Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

- Engine makers tout “Plan A” but have “Plan B” backups in R&D June 23, 2025

Analyzing A350 backlog: special to Leeham News and Comment

Special to Leeham News and Comment:

Vinay Bhaskara of Aspire Aviation has provided the following analysis of the A350 XWB sales, on a variety of metrics, exclusively to us.

Analyzing the A350 Backlog

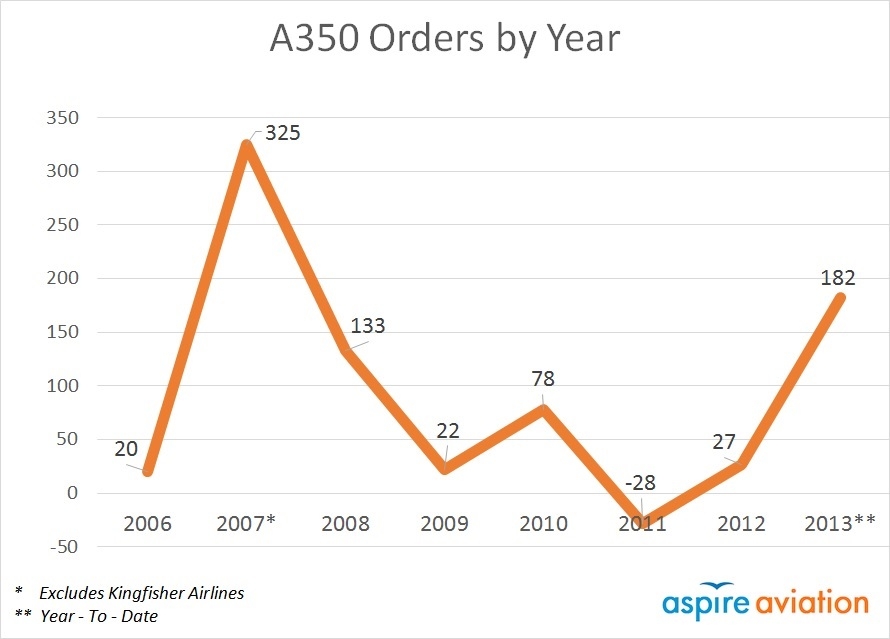

With the recent order for 31 A350s from Japan Airlines, we thought it would be instructive to take a look at the A350’s backlog. To date, the A350 has won 759 orders from 39 different customers (we are excluding Kingfisher Airlines in India and its order for five A350-800s – Kingfisher has been shut down for more than a year now, and it’s chances of re-starting appear bleak).

After slow sales in 2011 and 2012, 2013 has been an excellent rebound year for the A350, its second best behind 2007, with 182 orders to date. We expect South African Airways to place its delayed order for the A350s by the end of the year, and there are several upcoming fleet replacement decisions, most notably at ANA and Qantas, in which the A350 is a major player. The chart below shows A350 orders by year since it launched:

Digging further into the backlog, the following two charts discuss the geographic breakdown of the A350’s orders. Asia and the Middle East currently account for more than 55% of the program’s orders, and it has made limited inroads in the Americas relative to the 787.

.

