Leeham News and Analysis

There's more to real news than a news release.

Bjorn’s Corner: Air Transport’s route to 2050. Part 23.

By Bjorn Fehrm

May 23, 2025, ©. Leeham News: We do a Corner series about the state of developments to improve the emission situation for Air Transport. We try to understand why development has been slow.

We have since we started in October last year looked at:

- Alternative, lower emission, propulsion technologies, ranging from electric aircraft with batteries as energy source, different propulsion hybrids, and new concepts for Jet-Fuel and Hydrogen gas turbine engines.

- We have also looked at recent research into the role of CO2, NOx emissions and Contrails generated by airliners.

- Three weeks ago, we summarized the present situation around SAF, Sustainable Aviation Fuel.

We examined Alternative 1’s emissions improvement two weeks ago and compared it to the normal improvement in new airliners’ fuel consumption last week. Now, we examine the improvement that SAF can offer compared to the other two.

Improvement in emissions from SAF

SAF, or Sustainable Aviation Fuel, differs from the normal Jet-A1 fossil-based fuel by having its source’s CO2 absorbing phase in the same time period as the fuel’s oxidation into CO2 and other emission products in an aircraft engine. By it, a total CO2 emission reduction of about 80% can be achieved.

The problem is that last year, airlines consumed 1 million tonnes of SAF out of a total consumption of 300 million tonnes of Jet Fuel. The problem comes from SAF being more expensive than Jet-A1.

Right now, the industry is in a chicken-and-egg situation. Low demand and, therefore, production make SAF costly as it lacks scale. Its higher price throttles further demand.

We have also written that SAF can’t replace normal jet fuel 100% in present aircraft, as the fuel systems and engines need some of the fossil Jet fuel’s aromatics to keep their seals supple. As new-generation airliners enter the market, this limitation will gradually disappear as the sealant materials are updated with materials that don’t require these aromatics to keep seals fit.

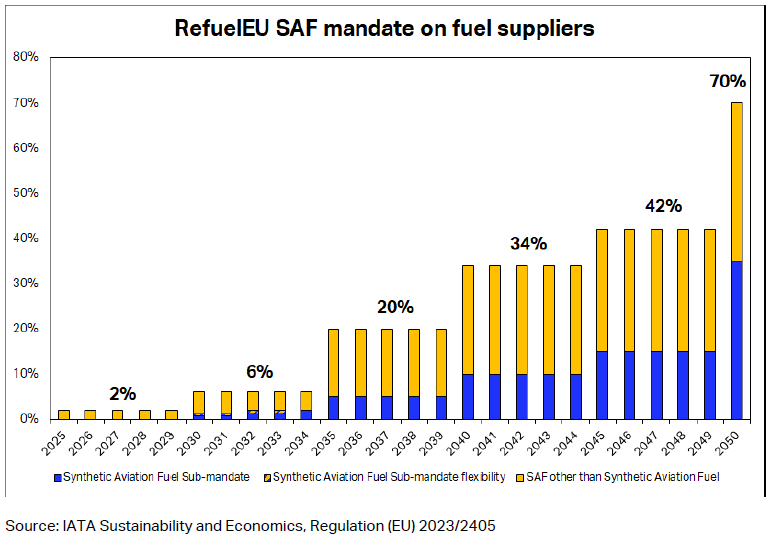

A path away from this stalemate is that states mandate a specific blend of SAF in an airline’s fuel consumption. The 27 European EU states decided on such a mandate in 2023, called ReFuelEU. It requires aircraft that depart from EU airports of a minimum size (800,000 passengers or 100,000 tonnes of freight per year) to any destination (EU or outside EU) to fuel their aircraft at the airport with jet fuel that has the following blend of SAF:

Figure 1. The ReFuelEU blend requirement on fuel suppliers at EU airliner airports. Source: IATA ReFuelEU Handbook.

We see that the blend requirement is 2% until 2030, then rises to 6%, and so on. This would require the SAF industry to produce about 1 million tonnes of SAF per year until 2030 and then 3 million tonnes. Neste, the largest producer of SAF, is producing 1.5 million tonnes this year, with a growth to 2.2 million tonnes by 2027. While airlines are worried about sourcing the required SAF volumes from 2030, the SAF industry says it will meet the demand.

How much will SAF reduce CO2 emissions?

Right now, the only region with a mandate for SAF blending is the EU. As traffic from such EU airports represents about 20% of worldwide aircraft traffic, on a worldwide basis, we apply a fivefold reduction of the SAF effect from this mandate.

If we take the 300 million tonnes of Jet Fuel consumed in 2025, where 1 million tonnes of these would be SAF before 2030, then 3 million tonnes, growing to 10 million tonnes after 2035, and so forth, we finish with a 70% blend of SAF from EU airports in 2050.

On a worldwide scale, if we assume that the improvement in fuel consumption from new aircraft keeps the yearly jet fuel consumption at 300 million tonnes, we will have a 14% reduction of fossil Jet Fuel consumption by 2050, or 42 million tonnes, with an 80% reduction in CO2 emissions, or 106 million tonnes. In the years before, it would have been an 8% reduction, or 25 million tonnes of Jet fuel, with the CO2 reduction at 64 million tonnes.

We shall remember these numbers when we come to compare the three different alternatives in future Corners.

Very enlightening, thank you.

I think you have left off the millions were it says 42 tonnes, 25 tonnes and 64 tonnes.

Yeah, thanks.

Tim Clark has again been making the rounds for a restart of the A380neo with some other upgrades to lower the fuel burn with 25%.

While AB is a bit reluctant over the 15-20bn€ it would cost, TimC says that if they make it, Emirates will buy it.

While the upgrades are likely interesting, the most keen question is if it can be made with folding wings, so it fits into category E slots instead of F.

That would mean that the mega hubs could convert their most valuable realestate into more passengers pr slot, even if they still have to have a strenghted runway & new airbrigdes. That is much cheaper than wastied apron m2. So that would be an posive business case for them, allwoing for both 777x & A380neo in the same converted E slots.

That would allow the megahubs, which are growing in number & size esp in China & India, to get more passengers & profits pr slot & per apron m2.

And for the airlines that would limit the risk of being able to use the plane on rutes that are not F gated. With airtravl growing of 4,5%, growing megaposlises & growing megahubs, it can make the difference in ABs A380 restart business case.

While the other things are equally important, I think the folding wings – smaller gate comtatibility – can be the key gamechanger, of the A380 are to be reborn and have succes.

It is hard to get the volume-salesprice needed. You would make a carbon-thermoplastic fuselage with 2ea 140k engines, a thin carbon with with active flutter control, non is fully developed yet. As well as 2 MLG instead of 4 making for more space for fuel and cargo.

Making folding wings should not more difficult than on the 777x.

They could take the existing wing and add a folding mech to it, so it comes in below 65m as the E size gate is. As the current wing is 80m, that would be 8 meter folding on each side.

From there you can the add as many other optimizasions as it makes sense.

The whole aircraft design is old by now. Both Airbus and Boeing await the thermoplastic technology to mature to make the aircraft structures faster and cheaper than today.