Leeham News and Analysis

There's more to real news than a news release.

Embraer presents 3Q2019 results.

By Bjorn Fehrm

November 12, 2019, ©. Leeham Co: Embraer announced its 3Q2019 results today. The company delivered a report which disappointed analysts regarding revenue, earnings and free cash flow. Commercial deliveries were 17 jets (15 in 2Q2018) but only two of these were of the E2 generation. Total E2 deliveries now stand at eight jets after 18 months of deliveries, a very low figure.

The Joint Venture with Boeing is now delayed as the European Union says it sees a risk for diminished competition in the Airliner market. Embraer will close the carve-out of the Commercial Aircraft division and its services at the end of the year while waiting for final approvals.

Embraer results hit by carve out and early E2 production costs

Embraer’s 3Q2019 revenue was $1.176bn ($1.159bn 3Q2018) with profit at -$21m (€54m). The loss includes carve out costs of -$35m. Embraer delivered 17 (15) commercial jets and 27 (24) executive jets in the quarter. Free Cash Flow was -$0.257bn (-€0.163). Cash and financial investments are at $2.175bn ($3.138bn). Backlog is at $16.2bn ($17.4bn).

The figures show how the liquidity of the company has shrunk by $1bn over the last year and free cash flow has shrunk with $100m. We see the reason for the lowered results in the costs of E-Jet E2 initial production. A new aircraft program is not contributing to the bottom line until well after 200 units. Right now, every delivered E-Jet E2 eats into Embraer’s profits. This probably the reason for Embraer keeping deliveries at about one aircraft per quarter so far for the E2 program (eight deliveries in 18 months). A higher delivery rate would lower the Commercial division’s results and it could negatively affect the Boeing Joint Venture valuation.

Commercial Aircraft, which represents 35% of revenue (Figure 1, 33% in 3Q2018) didn’t sell any aircraft in 3Q2019. The backlog shows one order and three options were lost in the quarter. Deliveries of large Executive jet is finally picking up with 12 jets delivered compared with seven 3Q2018. Defense shows a loss in revenue compared with last year whereas Services are slightly up.

Figure 1. Revenue by division for Embraer 3Q2019. Source: Embraer.

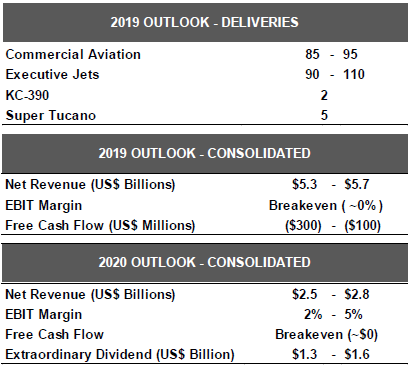

Guidance for 2019 was changed as the merger with Boeing for the Commercial division will now be delayed. Embraer also delivered guidance for 2020, with the new guidance summarized in the table below (Figure 2).

Figure 2. Updated guidance for 2019 and 2020. Source: Embraer.

The guidance for 2019 is unchanged except for no expected merger with Boeing in the year. A Free Cash Flow guidance has been introduced and the extraordinary dividend from the Boeing Joint venture has been moved to 2020. The new 2020 guidance has the extraordinary dividend (the payment surplus from Boeing) a bit lower than previously guided.

E-Jets

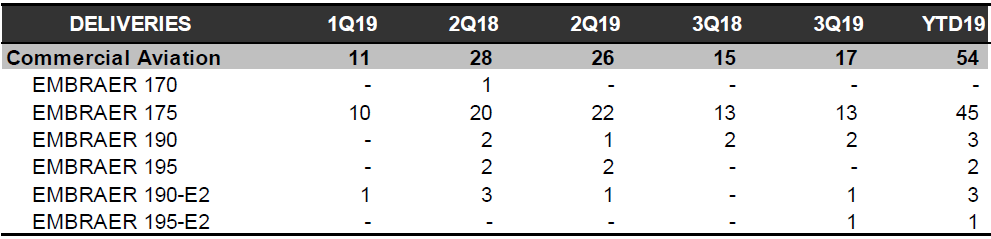

Embraer is still dependent on deliveries of the E175, mainly to the US Scope Clause market, Figure 3.

