Leeham News and Analysis

There's more to real news than a news release.

Fuel prices up sharply, but not sustained at record levels–yet

Subscription Required

Now open to all readers

By Scott Hamilton and Karl Sinclair

March 28, 2026, © Leeham News: Oil prices skyrocketed this month with the beginning of the 2026 Iran War.

Yet, as sharply as prices spiked, they are not yet a record relative to inflation-adjusted prices since the 1973-1974 OPEC-inspired oil embargo and other regional or global events, an analysis by LNA shows.

West Texas Intermediate Crude oil prices topped $100/bbl. Brent crude briefly hit $197/bbl on March 20. On March 27, Brent topped $100.

Some airlines worldwide hedged fuel against dramatic price hikes. Our detailed analysis is below.

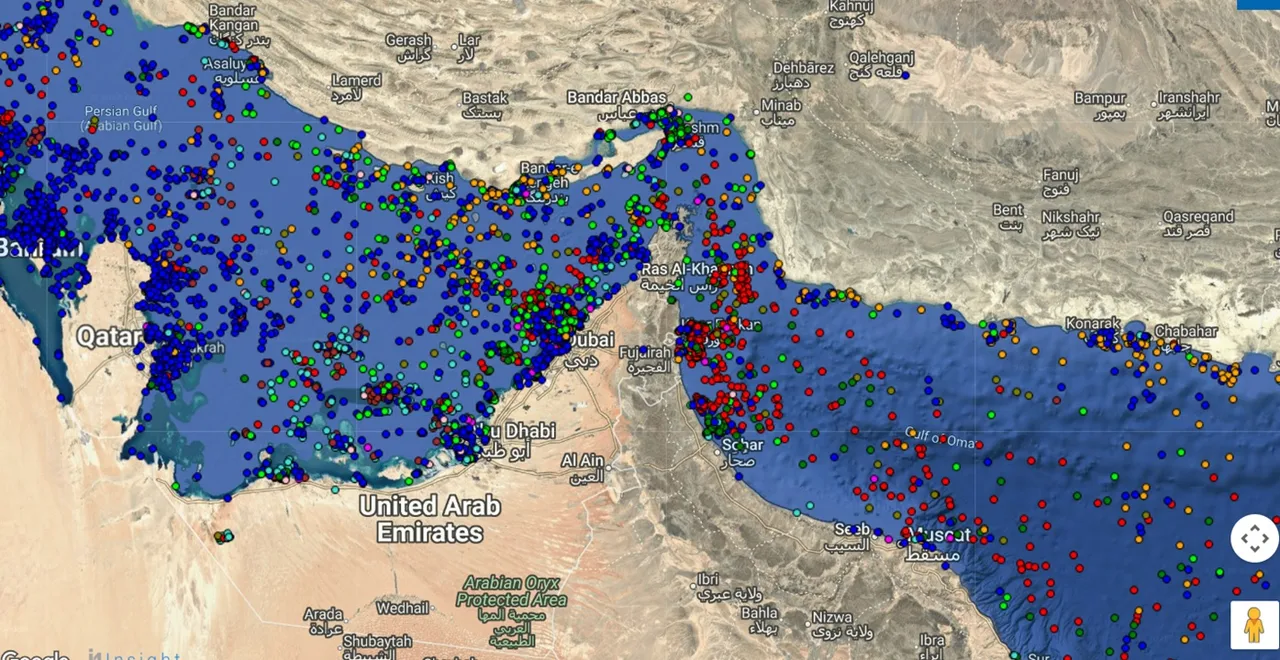

There are dire predictions that the prices could reach $170 or even $200/bbl if the Iran War continues. Bombing of Iran by the United States and Israel began on Feb. 26. Shortly after, tanker traffic through the Strait of Hormuz all but ceased. Twenty percent of the world’s oil transits through this bottleneck. Some countries, such as Japan and China, obtain more than 90% of their oil via the Strait.

