Leeham News and Analysis

There's more to real news than a news release.

Risk Adjusted Business: Aircraft and leasing values

By William Loh, International Aviation Advisors and

Dr. David Yu, CFA, Senior ISTAT Appraiser, AAVA Group, NYU Shanghai and Stern

Special to Leeham News

Oct. 3, 2023, © Leeham News: Investing in aircraft has become increasingly popular over many decades now, and for good reason. The returns can be most attractive and well-chosen assets tend to hold their value well over the medium term. Some of them have the option to extend the useful life out to 40 years or more in a freighter conversion.

As with most investments though, owning aircraft involves risk and requires subject matter expertise to avoid surprises and pitfalls. Some of this will involve aircraft selection, understanding industry dynamics, and incorporating these into the modeling of future values/lease rates and equity returns, which have been a focus of ours for several years.

Rather than the traditional method of producing bi-annual static forecasts of future values, our approach has been to develop a simulation model of possible future outcomes. This results in a market-driven probability distribution of the future asset value, rather than a single point forecast (rarely achieved in practice). Most traditional forecasts are discrete points including the classic high/low/base versions. Our forecasts are updated whenever it is appropriate based on market changes.

Future value forecasting

Even before Avolon’s “Values and Valuers” White Paper of 2016, it had become clear to us that there was a need for a robust analytical methodology. We have also found that there is often a requirement for an investment return and pricing model that can assist existing and potential new investors in estimating the critical assumptions in their analysis of existing portfolios, and for evaluating new purchases. These techniques have been widely incorporated in other financial asset classes and industries.

Given the unprecedented disruption to the aviation sector following the effects of the pandemic and lock-downs (and the current engine/airframe troubles), many of those who have invested in aircraft over the last decade are faced with new uncertainty in terms of lease rates, values and even future market demand for aircraft. This may indicate the need for a review of their internal models. No one has a crystal ball that provides absolute clarity, but investors will want to model a variety of scenarios, especially for twin-aisle/widebody aircraft which historically have had higher volatility.

All investors have an interest in properly analyzing the impact that future uncertainty may have on their returns, the timing of selling existing aircraft exposure, or the price at which it will make sense for new investors to buy or build an aircraft portfolio.

Market simulations and cash flow analysis

Models such as ours combine the market simulation approach to future aircraft valuations with a powerful analysis of future cash-flows to provide decision-makers with a pricing and return model under different scenarios. Many parameters must be adjusted based on the end user’s needs, and then input into the Lessor Trading Model which helps investors understand the potential returns available, as well as things which are best avoided. Our Lender Repo Model allows lenders to understand the benefits available to them by choosing to lease an aircraft instead of pursuing a possibly distressed sale.

Leasing’s two largest expenses are depreciation and finance costs. There are many parameters to be analyzed, such as the various debt and equity market conditions, debt/equity split, asset depreciation policy, and lease rate factors, among others.

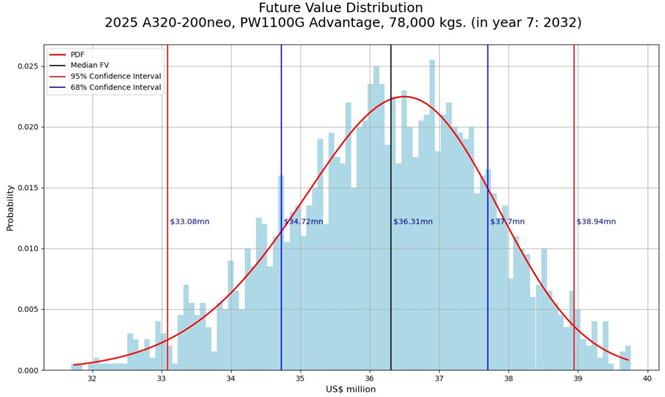

This is part of an example return output for an A320-200neo from the Lessor Trading Model, with book value sales included:

Based on this kind of analysis, investors can be more confident in their decisions, and that they’ve made the necessary investment in time and effort to get their numbers right.

We’ll go into more detail about the models in our next Risk Adjusted Business article.

Values can swing alot depending on replaced engines, APU, Nacelles, landing gears or avionic boxes of different age and SB standard. Now the A320neo with PW1100G engines will see lots of engine changes.

Claes:

It appears P&W is getting their house in order and the engine change issues will be on a descending trajectory.

