Leeham News and Analysis

There's more to real news than a news release.

Dissecting Boeing’s 2025 orders and deliveries

By The Leeham News Team

![]() Jan. 16, 2026, © Leeham News: Boeing won more orders than Airbus last year. Airbus delivered more airplanes, given its higher production rates and Boeing’s long, slow path to recovery.

Jan. 16, 2026, © Leeham News: Boeing won more orders than Airbus last year. Airbus delivered more airplanes, given its higher production rates and Boeing’s long, slow path to recovery.

But a dissection of the numbers also shows positive results for Boeing.

Boeing 737 MAXes awaiting delivery at Boeing Field. Credit: Leeham News.

On top of Delta Air Lines’ breakthrough order for the 787-10, its first for any 787, United Airlines converted 56 787-9s to the 787-10. The 787-10’s seat-mile costs are the lowest in its class. If an airline doesn’t need the longer range of the Airbus A330-900, the A350-900, or the 787-9, the extra passenger and cargo capacity of the -10 is a winning combination.

The total twin-aisle passenger aircraft deliveries were 179 (91 Airbus A330 and A350, 88 Boeing 787s). It is far below the peak of 2015 (362), at the level of 2011 (179), and below the peak of the late 1990s cycle (227 in 1999). Boeing needs the 777-9 certification to reclaim its historical lead in twin-aisle passenger aircraft deliveries. Boeing handily dominates the twin-aisle order book.

Single Aisle numbers

Boeing dominates the single-aisle market vs. Airbus for orders and deliveries of anything the size of the 737-8 or below:

|

Metric |

A220/A319/A320 | 737-7/737-8/737-8200 |

Boeing Share |

|

|

2025 Deliveries |

313 |

388 |

55% |

|

| 2025-12-31 Orders |

2282 |

2964 |

57% |

|

It is obviously the segment above the 737-8 that Boeing’s market share is problematic, which highlights the urgency to get the 737-10 certified:

|

Metric |

A321 |

737-9/737-10 |

Boeing Share |

| 2025 Deliveries |

387 |

54 |

12% |

| 2025-12-31 Orders |

5349 |

1600 |

23% |

Airbus and Boeing combined delivered 1,142 single-aisle passenger aircraft in 2025. It is the second-highest combined tally after 2018 (1,220).

Bottom line: Single-aisle deliveries are close to surpassing their pre-COVID-19 peak, while Twin-aisle passenger deliveries are still in the doldrums.

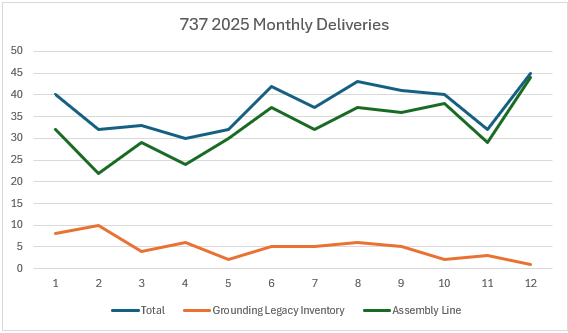

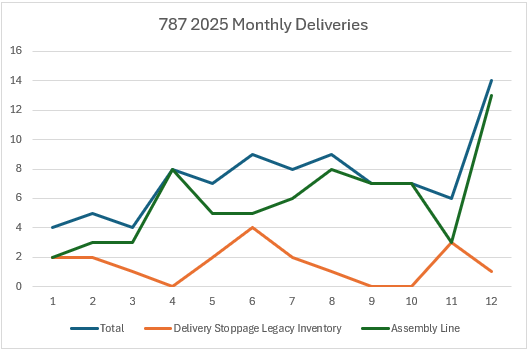

Monthly delivery numbers

Monthly delivery breakdown between the assembly line and legacy inventory for the 737 and 787:

The upward trend in the number of aircraft coming off the assembly line is obvious.

There are now two 737-8s (one for Air Europa, one for Shenzhen Airlines) and seven 787-9s (all for Lufthansa) left from the legacy inventory.

Melius Research sees Boeing Commercial Airplanes (BCA) turning book profitable in 2026. This assumes an average monthly rollout rate of 43 units for the 737, eight for the 787, two on the 777 Classic, less than one for the 777X, and 2.5 on the 767/KC-46 line.

“Melius Research sees Boeing Commercial Airplanes (BCA) turning book profitable in 2026.”

