Leeham News and Analysis

There's more to real news than a news release.

Airbus FY2025: Not happy with Pratt & Whitney

By Karl Sinclair

Feb. 19, 2026, © Leeham News: The normally reserved Airbus (AB) CEO Guillaume Faury had some strong words for engine-maker Pratt & Whitney (P&W), at the annual video conference reporting results for the 2025 financial year.

Feb. 19, 2026, © Leeham News: The normally reserved Airbus (AB) CEO Guillaume Faury had some strong words for engine-maker Pratt & Whitney (P&W), at the annual video conference reporting results for the 2025 financial year.

Airbus is ready to “enforce contractual rights” with regard to the engines being supplied to the airframe maker from P&W (corporate speak for “You’ll be hearing from our lawyers”), in an effort to meet delivery requirements.

The issue is centered around the resources that Pratt is deploying to remedy the problems caused by powdered metal coating contamination misstep, which is hampering production of both the A320neo and the A220 families.

According to Airbus, the engine-maker has focused more effort on addressing in-service fleet issues, while eschewing its responsibility to provide engines to the aircraft OEM for deliveries.

This is hindering Airbus’s efforts to increase production as it seeks to meet its commitments to airlines and lessors.

“On the A320 family, the continued failure to commit to the number of engines ordered by Airbus is negatively impacting this year’s guidance and the ramp-up trajectory for this year. As a consequence, we now expect to reach the rate of between 70 and 75 aircraft a month by the end of 2027, stabilizing at a rate of 75 thereafter,” said Faury.

Whether this is simply sabre-rattling to force P&W to increase production by publicly calling them out is unclear.

Faury elaborated further in the earnings call, “Pratt & Whitney has resigned from the orders we had placed, and they had accepted for the volumes in 2026. We have to base our guidance on what they tell us now they’re willing to commit and deliver. We’ll continue to work hard to enforce our contractual rights, which we believe are not respected in that case…We are not happy with the outcome, but that’s what it is today.”

These are choice words in an industry where airframe and engine makers work closely together to meet their customers’ needs.

Company Results

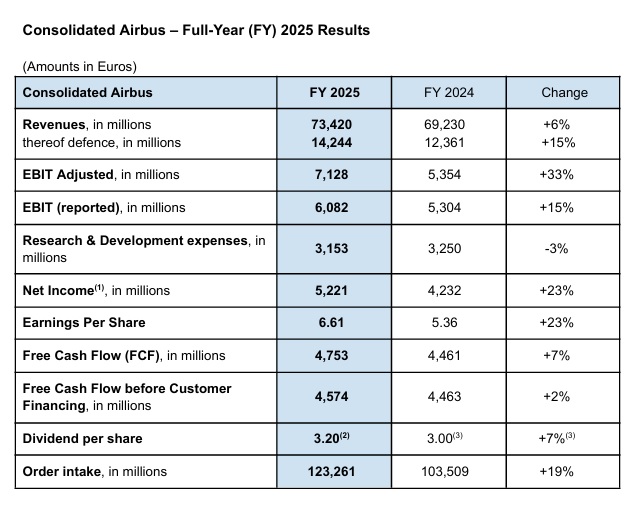

Source: Airbus.

Company-wide, Airbus had a solid 2025. Revenues climbed €4.19bn, year-over-year (YoY), up 6%.

EBIT adjusted jumped a whopping 33%, up €1,774bn. Free-cash-flow (FCF) was up a modest 7% to €4.753bn and the net cash position rose to €12.2bn, up from €11.8bn at the beginning of the year. Order intake rose €19.752bn in 2025 to €123.261bn and the consolidated order book stood at €619bn at year-end.

In a nod to investors, Airbus increased its dividend to €3.20 per share, a 7% increase.

Division Revenues

Airbus 2024 revenues by division. Source: Airbus.

Airbus 2025 revenues by division. Source: Airbus.

Airbus commercial aircraft lost ground in the consolidated revenue pie in 2025, dropping to 70% of total company revenues. While this may be seen as a slipping of the commercial position in the company, given the spate of recent difficulties at Defence and Space (with 2025 seeing another modest charge of €73m to the A400 program being taken), many will take this as positive steps in the right direction for Defence.