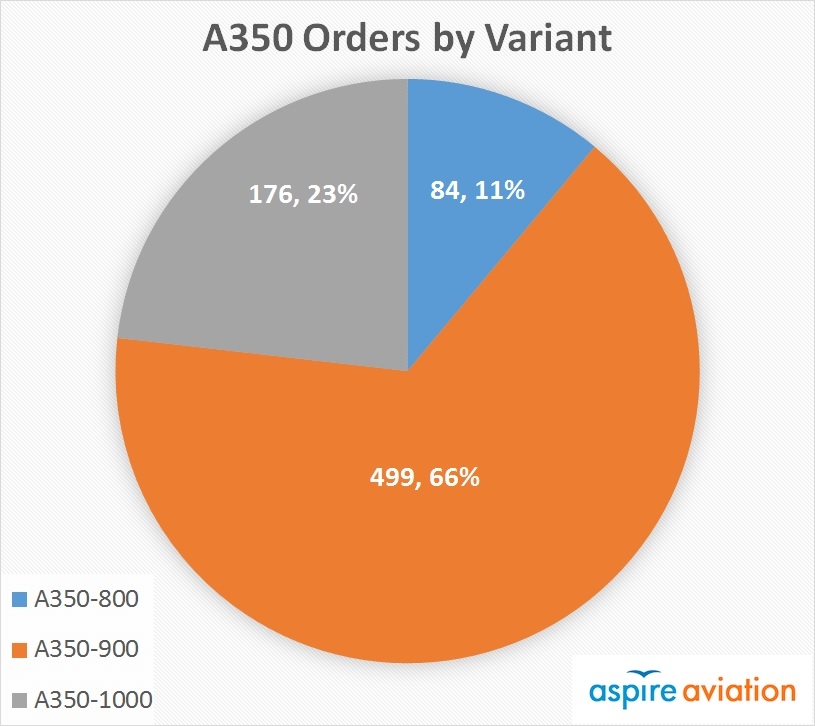

The backlog recovery has been particularly pronounced for the A350-1000. As recently as two years ago, there were major questions surrounding the A350-1000, but since then, it has won several high profile 777 and 747 replacement battles, including Cathay Pacific, British Airways, and now JAL. The A350 program backlog by variant is presented in the following chart:

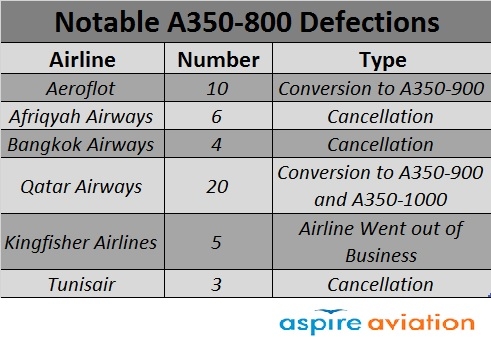

This chart does highlight the ever-growing weakness of the A350-800. With a backlog of just 84 frames and a spate of cancellations and conversions to the larger A350-900, it will be interesting to see what action Airbus takes on the A350-800. We expect US Airways, the type’s largest customer, to convert to the A350-900 if the merger with American to go through so as to avoid overlap with the 787-9. That might be the death knell for the A350-800.