Figure 3. Commercial aircraft deliveries. Source: Embraer.

The E2 program has only delivered four E190/E195-E2s in its second year of deliveries. This is a delivery rate that is troubling. At our visit a month ago, we could verify there are no special parts or manufacturing problems. The reason could be these initial aircraft has a much higher production cost than their sales price. The delivery rate is kept down to keep the losses from mounting in the Commercial division, which could affect the Boeing Joint Venture valuation.

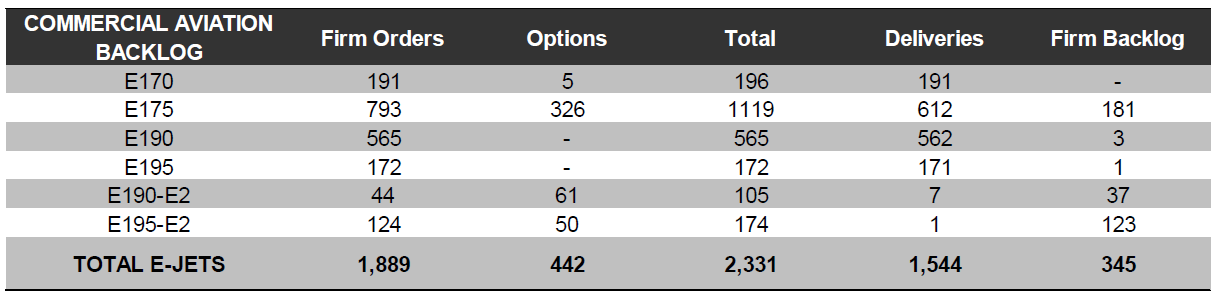

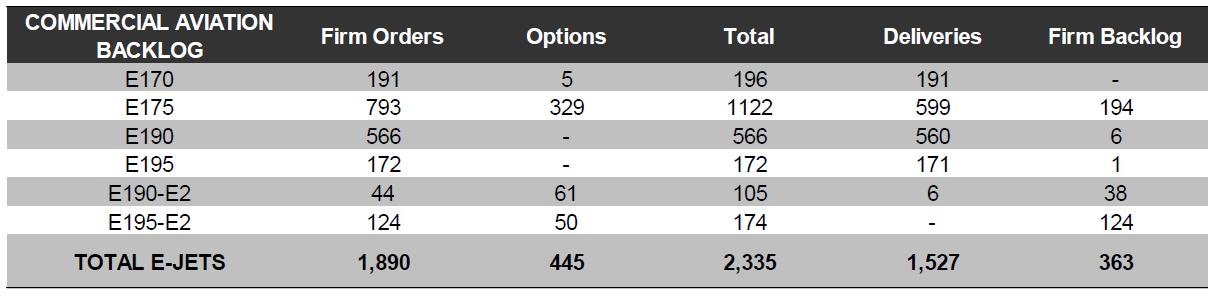

There were no sales in the quarter as seen in Figures 3 and 4.

Figure 3. Backlog and Deliveries for Commercial jets 3Q2019.

Figure 4. Backlog and Deliveries for Commercial jets 2Q2019.

The firm backlog is now one aircraft lower than the second quarter backlog minus 17 deliveries and the options column has lost three E175. The very low delivery rate of the E2s is evident in the tables, E2 deliveries will be closely watched in the next quarter.

Business jets

The margin richer mid-range business jet has finally picked up sales and deliveries. It’s the new Praetor jets which deliver best in class range and comfort. The smaller Phenom 300 is also selling well.