More than 300 tankers are trapped. Some were attacked by Iran. Hundreds of ships of all kinds are blocked on both sides of the 35-mile-wide Strait.

Figure 1. Source: About 750 ships were trapped at the peak. Iran is allowing limited traffic through. Seatrade-Maritime magazine.

The price of oil is being whipsawed as President Donald Trump mixes messages about the war’s progress, sometimes within minutes. Sometimes the war is “won,” but more troops and ships are being sent to the region. Trump threatened to increase bombing, attack Iran’s power stations, invade an island, and then take it back. Allies are needed to reopen the Strait, and then they are not.

An uncertain future; a past to look at

Scott Kirby, the CEO of United Airlines, recently said he thinks oil will cost at least $100/bbl through 2027. At one point, he said United’s annual fuel cost could increase by $11bn; the carrier’s best profits were $5bn.

Figure 2. The cost of a barrel of Brent crude. Source: IATA. However, the peak wasn’t sustained and fell back to +/-$100 as March came to a close.

With an uncertain future, looking to the past may offer some guidance on whether airlines can withstand spiking fuel costs.

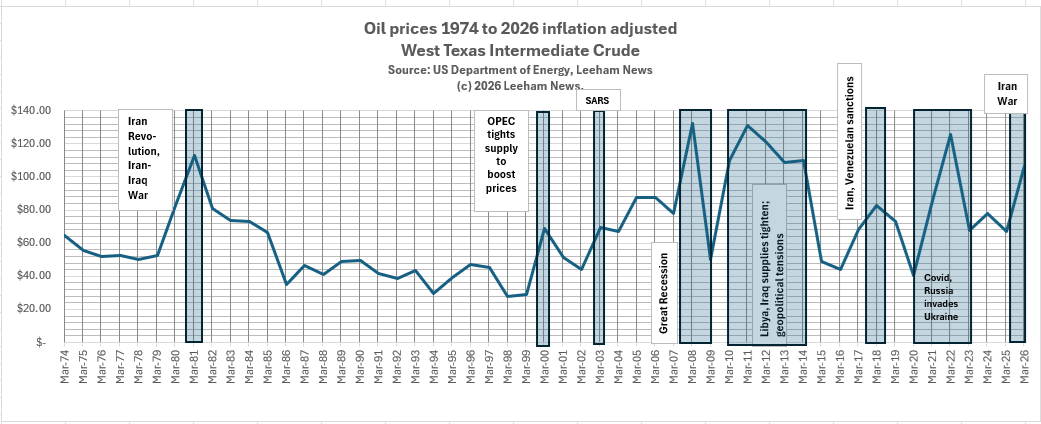

LNA uses West Texas Intermediate crude oil as the benchmark. The US Department of Energy posts historical fuel prices for the last 50 years. Throughout this period, US airlines suffered as prices spiked, sometimes dramatically. Following the 1991 Persian Gulf War, 40% of the capacity of US carriers operated under bankruptcy. Some successfully restructured, but most ceased operations.

After the 9/11 terror attacks on New York City’s World Trade Center and the US Defense Department’s Pentagon, fuel prices went down. However, the huge drop in passenger traffic drove many US airlines into bankruptcy. Some survived with federal loan guarantees. Some were turned down for guarantees and ceased operations.

The Great Recession, beginning in 2008, saw a spike in fuel prices and more airlines filing for bankruptcy, with some ceasing operations, this time including in Europe. Costs spiked again in 2010, 2018, and 2020 for a variety of global events. By this time, the carriers in the US had learned how to live through these events.

Figure 3. The history of the price per barrel of oil, adjusted for inflation. Sources: US Department of Energy and Leeham News. Click on image to enlarge.