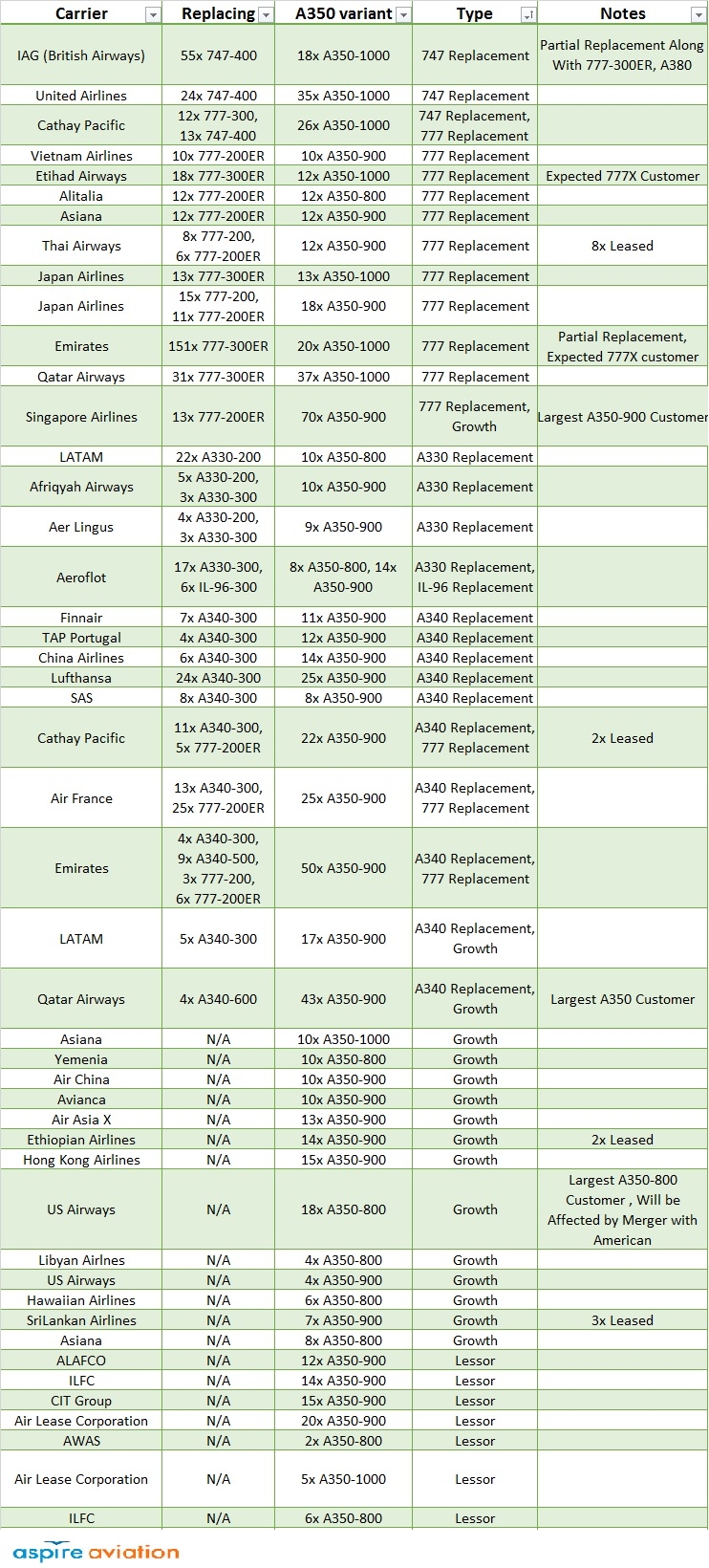

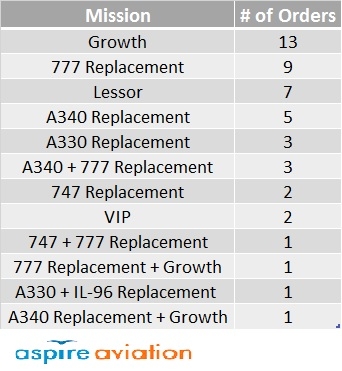

The following table outlines the planned mission for every current A350 order on Airbus’ books. The table splits orders for different variants by the same carrier into distinct order entries with differing missions, except in the case of Aeroflot, where the mission is common across the two variants.

The following table summarizes the orders by mission type. Of note is the fact that the A350 has already won several major 777 replacement battles.

*************************************************

800 has long been the dog, certainly because it’s facing 787-9…

for every shrink/stretch to be equally competitive would be a strange thing,

certainly the same holds for Boeing’s platforms as well (787, 777X), nothing new.

my question is what COULD 800 be, if it were delayed, 1000 pushed forward,

and a new 800 designed possibly with more variation vs. 900,

and aiming to achieve a more substantial niche where it’s competitive.

what would the most viable redesign of 800 look like?

By delaying the A350-800 EIS to 2020, Airbus could send out a RFP asking for an engine that’s at least 5 percent more efficient than the Trent XWB-84. Rolls Royce, for example, could offer a scaled down RB3025. The fan should have the same diameter as that of the TXWB, and the core would be smaller and lighter, and should use the same nacelle and pylon as that of the TXWB.

http://www.flightglobal.com/news/articles/in-focus-engine-makers-prepare-to-do-battle-on-777x-376865/

Due to the lower fuel consumption, lower engine weight (up to 3 tonnes), new smaller optimised main landing gear, and other weight saving measures, IMO the MTOW of this new optimised A380-800 could be as low as 230 metric tonnes for an 8000 nm nominal range (pax and bags).

Airbus could also offer a 230-tonne version of the A350-900 that would be optimised for medium range.

Correction: IMO the MTOW of this new optimised A350-800 could be as low as 230 metric tonnes for an 8000 nm nominal range (pax and bags).

The -1000 cannot be brought forward because it depends on the updated Trent XWB engine. If Airbus delays the -800 it will be for other reasons, like looking at ways to reduce the OEW. But even significant weight reductions will make life of an optimized -800 hard because the 787-9 can hold 10 more seats and more cargo (= more revenue) anyway.

A 230-tonne MTOW version of the A350-800 as described above would have a MTOW in the neighbourhood of that of the 787-8; or 20 tonnes lower than that of the 787-9. It would have year-2020 state-of-the-art engines and a TSFC some 5 percent lower than the TXWB and some 7 percent lower than the current engines on the 787. Hence, it would compete not only with the 787-9, but also with the 787-8. The higher airframe weight would be compensated by the more efficient engines. This is quite similar, of course, to how Boeing wants the 777X to compete with the A350-1000.

@OV-099

Sounds good. 2020 seems far away but given the large forecast numbers by both Boeing and Airbus until 2032, such an airframe might still capture a large trunk of orders.

