovery toward around 100 commercial jet deliveries per year by 2026–2027, implying roughly 8–9 E2 aircraft per month on a normalized basis. Together, the A320neo, A220, and E2 families form the core of the GTF ecosystem.

Calio reinforced the scale of that installed base, noting that Pratt’s total engine deliveries in 2025 were up more than 50% versus 2019 levels. More than 2,000–2,200 GTF-powered aircraft are now in active service worldwide, representing over 4,000 engines flying, with a broader order and commitment base exceeding 12,000 engines. Supporting that growth, Pratt continues to invest in capacity, including a new powder metal tower, a forging press, and expanded turbine airfoil capability in Asheville. While some of those investments, including castings capacity in Asheville (NC), will not fully impact output until later in the decade, they are intended to underpin both OE production growth and aftermarket support as GTF volumes continue to rise.

Pratt & Whitney: Growth Across All Channels

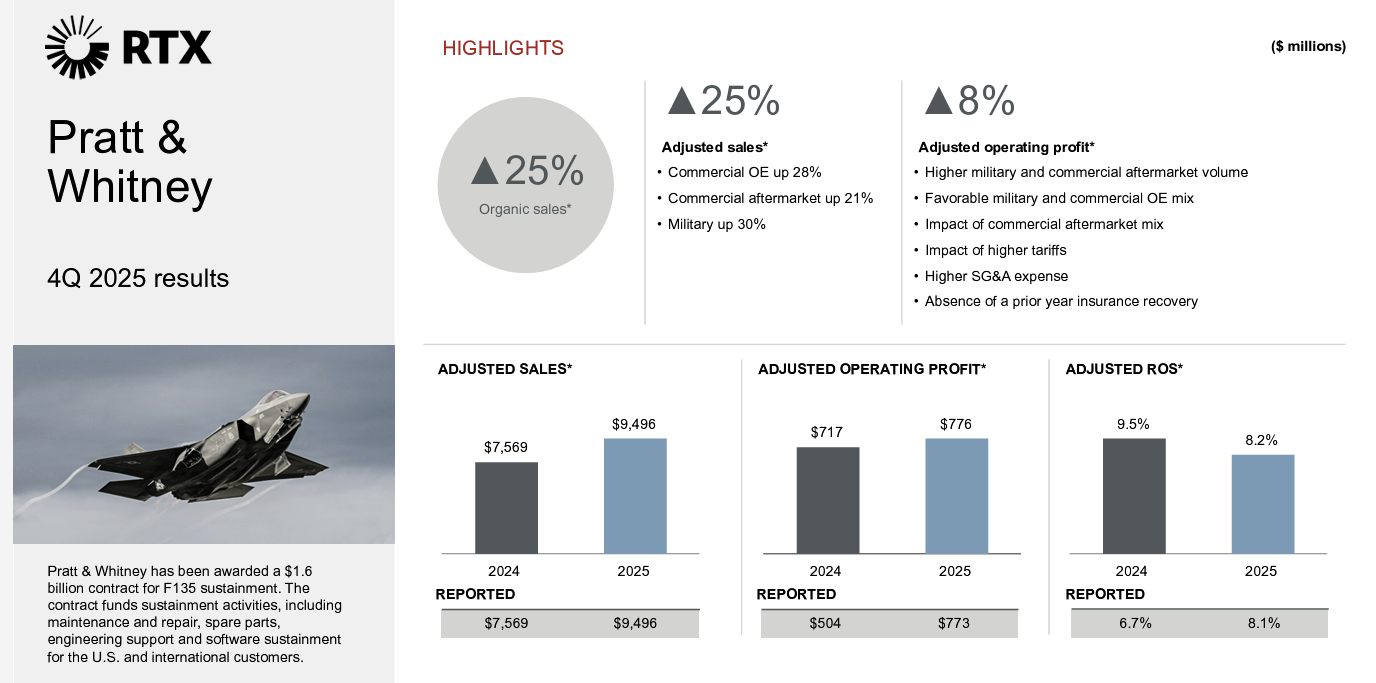

Pratt & Whitney delivered broad-based growth in 2025, with gains across original equipment and aftermarket. Fourth-quarter sales of $9.5 bn increased 25% on both an adjusted and organic basis, Ware reported. Commercial OE sales rose 28%, with large commercial engine deliveries up 6% for the full year. Commercial aftermarket sales increased 21% across large commercial engines and Pratt & Whitney Canada.

