Leeham News and Analysis

There's more to real news than a news release.

Boeing to cut 787 production rate, cites global trade environment

Oct. 23, 2019, © Leeham News: Boeing will cut the 787 production rate from 14 to 12 for two years beginning next year, the company said this morning.![]()

“Given the current global trade environment, 787 production rate will be reduced to 12 airplanes per month for approximately two years beginning in late 2020,” it said, an apparent reference to the Trump Administration trade wars.

Boeing raised the 787 production rate in part in anticipation of orders from China. Donald Trump’s trade war with China has frozen orders by the giant country since 2017.

Boeing CEO Dennis Muilenburg previously said slow 787 orders were tied to China’s lack of them.

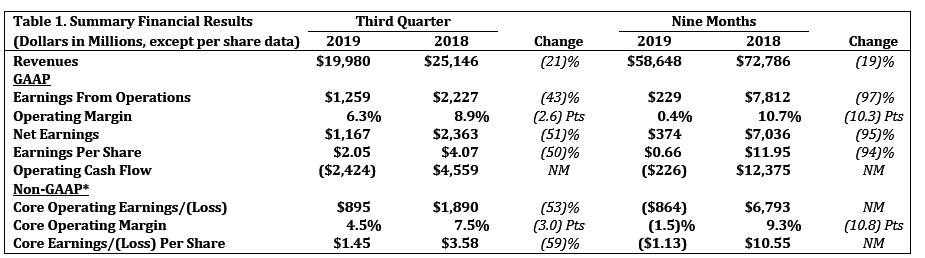

Earnings release

Boeing made the announcement in its third quarter earnings release.

The company, as expected, announced a loss for Commercial Airplanes and negative cash flow due to the 737 MAX grounding, which halted deliveries March 13.

No additional charges were announced, as many had expected.

The Boeing earnings call begins at 10:30am Eastern time. Signing into the webcast is here.

They cut 787 production instead of 737 MAX – funny guys.

Next year . Its a response to order slowdown.

All the 737 production for the next few years have been sold

Still, for the Max disaster, Boeing looks quite unharmed.

Making not losing money with a single family (B787) carrying the whole civil aviation.

Actually, those numbers are still awesome for the situation Boeing is in.

You would have expected cash flow and turnover issues, maybe even a huge loss due to the main product being out.

Financials are still looking good, not to say great.

Seems like military and B787 can carry the whole company alone, with reasonable earnings.

B777x will come in 2021, no statement about the production gap, should be a bit larger now , did they get orders to close?

This earnings table really depends on predictions about the future of the MAX. A company can in fact show a nice profit just by producing and stocking product, as long as those are booked in above production cost. To me it looks like Boeing is booking the produced MAXs at production cost, which is neutral to earnings.

The entire pictures changes dramatically if you factor in substantial rework of the product before devliery, or much more dramatically, if you can not sell it at all (no re-certification) or only to some of your customers (only FAA re-certifies). All over sudden this earning sheet would look really ugly.

IPIS stands for “internal profits in stock” is not PERMITTED in any accounting procedure

At least Boeing is following this procedure wich is not under FAA control … :=))

Think “deferred cost” .. (Basket)..

Thus not immediately visible.

I thought Trade Wars were “Easy to Win!!!”

Oh no. not here too

I can only refer to Rex Tillersons remark that said it all.

Chinese carriers are the biggest A330 operators but have not placed any orders for A330 NEO’s yet. There is a new A330 completion center in Tianjin..

https://www.bloomberg.com/news/articles/2019-10-12/trump-says-u-s-china-deal-may-spur-20-billion-in-boeing-sales

China has money, centralized leverage and choice, a good negotiation position.

Airbus needs some big order/s from China for the 330NEO’s as Chinese carriers are as you said big 330 operators. AB could wave the facility at Tianjin as carrot for A330 sales.

Lets see what the deal is about but I think China could do with 779’s from Boeing?

Then there is the C929 in the making which in the long term is not good news for the 330N’s and 787’s.

With all numbers, if they are to good to be truth, they probably are.

Big chuncks be be moved around, valued, deferred, not included, pulled forward.. there’s flexibility.

If everybody wants to see an certain outcome, it can be taken care of, so everybody is happy. Or at least feels better than expected.

I tend to agree with you, given the likelihood that the CFO/CEO cabal will be put out to pasture in years near future what’s the betting that the books have been well and truly dressed in a window

Latest excuse “trade wars”. Before that, “currency headwinds”. Anything but a look in the mirror.

Status summary:

– 737MAX: Still grounded, Boeing still fudging about re-introduction date, still not clear what fixes are required/involved…not even clear if the wreck can ever be fixed.

– 777X: Engine problems, and door blowout during static test. Boeing fudging about first flight / introduction date. Relatively few orders, predominantly from the ME3, who are all somewhat shaky. Airbus coming with a 319t A350-1000.

– NMA: Seems to be dead, but not yet buried. Instead a vague plan to re-engine the B767. Meanwhile, the re-engined A330 is already on the market, with a lead time of years.

– 787: Complaints about shoddy workmanship in Charleston, and now a production rate cut in the pipeline.

Anyone interested in buying Boeing stock? 😉

@Peter…

B737 MAX-Yes, still grounded however IMHO they are moving closer to solving it and it will be a huge cash flow in 2020 once they start delivering planes

B77X: Engine problems – We don’t know how major and ostensibly it seems a couple of engines were already shipped to Boeing. Also, engine problems are GE’s fault, not Boeing’s.

B77X: “Door blowout during static test” is rather a useless comment as it was close to 149% of max failure anyway. In fact, like the Airbus A380 wing test, I wouldn’t be surprised if Boeing simply needs to adjust their finite elemental analysis or make some very minor adjustments to get it sorted out. Its certainly not a major problem.