The term “book profit” as used here is presumanly referring to gross profit, i.e. revenue minus *direct* costs (COGS)…?

As opposed to net profit, which is revenue minus *all* costs — including interest, which is the real killer in Boeing’s case.

It will be interesting to see in which quarter book profit turns positive (if at all), and also how positive it ultimately becomes.

This will indirectly give us (averaged) information on unit margins, with attendant implied discounts.

+1

At this moment, my guess is Melius Research has adopted assumptions on the optimistic side, the first confirmation will come after Q1 when we shall see to what extent BA is able to meet:

“This assumes an average monthly rollout rate of 43 units for the 737, eight for the 787, two on the 777 Classic, less than one for the 777X, and 2.5 on the 767/KC-46 line.”

In 2025, BA delivered ~70 787 (my est.) from the production line, a jump to eight per month seems an extraordinary task to achieve.

So far in Jan, BA has delivered two 787s from the line, and one from the parking lot.

9 MAXs have been delivered from the line, and one from the parking lot.

The situation at AB is even worse to date:

0 widebodies

6 A320/A321 neo

0 A220

Same pattern as last year: after the delivery tempest in December, we sail into the Doldrums in January.

We’ll probably have to wait until March before we start to get more indicative data.

But I agree with your premise that BA will be pushed to reach the cited rates.

I didn’t realize that BA only has 23% of the market in A321/737-9/-10. Scherer must be smiling as he retires. Basically, AB can do nothing and watch BA continue struggling.

Are we going to ignore that Boeing delivered 35 777Fs in 2025?

So they actually delivered 123 widebodies. Maintaining their widebody delivery lead

You may also count some KC-46 and 767-300F but they are not regarded as “twin-aisle passenger aircraft”.

The freighters may be less profitable for Boeing than it looks. Nearly all 767-300F were sold to keep the production line open for KC-46. For 777F it looks like many of the recent orders were somehow offered as compensation for delayed 777-X.

Plus: the legacy lines are dying out, so they’re uninteresting from a product portfolio and order book point of view.

Really? Define legacy how?

737 is going to be built for a long time (like 4600 backlog).

767 is still building and KC-46A is going to be built for 10 years more or less.

777-NG is the only one really going away and its replaced by a (ahem) 777

A330 is still chugging along.

A320 is still chugging along.

Or are we talking 737 classics, A320CEO and the A330CEO and the A380?

“Legacy”: not fit for new ICAO emission rules. As a military product KC-46 is not required to meet this specifications.

737MAX has new engines up to the new emission rules and is no widebody.

777F is probably more profitable than a 787 delivery believe it or not. It’s only available freighter that is actually certified. What else can you buy? It’s been like that for a while and it’s a pretty good freighter too.

There P2F options, at far more attractive pricing.

Keeping the 777 line open to support a trickle of deliveries + discounting heavily to compete with P2F offerings = not very profitable at all.

Wrong assumption.

The reality is that its a complex situation of a lot of factors, feedstock being a bit one.

FedEx went new 777F because they could not get enough of a run to make it worth while.

Even with feedsto0ck there is a balance of hull life left and the cost to convert as well as a P2F is less efficient ops cost and carry capacity.

Boeing has long retired the setup costs, so as they used to say about the A330, they can offer bargains because its all paid for.

Funny how Boeing sold 787 to Hawaiian and Airbus was jumping up and down how Boeing had sold them below the Airbus margins. It was pretty funny. How Dare You!

And yes, Boeing can elect to sell below cost if they decide it has some benefit. In the case of Hawaiian they did not make as much per aircraft on the first go, but now Alaska is expanding the whole thing into whole new markets and they have a lot more sales. That also is parts and support that they make money on.

That poor dead horse is getting pretty beat up.

I’m a believer that 777F are doled out to pacify angry 777X customers.

That’s why BA continues to struggle getting back to profits.

+1

@Opus:

When FedEx got their initial ones, management was ecstatic and the mechanics were too.

One aspect was that mechanics got to work on the same setup vs a P2F where you had different Airlines with different builds and engines.

It was more efficient on support and maint so along with how it did, management was happy to see those costs a lot lower.

The early MD11F for FedEx were all the same, but latter ones they took what they could get so it was an engine mix vs the GE they liked as well as all the system variations they had to deal with.