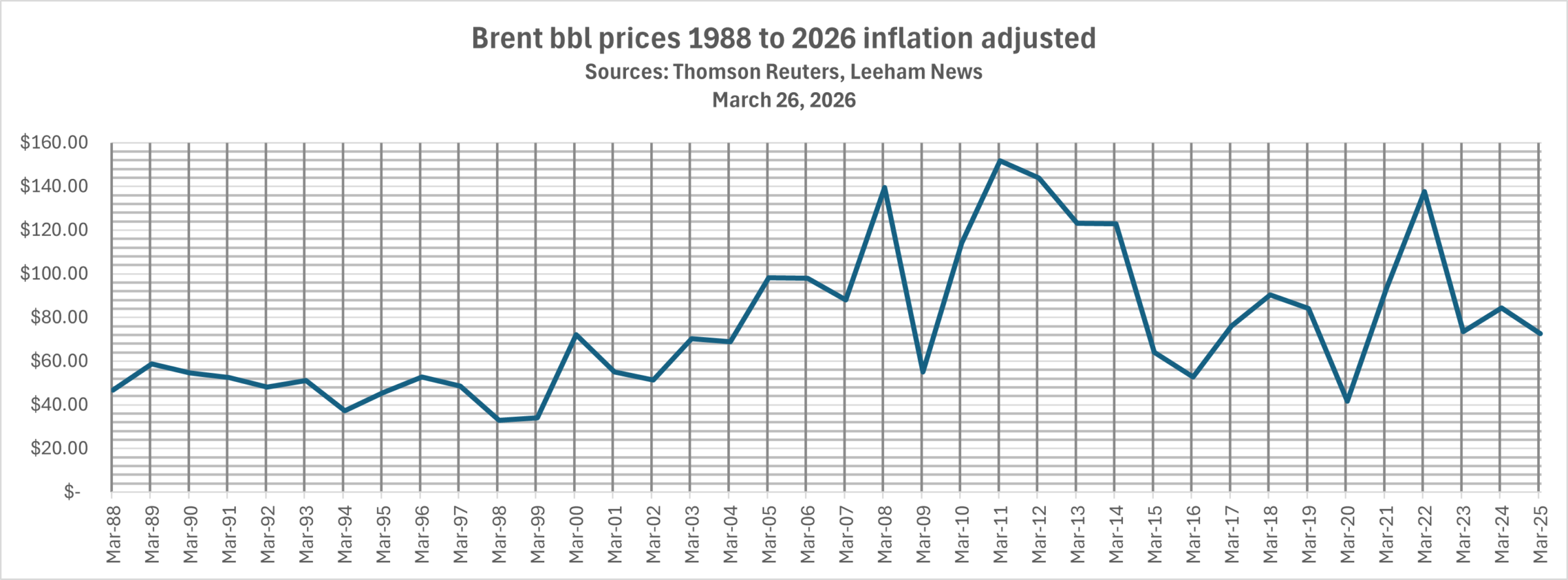

Figure 4. Brent crude oil prices, adjusted for inflation. Despite the recent spike, today’s Brent oil price is well below the inflation-adjusted peak in 2011. Source: Thomson Reuters.

Now, there’s the Iran War and concern that airlines won’t be able to survive through high fuel costs again.

On an inflation-adjusted basis, West Texas crude hasn’t blown through fuel costs of the past.

This hardly means that airlines won’t have trouble flying through this crisis. In fact, most of the Middle Eastern airlines have parked large portions of their fleets and are flying only a fraction of their airplanes. Most of these airlines have large government ownership stakes or are entirely state-owned, so no matter the losses, they are certain to survive.

