Leeham News and Analysis

There's more to real news than a news release.

Boeing still needs hundreds of 777 Classic orders to fill gap

Subscription Required

Now open to all readers.

Introduction

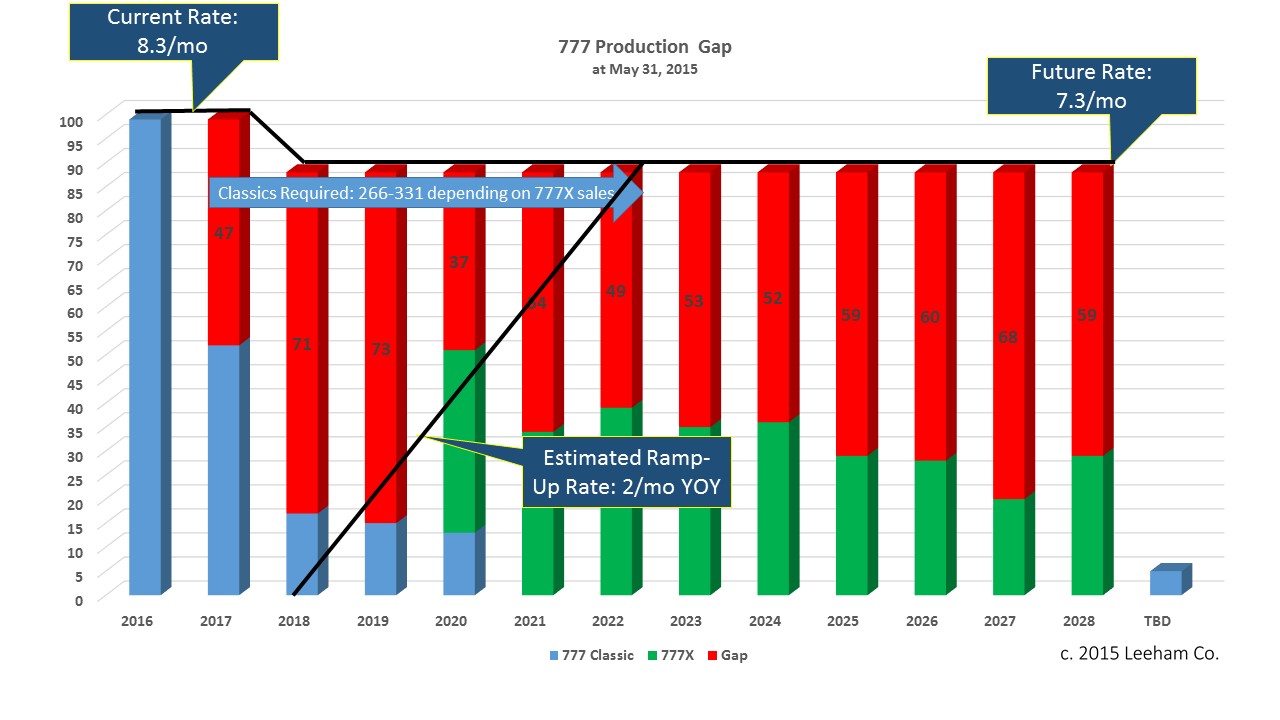

June 9, 2015, c. Leeham Co. Boeing may acknowledge that it will cut the production rate of the 777 Classic by one per month in 2018 as production of the 777X begins, Officials may claim the 777X production is the same as maintaining a rate equivalent to 777 Classic. But a fresh analysis taking these factors into account shows Boeing has a steep hill to climb to maintain sales and cash flows.

We’ve updated our analysis from last February on the production gap facing Boeing to maintain production rates through the introduction of the 777X in 2020 and beyond until the X ramp-up is complete. We’ve taken into account the delivery dates of the 10 Classics ordered this spring by United Airlines. We’ve also taken into account information emerging from Boeing’s Paris Air Show briefings last week. This includes information that Boeing will cut the rate of the Classic by one per month in 2018 from the current 8.3/mo as the X is integrated into the production system.

Summary

Boeing’s initial claims that it will maintain the 777 Classic production rate through 777X EIS has been eroding for months.

When the estimated 777X production ramp-up is factored in, Boeing’s task of selling the Classic to maintain rates is daunting.

Boeing still has to sell hundreds of Classics to maintain production even at the lower rate, according to our analysis.

Even with the new information and Boeing’s revised messaging, we remain firmly convinced 777 production rates will have to come down much more than suggested last week.