Contracts were negotiated with customers years ago when BA pretends it can achieve much higher production rate around 4/mo by 2025/26 per LNA;

many have purchase rights and options included (before the current cost inflation is factored in);

per reporting of FedEx: “the aircraft were ordered years ago when market conditions were very different, and **canceling an order can be costly**”; nevertheless, FedEx gave up purchase options of more 767F to reduce its capex (contrary to what poster here said that the 767F is in high demand).

the 787 program is still digging itself out of the huge hole BA dug for itself.

At the end of the day, Ortberg expects BA to have a cash burn of around $3.5 billion.

You can define out anything you want, but the rreality is that the 777F is a 777. Argue the 767F/KC-46A – they too are still 767s.

All of those are normally accounted for in production numbers as would the 737NG that are builds for the E-7 and P-8.

Leeham has some interesting dissection and definition. It has an interesting validity in showing where the break in single aisle is. The NG adds are not that much but they are also not nothing. It adds to the overall rate builds and until they are moved out, the benefits are there for more production of 737.

Splitting out the A320 from the A321 does make for a dramatic and logical in Boeing’s gap there.

A full on set of data shows the whole picture. Airbus elected

not to do F models, did not succeed in the tanker contracts and does not build Single Aisle Patrol/Radar aircraft.

I can see Leeham generating target area reports for customers who want that data. Just not a general true status of build.

It does make a significant difference in the Wide Body deliveries. For all the travails, that is an area Boeing continues to lead in, good for morale to have that and a demonstration they did get some things right. The 787 is a huge winner despite the Boeing management at the time doing their level best to sink it. Kind of like Titanic deliberately being aimed at ice bergs (there is some engineering that says it would have survived that!)

Realty is sometimes somehow strange. KC-46 is based on a 767 but did that program made any profit for Boeing? About 200 P-7/P-8 were built since 2004/2009. That’s less than 1 aircraft per month. Did Boeing made profit on that programs? I don’t know. Looking at all these numbers or freighters won’t help us to understand what’s going on in the aircraft market for passenger jets. It was eye opening for me to see the A321/737-9 distribution.

Would MTU include its tank engines for an outlook on jet engines?

“Airbus elected not to do F models, did not succeed in the tanker contracts and does not build Single Aisle Patrol/Radar aircraft. ”

May I mention the A350F and https://www.elbeflugzeugwerke.com/en/?

Airbus delivered so far 66 A330MRTT and has even orders for the A330-800 as MRTT .

Airbus already has the C295 MPA/ASW and France paid for a A321XLR MPA/ASW concept study (production is now secured due to agent orange).

The Boeing management steered the ship full speed ahead into the fog fully aware of iceberg warnings (I may mention the opposition to the plastic 787 by former Boeing head of engineering for synthetic materials). Far to few lifeboats due to faulty regulations not up to time (e.g. lithium batteries). A head on collision would have flooded far less sections but the final fault were brittle rivets (you may blame the men at helm for their decision / MAX pilots).

I suspect that the A321 MPA is going to be a lot more successful than one might currently think.

I believe it’s clearly stated:

“The total twin-aisle passenger aircraft deliveries were 179 (91 Airbus A330 and A350, 88 Boeing 787s).’

“seven 787-9s (all for Lufthansa) left from the legacy inventory.”

Is this a “source” or a “sink” problem? ( i.e. LH being picky.)

There’s an ongoing problem with lack of FAA cert for Lufthansa’s new 787 business suites…

Sales numbers may be misleading as well. I am not surprised that Boeing had a better year. Airbus is otherwise sold out for near-term slots.

Stated production rates are all that really matters if you can convince yourself that neither OEM is going to be making white tails.

Fully agreed.

Airbus has great backlogs. They vastly dominate the A321 area. So, sales? Do you want to tie up money for the far future that will change? There is a limit. I suspect orders are speculative and being used as trading stock.

Its a nice bonus for Boeing to win on sales for once. Airbus has a thing about bragging rights and so does Boeing.

I doubt that sales are ‘speculative’ as I understand delivery spots cant be traded amongst airlines. Thats Airbus or Boeings desk where they revise the delivery skyline when an airline ‘cant cook-wont cook’ at the previous dates

I don’t disagree but I think its also a subtle difference.

I will leave the trade question aside, I don’t know one way or the other. I suspect you are right.

But, that does not mean you don’t get a slot and can’t trade with Airbus or Boeing for giving up that slot.

