Leeham News and Analysis

There's more to real news than a news release.

Boeing posts 2019 loss, IDs $9.2bn in additional MAX charges, costs

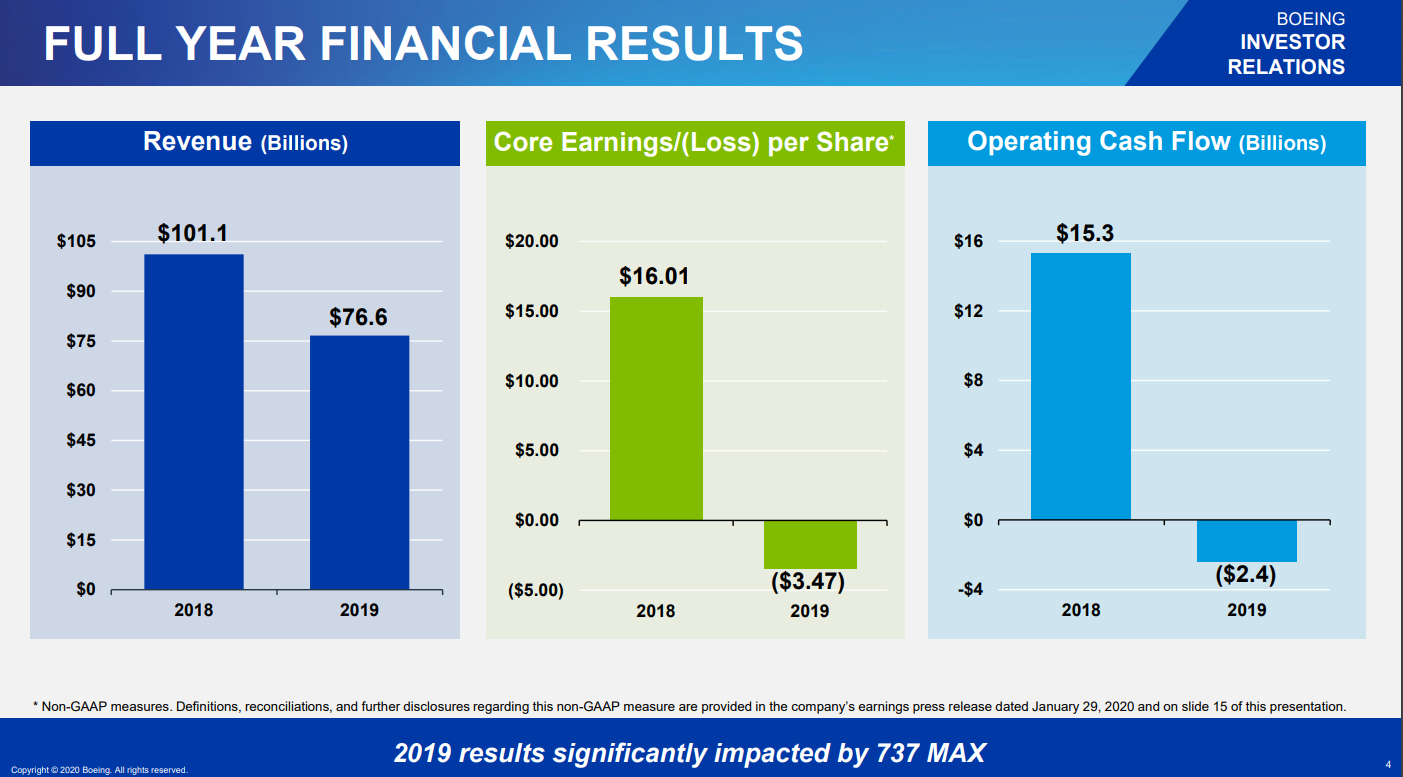

Jan. 29, 2020, © Leeham News: Boeing today announced a full year loss for 2019, as expected.

- Revenue of $76.6bn, GAAP loss per share of ($1.12) and core (non-GAAP)* loss per share of ($3.47)

- Operating cash flow of ($2.4bn); cash and marketable securities of $10bn

“We recognize we have a lot of work to do,” Boeing President and Chief Executive Officer David Calhoun said in a statement. “We are focused on returning the 737 MAX to service safely and restoring the long-standing trust that the Boeing brand represents with the flying public.”

Boeing ended the year with $10bn in cash and marketable securities, down slightly from the $10.9bn at the end of 3Q2019.

Debt rose slightly to $27.3bn from $24.7bn at the end of the third quarter.