Segment Results

Commercial Aircraft

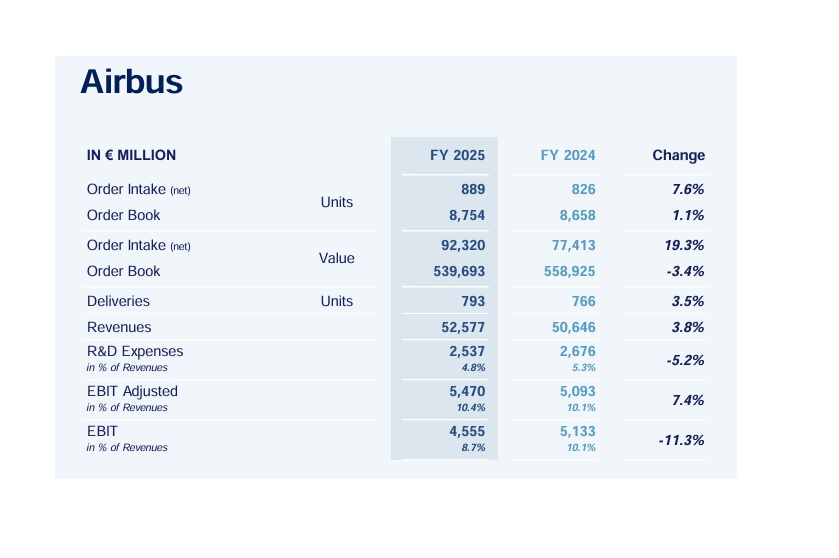

During 2025, Airbus delivered a total of 793 aircraft, including 93 A220s, 607 A320neo family, 36 A330s, and 57 A350s (up from 766 deliveries in 2024). A220 handovers grew from 75 units in 2024 to 93 in 2025 and now account for 12% of commercial deliveries (up from 10% in 2024).

The original guidance at the beginning of the year called for a target of 820 deliveries in FY2025, which was revised mid-year to 790 aircraft. Guidance for 2026 now calls for 870 commercial deliveries in 2026, a ~10% increase, YoY.

Revenues rose to €52.577bn during the year (€50.646 in 2024), growing on an increased delivery tempo, up 3.8%. Services revenues increased at commercial aircraft to an 11% share of the pie (up from 10% in 2024), with platforms declining to 89%. EBIT adjusted jumped to €5.47bn (up from €5.093bn in 2024 – a gain of 7.4%) and a margin of 10.3%.

Returning to P&W

Faury is obviously displeased with the pressure Airbus is facing as it attempts to ramp up production to meet its future delivery targets.

As if to underline the issue, he addressed the Pratt & Whitney problem a third time in his comments, delving deeper into the details of the travails the engine maker faces.

“P&W have the combined needs at the moment of serving the production for new aircraft and serving the MRO capabilities for the recall campaign. [This is] linked to the metal powder and to the rather low durability of the engine and that puts stress on a number of bottlenecks, supply of certain parts which are too small in numbers to serve completely both needs and the MRO capability to retrofit all engines in service and reduce the number of AOGs….We are very frustrated that they have decided to reallocate more to the in-service because they miss global capability, and to the detriment of Airbus.”

Airbus Commercial Aircraft summary. Source: Airbus.

Airbus is now targeting a rate of 13/mo for the A220 program in 2028, 70 to 75/mo at the end of 2027 for the A320 Family, 5/mo for the A330 program in 2029, and 12/mo for the A350 in 2028.

Airbus also took a €188m charge during the year, relating to the Spirit AeroSystems work packages acquisition and integration. This was to be expected, as part of the acquisition terms, Spirit (now Boeing) was required to pay Airbus some €500m at closing to fund the money-losing operation.

How much more Airbus will have to add in the future is unclear.

Helicopters

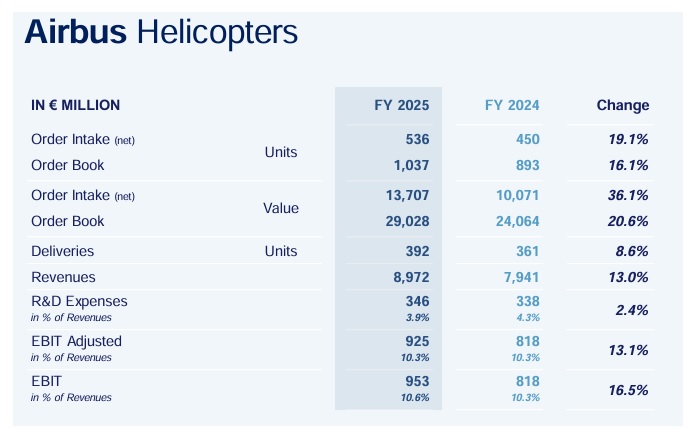

Airbus Helicopters also performed well in 2025, with increases across every metric.

Airbus Helicopters summary. Source: Airbus.

Revenues were up 13% to €8.972bn (€7.941 in 2024) on higher deliveries and services growth. This resulted in a 13.1% gain in EBIT adjusted to €924m (€818m in 2024). Deliveries were up during the year, hitting 392 units (361 in 2024), an 8.6% rise.