Impacts on Boeing and Airbus

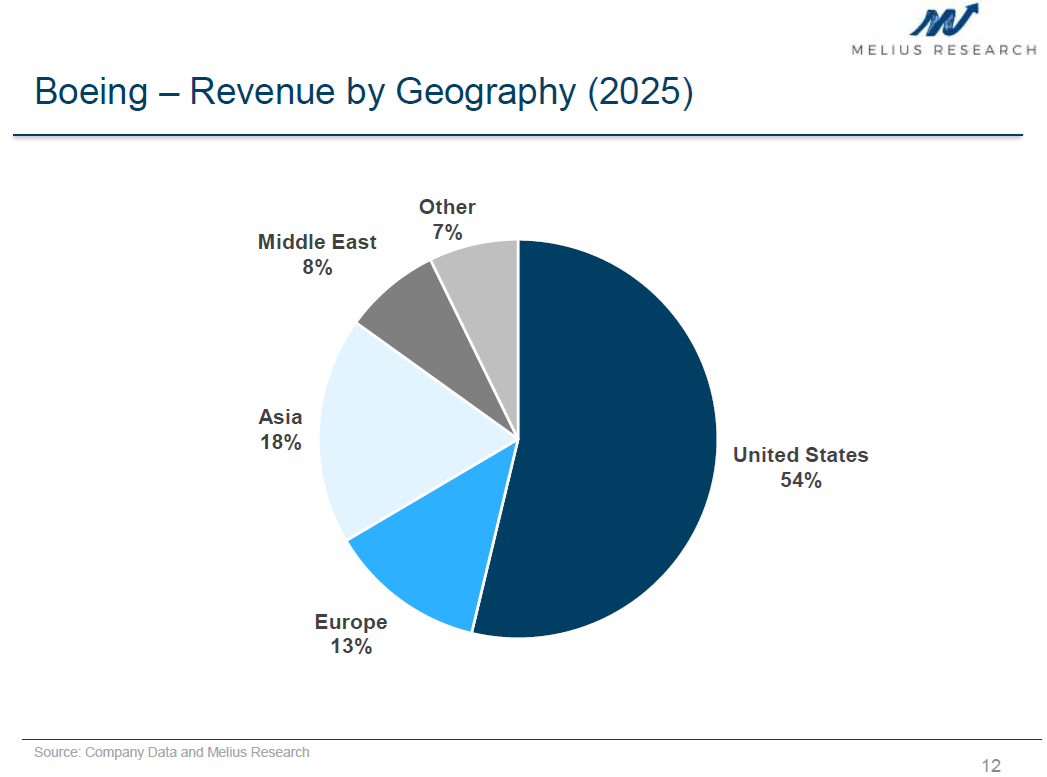

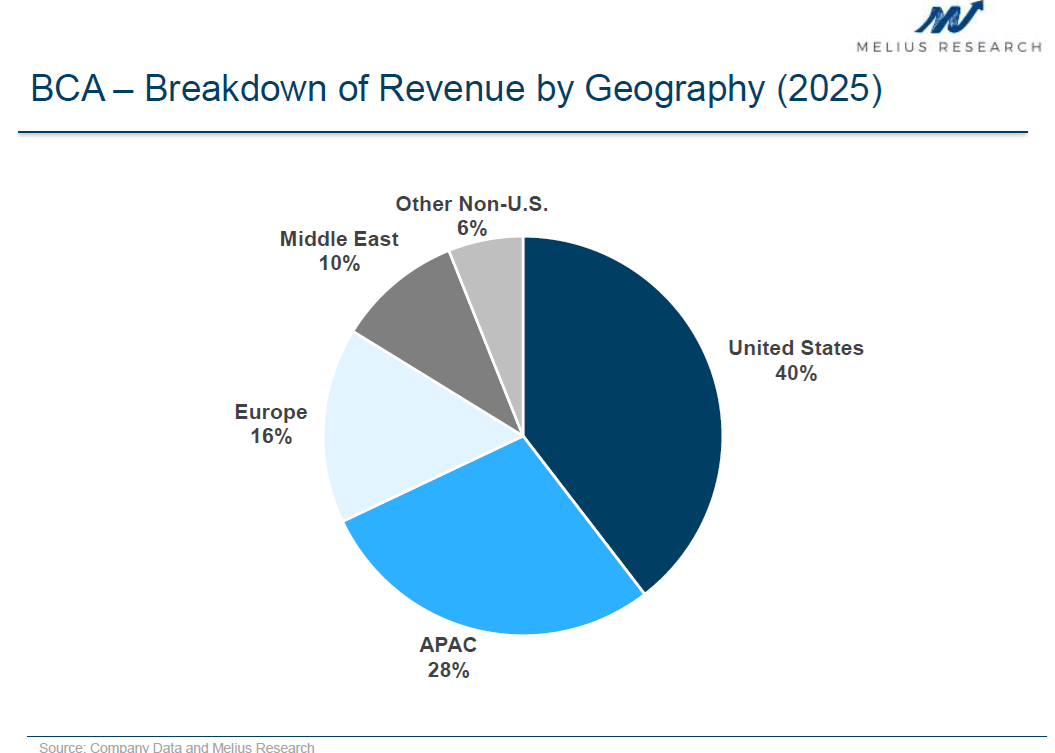

The Boeing Co. receives about 8% of its consolidated revenue from the Middle East, according to an analysis released on March 23 by the boutique investment group Melius Research. Boeing Commercial Airplanes receives 10% of its revenue from the Middle East.

Related stories

- Iran War threatened Boeing in more than just orders

- Middle East conflict’s impact on Airbus and Boeing

Figure 5. The Boeing Co. gets about 8% of its revenue from the Middle East. This includes commercial, defense and services. Source: Melius Research.

Figure 6. Boeing Commercial Airplanes gets about 10% of its revenues from the Middle East. Source: Melius Research.