New charges

“An additional pre-tax charge of $2.6bn related to estimated potential concessions and other considerations to customers related to the 737 MAX grounding,” Boeing said. “The estimated costs to produce 737 aircraft included in the accounting quantity increased by $2.6bn during the quarter, primarily to reflect updated production and delivery assumptions. In addition, the suspension of 737 MAX production and a gradual resumption of production at low production rates will result in approximately $4bn of abnormal production costs that will be expensed as incurred, primarily in 2020.”

This totals $9.2bn, slightly less than the $10bn anticipated by some aerospace analysts.

The press release with full financial results may be found here.

The earnings webcast is at 10:30 Eastern time and may be listened to here.

Hi investor chappies, I will sort it all out.I am ‘new’ let’s get all of the bad news out of the way ASAP. At least I hope it is all the bad news..

Mr Calhoun

not on the safe side!

quite a few MAX costs are delayed on 2020

787 deferred costs will not go down quickly at 12/month rate

even slower at 10/month

and who can believe that the rate will bounce back to 12 in 2023?

“As previously announced, the 787 production rate will be reduced from the current rate of 14 airplanes per month to 12 airplanes per month in late 2020. Based on the current environment and near-term market outlook, the production rate is expected to be further adjusted to 10 airplanes per month in early 2021, and return to 12 airplanes per month in 2023”.

all Leeham readers are aware that WB sales are slow, and will remain slow during quite a few years….

also 777X will come later than expected, with higher certification costs….

2020 will certainly be ugly

and maybe 2021????

So, negative cash flow from operations, net loss, but are they still persisting in paying dividends for some reason?

I know, crazy.

But @Rob probably will explain you soon in 500 PR words that is completely “normal” that a company in troubles first pays dividend then takes a huge loan to maintain liquidity.

So true. Expect the tsunami that we call Rob.

Not so much a tsunami, as adding balance and perspective. Issues have multiple sides and are often not as simple as they first appear. So here is some balance and perspective on the dividend issue:

Boeing has long pursued a stable dividend policy. They’ve paid dividends without interruption for 80 years.

The stable policy means payout is based on the long-term average income of the company. It can change over time as the average income changes. So losses at Boeing now will likely impact future dividends.

To use this policy, the company must have large capitalization and internal equity. Buybacks were one method to generate that equity. These characteristics are generally true of large aerospace companies. It was true of Boeing until the MAX crisis. But until MAX deliveries and income can resume, their internal equity is no longer sufficient to maintain liquidity, hence the borrowing.

Dividend policy also impacts the kind of investor. Stable policy attracts committed investors looking for reliable income (for example, retirement), as opposed to speculative short-term investing. This reduces the stock price volatility and holds the stock value. As we’ve seen, Boeing investors have not deserted or sold off their stock, even in the face of significant financial difficulties. It also makes obtaining credit easier.

Another factor is the perceived investment competition. Boeing has to compete for investor dollars, as well as customer dollars. Aerospace companies traditionally have good dividend yields. Boeing pays a yield of 2.2%, Lockheed pays 2.4%. United Technologies and General Dynamics are at 2.3%.

Another indicator is payout ratio to earnings. Boeing is at 40%, Lockheed at 43%. United Technologies is 37% and General Dynamics is at 34%.

Whether or not Boeing can sustain the stable policy, only time will tell. I suspect Boeing will try as they always have, and if they can’t, will gradually ramp down dividends before possibly changing to a different policy based on shorter-term income. A disadvantage of the stable policy is that it’s not easy to change, as once in place, it’s viewed as a strong indictor of stability.

So if I understand you correctly stable policy is an indicator of .. erm.. stability….

I have never read such management hogwash in a long time. You are suggesting investors look no further than dividends. That may be the case if the company’s underlying performance is normal. At present Boeing is not normal, it is thrashing about in what could be death throes. In this circumstance the dividend is a single ray of superficial good news in an otherwise starkly bleak outlook.

Issues have multiple sides and are often not as simple as they first appear. So here is some true balance and perspective on the dividend issue

Sowerbob, this all depends on your perspective. It’s true that the benefit of stable policy is that it creates stability, or at least the perception thereof.

If Boeing is riding through a rough patch with the MAX, but is strong otherwise, as they claim, then the stable policy is a reasonable approach, and a continuation of long-held practices. In that case the perception of stability is accurate.