Defence and Space

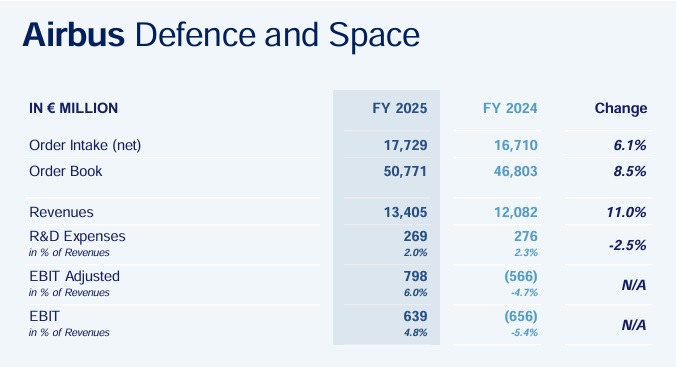

In FY2024, the segment took a €1.3bn charge linked to the Space program. Airbus has now put that in the rear-view mirror, and Defence and Space provided steady gains for the company in 2025.

Airbus Defence and Space summary. Source: Airbus.

Despite the aforementioned FY2025 charge to the A400 program of €73m, EBIT Adjusted was back in the black, earning €798m on revenues of €13.405bn, for a respectable 6% margin. The division also grew revenues by 11% during the year, up €1.323bn (from €12.802bn in 2024).

Work on the proposed joint venture with Leonardo/Thales (codenamed Bromo by Faury) is still ongoing and is not yet at the integration stage, according to Faury. There is still much regulatory and governmental work to be done, according to him. Last year was solid for Airbus, and management must be pleased with the financial results. However, they are obviously unhappy with the impediments facing the commercial segment, which are hampering the ramp-up efforts.

Translation: screw our customers who have grounded aircraft; our production ramp-up is far more important.

One could also attempt to keep *both* parties happy.

Ultimately, customers also aren’t happy with delayed deliveries…

no, unfortunately not. If you do not have enough capacity you have to decide if you annoy A, B or both. Making both happy is impossible.

Define “not enough capacity”.

Is it a staffing issue?

Tooling issue?

Raw materials issue?

Funding issue?

Something else?

Raytheon has vast resources at its disposal.

Can be any but most likely is capacity to produce one single component that they are short of

.

Result: not enough engines available

There’s a mantra in the marketing and sales department: JUST GET THE PAPER (translation – the sales.)

We’ll worry about manufacturing…

You do your job we’ll do ours.

Obviously, the company is not performing at peak performance. But aerospace is filled with monopolies.

Most, if not all, have been reduced to just “optimal” in response to price cuts demanded by the one sitting at the top of the chain and the relentless pursuit of short-term profit maximization.

There are things you think and there are things you say.

That’s a slanted take on PW failing to deliver the contracted number of engines to their biggest source of revenue.

Keep in mind that Airbus has been putting huge pressure on both P&W and CFM to dramatically RAISE production above levels that had been previously planned.

The path to higher production rates was set quite some time ago.

What Airbus seems to build pressure on is actually toeing the line of planned production increases on the engine maker side.

sideNote: newspaper here (SH.Z) offered today that “Faury is livid”. quite a bit beyond “unhappy”.

I can still remember that back in May 2021, Airbus told suppliers to get ready for producing 70 A320-family jets a month by Q1 2024 and raising production to 75 per month for 2025. Suppliers have plenty advanced notice of what’s going to happen in the next few years.

The engine makers (both) didn’t want to flood the market with new, more efficient NB aircraft that would undermine their significant source of revenue from major overhauls (like what happened to RR about a decade ago) and, one way or the other, they succeeded!

I never thought of that possibility. One way or another decisions made pertaining to this matter involve money. They could be dragging their heels, so they have a revenue stream in M&O as they figure out engineering and manufacturing…

If your supplier has a problem, you also have a problem. Nevertheless if Pratt is contracted to deliver a certain number of engines and parts, and fails to do so, that’s on Pratt, not Airbus

well, i d say it depends on who has the earlier contract.

Different regulated industry but I remember the end of 2022 when we were taking our supply chain managers out to fancy dinners and giving them bonuses for successfully navigating us through the pandemic and the post-pandemic path back to normal. Then came 2023. And 2024 which was in some ways worse particularly for construction and complex equipment purchases. I can understand Airbus’ frustration but there may be no there there for Pratt to squeeze.