Defense & Security

The quarter saw the first delivery of the KC-390 tactical transport to the Brazilian Air Force. The next aircraft will be delivered in the fourth quarter. The continued flight tests are now focused on tactical capabilities.

Interesting that its fine for Airbus to buy BBD A220 out and Boeing can’t buy Embraer.

As he A220 actually was a competitive product to the sing aisle market with the ability to make it a killer of both 737 and A320.

Embraer is just one of many regional airline competitors.

Me thinks they let the cows out of the barn and are now closing doors.

Of course the KC390 (not part of the direct deal) will knock the A400 off its poorly executed kiester.

When Airbus and Bombardier did their JV there was more competition as Boeing and Embraer were separate. Thats the difficulty of waiting till the consolidation has completed, you are the one removing the last hurdles. Additionally Cseries covered only around 110 seats plus and the CRJ and DHC products werent included – and since have been sold separately. Boeing is getting the whole 75-145 seater market. There are no multiple regional jet producers, only Embraer -soon to be Boeing, and Mitsubishi now)

Precisely. That is the decisive difference!

It is not a sabotage action or transatlantic battle, it is about the competitive landscape past merger. Magic number is usually 3. Do you have 3 credible competitors in relevant market post merger of not?

In the C-series issue you could say: 319 with C, 737-700, E 195 and maybe CRJ 1000, so yes.

I guess it will depend on if the Commission considers the CRJ 1000, SSJ, etc serious competitors or not.

Ah, the EU Competition Commission – always looking out for the best interests of the whole world and applying the Law(tm) impartially and without bias. As a non-EU person I feel so much more economically secure.

They are only concerned about EU , not the rest of the world. Its not new , remember when they opposed GE-Honywell merger , it was on the grounds of reducing competition within the EU.

That merger could have proceeded if they did not wish to sell within EU , but did not want to do so.

The US and EU have different approaches to reducing competition from mergers- within their countries. Broadly put the US ‘looks to where consumers benefit or are harmed’, while EU criteria are around ‘ size of a merged firm and market dominance’. That was the approach taken by US too more than 50 years ago, but no longer.

Embraer is clearly only a minnow compared to Boeing , but since the JV/merger only came after the Airbus -Bombardier tie up ( which didnt included its regional and turboprop lines) it can be said to remove the last competitive airframe supplier and increase Boeings dominance.

To me the Embraer tie up isnt such a problem , the future issues lie with both Airbus and Boeing dominating the aftermarket and service/maintenance areas as well. As EU can only restrict that happening in their territory, they may want leverage over Boeing if they approve the JV . Remember they havent decided to block the JV yet, just going to do a deeper dive into the issues.

Boeing claimed that MAX 7 was direct comp for c series that they took bombardier to court for dumping. EMB bragged about E2 as equally capeable as C series. Now both EMB and BA has to explain why and how they can merge to control 67% of that aircraft size market. You can build a product and gain market share bu selling it but cant gain more than 50% by buying out comoetion. This would explain why BA and EMB can’t provide all the required information that EU is looking for.

Tom,

do you think this merger won’t be allowed.

Leon,

I think politics will pay big part of it. And who knows what will happen. Boeing and Embraer not providing required information could be that they are not as interested in the tie up or Boeing is tied up with MAX grounding issue.

Perhaps one difference between BBD A220 and Embraer is that BBD was about to go bust and Embraer doesn’t need Boeing to buy it. Embraer can probably survive quite well, although the E2 must be a dilemma.

If Airbus had not bought BBD there would have been no BBD and therefore buying it didn’t reduce competition.

On the other hand Embraer is a successful business, and I imagine it can survive quite well without the Boeing takeover. This does represent a reduction in competition.

The problem is that Embraer cannot survive alone against Airbus dumping practices, selling A220 well below price while still having a costly production line.

I think that’s what Embraer did before too,

selling below price hurting Bombardier … then Karma stroke

Both Embraer and Bombardier did that, but it was to companies of the same size fighting each other until WTC settled things between them. Now it is a giant gorilla doing this.