Discussion

Boeing just can’t get there from here. The production gap is too great to match even the reduced rate of 88 per year, down from 99 per year, of 7.3/mo from 8.3/mo.

Click on image to enlarge to a crisp view.

Assumptions

- Boeing indicated that a rate reduction in 2018 of 1/mo is likely as the 777X is “feathered” into the Classic production. This is reflected in the Figure above.

- 777X production begins in 2018. The first 777X is scheduled for delivery in 2020. Flight testing begins in 2019.

- Production ramp-up begins slowly as a new airplane enters the system and the learning curve begins. We assume Year 1 will have a production rate of 2/mo (which may be a bit high), Year 2 goes to 4/mo, Year 3 to 6/mo and Year 4 tops out at the highest rate (in this case, 7.3 or even 8.3/mo).

- With 777X production beginning in 2018, we have production hitting the maximum in 2022, four years later. We actually believe this will be in 2023, but we’ll be generous in our assumptions.

As the Figure illustrates, Boeing’s current production gap, even at a reduced rate, is substantial—and a challenge we don’t believe Boeing can meet with an end-of-life Classic series.

Next year’s production is sold out, according to the Ascend data base. Boeing said its 2017 production is half sold out, which Ascend also reflects. From there, the 777 Classic backlog drops off sharply to low double digits.

Boeing hopes the 777F, of the Classic line, will continue for five years after EIS of the 777-9, according to information from the PAS media briefings. Based on an interview we did with Boeing about freighters, and on Boeing’s assumption of a recovery in the global cargo market, production of the 777F would be between one and two per month.

Boeing’s cash flow from the 777 Classic program is already taking a hit. Our Market Intelligence indicates that Boeing has offered the 777F for $150m and that United Airlines’ cost of the 777-300ER is $130m-$135m including Buyer Furnished Equipment, and $120m without the BFE. Aerospace analyst Kenneth Herbert of Canaccord wrote in a research note last month that he believed the 777s were priced the same as the 787-9s UAL swapped for the larger, but older airplane, of $110m. UAL (Continental) was the US launch customer for the 787. A 777-300ER historically sold for $148m-$170m, depending on the customer and quantity, according to long-standing Market Intelligence.

Boeing’s cash flow has been squeezed for many quarters now. Cash flow was well below forecast in 3Q2014 and analysts pummeled Boeing as a result. This led Boeing to ask key customers to accelerate Pre-Delivery Payments (PDPs) and increase the size of Advances when ordering airplanes. This caused the 4Q2014 cash flow to shoot up dramatically. This process continues this year. The purpose is the meet stock repurchase commitments in the billions of dollars annually, according to several Wall Street analysts we have talked to.

The production gap Figure illustrates the looming cash flow squeeze Boeing faces in the coming years from just this program. Furthermore, sales of other 7-Series airplanes are falling off because of the huge backlog that extends beyond 2020 for the 737 and 787 programs. Opportunities to get larger-than-normal advances for orders from these programs are diminishing, too.

Our Market Intelligence indicates Boeing will be forced to face the music on future 777 production rates by the end of this year. Notice of 12-18 months to the supply chain is required to adjust rates up or down.

Wow no comments.

Looks spot on to me

I agree with the thrust of the analysis, But I believe that 777X’s launch is going to be troubled, mostly by implementation of lean and new production techniques. Beyond the extra time you allotted. All of 777x’s value as a low cost alternative to a clean sheet design seems to be falling away. It’s going to get the 787 treatment I fear. Boeing just doesn’t seem to be able to get out front on production issues anymore.

My concern however, is less on 777 orders than 777x orders. Since launch, orders have been scarce, and it looks like Airbus has beaten Boeing to market by such a huge time frame that it will seriously erode 777x sales.

What’s your view on current 777x sales? Are my concerns unfounded?

One of the Boeing VPs for marketing has his own blog, which makes it easy to see progress as the new production facilities for 777X are built ( amoung other)

http://www.boeingblogs.com/randy/

In fact today has Boeings latest market forecast. 12 July.

As for 777X development. Its much lower risk than the 787. The fuselage is mainly the same production facilities and the composite wing is being built by Boeing in house. The real risk is the GE engine

I think that it is too soon to say that it will be troubled. Granted anything is possible but I think that Boeing has made great strides since the 787-8 debacle and now that the production lines are humming along, the 787-10 ahead of schedule and the 787-9 having had a smooth introduction into the 787 Boeing portfolio, I think the 77x will be ok. With the 777 line being the most profitable plane in the Boeing lineup, I seriously doubt that they’d be so lax and careless. To my knowledge Boeing only has the MLG (Canada) and the folding wing-tips (Germany) being made outside the US, everything else is in house, this making the assembly smoother, sans missing rivets and tools left behind in avionic bays. Sheesh, the memories.