[Edited]the big US defense corporations [were chided] a few weeks ago for falling behind on output, [Edited].

https://www.defensenews.com/industry/2026/01/09/trump-threatens-to-cut-raytheons-government-contract/

One wonders if this is why production of new commercial engines has slid down the priorities list at P&W. [Edited]

P&W present a recurring problem for Airbus.

start with the SuperFan

continue into PW6000

and now the GTF

bad luck or enemy action 🙂

+ 1

Totally agreed, that the Commercial Airline sector is suffering the consequences of the more lucrative Warmongering demand.

The “Division Revenues” pie charts got the same label.

The second one should be “Airbus 2025 revenues by division. Source: Airbus.”

Thanks, fixed.

Strong words indeed from Mr. Faury. We’ll see how it goes.

Well they haven’t done anything about P&W’s abysmal record over the last 6-7 years so I doubt they are going to do something about it this year or the next.

Powder metal contamination is a big issue. The pressure is on P&W now, but it applies to any engine manufacturer. I can see rocket engine turbopumps having similar issues. One of the fixes is to drill down to Tier III and IV suppliers of raw materials, and bring additional inspections and certifications. A costly endeavor and one that will take added time to the delivery line.

Interesting as this is a subject I have been pondering as of late, so hold your hats, its going to be earth shaking! (hmm, maybe wind blown?) whatever.

As I understand it, the engine MFG is NOT contracted to Airbus, they are contracted to the customers buying Airubs (or Boeing or those ever elusive COMAC/UA/) Embraer and so on.

So the beef is between PW and the customers.

So using a current example, Vietjet just (ahem) selected PW to power another tranche. From he wording (did not look it up) PW had the original NEO fleet. So VJ is fine or resigned or whatever but went with the GTF again.

Things of course are not clean, Vietjets jets are not next in line. So lets say Whiz Air is. Vietjet is happy PW is getting them engines for their AOGs. Whiz Air may not be (don’t know if they are a customer, should have looked that up) but also happy PW is prioritizes its AOGs.

So what we hear in a previous Article was that the customers were happy with PW in that while the problems incurred were nasty, PW has given them full support to corrected it which means engines and spare parts sent.

A running aircraft vs a new one you are bringing into the fleet seems to be preferable.

So in fact Whiz Air has opted for more PW 1000s (looked it up) as has Vietjet.

Now I could be wrong (it happened once before, see note) but I don’t recall a single airlines cancelling out of PW 1000 engines. I know there was some noise about Indigo but it seemed to wind up PW 1000.

note: There was the time I thought I was wrong but I was wrong about that. So it goes.

So given happy customers (well sort of happy) and orders continuing vs an unhappy Airbus, I choose the Customer every time.

Someone might enlighten me as to any payback a mfg gets for the opportunity to select engines. Sort of recall payments towards the program but vague and no idea if those continue or its a one time sort of thing.

However it is, PW clearly has moved to support customers as its their fault the aircraft are grounded.

Does Airbus even have a spanner in the works? They were the ones that wanted two engine choice (which may still be a good thing, could CFM have ramped up another 25% (more or less the share of CFM engines supplied to Boeing and Airbus.

Do the contracts even say who gets what if there is a shortage?

Certianly PW has taken a Customer approach and those will have the biggest bucks and impact involved.

At least in theory if you have an aircraft shortage, the Airliner can stop the retirement of older aircraft (yea the pesky lease thing get involved but they seem to work that out).

Now flip the coin and see the other side visa the Trent 1000/TEN. Customers are abandoning that engine. So, the impact hitting them, RR support, the worse fuel burn probably all have their part in those decision and I am not sure anyone is ordering aircraft with those engines now.

Faury can be as displease as he wants, I doubt PW is shuddering in their boots. Recent builds have the fixes, those fixes are working their way into fleets in the form of spare engine (or exchange engines)

So then explore the alternaive. PW or Airbus simply stops engines to Airbus (different aspect but same result). That leaves a 50% in Airbus A320NEO world shortage of engines.

Now that is 25% to CFM, but how long would it take CFM to crank up production to fill that 25%? GE does have an obligation to Boeing as the only offered engine. Probably a different clause set involved there.

CFM has its issue on the LEAP and are scrambling to deal with those as well as putting the PIP into current engine. 5 years to deliver what PW is delivering now? Do they get an exclusive or are they back to competing for airlines at some point? How happy are airlines going to be that have committed to GTF?

Short Boeing when you have a non compete deal going? Not going to happen. Its a different engine despite the name, so it has all the elements of a whole new build set.

And the production is supplying parts to Safran to build those engines for Airbus, which means Safran has to up their work and production as well. Parts and assembly operations.

I think Faury is spitting into the Hurricane here.

This adder on the subject is interesting. Basically CFM only provide what they agreed to for 2026. Makes sense as that planning is done well ahead. Can not change it on the fly. Its not stamping out widgets.