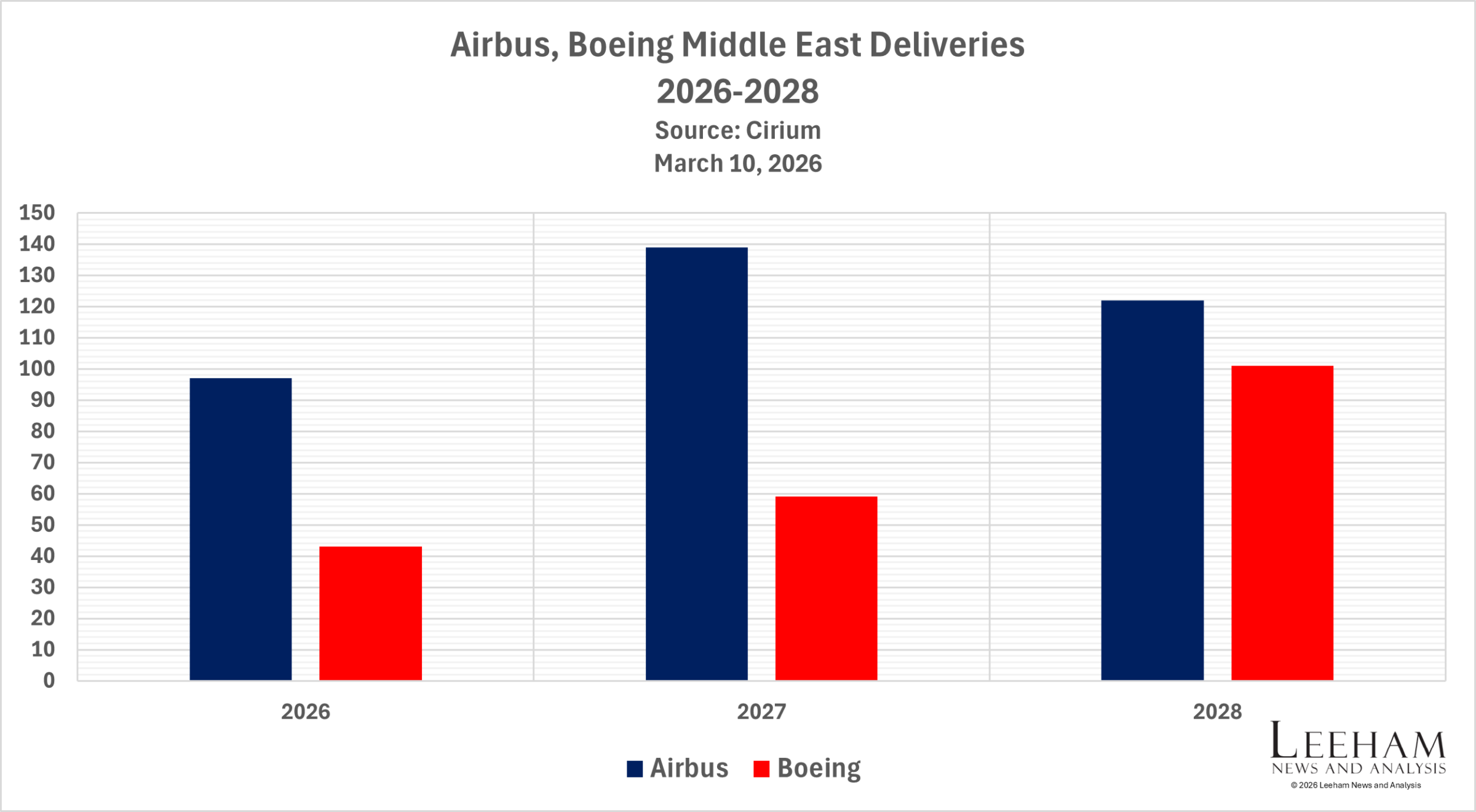

No such study is recently available for Airbus, but LNA published an analysis comparing the backlogs and near-term deliveries of Airbus and Boeing to Middle East customers.

Figure 7. The current backlog of airliner orders destined for the Middle East. Sources: Airbus and Boeing.

Figure 8. The delivery stream through 2028 from Airbus and Boeing to the Middle East customers. Sources: Airbus and Boeing.