Orders – Airlines who have a mixture of 744, 346, 345 aircraft could make a lateral move to the 778 or the 779. Carriers who have smaller aircraft and are looking for a bump in capacity could favor the 779 as well as it would be easier to fill and Boeing would likely swing a deal with the 77W and one of the 2 777x models. In the same breath airlines who want to decrease in size from the A380 could be candidates for the 779. China Southern comes to mind. TK, BA, ET could order the type(s). SQ is a maybe since they have so many A35J’s on order but they were rumored earlier this year to have mulling over an order of the 779, up 40.

Leeham: Boeing’s cash flow from the 777 Classic program is already taking a hit. – Boeing’s cash flow has been squeezed for many quarters now. – The production gap Figure illustrates the looming cash flow squeeze Boeing faces in the coming years from just this program. Furthermore, sales of other 7-Series airplanes are falling off because of the huge backlog…

All that is certainly a big concern. But if everything goes well the situation should not be catastrophic and will likely remain mangeable. That being said, the rosy picture Boeing is painting for us could turn out to be quite ugly if the 777X does not EIS in 2019. And frankly I don’t believe this is possible given the size and complexity of this undertaking. In each project there is always an element of risk, no matter what precautions you take and however experienced you are. In this particular case the risks are extremely high because of the new technology involved and because there is no continuity. Boeing is almost starting from scratch here. The fact that Boeing wants to take the wing in-house is laudable, but they should have started with a smaller wing on a smaller aircraft. In other words on a New Small Aircraft.

I was already concerned because of the situation in other programmes: various military projects, the 787 deferred costs, the antiquated 737 platform, etc. But now I learn that the cash flow position is deteriorating faster and earlier than I had anticipated. If we add all this together we can see that the next few years could be a very difficult period. I think that by 2020 Boeing might start to feel the weight of its indecision.

” But now I learn that the cash flow position is deteriorating faster and earlier than I had anticipated. ”

Previously I assumed an additional discount of 10%, now it seems that the additional discount is about 10-20% of the tag price. This a perfect example of “indirect” cost that I frequently refer to. ~50 millions additional discount per aircraft means up to 10 billions loss of profit on a basis of 200 units. When considering this additional cost, the total cost of the 777X is much larger than the R&D cost. Considering the deferred production cost of the 777X, we will probably have a value of 25-30 billions.

What do the airlines get for accelerating their pre delivery payments?They are not going to do it for nothing.Might it be cheaper to borrow it from the banks?Boeing were fairly quickly found out,so they couldn’t of done it just to be sneaky.Completely baffles me, but then I’m not bright enough to work in the city.

If anyone has seen the recent Boeing predictions for the next 20 years, the numbers are 4470 for small widebodies (200-300 pax), 3520 for medium widebody (300-400 pax) and 525 for large widebodies (400+ pax).

Now if you do the math then we have approximately 20 planes/month for small, 15 planes for medium and 2.3 planes for large widebodies, or in total 37.3 planes/ month.

Taking into account 11months production for Airbus then we can come up with these assumptions: 6 planes/month for A338/A339, 11 planes/month for A359/A351 and 2 planes/month for A388 or in total 19. For Boeing the figures will be 12 planes /month for B788/B789/B781 and 6 planes/month for B778/B779 or in total 18 planes/month.

The sum is 37 planes/month and in very good agreement with Boeing’s prediction.

Of course I know that Boeing is aiming to 14planes/month for B787 and 8.6planes/month for B777, but I think this is not sustainable, unless they take a larger portion of the pie and this is not justified from the current product line and order portfolio.

Now let’s split the production by plane category and show that there is a problem here with the production of B777.

For 200-300 pax we can assume 6/month for A338, A339 and 9/month for B788, B789. We have a shortage in the predictions of 5 planes/month.

For 300-400 pax we can assume 8/month for A359, 3/month for A351, 3/month for B781 and 6/month for B777 or 5 planes/ month excessive production.

This can be justified only by moving the B781 to small widebodies and taking into account the 2.3 planes from large widebodies. However this implies that A380 will be terminated in the near future and I am not so sure about this. Even if it will be terminated Airbus will proceed to the A350-1100 for the 400 pax market.

In the bottom line I don’t think that Boeing can sustain according to their predictions a long-term production of more than 12 planes for B787 and 6 planes for B777. The cash flow problem is more severe than many people anticipate.