My pet project would be to put a new midsection on the A350: lighter wing, landing gear and much lower thrust engines. Everything fore and aft of the wingbox is the same as the A350, as are the systems and the dimensions of each model. This new plane, which we will call the A360, will be the replacement for the A330 and will be available early part of the 2020 decade. It will be optimized for the -800 model with about 6500 miles of of range.

It’s nice to be an armchair aircraft designer! Airbus certainly know more about how to do it than us.

The point is, if Airbus do something like this there is no additional cost to producing an A350-800 beyond the certification. They have sold the -800. They might as well produce it, unless cancellations mean there are none to produce.

Maybe the answer would be to drop it and make its replacement the largest member of a smaller family to replace the a330-200/300?

A whole different airframe to replace the A330? Far too expensive. If there is no A358, the options are an A321 stretch, A330 neo … or just a gap in the lineup.

Airbus could re-engine the A330. But I think it would be better to develop a new wing for the A350-800, optimising it for A330 missions. The fuselage cross section is sound, just it is a bit too much aircraft for its size.

“what would the most viable redesign of 800 look like?”

http://i191.photobucket.com/albums/z160/keesje_pics/A330NewEngine.jpg

IMO the A350-800 will be delayed and if delayed airlines will be more motivated to switch to the -900s. . Airline pilot board the aircraft today and check performance themselves, Dreamliner like hick-ups have been absent sofar. A380 EIS went relatively smooth. The A350 sales rush at this stage was to be expected.

A350’s are getting sold out, improving chances for further A330 enhancements making it a better fit under the A350-900 in terms of capacity & range.

An A350-900 optimised for intermediate range and having a MTOW around 230 metric tonnes as outlined above, would have an engine with a TSFC some 20 percent better than the current Trent-700 on the A333. Hence, it would IMO be a very good replacement aircraft for the A330-300.

IMO, Airbus should not do anything further with the A333 than what’s already been announced, and just try to sell as many as possible. A re-engining programme would IMO not be a good investment.

The A350 fuselage is replacing the 40 year old A300 legacy fuselage. Therefore, investing more resources and capital in the A330 would IMO see diminishing returns much quicker than what is the case with new A350 derivative aircraft.

I concur with you statement. But the A350-9/10 wing on the -8 means a wing designed for 40-60t more MTOW than actually needed. Make the wing smaller! A new wing costs money, but not much more than bringing the A330 anywhere near the B787-9/10.

AFAIK, the wing of an all new aircraft accounts for about around 40 percent of the total costs. I’m not sure if that’s a realistic thing to do in the time frame that we are talking about, and especially not if Airbus would decide to upgrade and stretch the A380 during the same time period (i.e. EIS 2020/2021).

In fact, I’m of the opinion that the A380 should be stretched and upgraded with new engines that are at least 10 percent more efficient than the current Trent-900s and GP7200 engines; or having about the same level of percentage-wise TSFC reduction as the GE9X will over the GE90-115. In addition, if the A380 was to be modified with two 4.5m 777X-style folding wingtips, increasing wingspan to 89m, the required max take-off thrust would be reduced by about the same level as what’s the case with the 777-9X vs. the 77W.

Therefore, an A388neo and an A389 should be able to use the same advanced engine as that of an A350-800.

with the production line filled with all these new orders, they should follow their concept further in making the 800 a minimum change version with more range. It does not make sense to first invest a lot of money for changes and then discount the 800 if you can easily sell a 900 or 1000 for that production slot and earn 10 times more cash!

A minimum change A350-800 with more range would be a niche C-market ULR aircraft. Look at the total sales volume of the 777-200LR and A340-500. Doesn’t look like a very big market, does it?

As for A350 production levels, IMJ Airbus could increase total output to at least 20 per month by the early 2020s. If an A350-800 developed as I’ve outlined above, would be more than competitive with the 787-8/9, there would be no reason not to increase output (i.e. 2nd FAL etc.).

The A350 will never be a good medium range, regional aircraft. That’s the price it pays for being a capable long haul twin.

http://www.airbus.com/fileadmin/media_gallery/photogallery/big/800x600_1379691402_Airbus_Family_flight_air_to_air_A330_and_A350_XWB.jpg

Everything on it is to big, heavy and expensive for short flights / many cycles without cargo.

