Leeham News and Analysis

There's more to real news than a news release.

Farnborough Air Show: No NMA, unlikely A321 Plus, no Boeing-EMB tie up

Subscription Required

Introduction

June 25, 2018, © Leeham News: Little in the way of excitement is expected at the Farnborough Air Show next month.

There won’t be any launch of the oft-talked about Boeing New Midmarket Aircraft (NMA, aka 797).

There won’t be any launch of the oft-talked about Boeing New Midmarket Aircraft (NMA, aka 797).

Airbus continues to be coy about its response to the NMA. Studies about an A321neo Plus or Plus-Plus have been talked about almost as long as Boeing has been discussing the NMA. More recently, now there’s talk of an A321 XLR.

Summary

- Expectations for incremental airplane orders at the show should be low.

- No NMA program launch.

- Doubtful if Airbus launches A321neo enhancements.

- Airbus-C Series makes its debut—but to what end?

- Mitsubishi to showcase MRJ.

- Bombardier renews emphasis on Q400, CRJ.

- Embraer looks for order boost.

Pontifications: Rockwell buying B/E Aerospace: getting out while the getting is good?

By Scott Hamilton

Oct. 24, 2016, © Leeham Co.: An announcement Sunday by supplier Rockwell Collins (NYSE:COL) that it will acquire B/E Aerospace (NYSE: BEAV) for $6.5bn caught analysts by surprise. The price tag rises to $8.3bn when assumption of BEAV’s debt is included.

The surprise is not so much BEAV is selling itself. A few years ago, BEAV sold of one of its division and analysts since then believed an exit strategy was underway for the principal owners of the company.

The surprise is that the buyer is Rockwell, a supplier that has little in common with BEAV. A slide from Rockwell’s own investor presentation Sunday illustrates the point.

Rockwell will have an investors’ call Monday at 0830 EDT to further explain the merger.

Weekly analyst synopsis: Farnborough recap

July 20, 2016: Aerospace analysts had somewhat different takes on the commercial aviation portion of the Farnborough Air Show. This week’s analyst synopsis includes some of the analyst reports. Between now and the end of the month, earnings season begins reporting the second quarter results. Airbus reports July 27. So does Boeing. Bombardier and Embraer report after July.

July 20, 2016: Aerospace analysts had somewhat different takes on the commercial aviation portion of the Farnborough Air Show. This week’s analyst synopsis includes some of the analyst reports. Between now and the end of the month, earnings season begins reporting the second quarter results. Airbus reports July 27. So does Boeing. Bombardier and Embraer report after July.

Analysts opine on Airbus, Boeing, Iran and Brexit

Click on image to enlarge.

June 24, 2016: Brexit continues to creep into US analyst reports for the potential impact of companies doing business in the United Kingdom.

But there are other issues as well. Highlights this week:

- Spirit Aerosystem is a supplier to Airbus and Boeing. Deliveries to Airbus for the A350 continue despite program delays. Negotiations continue with Boeing over new contract terms. (Buckingham.)

- Don’t freak out over the Southwest Airlines deferral of Boeing 737 MAX. (Credit Suisse.)

- The Iran deal isn’t a big deal yet for Boeing. (Goldman Sachs.)

- Brexit may benefit B/E Aerospace. (JP Morgan.)

- US trans-Atlantic airlines likely will be hurt by Brexit but purely US domestic carriers are fine. (Morgan Stanley.)

“MAD” at Airbus, Boeing?

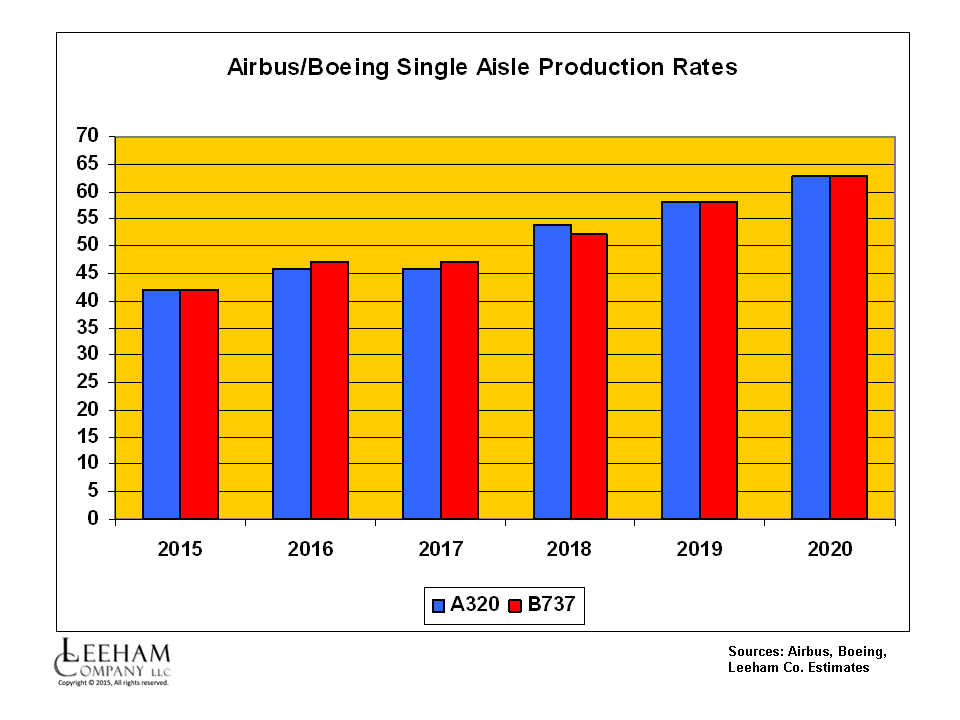

Nov. 3, 2015, © Leeham Co. Aerospace analysts are weighing in on 3Q2015 Friday’s earnings call on the Airbus announcement that it will lift A320 production to 60/mo by mid-2019 and may go to 63/mo the following year.

Figure 1. Click on image to enlarge.

Way back in February we predicted Airbus and Boeing will take their single-aisle production rates to 63/mo. (Figure 1.)

Ken Herbert, the aerospace analyst for Canaccord, noted that even with the same higher rates, Boeing will still out-produce Airbus because Boeing works on a 12-month year and Airbus shuts down the assembly line for a summer vacation. His forecast production chart takes this into account (Figure 2.)

B/E Aerospace sees “flat” widebody deliveries through 2016

Aug. 12, 2015, © Leeham Co.: Widebody deliveries are “flat as a pancake” and will remain so through 2016 before going up, driven by the Airbus A350, says a major  supplier.

supplier.

Officials of B/E Aerospace appeared yesterday at the Jefferies Co Global Industrials Conference, making the near-term forecast. B/E is best known as a seat supplier but also supplies galleys and lavatories.

With passenger load factors now routinely running around 85% and traffic growing, B/E’s backlog is greater than ever and the OEMs, pressured by airlines for on-time deliveries, likewise pressure suppliers. B/E competitor Zodiac had difficulties meeting demand late last year and early this year.

“You cannot image how much stress is created cannot deliver an airplane on time and the reason is a supplier,” a B/E official said. B/E has been able to keep up with demand.