Leeham News and Analysis

There's more to real news than a news release.

“MAD” at Airbus, Boeing?

Nov. 3, 2015, © Leeham Co. Aerospace analysts are weighing in on 3Q2015 Friday’s earnings call on the Airbus announcement that it will lift A320 production to 60/mo by mid-2019 and may go to 63/mo the following year.

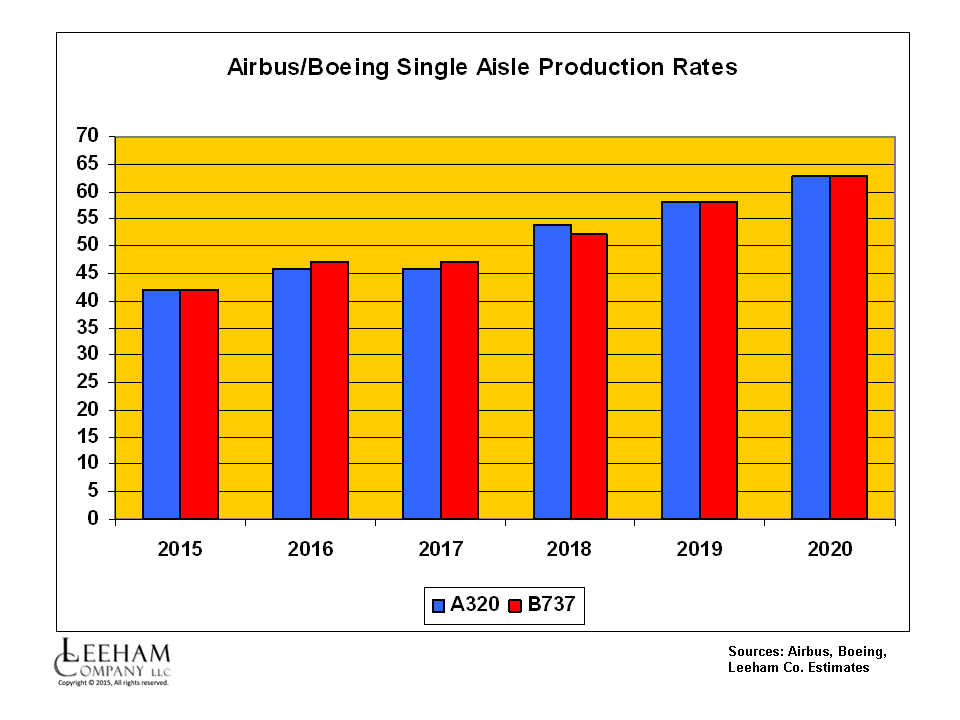

Figure 1. Click on image to enlarge.

Way back in February we predicted Airbus and Boeing will take their single-aisle production rates to 63/mo. (Figure 1.)

Ken Herbert, the aerospace analyst for Canaccord, noted that even with the same higher rates, Boeing will still out-produce Airbus because Boeing works on a 12-month year and Airbus shuts down the assembly line for a summer vacation. His forecast production chart takes this into account (Figure 2.)

Figure 2. Click on image to enlarge.

We generally agree with his numbers, including his prediction that in 2018 Airbus will out-produce Boeing. We think there is a likelihood Airbus will do so in 2017 as well, with Boeing 777 Classic rates coming down to a lower level than Canaccord predicts. We’ve highlighted in yellow Airbus and Boeing rates that we think will be lower than Herbert suggests. We also did the math to show the production market share between the two companies on an historical and forecast basis.

Concerns over whether the supply chain can meet the higher production rates have been widely reported. Canaccord’s Herbert identified 11 companies that are key in the 737 supply chain that are public companies he follows:

| 1. Astronics

2. B/E Aerospace 3. Crane 4. Ducomm 5. Esterline 6. Hexcel |

7. Precision Castparts

8. Rockwell Collins 9. Spirit Aerosystems 10. TransDigim 11. Triumph Group |

“Due to its oversize exposure to the 737, we believe Spirit holds significant bargaining power as Boeing looks to take rates higher on the 737, and would not be surprised if there were additional capex or pricing benefits for Spirit if Boeing does in fact look to take rates to ~60/month,” writes Herbert.