If instead, as you claim, Boeing is in dire straits and is about to fail, then the stable policy will hasten their downfall, and is only a mask for their internal problems. In that case the perception of stability is inaccurate.

Like I said, time will tell. At least for now, the market does not agree with you.

There is legitimate concern that the payout was too high for the given financial statements, in my opinion. Boeing has been working to increase dividends for several years, and could have paused or suspended the increase for this year. That would have been a more cautious approach. I think investors would have understood that. But, I don’t make the decisions.

Possibly Boeing committed to the increase in late 2018 before they realized the extent and duration of the MAX crisis. I guess we’ll see in a few weeks when the first 2020 dividend becomes due.

If instead, as you claim, Boeing is in dire straits and is about to fail, then the stable policy will hasten their downfall, and is only a mask for their internal problems. In that case the perception of stability is inaccurate.

You know I didn’t say that but have chosen to twist my words to fit your comment. I said that Boeing is not in a normal operating environment and is flailing around. It does not have a coherent strategy of that we both must agree on surely!

There is legitimate concern that the payout was too high for the given financial statements, in my opinion. Boeing has been working to increase dividends for several years, and could have paused or suspended the increase for this year. That would have been a more cautious approach. I think investors would have understood that. But, I don’t make the decisions.

No,you don’t make the decisions, instead you contrive an ‘independent stance’ when being a Boeing apologist. Any situation where a company is brewing heavily to effectively fund a dividend is going to be suspect. At the very least leverage is increased and they are effectively mortgaging the future to pay for the present.

This is not a calm, measured response to the decision as to how to best satisfy shareholders but rather a desperate means of shoring up the share price when all other news is bad. Investor gurus (a contradiction in terms maybe) have consistently been bullish about BA stock. I understood this even a year ago, simply then a Boeing was a cash machine. Now I look at the FS and the annual report and knowing about the state of their many programmes this mystifies me. I believe most are unwilling to be seen to change their call

Sowerbob, you used the term “death throes”. There was no ambiguity about your meaning or intent. Or in your other comments here.

Boeing has borrowed about $20B in the last year against a MAX inventory of about $25B, not counting any other assets. The first $10B was in their already established line of credit. The dividend payout to investors was about $4B, and Boeing would have planned for that in 2018 or earlier, as it results from a stable policy.

There is no need to apologize for Boeing unless you believe the company is fundamentally wrong, as you obviously do. You’re welcome to that opinion, but you have to understand that not everyone shares it.

“So if I understand you correctly stable policy is an indicator of .. erm.. stability….”

Essentially “wagging the dog permeates everything in that domain, it is the core mechanism”. 🙂

Uwe, stable policy is the formal name of one of several dividend policies that companies may use. It was given that name because the dividend is stable over time. Companies that use it are also viewed as stable themselves, if they can sustain it over a long period, as Boeing has.

It’s a pretty basic concept. I gave you the data and an explanation to help you understand. You’re welcome to look it up for yourself.

It all does not take away from the (superficially good) performance indicators being synthetic. faked.

Wagging the Dog.

Cargo Cult.

History is full of companies giving out too high dividents for too long. The Krueger crash is one of them, his companies got dependent on big bank loans and once the Banks teamed up and decided to kill his companies and let their other major customers divide its assets it was over. Boeing is not there yet but needs to modernize its narrowbody product line pretty quick. The 787 cannot alone carry Boeing Commercial Aircrafts on its sholders even after the 737MAX get recertified. One problem is that with its smaller gear and engine diameter it was optimized for the 787-8 and Boeing Chicago let the 787-9/-10 be marginal products not as flexible as the A321neo.

Claes, the Kreuger crash was caused by a Ponzi scheme. His conglomerate had a balance sheet with roughly 50% to 60% of assets that didn’t actually exist.

It’s true that he paid good dividends, just as Bernie Madoff did. But those are far different situations than Boeing.

Rob,

Circular argument, circular reasoning. Please read this link:

https://en.m.wikipedia.org/wiki/Circular_reasoning

wow, $19.5B profit delta on $24.5B revenue delta…

certainly not all of that profit delta is directly attributable to the lost sales, but wow.

I would suspect that some of it is due to keeping 420 737s on the books at “book value” rather than actual cost.

I also expect that this is the new CEO’s opportunity to get as much bad news out in one go while he can still blame it on the old CEO, so there are probably a lot of things in the books structured to make this report as bad as possible so they can show miraculous recovery as soon as the MAX is recertified.