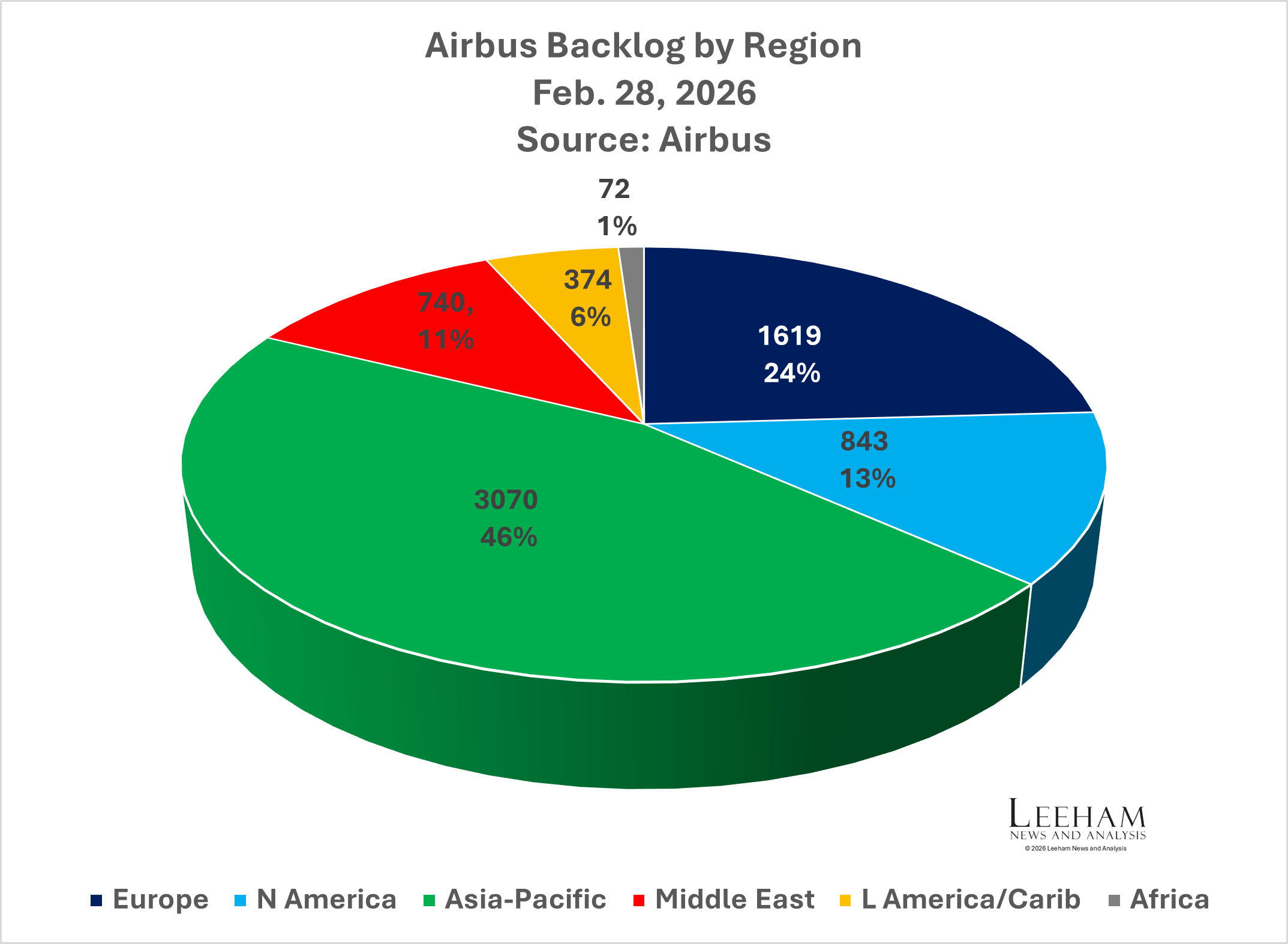

Using Airbus’ monthly report, Middle Eastern airlines represent 11% of Airbus’ backlog. This is a mix of single- and twin-aisle airplanes.

Figure 9. The Middle East represents 11% of Airbus’ current backlog. Source: Airbus.

Fuel Hedging

Airlines around the world have used a strategy called fuel hedging to mitigate potential price spikes in jet fuel.

Hedging is a technique that any company that uses large amounts of fossil fuels can employ, including airlines, cruise lines, and trucking companies.

A corporation can purchase a variety of futures contracts, which cap the cost of fuel for a determined period of time. The company usually pays a premium over the current market price.

Typically, if an airline does not hedge, it is confident of one of two things:

1) The price of oil will stay low or decrease in the future

2) If the price of oil rises, it will be able to pass those costs onto customers

Southwest Airlines used an aggressive fuel hedging strategy to great effect from 1999-2008, which saved it over $4bn when oil prices rose.

The downside to fuel hedging is that if the price of oil falls, an airline is paying more for a hedged position than a competitor who is paying market rates. Southwest discontinued hedging for this very reason when the price of oil plummeted as the Great Recession got underway.

The Crack Spread

In the aviation industry, the price of oil is just one component of what airlines pay for jet fuel.

As noted in the IATA table above, there is an added expense to the price of a barrel of fuel, known as the crack spread. This is the cost associated with “cracking” the extracted product from crude oil’s long-chain hydrocarbons into useful, shorter-chain petroleum products.

There are other factors involved in determining those costs, such as refining capacity, the type of oil being refined, foreign exchange rates, and the demand for the different refined products.

The proportion of what can be produced from a barrel (bbl) of crude oil can be varied by the refinery to a degree, depending on market demand. There can also be seasonal differences, such as a spike in demand for heating oil, during the winter months.

In short, it is the profit that is made by oil refineries. For the week ending March 20, the crack spread is $86/bbl.

Exposure

According to a Reuters report on March 12, American carriers were not hedged to a significant degree at the outbreak of hostilities and thus face the greatest exposure to higher jet fuel prices.

However, Delta Air Lines owns Monroe Energy LLC, which owns the Trainer Refinery in Trainer (PA). This facility has a capacity of 185,000 bbl per day. Delta spent ~$100m to transition the refinery to produce ~40% of its capacity as jet fuel.