That said, CFM is stated here as having its own issues with support of existing LEAP fleet.

https://archive.ph/WaIFB

It is of course ironic that is why PW is not delivering what they thought they could. Their problems exceed CFM so its not short term.

And even if CFM could, if the aircraft in line are GTF powered, you owe it to the Airline to deliver that even without engines. The engines being an issue between PW and the Airline.

PW has a fairly good idea how its all progressing. As the upgrades set in the problems reduce and that frees up engines to go to Airbus for install.

It is kind of funny in that Airbus will not get paid for the Aircraft because its not flying and proving its all working right when you can’t test without engines (temporary mount the engines, do all the delivery stuff and then yank the engines for the next aircraft?)

Now pay us darn it, you choose the engines, you find the engines!

At issue of course is scheduled builds and 50% more or less is PW engines and you can only go so far out of sequence and then you can’t get engines from the other guys if you do.

Catch 22 at its finest.

Maybe they should have made the engines easily swapable on the A320 like the 787 (that no one swapped an engine on yuet as far as I know though maybe in the future as the Trents reach rebuild?)

The aircraft with registrations N74751 and N94750 that will be delivered to United Airlines are the airline’s first A321neos equipped with CFM engines, since all other United neos use P&W engines. I don’t know if it was a purely contractual choice or if it’s related to P&W’s problems.

Thanks. A lot of weeds stuff and of course I miss some of it.

United of course is not going to tell us. It has to be a fairly long lead time decision. Airbus has to get the right kit for the CFM choice and United has to be geared up to deal with the engines on a maint aspect.

Hahaha I can’t believe that after so many days no one bothered to correct this post, usually I’d ignore this one but I think this subject matter is important enough and there’re other posts that sow confusion here:

Take a look at this, one just have to change the airframer to Airbus (even AI knows a thing or two better):

> XXX has a long-term agreement with YYY International to supply the ZZZ engine as the powerplant for the ABC aircraft. The deal, solidified with a master contract…

> A master contract was signed in 201x to finalize the engine supply for the ABC’s Integrated Propulsion System

> This is the first master contract for airborne systems that XXX has signed for its ongoing ABC Program.

##########

I don’t know what’s meant by canceling “out of PW engines”: explain how it works. Nevertheless, an Indian airline had gone bankrupt partly because of the aircraft with PW engines were grounded and airlines had switched future contracts to other engine supplier. What happened to RR’s customers no doubt also happened to P&W’s customers. No amount of whitewashing is able to rewrite the reality.

“I think Faury is spitting into the Hurricane here.”

Remember this. Check back later to see if it matches future development.

When it’s reported that: Airbus has now triggered a dispute clause in its contract with the enginemaker, it’s logical that there’s a written contract between the two parties, containing a dispute clause. A new aircraft program worths tens of billions, why would anyone proceed with luck and prayer, without knowing their legal rights and responsibilities. Airbus has been in the business long enough (and has enough in-house lawyers) to know what it’s talking about, unlike the one here.

##########

> Airbus is known to be working on a big plan to significantly increase output of the A350 in particular over the next several years…

Outstanding revenue performance from Airbus. No mention on how their services division performed.

GE would be keen to provide a second engine option for the Airbus …A220. But that’s a dream that’s sailed.

The Airbus A220 is exclusively powered by Pratt & Whitney PW1500G geared turbofan engines. In contrast, the Airbus A320neo family offers a choice between two engine options: the CFM International LEAP-1A and the Pratt & Whitney PW1100G-JM (also known as the GTF)

This article doesn’t segregate out the percentage of 75/month build rate requires from P&W that Faury is complaining about.

Understanding P&W conundrum with the powered metal oxides.. to improve heat transfer (cooling) has been challenging and their engineering is working OT to solve this issue. Each improvement requires massive testing on the ground and sometimes on wing. Patience is a virtue but don’t tell the airline or OEM customers that. 😉

Let’s not forget that CFM has their own set of problems with the LEAP.

@Airdoc: PW supplies about 40% of the neo engines.

That is great data. I had thought 50% so its probably telling on the more PW issues aspect.

Ball Park 700 engines a year to replace all the PW engines.

CFM is ramping up for the MAX increasing build and that I suspect is a no choice engine supply. You don’t get an exclusive without tight contractual terms. It also impacts programs in progress or going forward.

I don’t think CFM can afford to do an A220 engine. Just modifying a MAX engine does not work (large and heavy) and you have virtually a new engine.

Even at rate 14, that is an unknown number of engines per year but its not large as PW will get its share and call it 70/30 and your only market is the -500.

Looks like a loosing proposition.

Or you can make money on MAX and A320NEO engines.

