Leeham News and Analysis

There's more to real news than a news release.

Risk Adjusted Business for leasing aircraft

By William Loh, International Aviation Advisors and

Dr. David Yu, CFA, Senior ISTAT Appraiser, AAVA Group, NYU Shanghai and Stern

Airbus A320neo. Credit: Leeham News.

Oct. 17, 2023, © Leeham News: We have seen over many years that mainstream commercial aircraft are attractive assets to own and lease. They are easily recoverable, and produced by a stable duopoly of manufacturers. In normal times, aircraft generate fairly predictable US dollar cash flows over their long economic lives. There is no near-term risk of technological obsolescence, especially for the latest generation narrowbody aircraft.

Demand for travel drives demand for aircraft. On average, the aircraft fleet has doubled approximately every 15 years as travel demand has risen by 5% annually. Passenger growth has grown by 1.6 to two times world GDP growth over the last 30 years, but these relationships have been shaken to the core since 2019.

The airline industry is a derivative of the economic cycle. It is also prone to occasional external shocks as the result of war, terrorism or as we’ve recently seen, disease. Historically the industry has a proven resilience to these shocks. Over the last 30 years, the industry generally recovered within a relatively short time, with demand reverting to the long-term trend line.

Such stability does not mean that investors should be lulled into a false sense of believing that they understand the details well enough. This is where the rubber meets the runway and good advice plus prudent models come into play.

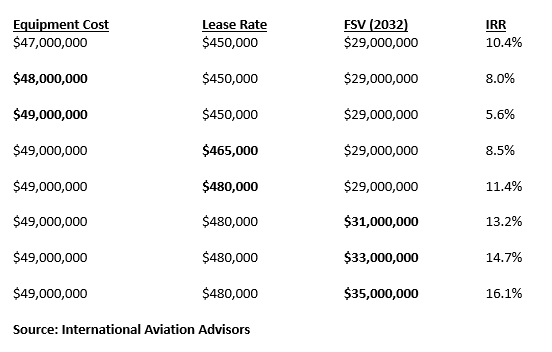

In this article, we discuss our Internal Rate of Return/Net Present Value (IRR/NPV) Model and the results of changes in some of the parameters. The main drivers of the return are normally the equipment cost, the monthly lease rate, and future sale value (FSV) (and year). Downtime is obviously also important, but we will assume none in this case. The following is a table of (pre-tax, annual) IRRs based on changes in these parameters, for a 2023 Airbus A320-200neo. Note that the parameters that have changed from row to row are in bold.

Financial Analysis

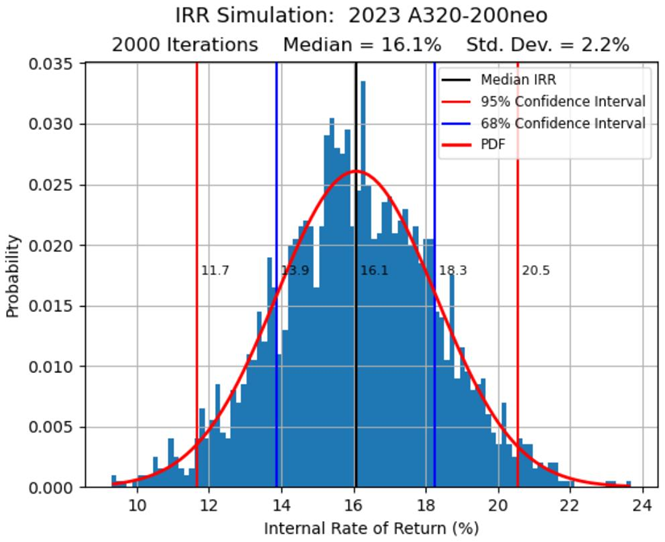

We have developed a simulation module as well, and this provides decision-makers with a probability distribution of IRRs, based on the inherently random uncertainty involved.

The simulation varies certain parameters through a User-defined range. This lets us take advantage of the computing power we all benefit from, and helps investors price deals based on understanding the reality of what might happen over time.

Simulation is the only reasonable way to take into account things like the pandemic/shutdowns, and other market changes or unexpected events that are difficult if not impossible to forecast. This makes it a powerful tool to use to forecast future values too.

We’ll go into more detail about the models in our next Risk Adjusted Business article.

Well the used to be easily recoverable.

Not only not our of Russia but a number of countries will not secure aircraft that were stolen that are flying into said country(s)

Of course lessors can take what Russia tells them they will pay. So a new reality has hit the system and do you lease aircraft to countries that will not follow their own legal system?

“So a new reality has hit the system and do you lease aircraft to countries that will not follow their own legal system?”

…that is highly, highly debatable!

Why not? If IB can peddle “century” bond from Argentina and tuna bond from “frontier” market like Mozambique, what’s impossible?

AFAIK some lessors received compensations that are pretty close to the carrying value on their books.

The last (start-up) airline I modelled was just over two years ago using the then discount rate. In the intervening period, due to the disastrous policy response to COVID we have experience the fastest and deepest bond crash in history causing the discount rate to increase by 1000% rendering the IRR, MIRR and NPV for that and any other project designed in and prior to that period irrelevant.

From 1940 we had a 40 year bear market in the long bond followed by a 40 bull market which came to an end two years ago.

For the airline industry there was the world prior to COVID and the world post COVID. I see little tangible sign that the airline industry has even begun to adjust to this new order. Will we see another 40 year bear market?

Used Jets Rents Surge 44% as Airlines Pay Up to Buoy Fleets – Bloomberg

https://twitter.com/BrianRynott/status/1714989153526383007

I think a lot of that is backup for faulty new aircraft, a substantial number of which are AOG.

Both airframers face supply chain constraint and delivery delays.