Obviously you can’t sell below cost forever. So no one is doing that. But it takes about 100 to 200 frames before manufacturers figure out how to build an aircraft in the most cost effective way. So the early frames are always sold below cost and then it is hopefully made up later in the program.

From an account perspective different airfares deal with this in different ways.

early 787 cost well upwards of $200M to produce

… sold for much less than $90M. Again, what was you issue?

It’s a very complicated area I find somewhat confusing in terms of what the market wants in that the A220-300(ex C300) covers the same passenger segment that the A319 and B737-7 does i.e. up to 140pax but no one is really ordering many of these. Boeing had the highly respected B717-200 just below this area and were planning a B717-300 stretch to 136 passenger but ended production due to low sales and competition in the area from smaller regional jets and turboprops. The Fokker 100 also terminated.

Sales of the A319neo and B737 MAX 7 have been extremely subdued so its surprising that the A220-100/300 are selling. It suggests that operators are extremely sensitive to some other factor, maybe fuel or take-off run. Maybe scope clauses have been eliminating jets in that 80-120 seat range but now economics have made them attractive again.

The difference is the A220 is a modern aircraft. None of the others are.

A317 etc is heavy, very very heavy for its size as its derived from an A320 air frame . 737-7 is worse as its just shrunk, no fine tuning of materials to lighten it up.

The 717 dates back to the DC-9 days, and while the setup was not bad, the last 3 or 4 rows were awful next to the engines. Also a 737 mechanical aircraft some hate so much. Fairly efficient but not an A220.

The A220 is relatively light, its got an all new modern wing and it has the highly efficient (if somewhat troubled) PW GTF that are more efficient than promised.

A220 has true full pax tran continental range and even trans Atlantic.

Its also a fully modern well designed cockpit and exceeds both Airbus logic and the Boeing mantra of pilots have full control (until they don’t ala the removal of the cutout on the column that should have disabled MCAS 1.0)

You see the 787 doing long range ops due to its setup. Japan to San Jose or Boston was unheard of in the day even the pretty good 767.

Airbus did not buy Bombardier Aerospace Co

What Airbus acquired was the CSeries program, now A-220

I suspect that there is enough commonality between the E1 and E2 that deliveries of the E2 are not nearly as dilutive as you assume. Be that as it may, the slow pace of deliveries relates to the fact that most of the demand is for the E195-E2, which only entered service a couple of months ago. There have already been 3 deliveries of E2 jets since the beginning of Q4, and that number will end up at 8-10 by the end of December.

Embraer might have the same problem as Canadair had with the C-series of too expensive parts flowing in from a big number of suppliers and it is not that easy to have them reduce their prices unless volume booms. Having Boeing lean on them and replace some with 737MAX suppliers is probably necessary. Airbus is in the middle of similar work on the A220’s.

I’m not so sure of that. There is quite a difference in MTOW so probably all structures will be different, including skin thicknesses. The engines are different, Probably gear needs to be different to accommodate greater weight. Wings are new so new actuators etc.

Yes, seems to be major surgery to go from ERJ195 to 195E2. Hence most pn’s are different even though might look the same from a distance. I think the divider is if you really need the A220 range you buy it, if you don’t need it the E195E2 should be cheaper and lighter.

The A220-300 was probably Max’d out after LH told them to maximize pax count so doing a A220-500 might be harder and more expensive than a simple stretch. Still Airbus might do it with Canadian goverment money as internal competition with a light weight shorter range A220-500 as a MD80 from the 2000’s is better than having the Chinese selling them for a rock bottom price. Ideally designed for SWA reaching all of continental US from Chicago and Dallas with full pax load. With a short range minimum fuel burn A220-500 available forcing Boeing to compete against 2 different Airbus product lines. That hopefully will force Boeings hands to move HQ back to Seattle forcing all white collar workers to pass thru a few workshops everyday to their offices and getting to know new hard facts on the way.