I haven’t counted in B747 since only 19 left for produciton.

“Boeing hopes the 777F, of the Classic line, will continue for five years after EIS of the 777-9, according to information from the PAS media briefings. ”

Economically, does it make sense to continue the 777F at a rate of 1 or 2 units per month considering that the 777X is almost a completely new aircraft (new wing, new engines, “new” fuselage, new ECS, hydraulic, etcs.)?

Good questions.

Or another way to put it is how do you mix up two majorly different aircraft on the same assembly lines.

As noted wing production has to continue and its now very low numbers per previous in a facility that was designed for over 16 a month (two wings per aircraft) and 8 center sections that are not common to the two aircraft.

Cockpit changes? Those will be updated and at least somewhat different.

Landing gear is no longer common.

“Or another way to put it is how do you mix up two majorly different aircraft on the same assembly lines.”

On a previous post, I claimed that Boeing will not continue the production of the 777F after the introduction of the 777X and that Boeing didn’t launch a 777X-F because it doesn’t want an internal competition with the 747-8F which Boeing desperately try to sell.

“Landing gear is no longer common.”

Yep, and new flight control systems, new electric systems, the list is long…

So I am questioning Boeing commercial strategy…

Wow, this is super interesting, thanks for sharing! Your article also triggers a question in my mind, specifically about 2017: how big a challenge will it be to fill the 2017 slots? It seems to me there isn’t much time left to fill the 2017 slots. Furthermore, airlines rarely place order on a whim for short-term delivery – it’s usually the result of a long, thorough planning and evaluation process. So when they order planes, especially widebodies, isn’t there a significant gap between time of order and 1st delivery? What is the typical time gap between order and 1st delivery? And what is the minimum (reasonable) gap that we can expect? Given that, how difficult will it be to fill the 2017 slots?

Sooner or later all these pigeons are gonna come home to roost. Especially the 27B crater sitting on the 787 books. Since McNerney is expected to retire in 2016, one can only assume they are trying to defy gravity until he leaves and all his options vest. Then KABOOM!!! Greed has no limit.

That would be a very noble gesture by all the other execs who are not leaving at the same point and who may well see the value of their own options plummet in the following period.

No-one seems to have noticed either that the downside of accelerated up-front payments will be correspondingly smaller ones on delivery!

I disagree, terms such as Robbing Peter to Pay Paul clearly recognizes that bringing payments forward is a short term gain at the expense of the long term cost to the company.

Its a strategy of desperation and the board should have taken action.

Clearly the board no longer functions as anything other than a rubber stamp.

“That would be a very noble gesture by all the other execs who are not leaving at the same point and who may well see the value of their own options plummet in the following period. ”

Those execs have no control, CEO controls, board oversees his (and other execs actions)

Their job in a truly capabilities system is to reign in the CEO if he has gone on a bender which clearly they have not.

The system is corrupted from what its supposed to be and how its supposed to work. We can call it a good old boys network, I don’t fathom the workings of it or why this has occurred but you don’t have know what has occurred, you can see the evidence (the quack, legs, fly, dive like a duck its a duck)

McNeneary belongs to an organization that wants to eliminate social security. Its a personal agenda that goes along with destroying unions. Personal agenda are not supposed to be business decisions but he is allowed to wrap his agenda with a lot of spin to make it look like a business decision (we are seeing the result of his decisions)

Execs are dealt with carrot and stick method. Ray Conner was making statements that were not in line with McNeneary concerning works and the future of the company,

He was given a fake promotion (title only, still head of BCA) and the line changed back to the party line. Obviously he was given a carrot and may or may not have been shown the stick, he got the point. Continued career and money or give the old heave ho (a lot of excecs from Boeing are gone, including the very successful O’Mally who saved Ford).

Sad state of affairs but its now the American way.

The Board situation needs reformed, how to do it I am not that kind of player, I can see it but I don’t know the solution. Until that happens we will continue to see this stuff go on.

Mark is right on-I can see the Boeing Everett flight line from my flat it’s all about turning Boeing into GE where only the top management comes out smelling like a rose. The only real solution @ Boeing is to dump McNerney now and get an old non Boeing aviation engineering professional to run it. Just a note: wait until the 787-10 sole sourced to Boeing SC goes south next year because SC just can’t cut it as well as Everett.

Pingback: » Daily Aviation Brief – 15/06/2015

Pingback: Aeroflot selling a quarter of its fleet; bad news for Boeing, Airbus | SkyWriter Aviation