Leeham News and Analysis

There's more to real news than a news release.

Embraer 1Q2022 results; lower deliveries as Commercial aircraft division is re-integrated

By Bjorn Fehrm

April 5, 2021, ©. Leeham News: Embraer presented its 1Q2022 results today. The airframer had lower deliveries for Commercial aircraft and Business jets than in the 1st quarter of last year after shutting down production in January to reintegrate the Commercial aircraft division.

Despite a lower revenue for the quarter, the EBITs were similar, and free cash flow usage was down as Embraer has trimmed its cost base. Sales were positive, and the backlog has grown to $17.3bn from $15.9bn 1Q2021. Profits before tax were -$32m compared with a -$90m a year ago. The company confirmed the 2022 guidance.

Group results

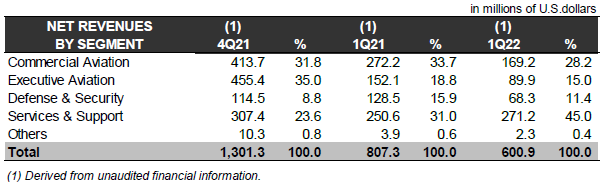

Group revenue for the quarter was down 26% at $601m versus $807m in 1Q2021. Earnings before interest and tax (EBIT) freed of one-time charges was -$27m (-$30m). Free cash flow was -$68m compared with -$227m 1Q2021.

The revenue for the different segments is per Figure 1.

Figure 1. Embraer’s segment revenue. Source: Embraer.

The company paid off $0.4bn in debt in the quarter, with total debt at $3.6bn and cash at $2.1bn.

The company confirmed its guidance for 2022, Figure 2.

Figure 2. Embraers guidance for 2022. Source: Embraer.

Commercial aircraft

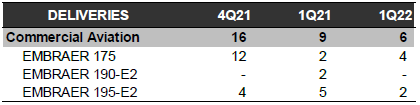

The Commercial Aircraft division delivered six E-Jets during 1Q2022 compared with nine for 1Q2021, Figure 3.

Figure 3. Commercial aircraft deliveries. Source: Embraer.

Commercial aircraft revenue was $169m versus $272m for 1Q2021 due to the January shut down of production.

Business Aircraft

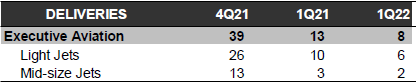

Business jet deliveries were affected by the reintegration of Commercial aircraft. Eight jets were delivered in the quarter compared with 13 a year ago, Figure 3.

Figure 3. Business jet deliveries. Source: Embraer.

Segment revenue was down 41% at $90m versus $152m 1Q2021.

Defense & Security

Segment revenue decreased 47% to $68m vs. $129m for 1Q2021. The decline was mainly as there were no deliveries of KC-390 during the quarter.

Services and Support

Services revenue was the bright spot during the quarter as airlines fly their aircraft more. Revenue increased by 8% to $271m vs. $251m 1Q2021 and gross margin grew from 24.6% to 26.5%.

These figures aren’t very rosy: Figure 1, in particular, paints a picture of “just hanging on” rather than thriving.

It would be nice if Embraer could enter into some sort of JV in order to improve its fortunes. There was a time when a JV with COMAC/Irkut was being “sniffed out” (see link). Irkut is now probably out of the equation as a result of the Ukraine crisis, but COMAC might still be an option. Such a JV would have benefits both ways.

https://www.airdatanews.com/comac-and-irkut-may-establish-partnership-with-embraer/

These figures are either not credible or an absolute miracle when you consider what they have gone through.

You may concratulate Boeing. They did Embraer twice. First their stupid claim vs. Bombadier to drive the CS into Airbus arms.

Then they realized instead of finishing off a darbing CS, they have created a monster for their loosing Max 7.

To fix it, they tried to buy Embraer, with their subpar E2. When they stumbeld over their Max.

So not only did Boeing force the CS into Airbus, they also harmed their biggest competitor and shot themselfs in their gut with their Max.

The numbers are not that bad for Embraer, but what is their perspective long term, with the A220 at Airbus?

How many E2 jets can they sell against market, service and production power of Airbus?

Overall, one may congratulate Boeing – sucessfully defended the duopol.