Profitability improved year over year, with modest margin expansion for the full year. For 2026, management expects continued growth, led by the aftermarket. Mitchill outlined expectations for full-year sales to rise at a mid-single-digit rate on both an adjusted and organic basis. Commercial OE is expected to grow in the low single digits, while commercial aftermarket is projected to increase at a high single-digit rate.

RTX Q4 and FY 2025 Earnings Call Slide Image: RTX

As Mature, MRO-Heavy Programs Retire, Where Do Pratt Margins Go?

Analysts pressed management on how Pratt’s margin profile evolves as mature, MRO-heavy programs begin to retire, and the GTF fleet becomes the dominant driver of growth. Management framed the answer around the interaction between legacy engine cash flow and the accelerating scale of the GTF installed base.

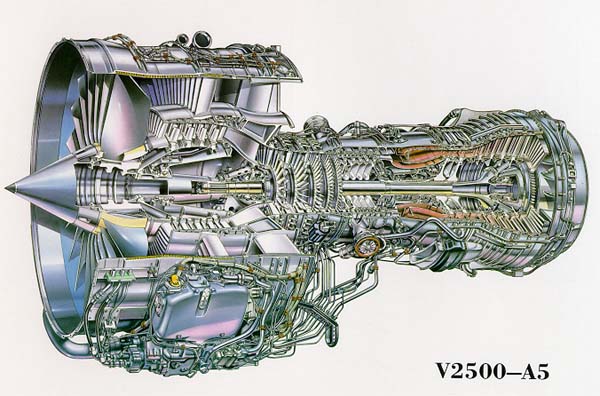

Calio emphasized that the V2500 remains a meaningful contributor, with shop visits expected to stay around 800 annually, low retirements, and continued demand providing near-term margin support. Over time, however, margin expansion increasingly depends on the GTF aftermarket. “It’s going to be the GTF aftermarket that’s going to need to continue to grow in profitability,” Calio said, pointing to durability improvements already entering the fleet and expected to deliver incremental benefits as they propagate across the installed base.

Mitchill reinforced that outlook by focusing on fleet mix and scale. He noted that today’s GTF fleet is roughly the same size—and slightly larger—than the installed V2500 fleet, and that “as you look out a number of years, that GTF fleet is just growing at a really significant rate,” a dynamic he said will “overcome sort of lost revenues and profits” as V2500 engines retire. As the fleet expands, demand for spare engines is expected to remain strong even as ratios evolve. “While the ratio might come down, we’ll still be selling a lot of spare engines,” Mitchill said, describing spares as a steady source of revenue and profit that also feeds future overhaul activity. That cycle—supporting the fleet, driving aftermarket contracts, and generating repeat MRO work—was framed as central to Pratt’s long-term margin trajectory.

IAE V2500 Cutaway Image: IAE

Collins Aerospace: Transformation Underway, Margins in Focus

Collins Aerospace delivered steady performance in 2025, even as management devoted less time to the segment in prepared remarks. Fourth-quarter sales of $7.7 bn increased 3% year over year, while full-year sales reached $30.2 bn, up 7%, according to company data. Growth continued across commercial OE, commercial aftermarket, and defense, reflecting the breadth of Collins’ installed base.

Margin performance, however, remained top of mind for investors, prompting requests for more color during the earnings call. Management framed the outlook around a multi-year transformation effort rather than a near-term mix. “When I think about Collins in particular, they’ve kicked off a pretty significant transformation effort there to drive cost out of both the production side as well as the back office,” Mitchill said. “So I see tailwinds supporting the Collins margin trajectory.”