This article suggests that Airbus is already further along the path to confrontation:

“Airbus has now triggered a dispute clause in its contract with the enginemaker, a subsidiary of RTX, Faury said, declining to elaborate further.

““They are not respecting their contractual obligations, so we want to enforce our rights. And indeed we have initiated a process,” Faury told reporters Thursday, criticizing Pratt for not scaling up production enough to meet its commitments.”

https://www.wsj.com/business/earnings/airbus-warns-of-hit-to-a320-jet-production-from-pratt-whitney-engine-shortage-98bc96f1

===

We’ve seen before in the Qatar case that AB isn’t shy about escalation…

So, who wants to be an engine supplier for my next gen aircraft? Ready to launch in 2030, so engine selection in 2028-29. Ahh, Pratt & Whitney, that contractual dispute on allocating engines away from us – let’s have a chat

Maybe its time to look at another supplier? Aero Engine Corporation of China CJ-1000 and CJ2000 engines! While some will scoff at the thought….maybe in 10 years P&W will no longer be in the engine business and China’s engines will have been proven and production has ramped up to take care of Southeast Asia commercial aircraft deliveries

Don’t rule out (new) European players, either.

The market is big enough, and the supply side is currently too concentrated in one country.

You can be sure that AB would like more (sovereign) options closer to home.

just a fyi Google AI “Starting a company to build commercial aircraft engines requires billions of dollars in capital, with development programs often exceeding $10-$30 billion and individual engines costing up to $25 million. Initial factory infrastructure alone for aerospace startups can cost over $4.7 billion”

Seems like only China has the resources (e.g. government policy and resources) to be a EASA certified commercial aircraft engine mfg. market! 10-15 years?

Europe already has multiple players, but two of them are currently hitched to outside OEMs (remnants of the old snuggle-up days of globalization).

However, there are, of course, alternative hitching constructs possible. MBDA could serve as a model — a successful JV between three separate companies in three different European countries: the underlying companies still exist, and do their own thing, but they also operate under the MBDA umbrella when it suits them.

We’ve already seen stresses in the CFM marriage (w.r.t. the recent unilateral ban on China deliveries). And MTU might not be entirely content with the current policy at P&W.

Well in fact European players are playing, one is Safran and the other is MTU.

Reality is you just took two of the bigger ones out of the mix. They have contractual agreements and are not going to jump off a cliff. GTF might as well be a V2500 Consortium product.

RR is the closest builder to Europe with experience (they do not consider themselves European) .

So the remnants start now and 10 years form now have a LEAP type. Why would anyone buy a new LEAP type and all the issues that go with it when they can buy a sorted out LEAP?

Market is probably pretty skinny unless you have 30% of it (and hopefully better).

V2500 became a good engine after it got through the teething issues that PW1000 and LEAP are through. Yes the issues are there but the fixs are in.

Massive project for no return is not a good way to stay in business.

You got to weight possibles vs reality and the reality is airlines are ticked off about new engines. Great time to jump in with a (ahem) new engine.

Mini Mac 10 milling off your foot.

“GTF might as well be a V2500 Consortium product.”

That actually was what Airbus would have liked to see.

Expressed position before the commitment to the GTF in scope of the NEO project. see:

https://www.flightglobal.com/no-interest-in-gtf-for-a320-unless-offered-through-iae-leahy/90481.article

Who told you RR do not consider themselves European?

Only a vocal but decreasing percentage of Brits don’t consider themselves to be European.

Last time I checked, the UK was part of the continent of Europe — which means that RR is European, regardless of whether or not it considers itself to be.

@DP:

Sorry to be one of the scoffers (well not really). PW is not going anywhere.

Its a huge enterprise with jet engines in the military and civilian areas as well as Turbo Prop presence almost everywhere.

Customers putting in new orders selecting PW shows (per above) that they have winning hearts and minds.

In Ten years China will have achieved something around a JT-8 (more or less reliable, ok maint levels, added more bypass – not up to CFM-56 standards)

In the meantime PW has thousands of engines being built, tested, upgraded.

PW clearly lost focus on an engine is a package and thought you did not have to keep a sharp eye on the known aspects. Certainly were wrong. They clearly have the experience and ability to have corrected that and are.

Lo many years ago, RR thought they could build a better automatic transmission for the RR (Ghost?). They had been using GMs Turbomatic 350 or 400. RR failed miserably and went back to buying what was the best autonomic cranny of the era from GM.