“Note that since Airbus takes extensive shut downs in the summer months, this rate of 60/month is basically the equivalent of 55/month for Boeing in terms of delivery slots,” Herbert writes.

“Are we approaching mutually assured destruction?,” Herbert asks. “The primary risk remains the length to which Airbus and Boeing can sustain these unprecedented production rates. We believe this announcement by Airbus is a bullish statement for the aerospace cycle in general, but we believe it does favor the suppliers in the OEM-supplier relationship. Moreover, we remain bullish on the commercial OE cycle, but production rates at these levels are unprecedented, and do add risk for the suppliers, especially if these rates are not sustainable.”

Doug Harned of Bernstein Research also believes Boeing will match the Airbus production rate increase.

“We believe Boeing will likely respond with a 737 rate increase, but that decision could come later,” Harned writes. “Like Airbus, Boeing has also said that it is oversold on the 737MAX, with its rate going to 52/month in 2018. We normally consider market share unimportant in this industry, but for narrowbodies it can matter. This is because once airlines choose a narrowbody platform, they tend to keep it forever. So, Boeing will not want to miss opportunities to keep airlines as 737 operators, which will likely mean an eventual rate increase. Our understanding is that Boeing can wait longer to announce, if it wants to take rate up in 2019. To match the rate increase from Airbus, Boeing would need to take 737 rate up to 57.5/month (this equates to 690 aircraft per year, since Boeing is on a 12 month year, versus the 11.5 month production schedule for Airbus narrowbodies).”

Isn’t “Werksferien” limited to Airbus in France and VW in Germany ;-?

Expanding production in Germany should thus result

in a slight increase in “month per year” production.

( I’ve seen estimated of 11.5 to 11.7 )

The “Real” metric will be deliveries per year.

How did that comb together in the last years for

A and B ?

( 2014 :: A:40.83/m B:40.42/m.

What were the “officially communicated” production rates for 2014?)

official and stable rate for 2014 seems to have been 42 ( nice perfect number, that 🙂

That would result in a “loss” of ~1.2 frames per month

or equivalent production at rate 42 of 11.7 month per year

Thus Ken Herbert’s computation seems to be scraped from hot thin and stale air 😉

Herbert is wrong with his monthly computations … even for France

People in large companies do not take their hollydays all together in August … most of them go out 2 to 3 times a year BUT THE FACTORIES STAY OPEN 12 month per year production may stop 1 or 2 days between Christmas and New year for so called “inventaire”.

If he’s wrong it’s surprising that Scott let it past. Maybe he will address it in a future post or he agrees with him.

I too am skeptical of the figures as when I check the match, Airbus and Boeing made virtually the same number of single aisles last year despite the so called monthly production difference.

I think it was 2 to Airbus favor.

We get another good check in a couple of months.

Scott is not always checking what comes on t

his blog !!!

In this case as owner of a small company (150 workers only) in France I guess I know the subject … many times the French holidays comes up when talking about monthly/yearly production = 11/12 month per year.

However, my factories close during August BUT we deliver our customers from “over producing” previous months !!

I am eagerly waiting for Scott comments … just in case that I am wrong !!! = 🙂

Airbus announced to open another A320 line in Hamburg. So the French holiday fraction will shrink.

I’m not sure production centers in Germany, UK, Spain too have production halts, neither end lines in China and US.. this is not widebodies.

lately I see many 737NG being changed into MAX orders. Few 737NG are widening the 737 production gap.

https://leehamnews.com/2015/09/02/boeing-faces-737-production-gap-analysis/

Boosting production before MAX might seem a bold move, but they have to sell them first.

There a significant backlog gap between the A320CEo+NEo and 737NG+MAX. While 60 might be realistic for the A320 it isn’t automatically for the 737 too.

A few substantial A321 orders from e.g. DL, UA, JAL, a few hundred “undisclosed” orders / commitments vaporizing and NB strategy is back in the board room earlier then hoped.

http://www.pdxlight.com/neo3.png

60 737’s a month

The graph that speaks to me most is the bottom one on this page: http://www.pdxlight.com/neomax.htm

It says that the NEO-MAX marketshare ratio has stayed stable around high-50s to low-40s for close to three years now. Which does argue that Airbus can sustain a higher rate than Boeing.

