Leeham News and Analysis

There's more to real news than a news release.

Fuel prices going forward

By Bjorn Fehrm

Source: Google images.

January 16, 2017, ©. Leeham Co: Oil has now doubled in price since the lowest point a year ago, with a present level of $50-$60/barrel. What is the trend going forward?

We are at the Growth Frontiers 2017 conference in Dublin, where Paul Horsnell, Head of Commodities research at Standard Chartered and Mike Corley, Mercatus Energy Adviser, gave their view on the future of oil prices.

The air transport market has seen a worldwide passenger and profitability growth over the last 12 months. The driving factors are increased appetite for air travel, especially in Asia, and cheap fuel.

Supply and demand

The world market price for crude oil (and by it the price of jet fuel) is decided by supply and demand. The demand-side of that equation is predictable and stable. The need for energy, for industry or private use, is not changing fast.

This is not the case for the supply. The past slump of oil prices from over $100/barrel to under $30/barrel was driven by the oil producers in OPEC (essentially the Middle East producers), wanting to weed out new competition that had come into the market.

The OPEC producers had the strategic advantage of low production costs, below $10/barrel. The new competition by, predominantly US shale oil producers, had a production cost north of $60/barrel. By forcing the world market price to dip well below $60, OPEC would make the US shale oil production unprofitable.

With it, several other producers would be forced to sell oil below production costs. Examples would be North Sea Oil (production cost around $60/barrel), Russian oil ($70/barrel) and oil from South America.

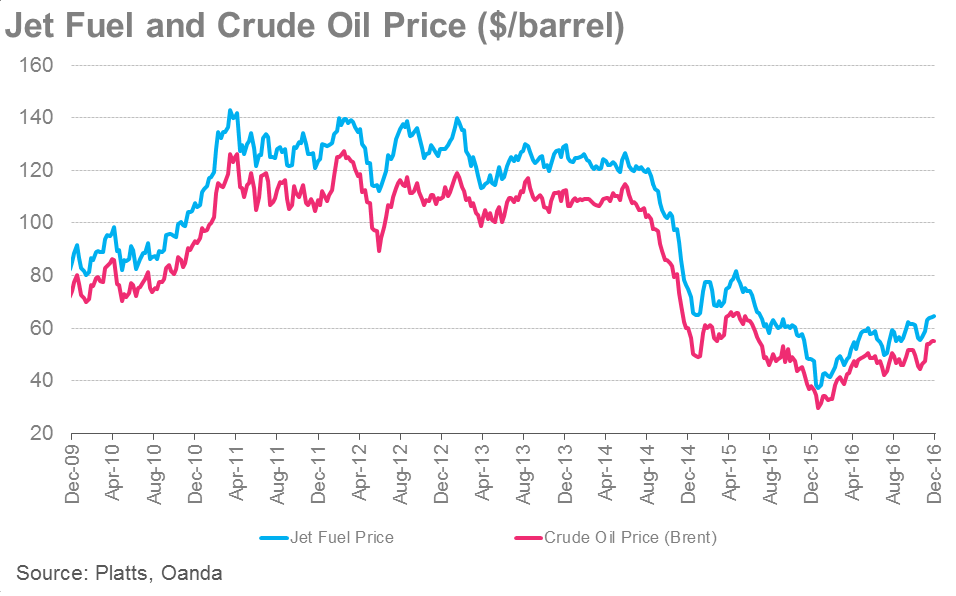

Since price hit bottom at $26, it has now gradually climbed up to $60/barrel, Figure 1.

Figure 1. Oil crude price development over last seven years. Source: IATA.

The big question is now, what happens next?

Oil prices in 2017 and beyond

Horsnell/Corley said the low oil price had a profound impact on the market. Producers stopped investing. The capital behind the expansion of shale oil in the US disappeared as fast as it appeared. Longer term investors in other forms oil exploration decided that this was not an attractive market anymore.

Those that had no choice but to slug it out (North Sea, Russian, South American producers) stopped investing. They continued production but planned capacity increases were stopped.

For many producers the oil at $60 is just at the break even, where they get their production costs covered. As the investors are no longer there, they will avoid making continued losses but their capability to follow an expanding market is hurt.

The result is the strategy of OPEC, to stop alternate source competition, has succeeded. The experts see it as in OPEC’s best interest to keep a steady oil price going forward with a steady, slow increase from the present level.

They don’t see what constellation should argue this with OPEC. The risk willing capital that came into the market to exploit alternative sources for oil has backed out. There are easier ways to earn return on invested capital than to pick a fight with behemoths like OPEC.

Shale oil is not only available in the US. It can even be extracted in continental Europe. The Shale Oil Genie can’t be put back in the bottle. As soon as prices go up enough, shale oil production can quickly start rising again.