So it goes

Trans…”In Ten years China will have achieved something around a JT-8 (more or less reliable”

Not exactly…comparison from Google AI

While the JT8D was a pioneering engine in its time, it is not a direct competitor to the modern, high-bypass technology of the CJ-1000A, which is designed to compete with engines like the CFM LEAP and Pratt & Whitney PW1100G

The comparison between the Pratt & Whitney JT8D and the Aero Engine Corporation of China (AECC) CJ-1000A represents a shift from a 20th-century low-bypass turbofan to a modern, high-bypass engine designed for 21st-century efficiency. The JT8D is a historic “workhorse” engine, while the CJ-1000A is a developmental, next-generation engine aimed at replacing foreign engines on the COMAC C919.

Key Comparison Points:

Generation and Technology: The JT8D was introduced in the early 1960s as a low-bypass engine, known for reliability but high fuel consumption and noise. The CJ-1000A is a modern high-bypass turbofan, using advanced materials, 3D-printed fuel nozzles, and a much larger fan diameter for better fuel efficiency.

Bypass Ratio: The JT8D is a low-bypass engine (typically around 0.96:1 to 1:1). The CJ-1000A is a high-bypass engine, designed to be more efficient by having a larger percentage of air pass around the core rather than through it.

Thrust Class: The JT8D family produces 12,000 to 21,700 pounds of thrust (for the -200 series). The CJ-1000A is designed for a higher thrust range of 22,000–44,000 lbf (10,000–20,000 kgf), making it suitable for modern narrow-body aircraft like the C919.

Design and Materials: The CJ-1000A uses composite materials for fan blades and a two-spool design with a 10-stage high-pressure compressor, similar to Western engines like the CFM LEAP-1C. The JT8D is a mature design with less sophisticated, traditional metallic materials.

Status and Application: The JT8D has over 673 million flying hours and is still in use on older jets like the MD-80. The CJ-1000A is currently in testing, with, in some reports, positive results, aiming for commercial use around 2026 to reduce China’s reliance on foreign engines.

@DP:

All good points but the comparing was on the reliability and efficiency as a general comparison for stage of development.

So yes, China has the blueprint for the tech, even insert composites, but they don’t have the experience in making it work.

Their fighter engines look to be getting the thrust needed, but they suffer on reliably and TOW.

Any civie engine is going to have to go through the same learning process. Its not the tech that holds you back, its the IP of how to make the tech work and dance for you. Unless they bust into PW or GE etc computer system and get the process for each bit of tech, nope, you have to get it the hard way.

That is why patents are absurd. Its an idea. Anyone can steal the idea. Try to enforce it in China.

China is willing to pay the price on fighter engines, but civie engines means a direct competition with what works and you take serious hits when it does not work (see LEAP, PW1000, Trent 1000/TEN) . Those all had serious issue from firms that have the advance tech and methods at their fingertips. Successful fighter engines in two cases as well.

All are solved or being solved. China is just at the start of the JT-8 era in figuring it all out.

Jet engines started late 30s, a successful engine for commercial was not until 1956, and those were not the ultra sophisticated engines we have now.

Engines are also just the hoorah. 75% of the C919 is Western kit. Going to take a long long time before China could build a 100% Chinese aircraft.

Can China get there? Of course they can. But they are not going to get around the learning curve.

As we saw on the C919 hull, they go conservative when faced with a choice. They literally have to, its a PR disaster for not just COMAC, but the Indochinese government if it fails.

Heads generally do not roll there anymore but stuffed into a long time prisons cell yes. And its, Conrad, do you want to risk a crash (call it the get out of a conservative decision free card)

Engines impacting an aircraft are no different. Huge issue if they fail and worse if they cause a crash. Failures are so public that can not be swept under the rug.

I can see the China Airlines, uhh comrade, had you thought about selling those new engine C919s to Laos?

Trans

“had you thought about selling those new engine C919s to Laos?”

after they (CJ1000 engines) start flying on C919 in China, why not…maybe by the early 2030’s (after mass production starts)

Trans…does the 737 FAL have this?

Article titled “A Glimpse into China C919 Aircraft Smart Factory”

“This network integrates 5G wireless connectivity with time-sensitive networking to create a hybrid communication backbone that connects every sensor, robot, tool and worker across the final assembly line”

https://metrology.news/a-glimpse-into-chinas-c919-aircraft-smart-factory/#:~:text=Shanghai%20mega%20factory%20creates%20real,Commercial%20Aircraft%20Corporation%20of%20China).

Google AI

The C919 smart factory in Shanghai is a next-generation aerospace production facility utilizing a 5G-enabled industrial network and digital twin technology to achieve high-precision assembly. Developed by COMAC and Shanghai Jiao Tong University, it features real-time tracking of components, smart tools, and technicians to ensure quality and speed, featuring advanced AI monitoring.

Key Features of the C919 Smart Factory:

5G & AI Integration: The factory uses 5G wireless connectivity combined with AI algorithms to analyze live video feeds from cameras, immediately alerting supervisors to safety violations or assembly errors.