One thing to keep in mind is the production rates of the 787. Each year it has grown substantially. At the beginning of Nov, Boeing is at the number of deliveries it had in all of 2014.

That actually is equivalent to a 20% increase.

On the other side posters already moan over “a350 will double deliveries in 2016” as much too low and “a lot of catching up to do” 🙂

Having to double the deliveries in 2016 has more to do with the slow rate in 2015 than with the rate in 2016 being slow. I think that’s what the “catching up” comments refer to.

Mea culpa. Airbus has already delivered 5 350s this year… a 500% increase from lat year! 🙂

I think it’s actually 9 A350’s so far this year, so an 800% increase:)

A couple of FWIW thoughts:

1. Am I the only one who finds it interesting that year after year Airbus can “sell” more aircraft, yet Boeing always seems to “deliver” more? (and according to these charts is expected to continue to do so.)

2. Surely a better reference point would be revenue and profit for their respective commerical aircraft divisions rather than simply airframes delivered – it’s easy to move lots of frames if you give them away. Of course different methods of calculating “profit” would need to be adjusted between the companies to paint a clear picture.

year over year overdelivering Airbus? debatable, see: https://en.wikipedia.org/wiki/Competition_between_Airbus_and_Boeing#Orders_and_deliveries

The current overhang is mostly due to 787 ramp up.

3. Isn’t it a bit dated to attribute Airbus position to gifting away airplanes in a socialist jobs programme 😉

4. like for like profit reports are available for a range of years from Boeing reports under the “circumspect as non GAAP but required from some shareholders” moniker. for Airbus take the regular submittals.

5. Lots of guesswork around on rebates. But for me it looks like this is another discipline Boeing is excelling in 🙂

6.. I believe Bruce was referring to Boeing in point 2 though I might be mistaken.

7. Year after year out delivering Airbus is debatable?

Nothing to debate at all really. This will mark the fourth straight year they have delivered more planes. As for the excuse about the 787 ramp up, well sure whatever. I’m sure the 350 ramp up will have Airbus soaring to the top!Some year, maybe.>:P

8.”Surely a better reference point would be revenue and profit for their respective commercial aircraft divisions rather than simply air frames delivered – it’s easy to move lots of frames if you give them away. ”

Well that’s always the fanboy’s response to whenever the the “other” side makes big sells! Truth is both makers discount about equally so going by list prices doesn’t change the ration too much.

9.”Lots of guesswork around on rebates. But for me it looks like this is another discipline Boeing is excelling in”

So of course you guess Boeing. I’m shocked, what a surprise!*\0/*

It’s all good. 🙂

6.. I believe Bruce was referring to Boeing in point 2 though I might be mistaken.

There is this apples and bananas issue with

IFRS reporting and GAAP enabled program accounting.

700 deliveries in 2020 by either? That would be a spike in the historical increase in deliveries over the past twenty years.

Questions/observations regarding table:

1. Is 777x delivery slated to begin in end 2019 and thus 2020 should have some 777x output?

2. The 747-8 deliveries are small regardless

3. The 380 is the line with the most doubt. There are roughly 165 orders left of which around 40-50 are questionable (Transaero 4, Skymark 4, Air Austral 2, Hong Kong 10, Virgin 8, Amadeo 20. Qantas 4, AF 2 options are also not guaranteed to be taken. BA option is also not for sure? 7).

So 48 to 61 of the orders are not rock solid leaving 104-117 to be delivered over the next 5 years. Given that 30 are delivered in 2016 and long lead times are 2-3 years… orders are a must very soon.

The chart suggests 188 deliveries through 2020. That leaves a shortfall of 71 to 84 new orders or confirmation of that many from the list above.

4. Airbus will likely produce slightly more narrow bodies (A 3056, B 2978), Boeing more many more wide bodies (B1315 to A1028) in the time period 2016 through 2020 presuming all lines perform as indicated and there are no further increases or decreases in production.

How can deliveries favor Airbus in 2017 if there is a 57 unit difference estimate right now and the yellow boxes are only around 777, 747, and A380s. If we assume that the A380 and 747 figures are equally inflated then the 57 unit difference would have to come from 777s but I have not seen anyone pessimistic enough to say that there will only be ~38 777s delivered in 2017.