For 2025, Collins delivered about 30 basis points of organic margin expansion, even as tariffs created meaningful pressure. Management described tariffs as a roughly 90-basis-point drag on margins during the year, masking underlying improvement. Adjusting for that impact, Mitchill characterized Collins’ organic margins at about 17.1%, with cost-reduction benefits already flowing through the business.

Looking ahead, management expects those improvements to accelerate. While tariffs remain a factor, Collins is projected to deliver about 80 basis points of margin expansion in 2026 at the midpoint of guidance, inclusive of tariffs. OE sales are expected to grow around 10%, while roughly 45% of segment growth is projected to come from the aftermarket, which carries stronger drop-through.

RTX Q4 and FY 2025 Earnings Call Slide Image: RTX

RTX Pressure From the Administration Creating Tension Between Government and Shareholders?

While much of RTX’s 2025 performance was driven by commercial aerospace, defense production, and capital allocation came under sharper scrutiny late in the year following public criticism from the Trump Administration. In a Truth Social post, President Donald Trump called out Raytheon, now part of RTX, as “the least responsive to the needs of the Pentagon, the slowest in increasing their volume, and the most aggressive spending on their shareholders rather than the needs and demands of the United States Military,” warning that government contracts could be at risk without faster output.

That commentary prompted questions on the earnings call about balancing defense investment with shareholder returns. Calio responded that RTX fully recognizes the urgency to deliver more and faster for national security, noting output increases of more than 20% on several critical programs in 2025 and plans for higher production and capital spending in 2026, while reaffirming the company’s long-standing commitment to the dividend and its ability to fund both capacity investments and shareholder returns.

A Solid Finish to Q4 and 2025, Guiding to Steady Growth in 2026

RTX closed the fourth quarter of 2025 with continued top-line growth, even as tariffs remained a headwind. Fourth-quarter revenue totaled about $24.2bn, up roughly 12% year over year. Adjusted operating profit was $1.2bn, up modestly versus the prior year, despite approximately $600million of tariff-related impacts, Mitchill outlined.

For the full year, RTX reported revenue of approximately $88.6bn, an increase of about 10% versus 2024. Full-year adjusted operating profit also increased year over year, though tariffs and completed divestitures continued to weigh on results.