You can use historical data as a general idea and contrast with what is going on.

Yes, they usually do: PW2000, PW4000-94, GP7000, F100, F119

Some never really get fully fixed TF-30, PW6000, JT9D, PW4077 …

Some are being fixed F135, PW1100G

While this is very distant aircraft value news it is interesting that Raythoen (RTX aka P&W Division) is selected to be involved in the TBW

https://www.aviationtoday.com/2023/10/03/boeing-taps-rtx-for-x-66a-nasa-collaboration/

That does not mean GE is out of it engine wise, but they would be one of two choices.

All that P&W stuff on the TBW could be a heck of a win for UTX / Raytheon if the plane becomes a Go.

Is the TBW more efficient because the wing is so thin and light weight?

Reduced structure weight is one aspect. Another one is ‘thinner’ and reduced sweep means more natural laminar flow.

The wing is what the X-66 is about not the engine

While the focus is the wing, the engine is equally important as half the improvement will probably (assume development not current) come from the engine.

Its no small matter with P&W being the engine on this aircraft, it could be the sole engine (assuming TTBW ever comes to fruition) or its going to be a choice of two engines.

It definitively puts the GTF into contention.

Interesting… So the fuel tanks must be moved inboard.

I think Boeing sees the GTF technology has the most potential for higher BPR’s and further enhancements for the core engine. Though I expect they will start with one of the existing engines on the X-66, probably a PW1500, 73 inch variant to reduce risk. This isn’t primarily about the engine.

They need to develop the wing, its systems and boxes like anti-flutter system and wingtip folding. Once in flight test FAA/EASA needs to be involved to decide how the systems introduced can be certified. So you might get 9-12% improvement in the end flying the same routes at the same speed. Engines can give more, hopefully close to 20% but it is major work if it also should have 15 000 cycles on-wing time between removals “out of the box”.

All NASA studies I saw a couple years back were based on GTF.

P&W has a lot of upside the LEAP does not as they can push the core a lot harder with the right materials. They have a PIP in progress that focuses on reliability rather than efficiency.

Clearly parts of this are an issue during the design and or mfg.

But reality is, the only time will tell is time on wing and find the weak spots and correct. While not as bad LEAP has its issues as well.

I think it is a lot about the engine, though the real discovery is does TTBW work. You don’t need a new engine for that and even a upgraded one will work though it may not back insert into the original (which is a huge aspect for the existing various GTF model on wing now)

Collins was likely to have a lot of that work but the P&W end was not a given with Boeing working with GE so closely. I suspect its also a prod to GE to get into the GTF and not the RISE that they are dangling in front of people.

Lufthansa, United will love this.

https://airinsight.com/sas-future-lies-with-consortium-that-includes-air-france-klm/

From the link: “..and SEK 7.5 Billion in Structural Cost Reductions.”

Not sure I like the sound of that. Who exactly will suffer, and who will benefit from those cost reductions?

SAS was a consortia and each country had its HQ, i.e. more staff than talent. With a limited market with mainly business travel at rush hours it was hard to get good yields and load factors for 12-14hrs/day. We will see what happens to SAS brand new 60 aircraft A320neo fleet with LEAP-1A’s that AF might feel better belong in their operation.

‘Boeing said to set goal of record 737 output by mid-2025’

“Boeing (NYSE:BA) plans to increase output of its 737 narrowbody jetliner to a record of at least 57 a month by July 2025, Reuters reported Tuesday, citing two people familiar with the matter..”

https://seekingalpha.com/news/4017449-boeing-said-to-set-goal-of-record-737-output-by-mid-2025

Calhoun said BA would clear its 737 MAX inventory in two years back in around 2020 IIRC. 😁

Found it:

Dec 3 2020

Bloomberg

“The forecast for depleting that inventory is roughly a two-year time frame,” Calhoun said. “We are confident that can be done.”

Don’t forget “forty 737MAXes per month by mid-2023!”

Did that happen? What might be inferred?

Oh, Boing has said *lots of things*, Pedro, as we both know.

“57 MAXes per month by Mid-2025!” sounds a bit like Wimpy’s “I would gladly pay you Tuesday for a hamburger today!”

We will- as usual- see how Boing’s rhetoric and reality match up, over a bit of time. 😉

BTW it looks like contract with UA is made in September. Desperate to sell aircraft cheaply to create/fake FCF (deposits from UA). Winning strategy!