I see 2018 being very close and 2019 being the next closest year in terms of total production by OEM but by 2020, under current announcements the totals should swing back to Boeing.

tortugamon

looking at the graph, in my opinion the market just doesn’t justify a production rate of 65 per month for the 737.

Maybe Boeing launches a replacement in a few years, pushing down 737 orders/ deliveries. Not unlikely at all.

https://leehamnews.com/2014/02/25/the-case-for-a-boeing-nsa-in-2025-successor-to-737-8-max-continued/

Due to other shortcomings availability ( and price ) probably is a major selling point for the MAX.

Boeing has to burn through their backlog.

Keesje:

Boeing has sold a lot of MAX, the issue really is if it can continue to do so in the long term (out past 2020 or 25)

Transworld IMO the 737NG backlog is limited and might be shrinking, the MAX will enter production no sooner then it will.

So Boeing has to balance 737NG production into 2018 and I wonder how a 737 production increase in 2016 and 2017 might fit in ..

Beyond 2018, the apparent gap depends largely on the delivery stream of “Unidentified” 737 customers accounting for more than 1000 737st according to Boeing.com

350 of those “Unidentified” customers are for 737NG’s. So those must show up pretty soon now. Analysts are taking a blind eye.

I guess you don’t understand my take

Its not that I think its clear sailing for Boeing, but all they have to do is shift production to the MAX if sales don’t continue (or they want to shift to the MAX). They had people who wanted the old aircraft last time and are working it to accommodate that.

Regardless they have orders for 50 a year for a while. Will those all hold up? Maybe, maybe not, Airbus has the same issue (and do others want to advance the order)

Personally I think they are both nuts, and the MAD is spot on. They may produce themselves into a compete single aisle shutdown.

But if as I expect its across the board (affect both A and B) then they both will suffer the same.

Will see of course.

Boeing comes out with the MOM and suddenly they are back in the spotlight. Or maybe not.

The big elephant in the room is the assumption that CFM can ramp-up production of the all new LEAP-X to 180 units per month – assuming CFM will have market share of 50 percent of the A32Xneo market – over the next five years.

http://www.seattletimes.com/business/boeing-aerospace/new-737-max-engine-development-going-well-but-60-jets-a-month-may-stretch-limits/

They have plenty of time and money to get it all going.

Big elephant in the room is does the world need 120 single aisle a month?

Plenty of time?

Assuming P&W will split the A32Xneo market with CFM, they’ll “only” be producing some 60 PW1100G GTF engine per month by 2019. CFM, on the other hand, would have to produce 60 Leap 1As and 120 Leap 1Bs per month. Zero to 120 units per month over a period of three to four years. In comparison, CFM is currently producing about 1600 CFM56 engines per year – in a production system that has been fine-tuned over many years. Also, while the PW1100G received certification last year, the Leap 1B engine for the MAX will only see certification next year. Assuming, therefore, that going from zero to 120 units per month over a period of three to four years, won’t be much different from what they’re currently doing, seems to be somewhat optimistic – count me in as skeptical.

Production jacking is the only way that enables Airbus to continue poaching the single aisle market away from Boeing.

The planning that will make the 60/63 rate reality has been a mammoth task, some including Leeham had the foresight to see the inevitability of this decision which smoothly slots into the Airbus’s aggressive long term growth strategy, which has only one target, Boeing.

Comparative sales seemingly prove Airbus has got it right in terms of single aisle product. Boeings own product & production jacking is more often seen as a knee jerk protective reaction to address it’s declining crucial single aisle market with an airframe that for a host of reasons has declining popularity.

Good aircraft Airbus is offering of course have nothing to do with it.

“Airbus’s aggressive long term growth strategy, which has only one target, Boeing.”

I wonder why some think so.

Airbus do market studies, talk to their global customer base and look for new opportunities to sell more / grow. As the industry has been doing for 100 years.

The A300 was the first big twin, the 330/340 launched before the 777, A380 the first 500+ seater, A350 to replace A340s, A400M for European requirements, 320NEO was ahead of the MAX and A330NEO based on customer demand.

Regardless of what others like Boeing think /do.

The 350 was clearly in reaction to the 787.