Now seeing PFC in the 20,000 cycle area.

https://www.flightglobal.com/news/articles/south-korea-grounds-13-737ngs-with-pickle-fork-cra-462155/

Move it to 15,000 though I suspect all airlines are madly inspecting lower and lower tranches until it quits showing up.

13 in 100, is almost triple the rate of affected aircraft (early on, seen figures of ~40 for ~800 inspected). Is there a reason for this increase on South Korea’s numbers?

So far we have been given no information on the issue other than it is there and the cycles keep coming down as to when it shows up.

Until the root cause is released and some analysis of why its triggered , we got nada .

Stunning it got this far before being found.

Qantas got 10%, after it checked those planes that needed immediate checks and those who they had a longer time period to do so.

Southwest has been trouble for the NG they bought second hand, mostly from non US airlines, that had a litany of unauthorised/undocumented repairs . They were supposed to sort it all out before carrying passengers but didn’t. The reason why they had to buy some many used 737NG was their 737 classics had to be pulled from service as they started to have fatigue ruptures in the fuselage and need major and expensive rebuilds.

Southwest must feel that they are on a highwire with the 737

Its always good to be factual rather than alternative facts.

” Southwest suggested separating a group of pilots that would specialize in flying the 737-300s exclusively, since the FAA had varying, independent training requirements for the Classic airplanes. The proposed separation went over like a led zeppelin, however, and there is speculation that the pilots’ flat out refusal to accept what they believed was divisive action by Southwest led to the rapid replacement of the classic fleet in favor of the Boeing 737 Max 8.”

They had a dual classic /NG fleet for some time . Why had it suddenly become a problem

Sept 2016 and 2017 was when the last 500 and 300 classics flew in their colours, and Dec 1997 was the EIS of the NG.

For 20 years they flew the 2 types in their fleet with no pilot issues , and they suddenly after the fuselage fatigue ruptures they want to buy used 737NGs with poor maintenance history . No coincidence then that 737 classics would have had to have major maintenace repairs when they reached something like 45k cycles /50k hrs

An airline like that would have had meticulous fleet planning in advance from one type to another

Duke:

It had to do with the Pilots agreement on types and cross ratings, much like the scope clause with other airlines, SW just gave up trying to get it to work.

Some aspect in play is the 800/8 are better in the SW system overall so drop the 700/7 (though they are probably a bit sorry now)

For 20 yrs SW pilots fly both types …. its how their system of one type works. Plus they always bought new from Boeing for the maintenance advantage…until

Remember your bit about facts ..where are they

Pickle fork cracks on the E2’s. Didn’t know that.

Come on lets try stay somewhat on topic.

Might well spur some E2 sales.

If the MHI jet works out well there will be enough competition. I feel the bigger E2 jets will be succesful, the more successful 190/195E2’s are just recently been delivered. I assume they’ll be allright and keep being dominant arount 100 seats. And I foresee a big role in a 737 replacement program soon.

Boeing certainly backed themselves into that corner

MHI is only 100 seats and below. ( once they had looser agreement with Boeing with parts etc, but had to get CRJ once the Boeing had its own designs on their future market)

Embraer covers the 75-145 seat range , all taken out by JV with Boeing.

While I generally agree on non off topic posts, this is an important one and does tie into Boeing travails be it the merger or the MAX. Its also a fairly non heavy post in the specific area.

https://simpleflying.com/boeing-737-cracks-area-increases/

I will stand censored if others deem it too far out.

Pretty good summation

https://crosscut.com/2019/11/signs-turbulence-boeing-existed-long-737-max-tragedies

I’d tag it more as as “fascinating fiction”.

There is so much wrong with that story line …

forex:

“777 was on time and on budget”.

777 was reasonably on time by doubling its budget.

as topping:

787 doubled it time and quadrupled its budget. 🙂