On the contrary, I expect there is more on the books thats transfered to 2020. I expect FY20 will be worse and expect losses over the next three years.

This train wreck named Boeing is still skidding off the tracks.

I think you are both correct. Bilbo doesn’t say there won’t be more, simply “get as much bad news out” as possible, which I think they’ve nailed (financially) by coming out just a tad better than expectations. But is this all the bad news ot bed? No.

This will be the only quarter that posts losses though. Going forward Boeing will post small gains while they distribute the impact across several years of profits. Watch the stock buyback as the indicator of Boeing’s health. You’ll know there’s a problem if the buyback gets suspended in order for Boeing to show a profit.

The plus is that money was spent building 737s that they couldn’t deliver, but those planes all have owners names on them and almost as good as money in the bank.

For anyone else the drop in cash flow would have dire consequences but Boeing is big enough to tide over. What isn’t so easy to explain is the integrity deficit that meant Boeing has been in denial for at least 6 months about their Max problems and the pathway to re certification

Better than someone expected at some point, so positive.

Interesting interview of Dr. Keiser on https://YouTube.be/dOn-NF-MAI-o regarding BOEING’S Cash Health position.

@Norm: Link does not work.

https://YouTube.be/dOn-NF-MAI-o

Sorry Scott🙏

Interesting interview on Dr. Keiser on BOEING’S CASH HEALTH.

https://YouTube.be/_dOnNF-MAI-0

https://youtu.be/dOnNF-MAI-o

Here we go again, and hope it is Ok this time around

Link still does not work!!!!

Last chance. Check on You Tube RT News, “Keiser Report: QE 4Ever(E1494), published yesterday.

Never have I heard more garbage than this.

And this is coming from somebody on the complete opposite side to Boeing.

RT is well known as an outlet for propaganda. An extension of the Russian government. So have to keep that in mind for anything they publish.

http://www.youtube.com/watch?v=dOnNF-MAl-o&t=4m10s

–

https://www.rt.com/business/479396-boeing-garbage-company-walking-zombie/

Wow, thanks OV-099 for your expert indications of the Keiser article👍

Any news on the 777W production rate for this year and the next?

I am afraid the assembly line will be slowing down to a drizzle long before the 777X deliveries pick up steam.

Also did anyone ask Calhoun what he anticipates on deliveries to Chinese airlines of any aircraft family now that the virus epidemic has caused most to slash their flying schedule by a third or more?

It’s about right at the moment. But downstream expect the numbers to double, if not triple.

This view that the revenue will return is fanciful. If Boeing act now with a new FSA/NSA then they can expect a significant reduction in the revenue stream for now, but it will begin to return in 2027. If they delay they will be another MDC.

Will Boeing go out of business? No. Military contracts say no. But a major player in the commercial aviation market? Not unless they act with a new FSA/NSA.

Boeing need to take the hit, but rise from the ashes. As it stands they are burning in the ashes.

Why double or triple philip? Any particular drain/cost you see contributing the majority of this? I remember doing a quick calc last March (posted on a Leeham thread somewhere) suggesting to me an eventual US$15bn and rising. I haven’t recalculated since but off the top US$54bn feels too much.

Also, I don’t see revenue plunging absent some major new problem (eg if 787 reduced lightning protection proves inadequate, ME carriers drop the 777X, KC46 turns out to be a real dog, large parts of the global airline industry suffer a very large slump). After all, the 787 is a good aircraft for airlines, Airbus can’t provide a huge amount more than half of SA demand and the big military contracts look very solid.

Do you actually mean profit rather than revenue?

The costs of the MAX will double, perhaps triple. I don’t think they will be able to give away a MAX,

Just a view.

But why? Where do you see the additional US$18bn-36bn coming from?

Why?

Three parts:

1) I’m not of the view that Boeing have settled all compensation for non-delivery with regard to it’s customers. So there will be a lot more compensation costs.

2) Then wecome to the street value of a MAX. Prior to the crashes a MAX was worth ~$50 million. Typically that meant $10 million profit per airplane. It’s a ruff number, MAX contribution to profit was ~$6 billion. About ~600 were delivered per year. So $10 million profit per airplane. What’s the new value of a MAX. In my view a lot less than $40 million. They will be sold at a loss.

3) Legal compensation for misfeasance. Boeing are culpable all the way to the bone. To use Airbus, $4 billion. It’s going to cost Boeing a lot more than that.

Note all current contracts are void. Customers will wait until the regulators speak before making the decision on whether to accept delivery or not. If they accept delivery they will renegotiate the price.