The A350 mk1 was, the XWB is bigger & will replace A340s and 777’s everywhere. Not A330s/767s.

What are the deliveries in the chart for the 747 past 2017? I checked and the plane only has 21 unfulfilled orders when you take away Arik Air’s two which I doubt will ever get delivered. By my calculations if Boeing will not get any new orders it will be forced to shut down the 747 line in the summer of 2017 even with this snail pace production.

Back when the first (or was it second) tanker deal was being done, Harry Stonecipher was trying to put pressure on the USAF to get the deal done quicker by stating that the 767 line was close to being shut down (any time in the next year, I believe) and if that were to happen, it would be more expensive for the USAF to get their tankers from Boeing.

So about 10 years later, we still have the 767 line going, and I don’t think it had ever actually shut down.

Moral of the story, don’t underestimate their ability to keep a line going, if they think they need it for the future.

The reason to keep the 767 running was a tanker deal of 179 aircraft. In the mean time Boeing sold cheap freighters to keep the line busy.

For which important deal should Boeing keep the 747 line open?

Yep, that’s a big question

A380 is also a question, just a bit longer before it bites though.

Long lead items start to become a major factor.

I think the OEMs are crazy to go to those production levels on the single-aisle.

I can’t help but wonder if we are starting to see early warning signs with some of the sporty backlog orders.

http://www.businessinsider.com/r-exclusive-airasia-founder-began-buyout-talks-as-share-fall-put-loans-at-risk-sources-2015-10

That is one of the Airlines that is on the Leeham “watch” list.

At some point they have to make profits and when that does not occur the party ends.

Not an easy thing to do is run an Airline even when you have experience.

Let me dwell somewhat upon OV-099’s remark concerning CFMI’s headache : 180 engines per month and 22 work-days in a month, plus 1 spare engine every 7 deliveries, that rounds up to between 9 and 10 Leap engines per work-day … so when eventually the production black monday will sound its toll, then that sad day the social workforce crash of CFMI will be particularly severe … Wonder why Rolls Royce are not coming forward sine die with an engine programme in the 33-43 klbf bracket, to reach out with a helping hand making life easier for P&W and CFMI ?

It’s my understanding that RR is planning to re-enter the single-aisle market with the UltraFan engine, a decade hence. The UltraFan should be at least 10 percent more efficient than the Leap A engine on the A32X-neo. With a 15:1 bypass ratio, the UltraFan would not be suitable for the MAX, though.

@ OV-099 : Yes, I’m aware of the UltraFan but a decade (2025 ?) from now means a lot of water under the bridges of the river Arno @ Firenze. A lot of potentially rewarding business available to a third player would go lost. I’m convinced P&W and CFMI would welcome RR into the envied Club of engine suppliers into the MAX and NEO programmes, be it only to split the overall ramp-up RISK with a third MAD engine OEM ? Possibly, RR could rework the geometry of the RB211, of proven reliability, or scale down the latest of Trent geometries to come up with a 1:12 BPR revised (PIP’ed. upgraded, reworked …) contraption, to pick up one third of this gigantic business ? We are talking of approx. 80 engines per month for RR, a very attractive perspective, oder ? This would balance out the excessive risk falling upon P&W and CFMI if these two asked to alone gear up to the Narrowbody market folly !

@Frequent Traveller

The three spool architecture doesn’t scale down well with curent tech. Next Genration turbofan engine designs are aiming to achieve higher bypass ratios (i.e. more air) and lower fan pressure ratios. Very high bypass ratios involve the use of fans with very large fans – unless you split the fan in two parts and contra-rotate them, because contra-rotating fans having the same diameter as a single fan allows for a significant higher bypass ratio.

One interesting aspect about the three spool architecture, is that you could conceivably put a geared second fan that is contra-rotating to the first non-geared fan – on the intermdiate pressure spool, which would be contra- rotating to both the low pressure spool and high pressure spool. Hence, it might seem as if RR could have a massive untapped potential with their unique three spool/shaft architecture.

IMJ, therefore, a contra-rotating three-shaft engine – where you’d have the first non-geared fan on the LP shaft and the counter-rotating geared fan on the IP shaft and with the second fan having a slightly higher angular velocity than the first fan – might be able to scale down better, as you’d be getting a super high bypass ratio without having to increase the fan diameter.