The B77X has more order than the A350-1000 (who would’ve thought?). The ME3 are now primarily the ME2 and they certainly want their B77X -maybe no the B778X but certainly the B779X.

NMA- The A330NEO isn’t selling like hotcakes either and is being pressurized by the B787 (such as the Hawaiian order). The B767NEO is talk-we don’t know what the internal discussions are.

B787-Shoddy workmanship is irrelevant (if its even a factor)-it hasn’t had canceled sales because of that. Going from 14 down to 12 is not the biggest deal in the world.

Judging from your comments, it seems like Boeing is a finished company. LOL.

Apropos, you should’ve added that Boeing doesn’t have anything to counter the A220(larger versions) nor A321NEO…. 🙂

I wasn’t trying to do a Boeing vs. Airbus comparison. However, in reply to your various points:

– We disagree as regards the MAX.

– Regardless of what’s causing the delay, the fact is that the 777X will be delayed. The A350-1000 is flying, and available now.

– Orders can be cancelled…just look at the huge A350 order that Emirates cancelled a few years ago. Similarly, 777X orders can be cancelled — particularly if the ME2 feel that they’re being led along by Boeing.

– The A330 NEO isn’t selling very well, but it’s flying, and it’s available now. A re-engined 767 won’t be available for another 5 years. For airlines wanting to replace aging 767s, will it really be worth such a wait?

– When Al Baker complains about shoddy workmanship, and he happens to have a large 777X order — for which the 319t A350 now forms a possible alternative — then shoddy workmanship certainly does matter. The military tanker program also suffers from shoddy workmanship. Perhaps Al Baker fears that the 777X will as well.

I’m not suggesting that Boeing is finished, but I am suggesting that it’s in a very nasty position…and management seems to be doing nothing substantial about it…

The A330neo isn’t selling well?

Well, since 2014 Airbus sold more A330 neo and ceo than Boeing 787.

The LN comments section’s fascination with the 777X cargo door failure during ultimate load teeing is itself a fascinating subject of study. The A380 wing broke at 1.46 instead of 1.501 and that was handled by analysis and minor redesign, but fixing a cargo door test failure on the 777X puts the program in jeopardy? Forgive me if I don’t quite follow the analysis.

Also, under US antitrust regulations Boeing is forbidden from owning an engine manufacturer, so while the GE engine delay is no doubt frustrating to Boeing there isn’t much they can do about it.

I don’t think anybody is suggesting that the cargo door problem can’t be fixed. But it represents another delay to a program that can’t really afford to be delayed. If the ME2 (substantially) defect from the 777X, the program will be in serious trouble.

Similar comments apply to the GE9X engine: regardless of whose fault the engine problem is, it’s putting the 777X program in potential danger.

The ME2 — and others — may consider the A350-1000to be an acceptable alternative to the 777X. The fact that the A350-1000 has 40 fewer seats (10%) than a 777-9 is only relevant if you have a 100% load factor…which, in essence, nobody except Ryanair has. For a 70-80% load factor, an A350-1000 can sit comfortably in a 777-9’s shoes.

Once again, I’m not trying to be pro-Airbus: I’m merely pointing out that Boeing has some nasty clouds hanging over its head.

“The fact that the A350-1000 has 40 fewer seats (10%) than a 777-9 is only relevant if you have a 100% load factor…”

Yup. Now that the A380 program is done, and the 748 passenger version is effectively done (really, it never got started), the 779 takes over the mantle of “It’s a good aircraft, if you can fill all those seats…”

Indeed. In a slide presentation a few years ago, Boeing classified the 777X as a VLA (Very Large Aircraft), and grouped it together with the A380 and 747-8. It seems that airlines are happy with planes of the size of a 787/A350 — and, even within those families, the larger variants aren’t selling all that well.

Foolish move to tramp up to 14 in the first place.

Clearly even mid term it was not sustainable.

You can only read that as another short term add gasoline to the stock price vs, oh, now the Forrest is burning down, how did that happen.?

Not foolish . Its called planning. What was unexpected was the trade war which meant expected orders didnt eventuate.

I believe the ramp to 14 was almost exclusively to attempt to kill the A330neo. It had the effect of making the unit costs fall and freed up early slots. The simple fact is that the TA market is near moribund at present making that decision look a bit aggressive. The ramp down to 12 is a concern as to where it may lead, no more. I would be more concerned about the B777/x as the market appears to be finite and shrinking, sooner or later the A350 (in new variant form) will potentially kill it dead

Going to 14 was neccessary to prop the “787 pricing power” story.

Scale gains do not carry the poison that heavily leaning on suppliers does . Blowback for that: quality–!

I haven’t seen where the 787 production cut is coming from. Will it be equally shared by Everett and Charleston down to 6/month each? Production costs at Charleston are almost certainly lower, and it is the only site that can build the -10. I wondered when they boosted the rate to 14/month whether that was done to increase the Charleston rate before future cuts.

Charleston has been having trouble meeting is production goals as they stand now with lots of rework/make-up work on the ramp and not on-time or on-the-line. That kind of production is not efficient and probably makes Charleston planes more expensive currently.

I would image that Charleston would change over to building the -10 only and Everett would continue building primarily the -9 and the split to not be even: 7 Everett, 5 Charleston; maybe even 8 Everett (as they have shown themselves capable at doing that) and 4 Charleston (as they fix their production issues permanently and learn how to make the -10).

Stan Deal is a natural salesman. He can provide coaching and direction to the current sales effort which is floundering. Sales appears to be dropping the ball with customer complaints about poor communications surrounding the MAX and missed quotas on the 787 leading to the planned reduction in production rates.