I did note that other parts of Boeing’s business are healthy. Boeing only lost ~$600 million, even though the commercial side lost ~$6.7 billion. See Flight Global. So other parts made a profit of ~$6 billion.

They will be able to afford to build an FSA/NSA at $10-15 billion cost. They are down but not out.

OK, so you do actually mean profit, not revenue.

I agree broadly with points 1) and 3) that there is customer compensation yet to come and legal actions yet to reach the bottom line (and the latter is really the big unknown and why I wouldn’t dismiss vast additional costs out of hand).

But I don’t agree with 2). It is not in Boeing’s customers’ interests to cause Boeing to produce MAX’s at a (significant) loss for any significant amount of time. Unless financially engineered that way by eg folding any negotiated compensation into the purchase contracts, perhaps in order to benefit either party tax wise. I could see extended losses only if relatively minimal and if acting as a bridge to the replacement design. 7+ years would be a causeway, not a bridge.

I think I meant both revenue and profit. They will both go down,

With regard to 2). If customer can get it at half the price they will. So I do think customers will be expecting a bargain.

Suggest that while Boeing typically receives progress payments fornew ( MAX, 777, etc )aircraft, they do not get final ‘ check ‘ until delivery ( and hand over the ‘keys;.

Now with 400 plus produced but not delivered until AFTER rework and manintainance , any reasonable guess would be over a year until that backlog was zeroed out. meanwhile, production would start up, based on partial payments . . .

Thus, since MAX and related are( excluding military ) the major profit- revenue centers at Boeing- to say revenues will be a long time recovering to near previous grounding levels is IMHO not at all unreasonable.

But philip specifically indicated a belief in suppressed revenue thru 2027 at the earliest, not 2021-2022. If the MAX is returned mid 2020 the handover rate of frames (ie reaching the point the revenue comes in on the frame) combined with new production will start lower than pre 3/19 but it will reach a similar level (maybe shifted by some compensation or revisited contract terms etc) surely by 2022 latest.

Just watched Calhoun’s CNBC interview (https://www.youtube.com/watch?v=SxULJnNnBlU). I would like to believe him, I would like this all resolved and resolved well by mid year so that passenger safety is ensured and there is decent competition, but…

Again Calhoun makes, for me, simply unbelievable, without foundation claims to the returned to service MAX. At 3:46 he says “we believe this airplane’s safer than the safest airplane flying today”. OK, let’s excuse the broadness of the word airplane and assume he really means airliner, but seriously?!? I defer to specialists and experts in the various important fields but it frankly seems an outandish claim to make. And if he can make this claim, forcefully, not really pushed into it, straight faced, if this is not 100% accurate, how can he be trusted with anything else he says?

So, a question for Bjorn. In your opinion, will the returned to service MAX be the safest (airliner) in existence?

Woody, this is just my view, but I think Calhoun was providing a positive soundbite in the limited time he has to form an impression. In that format, he can’t launch into a detailed discussion of all the reasons he thinks the MAX is safe, or compare it to other aircraft. Nor would most people understand that. You would, but you are in the minority.

So he makes a broad general overly-positive statement that will convey the strongest possible impression that the MAX is as safe as any other current aircraft. That counters the overly-negative soundbites that have also appeared, such as flying-coffin, franken-plane and death-trap. Those are not factual statements either, they are meant to convey an impression.

So I would view it in that context, and not as a literal statement. It’s bombastic and exaggeration, but how TV journalism works in a format where time is provided for impression but not substance. The bottom line is that he believes the MAX is safe, but safest plane in existence would be very difficult to prove.

Bjorn can answer for himself, but he’s been on record that he would not hesitate to fly the MAX, once the issues are addressed.

The safety is heavily coupled to the maintenence program. In Soviet times before the split-up Aeroflot had few accidents flying Russian designed Aircrafts that was safe because of an intense maintenence program and on average well trained mechanics. The Aircrafts, Engines and systems were not competetive to Westen Products but still safe because of the intense maintenence done.

Woody,

It comes to these words: Forgiving, Margin (for error).

To use an article in FlightGlobal about A350 engine shutdowns caused by pilots spilling coffer over the centre panel. The coffer spill caused an inappropiate command to be sent to the right hand engine.

I’m sure Airbus will now provide better protection for the centre panel. But, without an airplane that was forgiving, without an airplane that has margin, there could have been a catastrophe.

Will the new MAX be forgiving, will it have margin? No, not in my view.