Digital Twin Technology: A,virtual, real-time replica of the assembly floor mirrors physical production, allowing technicians to monitor the status of the aircraft and optimize workflows.

Smart Tools & Tracking: Wireless sensors, including gyroscopes and laser rangefinders, track components and tools to ensure proper installation, significantly reducing quality issues.

High-Volume Production Focus: The facility is designed to support, with around 50 C919 jets planned for production in 2025, accelerating the delivery timeline

@DP:

Nope, Boeing has something better. An established system that makes 42 MAX a month vs 5 a year.

Of course COMAC built to the latest whiz bang specs and tech.

Their goal with all of it? 150 a year.

42 planes (and gong up) on your assembly lines are worth a whole lot more than a facility that does mass production on paper.

State Controlled business are bloated and incapable of rapid adjustment. Worse when the build of X is the Apple of the Regimes eye.

Comrad, there will be NO crashes.

Trans “Of course COMAC built to the latest whiz bang specs and tech.”

You are missing the point about production innovation, China’s commercial aircraft industry partners with their universities while the US focus on subcontracting to third tier suppliers that have limited technical breadth and depth.

P&W has an issue, but in the end it is the airlines/leasing companies that pay both Airbus and P&W so keeping them flying on what they operate should be prio 1. So I can understand P&W decision to allocate engines and parts to the airlines. P&W has a long tradition of improving its engines from poor reliability to good industry standard, just take the JT9D as an example, starting with approx. 500hrs on wing for the JT9D-7A on the 747-100 to +18000 hrs on the JT9D-7R4

ATR delivered fewer aircraft in 2025

DAHER delivered fewer TBMs in 2025

AIRBUS is not happy with GTF deliveries on the A320 production lines in 2025 and likely in 2026 , may be 2027.

EMBRAER and AIRBUS continue to increase their deliveries with the E2 and A220 equipped with GTFs in 2025.

Question: As far as I know, the powder issue concerns all GTFs. Could PW group ( US and Canada ) make internal choices to prioritize engine production based on their position as the sole source and the principle that it is better to have a satisfied airline with a fleet that flies, knowing that it can wait for new, more fuel-efficient aircraft, and that at the same time, the aircraft that flies generates orders for spare parts and complete replacement engines with a higher margin than the engine for FAL?

Does the “advantage” version of GTF A320 allows PW to ask airlines to wait a little bit more than for E2 and A220 where at my knowledge there is no planned “advantage” version in the near future? .May be for the A220-500 in 2030?

E2 as I understand it got improved versions that were a lot better. Not fantastic but better than A220/320.

A220 suffered as bad or worse than A320. I suspect the advantage is across the GTF line on upgrades.

I sort of remember PW saying they can insert fixes as well vs a whole package and are. Engines coming out of the shop will have the latest fix (assuming parts are there).

PW has to keep its nose to the grindstone. Airbus has to live with their choice of a 2nd engine. LEAP has its issues as well, not as bad but it too has a new improved variant.

@TW

The E2 and A220 engines are basically identical

The point is the E2 started ramp up latter and got engines with some of the improvements. They are no immune but not grounded in the same percentages.

Embraer had a couple of years before they took delivery and problems were being found and fixed.

“Transport Canada has certified General Dynamics’ Gulfstream G500 and G600 business jets, following threats from U.S. President Donald Trump.”

“A spokesperson for the office of the transport minister says the government is still discussing the certification of other aircraft with the U.S. Federal Aviation Administration.”

“The government has yet to certify the Gulfstream G700 or G800 models.”

“A government document says the G500 and G600 were certified on Feb. 15.”

“The G700 and G800 have been flagged because of possible de-icing concerns.”

How much incentive does P&W (or RR or CFM) have to keep everyone happy? They seem to be making massive profits no matter how many warranty returns they have to eat.

Huge incentive. Those engines are the next generation of profit and they are not making any money on them, loosing money offset by other profitable programs.

Right now its who they are trying to keep happy. RR has lost the Trent 1000 market, so their efforts are going into the NEO engines.

GE has one new program in the form of the 777X engines, that is not producing profits either. It won’t until routine maint based on the specs committed to arrive.

PW has a nice market in F135, currently they are not the choice for F-15.

So yea, the GTF is a huge deal and they need to get it sorted (and appear to be and have).

They are in a binary decision situation, they can’t keep both Airbus and Airlines happy so they have elected to keep Airlines happy and Airbus has to live with it as its an engine choice and Airbus has to build the aircraft with the engines the customer wants.

Ideally they don’t have to make that choice but its not ideal and they are going with where the bread and butter come from.