Maybe its, ok, slot may not be taken up, give me 1 million off on each of my other birds I am taking up.

Parts, upgrades to other aircraft.

While I was never involved in or around the slots, I did watch FedEx cancel the A380F before the contract said they could.

Fred was not stupid, he got something for the drop out. All he had to do was wait and get his money back. Whatever he negotiated with Airbus returned more than the initial payment.

UPS elected to wait till contract was violated and then cancelled.

For those who do not remember, the A380F was delayed but had not been cancelled for a while. You had to wait until Airbus expired the delivery promised date or cancelled the program. There was a period where it was officially delayed though they knew it would be cancelled. But you can’t drop out on the delay until its happened. They knew it was coming, just not past the clock time as it were.

It was assumed by the people I talked to FedEx got a lot of offset costs from Airbus for the fleet of A300/310s they had.

It was interesting, FedEx management liked the Airbus planes, mechanics did not.

I had some European equipment over the years. Always frustrating as US approach was different than European. Trying to sort out the logic in problems was the hard part.

Some was worse and some was just different.

A380F was hardly a typical plane or transaction

Widebody or not just sell and make us some money

I think you want to change that to BUILD. Sales make very little money in a desposit, the big bucks are on completion.

The “real” money is in delivery 🙂

Assuming that the original sale price had sufficient margin to cover costs…

Define costs? What I see is the same old lack of logic implied that Boeing is selling below costs.

Back in the day when I worked for Honeywell, we had a franchinse fee we had to pay. They asked us how we could save money. Cancel the franchise fee. Went over like a lead balloon. Why should a money making operation pay for money loosing Honeywell was doing?

Does the 787 program get charged for the empty halls at Everett? Defense losses on the 767? How about empty hall utilities?

Its the reason that all costs are combined and all money making is combined and you get a free cash flow number.

If management made massive mistakes (MAX, 787- 777X) should a given program have those costs attached to it?

Ergo the big combined numbers, either you are loosing more and more money, you are staying even, or you are gaining to break even level even if you are loosing money.

Despite all the issues and incurred management losses, Boeing is recovering.

To imply that Boeing is overall not making money is beating an old dead and buried horse.

-> BCA lost almost $4.5 billion under unit cost accounting in the first half of last year.

The numbers dont support this claim

“The 787-10’s seat-mile costs are the lowest in its class. If an airline doesn’t need the longer range of the Airbus A330-900…

The latest B787-10 IGW -probably Deltas version- has around the same ( nominal) max range as the A330-900.

B787-10 standard ~6,430 nm

B767-10 IGW around 7,100 nm

A330-neo ~7,200 nm

For Delta the 787-10 can fly at lot of the A350-900s routes more efficiently being 15 tonnes less airframe weight .

Looking at Deltas long haul routes. Pacific rim its Japan, Korea, China-Shanghai and Tawain plus South Pacific its Australia and NZ.

The Map indicates LAX to Melbourne is the longest at 12,800km/7000nm. Just inside the nominal IGW distance but might still favour the current A350-900 for commercial and operational reasons

It is even possible B787-10 Atlanta Tokyo at 11,000km, but would more likely be US west coast cities such as LAX at 8,800 km

In the real world 787-10’s don’t fly 6000nm. Marketing digits don’t matter.

Yes they do . Eva Air, Taipei to Seattle is 12 hour +.

Israel to NY is 11 1/2 hours

Tokyo- Chicago is just under 11 hours

These are the standard weight 787-10

Actual flight times from flightaware

Eva Air – TPE-SEA is never 12 hours or more. In the last 90 days the longest flight time has been 10:37, the shortest 9:19. This is according to FR24.

The great circle distance between the two is 5,278nm.

I haven’t looked up the other timings but TLV to JFK is less than 5,000nm.

Edit – I’ve just looked up the return SEA to TPE and that is indeed more than 12 hours but the great circle distance is obviously the same which is the point Alexander was making.

The route planning has to consider the longer period of the 2 legs there and back- headwinds are a real thing

Just route between London and New York is a 1hr longer eastwards.

@Duke

Good info. That changing of the models and what it does in their performance is very interesting. Nothing is static.

The 787 to the A350 is the flip of the A350 to the 777X. Wild

And no, I am not doing any fact checking, assuming the data is valid.

Everyone: The LNA website has been having technical problems since Friday (today is mid-day Saturday). IT is working on it, so please be patient. There may be addition times in which the site goes down for a while.