Same goes for the 787, A330. However those are destined to fill the hole left by 767 and A300/310.. Unless Airbus or Boeing invests a few billion in a much lighter dedicated smaller wing/ wingbox/ LDG etc. for a 767NG or A330NEO. http://i191.photobucket.com/albums/z160/keesje_pics/AirbusA330-700Light.jpg

Well, new engines as described above (minus three tonnes); all new 787-8 sized landing gear (minus 1.6 tonnes*); further optimised airframe than what was intended with the original 248 tonne version of the A350-800, and where a “couple of percent” fuel burn penalty** would have represented about 3-4 tonnes of extra weight over that of the 248-tonne version; all which should lead to a significant OEW reduction for an intermediate ranged A350-900. In fact, the OEW of such an intermediate ranged A359, may only be some 2-3 percent higher than that of the A333.

*http://adg.stanford.edu/aa241/structures/componentweight.html

**http://www.flightglobal.com/news/articles/most-xwb-customers-endorse-a350-800-rethink-airbus-341140/

* http://adg.stanford.edu/aa241/structures/componentweight.html

** http://www.flightglobal.com/news/articles/most-xwb-customers-endorse-a350-800-rethink-airbus-341140/

Why not “a much lighter dedicated smaller wing/ wingbox/ LDG etc. for” an A350-700Light? I don’t think fuselage weight is much different between A330 and A350.

Yes , a new higher aspect wing with say 60m span and two 4m folding wingtips that would comply with Category D conditions everywhere but the runway (i.e. Category D = 36 – 52m), would be a good option for a short-range/intermidate-range, A350 derived family of aircraft, spanning an overall aircraft length from 50 – 60m. However, that’s at least a $5 billion undertaking. What I’m talking about is entirely different. 😉

OV-099 MTOW is nice but not the determining factor for short flights.

Payload, range and the resulting empty weight -> engines and unit costs are.

Looking at the empty weight of some aircraft in this segment

B763 : 80t

A300 : 90t

A332: 120t

B788: 112t

A358: 115t (?)

it becomes clear those weights aren’t good or bad, they are the result of the intended use of the type. The 767 and A300 were smaller, shorter ranged and much more efficient on the shorter lighter flights they were developed for.

An A350-800 replacing a regional 767 would could carry 100 more seats in a typical domestic 2 class lay-out and a big (empty) cargo bay. Plus 35 (!) tonnes (~350 passengers) non paying carbon and metal. For 25 years flying around free of charge, burning gas. While you were looking for cheap 250-280 seater in the first place. Shave off a few tonnes here and there and it still is a very bad idea.

The wings of the 767 and A300 have too short wings in reference to today’s standard of relatively light, high aspect ratio wings. As the saying goes, span is “everything”. 😉

A new short-range/intermidate-range, A350 derived family of aircraft, as described above would probably not weigh much less than the 767 and A300, but would be significantly more efficient.

However, what I was talking about, is an A350-900 derivative that would be developed together with a “new” A350-800 which should be able to compete effectively with the 787-8/-9. Incidentally, as I’ve already indicated, the OEW of such an A359-derivative, should not be that much higher than the OEW of the current A333. By using engines that would have 20 percent better TSFC than the ones on the current A333, I can’t see why it shouldn’t beat the A333 handily even on short and intermediate ranged sectors. 🙂

Unless somebody invent the morphing ac, no design will suit the requirements from an A320/B737 to an A380/B747. It sounds stupid to say it that way (and it is) but our forums are littered with comments that ac are not designed to do this and that and then that as well, meaning silly designers.

We have to come to terms with the fact that ac as well are designed for a purpose with minor possible twickings in weight, length/seatings and flying performances.

The recent decisions by Lufthansa and JAL shows that clearly. They have looked for the ac suiting best their needs and have chosen the winner, be it an Airbus or a Boeing. Both companies are now regarded as equally reliable (or equally not by the way) as suppliers to the airlines.

I think that we should not reason anymore in duopoly (even if it is there), but in product availability.

But of course that would annihilate all the fun.

It appears to me that Boeing is struggling to sell the 787-10. The market reaction to this airplane is rather subdued.This is probably because most potential 787-10 operators have already defected to ab to buy the 350-9 or is it because of the reputation of the 787-8 of being the aicraft with the worse eis? At the rate at which Dreankuber breakdowns are occuring, boeing can nolonger fool us that

its eis record is only second best to the 777.