“One interesting aspect about the three spool architecture, is that you could conceivably put a geared second fan that is contra-rotating to the first non-geared fan”

You could have the same setup from the

gearbox ( and an attached set of fanblades 9 as the counterrotating element.

i.e. you do not return the reactive moment of the gearbox into the engine chassis but into a counterrotating fan.

for the same internal gear ratio you’d get twice the effective reduction.

Well, the second fan contra-rotating to the first fan should ideally have a higher RPM (i.e. up to 10 percent faster rotational speed). I’m not sure how you’d accomplish that on one shaft with a fixed gear ratio of, say, 3:1.

With a “loose gearbox” the drive moment for one fan is the complementary of the other fan +- the moment introduced on the input. thus you have to manage the rpm balance via power takeoff in each fan.

( someone did a model flying saucer design in a similar way.

center upright engine drove a propeller as first stage

while the reactive moment turned the fuselage as second fan in the opposite direction.)

.

I did my Engineer’s Memorandum with SEV Marchal (Valeo Group) on applications of the Epicycloïdal Gearbox, that allows to play with two energy sources (whereof one is reversible)/one sink i.e. alternatively one energy source/two sinks … I fathom UWE’s “loose gearbox” could possibly have points in common with the epicycloïdal gearbox, oder ?

Well, the GTF gearbox is an epicyclic solution to start with.

Currently the reaction force is taken up by the chassis/stator of the engine.

( the Toyota Prius sports a rather involved multiple power takeoff/insert architecture. rather intriguing design.)

for an example you can look at the NK-12 counter rotating props turboprop engine.

Well, where your gearbox seems to be quite a bit more intricate than a normal gearbox, I prefer to keep it simple – using an existing engine architecture, only adding one gearbox to the IP spool. 🙂

Also, there’s a reason why gearboxes have been in use on turboprops for more than 60 years, but only now being introduced on turbofans.

As for the NK-12, it’s my understanding that the engine had two separate units, each with its own compressor and turbine driving a single gear box with two output shafts driving the counter-rotating propellers.

BTW, here’s an interesting piece on the challenge of scaling up for the GTF:

http://www.bloomberg.com/news/articles/2015-10-15/pratt-s-purepower-gtf-jet-engine-innovation-took-almost-30-years

a.

this would actually take the same gearbox but fit blades to the box itself. sounds funny, sure.

b.

IMU that was the predecessor TV-T2

see forex:

https://docs.google.com/document/d/1QU_74YJ_JEl3_W_EFP-58rlLC0CvzoF5DTUqm6XLugg/edit

c.

your link :: interesting.

afaik the primary issues was transferred power.

( reason why GTF designs were limited to smaller engines.)

napkin computation of the most simplistic kind:

TP400D6 sfc .162kg/kWh @ 8800kW –} 1440kg/h

take as reference

CFM56 sfc .33 lbs/lbsfh fuel flow 3173kg/h –} 9614lbsf thrust. a rather small jet engine.

Well, I’d like to see a practical counter/contra-rotating fan sooner rather than later. Combined with a 70:1 overall pressure ratio and intercooling or intercooling/recuperation, you’d probably see this implemented on larger WB engines as diameter of the the compressor and turbines will have to be smaller. This means that the core wouldn’t scale down well for single aisle applications due to shaft stiffness issues for a three spool architecture. So, a geared two spool architecture is probably the way to go for single aisles.

http://www.icas.org/ICAS_ARCHIVE/ICAS2010/PAPERS/408.PDF

I think RR is planning a new engine scalable in the 28-43klbs range. likely aimed at NSA, maybe A32X, and medium sized / range aircraft being considered by Boeing and Airbus. Setting it part from the CFM LEAP and PW1000 offerings.

http://i191.photobucket.com/albums/z160/keesje_pics/Airbus%20A360%20Concept_zpszrtxls4q.jpg

I wonder about the A380 line rate and how sustainable it is.

Here is a good synopsis on that by CAPA.

http://centreforaviation.com/analysis/a380-fleet-profile-emirates-prepares-for-615-seat-configuration-sia-will-dispose-of-early-models-249033