Data seem to indicate that the worst has passed and a new upswing has begun.

http://www.wtrg.com/rotaryrigs.html

However, I believe the hale Oil “Genie” to be a mirage: a financial scam rather than a panacea. Shale oil extraction is only really done in the UK and the US – where it is possible to find a lot of gullible investors to buy newly drilled well in the hopes that their production will cover the buy-in cost and then deliver a profit. Just just doesn’t happen, though. The typical production curve of a Shale-oil well decreases radically after the first year and keeps decreasing so in subsequent years. So, what looked productive at first become highly unproductive withing just a few years and costs are never recovered.

But have no fear…for in the Great USA the Shale Oil Scam will return in force once oil rises to above $80/BBl. The governments of other countries typically don’t allow such scams….that’s why there’s no real shale-oil drilling outside North America.

It’s a bird…It’s a plane….Naw, it’s just another fracking unproductive shale-oil well!

What your analysis ignores is that many producers have worked hard to reduce their break-even point. This is particularly true of US shale oil producers who will dramatically ramp up production if oil hits $60 because that is a level that is now extremely profitable for them.

The business world does not stand still in the face of shocks.

Excellent points Bruce on the shale industry. They are now making money at $29 a barrel in some areas of the Bakken and other areas.

Shipping their product to market by rail isnt any good for their cost structure. The difference is that Bakken LC to East Coast by rail is say $15 bbl while piped- when available – is $10bbl.

It seems that just going to mid west & central states lowers the transport costs but of course the coastal locations get higher prices as they rely in imported crude.

The A330NEO is dead in the water at $55 oil.

Maybe the ceo but the A380neo may come back to live.

How so?

Some oil producers need the cash, hence they must pump oil and gas to get the needed yearly income. If the price drop they need to ship more. With Kuwait, Algeria, Irak and now Iran soon producing at full steam for the World markets there is a pressure on price. There might come regulations how much oil and gas that can be burnt yearly not to cause too high Earth average temperatures and thrus water shortages. That would put a downward pressure on oil&gas demand. Those countries exceeding limits would have to accomodate refugees from water shortage areas.

Break even is a lot lower if you aren’t investing. Old shale fields with infrastructure seem to cost $40 bbl but the moment you go to a new field it is $80. Those $40 bbl areas are getting worked as quickly as they can and after that I don’t see new money comming in to develop more expensive areas, it will take a few years before the infrastructure and geological experience of those areas is good enough to bring costs to $40bbl, and esp US investors don’t have that kind on patience, the excitement around shale was quick ROI, and take that away and investors loose interest. Off shore is around $60 in old North Sea areas but these are closing down as it doesn’t pay to keep investing. New off-shore area in Europe is the Barents and Kara seas. Norway has a 10 billion barrel deposit near the Russian border which they are going to start developing this summer and Statoil has the lease on the Russian side where there is probably more. Two other areas in the Barents are promising and under exploration. Big improvements off-shore and Statoil say the Kara sea project is viable at current prices. I sort of think OPEC will remain the “swing producer” in the future and keep prices in the $60-$80 range so as to keep frackers from opening up new areas and don’t forget, Bio is about $80 bbl last I heard, so $60-$80 keeps them in chack unless legislation is enacted to help them.

The other piece of the shale business in the US is the aprox 5,000 drilled but uncompleted (DUCs) wells that exist. These wells can be finished and brought into production for 1/4 the cost of drilling a new well.

And at the same time drilling costs have fallen as people have learned more efficient methods.

The shale producers have a much more valuable product than typical crude. The high light fraction content makes excellent chemical plant feedstock. And the surge in NatGas production has lead to that becoming a commodity of its own no longer tied to oil prices.

The landscape has changed, and US is likely to remain the worlds second largest producer of hydrocarbons for decades to come, largely thanks to OPEC.

These wells are called the fracklog and only come into play when it is worthwhile completing them. That there are so many tells you the price doesn’t justify bringing them online. If you have drilled a well that needs $70 to recover your investment you aren’t going to bring it online unless you can help it with oil at $50-60. There are some big companies in the fracking business, not just small ones, and companies like Shell and Exxon don’t have to pump and prey, they can wait for these wells to be profitable.

Its a see saw.

Oil shale operators are consolidating and getting more efficient at what they do.

They may choose to let the price drift up as well so they can make more money.

If someone can cut in a field at a low cost then that will affect it and they are still finding fields like that (odd as it sounds) next to in production fields.

Where is goes I think defies analysis because there are too many things in play (oil filed pun intended) .

Forecasting it is impossible.

Russian is cutting its defense spending dramatically, so they do not expect it to go back to the happy days anytime soon.

http://graphics.wsj.com/oil-barrel-breakdown/

Here is the cost of production for major producers. Libya has the capacity to double give some stability, Iran has huge upside as does Iraq. Canada has the ability to a 2M bbl/day over the next 5 years then there is a billions of barrels already in storage….

Maybe you should do a follow-up to this article.