Or is it because Boeing marketing tactics are lacking where it

counts the most. Just by looking at how ab has easily snatched

longtime boeing customers I wonder if the marketing department at boeing

is really up to it.

I wouldn’t say so. It’s only been on sale since June and they have sold 90 with more in the works. The -10 makes up the bulk of 787 sales this year

Slight correction there – Boeing only lists 80 787-10 sold so far this year (through September 30th), i.e. 61% of the net 131 total 787 orders in the same period.

I’m curious to see how this is going to play out for the full year 2013 and then 2014 – so far, we’ve only seen two leasing companies order 40 between them, and two airlines also order 40 between them.

Mind you, it’s a respectable number, but we’re going to be in a better position to gauge market reaction to the 787-10 about a year from now.

I think ten of them may have been conversions from other 787s ordered by United. A further dozen ordered by IAG haven’t shown up in the books yet. So about 100 in total.

But I still believe Boeing marketing is up to no good. they lack the aggression and skills that ab has demonstrated in order to snatch boeing customers. ab aircrafts are not necessarily better that boeing’s but it is all down to marketing strategy that ab is selling better than boeing. in the 1990 if you wanted an aircraft the first port of call was boeing and boeing is but now things have changed and boeing need to realise that and stop taking customers for granted.

I believe it was inevitable that Boeing would lose widebody market share to Airbus. By developing the A330, Airbus proved that they could do it. That they wandered along the way after creating it could be seen as a great gift to Boeing for the last 15 years. But Airbus, when forced to by their customers, finally decided on a new widebody, they really did their homework. The A350 is in no way a killing blow to Boeing but it is a sure sign that Boeing now has a competitor who is approaching being an equal. But that is not yet the case. Everybody knows that Airbus still has gaps in their fleet offering. Gaps that will exist for at least another 20 years, I would guess.

I don’t see Boeing having made any great mistakes, at least no greater than some of those that Airbus has made. Both companies have just made different mistakes and for different reasons. It is an ongoing strategic game and part of Boeing’s strategy focuses on another area of the business model than Airbus does.

“The wings of the 767 and A300 have too short wings in reference to today’s standard of relatively light, high aspect ratio wings. As the saying goes, span is “everything”.”

That depends on the use of an aircraft and its resulting shape, wing area, airport requirements etc. Boeing wasn’t cutting span on the 787-3 for fun. A wingspan within ICAO Code D limitations (52m) iso E (65m) opens up a mass of additional gates around the world. Now is that really that important for airline operations?

Of course it is, specially if you are doing 6-8 flights a day from stuffed hubs to secondary airports! http://www.qrsworld.com/Site/images/Atl%20Airport.JPG

The 787-3 was IMO a dead-end project from the get go. If anything it should have retained the wingspan of the 787-8, but should have been outfitted with two 3.5m folding wingtips in order to comply with Category D conditions everywhere but the runway (Category D = 36 – 52m).

Again, span is everything. Boeing’s SUGAR Volt concept , for example, would have a wingspan of nearly 100 meters and very high aspect ratio.

http://inhabitat.com/boeing-teams-sugar-volt-aircraft-burns-70-less-fuel/

Pingback: Habemus A350 | Aviación y turismo

I don’t agree with a number of the claims above that the intended purchases are for 777 replacement. The oldest 77E will not hit 20-years old until 2017 and many operators are choosing to fly their wide body aircraft significantly longer than that. EK and SQ may be on 12 year schedules but that is far from ordinary. Stating that EY bought their 12 A351 for 77W replacement when the vast majority of EY’s 77Ws started arriving in 2011 appears premature for a high-growth airline that can’t get enough aircraft and has resorted to buying second hand from AI. Same argument for QR and others.

This analysis does show, in my opinion, that A350 and B787 are either over ordered or we are going to see a shortening in life span of last generation aircraft.

“The A350 is in no way a killing blow to Boeing but it is a sure sign that Boeing now has a competitor who is approaching being an equal”

Yes, the 787 is still better then the A350, the 748 beats the A380, the 737 gives the A320 a run for its money and the 777 is far more advanced then the A330. And Airbus has to do some catch up on supply chain management, outsourcing and strategy. Gaps will still exist in 20 yrs. Anyway..

Essentially Boeing has been able to leverage reputation and “wining and dining” to subdue Airbus sales over some time in the past.

As we now can see quite well reputation is a limited resource and there is only so much you can achieve by “wining and dining” with a diminished platform of reputation to work from.