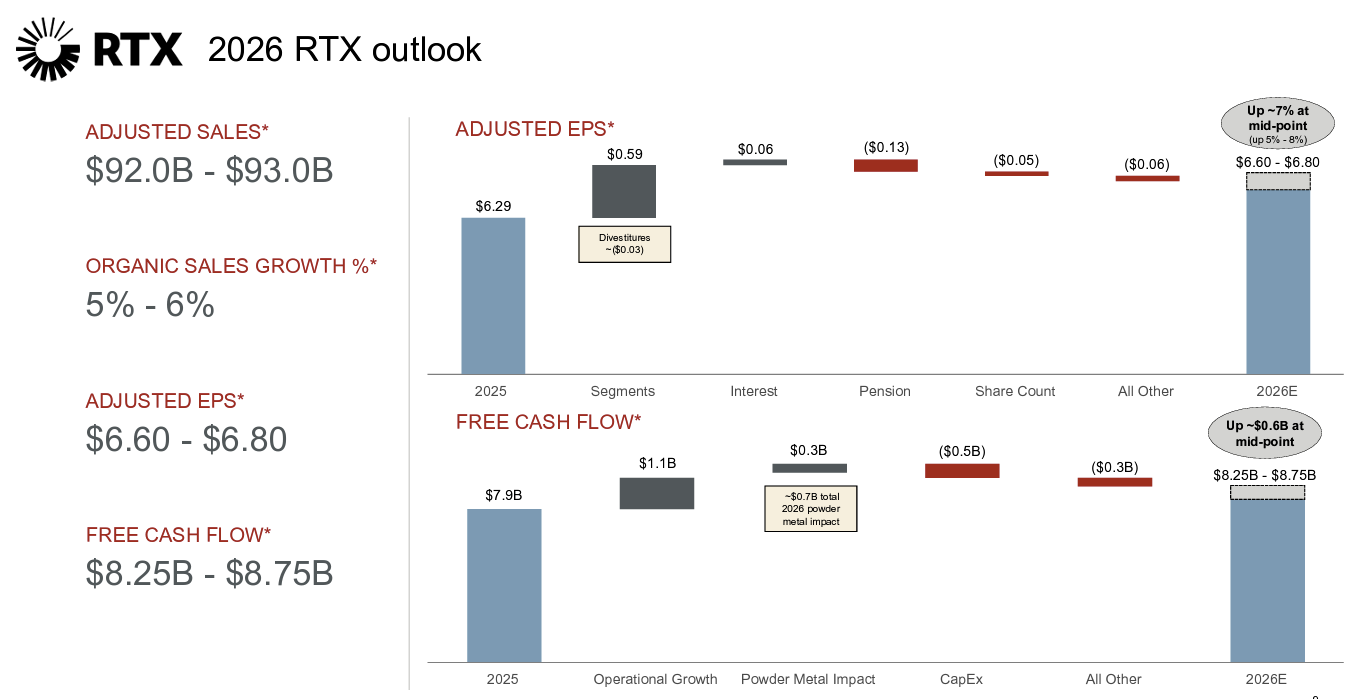

Looking ahead, RTX guided to 2026 revenue of $92bn to $93bn, implying 5% to 6% organic growth. At the company level, and adjusting for divestitures, management expects commercial OE and defense to grow at mid-single-digit rates, while commercial aftermarket is projected to increase at a high-single-digit pace.

Analysts viewed the results and outlook as steady. Robert Stallard of Vertical Research Partners described the fourth quarter as “a decent operating result” and said RTX’s initial 2026 guidance was in line with consensus, adding that “given the risk in forecasting the short-cycle aero aftermarket, this guidance may prove to be conservative.”

RTX Q4 and FY 2025 Earnings Call Slide Image: RTX

RTX says GTFA will be a “step-change” in durability, but do

not define that term in context. Interesting.

What else can the company say?

The PR departments at large corporations are tasked with cheshire-cat smiling, and talking without actually saying anything.

Keeping the stock price afloat at all costs 😉

There are 8000 testing hours in a year, with an install, you may get 10-12 hours a day use, so how is PW supposed to know how long things last until they get hours on them?

At best its a guess. There may well be a minimum they think they will meet, the maximum will remain unknown until you hit the minimum hours and start counting (or do not meet minimum)

TOW is the same. They can design to anything they desire. How it meets that design, unknown. Again there will probably be a minimum.

PW did not set out to deliver an engine that had issues. They should have been able to produce the base engine with no issues. Clearly they did not. Only PW knows the real story.

They are paying compensation for their failures. While it can compensate lost revenue, it does not compensate for failure of a flight to go and the customers (not guests!) being unhappy and loosing long term revenue.

The reality is its going to be a decade before PW and the airlines knows what each fix has done as well as what the combined fixes achieves.

I assume they will be measure on results.

If the GTFA can deliver on better fuel burn, durability and avaialablity,

they certainly could claw back market share – seems the Airframers would be capable for ramping up more A32x, A220 and E2.

It should be noted that the Metals issue was only one of a number of tech problems on the GTF.

It would be good to get some definition for odd terms.

I have no idea what aged stock means.

What does management of compensation mean?

Airbus build rates were noted as iffy for 2025? We are almost two months into 2026 and we know what build rate for 2025 was.

Remind me the build rate of BA’s 737 max. Has BA reached rate 38 on three-month rolling average?

How many 737 Max did BA roll out last month?

@Vincent

In the context of what the changes are it is helpful to understand what they are intended to do. Part of the upgrade is a top line thrust bump to support XLR. Most airlines do not need that extra thrust but it will still be helpful. A lot of the shortage on TOW is from the fact that those engines are at max output on A321.

Simply putting in a bigger compressor to cool of the turbine should do a world of good.

A good deal of the turbine is getting enhanced coatings or otherwise more aggressive materials choices.

The trade off. It’s a bigger engine and weighs more.

Yea, they call it a LEAP and its less SFC.

The GTF is just getting started, with the existing setup. LEAP is at the materials limit.

P&W could to a NEO GTF and bump it up a bunch.