People are human. They make mistakes. Airplanes must be forgiving, they must have margin.

In that CNBC interview Calhoun says: It wasn’t automation that caused the accidents but rather that MCAS added complexity to a boundary condition that inexperienced pilots couldn’t handle! (at around 7:00).

Still blaming the pilots.

One might have thought the prolonged worldwide grounding should have been enough indication, even for Boeing’s management that the aircraft has a serious issue(s).

That’s very disrespectful to all those victims. It’s bad enough no one will ever be held responsible.

Here is the actual transcript. Becky characterized MCAS as being the incipient failure event, whereas Dave argued that the AoA sensor failure (boundary condition) was the trigger, after which MCAS contributed to the problem and made it worse.

I don’t think that was intended to blame the pilots, he just said they were inexperienced and MCAS then put them in a bad situation, for which Boeing is responsible. This was in the context of increasing automation in aviation.

BECKY QUICK: … But I’d argue the automation caused this to begin with. It could have been pilot problems on top of that, but it was the MCAS system that started the whole thing.

DAVE CALHOUN: Yeah, I’m not sure that I agree with that conclusion, Becky. … In those instances, we wish MCAS was different and it didn’t add to the complexity to that boundary condition that caused the problem. So, we wish that hadn’t happened. And the changes that we made to the flight control system now and it being certified today would not have created that instance. So, I don’t want to infer that it was automation that caused those instances. I think in those cases we didn’t get it right, in a boundary condition that some inexperienced pilots had to deal with. That’s a Boeing problem, and a very specific and discrete problem.

“added complexity” where a computer puts an aircraft repeatedly into a nose dive shortly after take-off is a bit of an understatement.

The correct thing to do would be to say that MCAS was not sufficiently tested and badly implemented and accept that it was the primary cause of the two accidents.

Calhoun did say, later in the interview, that MCAS was not tested for the boundary condition that occurred (failed AoA sensor). He also said that Boeing didn’t get the implementation right. But he has not accepted full responsibility for the accidents because that is not the reality of what actually happened. MCAS was a major link in the chain, and Boeing has admitted this, but not the only link.

As I said elsewhere, compare it with playing chess against your app on your mobile. Say that pilots normally handle level 4 and under abnormal circumstances level 8, and are trained for that. With MCAS combined with AOA failure, Boeing created a situation that fielded chess ace Gary Kasparov against Max pilots. Not in a game where you have 2 hours for 40 moves, but speed chess where you may have a few minutes to win the game. Of course this is a situation where >90% of the pilots would loose, even if with hindsight a winning strategy could be reconstructed. Calhoun seems to continue the ‘inexperienced pilot’ mantra. Bah.

aTflyer, if you study the flight data, it came down to whether pilots recognized that extreme stabilizer movement was causing the nose-down movements.

In cases where they did, they corrected for it successfully with trim controls. If they didn’t, they relied on the control column, which ultimately could not overcome a full stabilizer deflection.

Boeing assumed that the pilot response to mis-trim would be instinctive and from memory, as it must be and is trained for, given the speed at which loss of control can occur. But that has since been proven not always valid, pilots sometimes did not react in the time expected, or did other things instead.

So further training on that is needed. We should see that reinforced in the newly required MAX training.

In JT610, the captain twice requested the memory items from the first officer, but he could not recite them and opened the manual instead, then struggled to find the correct sections. That is an indication of training and experience issues.

Michael,

It’s all about culpability. Will Boeing get away with it? No. If they keep following this line there will be what is referred to as natural justice. The world won’t consider Boeing to be a company that they can do business with. The stench, the smell of inproprietary will remain with Boeing. The world will take it’s business elsewhere.

It’s, in effect, what happened to McDonell Douglas. It will take a decade. But it will happen. As they say, death by a thousand cuts.

In the 4Q2019 Boeing lost $9.2b, surely the 3Q2019 loss was too low (jedi mind tricking). Now we are officially at a loss of $18.4b with no end in sight, at least for me.

I have no idea how Dickson can talk about RTS when flight tests didn’t happen yet. After all these wrong Boeing announcements, why should something change now. Calhoun seems to be part of the problem.

The 4000 MAX aircraft grounded and in the pipe line prevent Calhoun being honest and decisive. It’s his 100 lbs backpack & he oversaw the packing.

What if a blue chip customer cancels their 737MAX order outright. Their is probably a quick reaction force of lawyers and sales people out there to prevent it.