Delta will be able to profit from the increase in the crack spread, despite higher crude oil costs, which will drive up airline operating costs. It’s a pseudo-fuel-hedge position, as it will sell any production overages back into the market.

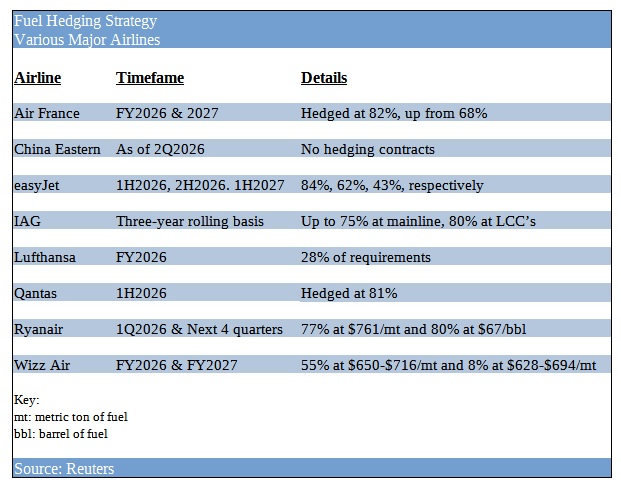

Below is an abridged list of select airlines and their unique fuel hedge positions:

Figure 9. Few airlines are hedged against spiking oil prices. Source: Reuters.

Yield management

Known in the airline industry as the “dark science,” maximizing revenues and load factors on a flight is part computer software science and part crystal ball gazing.

For some, it starts 330 days before a particular flight, and prices shift accordingly as seats fill or remain unsold.

Sell too many seats at a low price, too far out, and you might not leave enough seats open for last-minute travelers, like the business community. Conversely, holding too many seats in reserve risks having them go empty come flight time.

Delta flew with a load factor of 84% in FY2025 (85% in 2024) and is consistently near the top of the profitability chart among US airlines.

Typically, legacy carriers will aim for a ballpark load factor of 70% some 30 days before a flight. LCCs and ULCCs want that number to be in the neighborhood of 80%.

This is not a rule written in stone, and airlines adjust from route to route. Some higher-traffic routes may have a lower threshold (think Chicago to NY on a Friday night, to accommodate the business crowd, or Thursday nights from Washington, so that members of Congress can return to their districts on Friday to attend to important local affairs). In those cases, perhaps a 60% load factor 30-days out makes more sense.

In contrast, routes with lower traffic patterns might want to be sold to a higher capacity, as last-minute travelers are a rarity in those markets.

This leaves enough seats open for airlines to consistently raise prices as the departure date approaches. Walk up to the counter on the day of departure and you are paying the full fare price for that seat. Needless to say, those last-minute tickets sold are the most profitable for the carrier.

Herein lies the problem when oil prices skyrocket.

If 70% to 80% of a flight is sold out 30 days prior to departure, airlines cannot suddenly pass on a fuel price increase to customers flying on those tickets. For the week ending Feb. 27, jet fuel had a manageable average price of $99/bbl, with a crack spread of $28/bbl.

Fast forward, and by the week ending March 20, it is $197 with a crack spread of $86/bbl, less than 30 days later. One of the biggest hits that airlines will have to absorb will be at the end of 1Q2026 and early 2Q2026, when tickets were sold to customers in advance at a lower, non-adjusted price to account for fuel increases.

Fuel costs have doubled, and carriers have no way to pass on that added expense to those tickets.

In summary

As detailed above, hedging strategy is as unique as each airline and the country they are based in, is. What works for one does not fit for others.

Some airlines prefer to risk a potential price spike in the future to generate greater short-term gains, while others prefer the security of paying a little more now, knowing this is the most they will have to pay in the future.

Those who have gotten caught out naked, without the cover of a fuel hedging strategy, are at the greatest risk. They will undoubtedly attempt to mitigate those costs by passing them on to customers through ticket price increases and fuel surcharges.