Leeham News and Analysis

There's more to real news than a news release.

Boeing to cut rates on 787, 777 production; posts big 1Q loss

By Scott Hamilton

David Calhoun, CEO of Boeing.

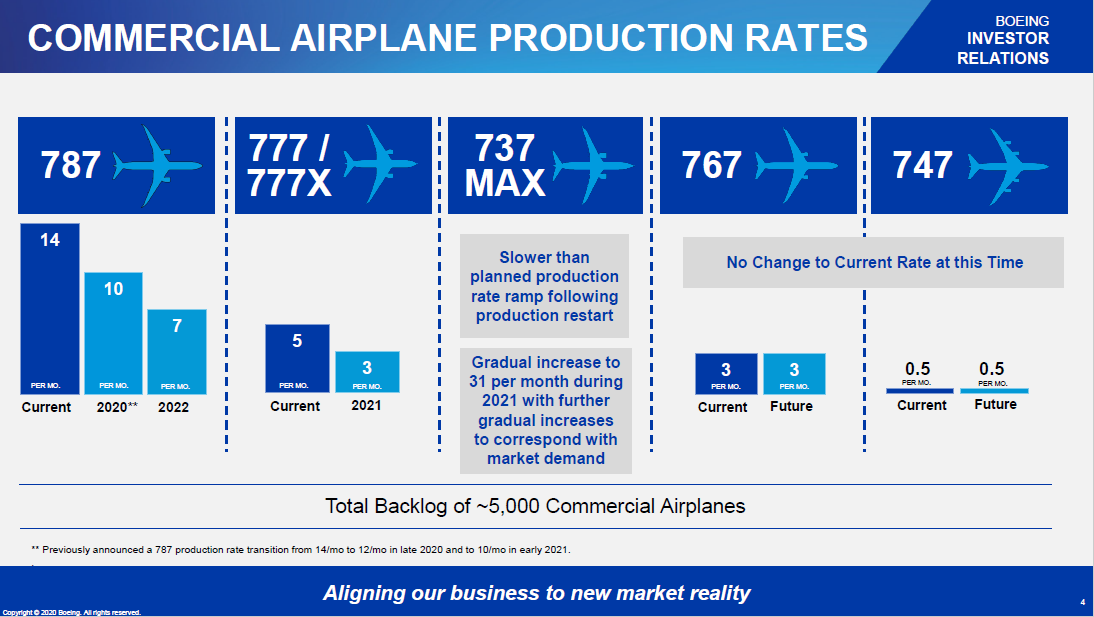

April 29, 2020 © Leeham News: Boeing will cut production rate of the 787 in half and the 777 from 5/mo to 3/mo in response to the dramatic drop in demand from the COVID crisis.

Production of the 737 MAX resumes at a low initial rate with a current target of 31/mo next year.

Boeing announced these rates in its first quarter financial results. The company has an operating loss of $1.35bn and a net loss of $641m on revenues of $16bn.

New production rates

The 787 rate was already on its way down before the crisis, from 14 to 12 late this year to 10 a month next year. Now, the rate will drop to 7/mo by 2022.

The combined rate of the 777 Classic and 777X will drop to 3/mo next year. The rate of 5/mo includes production of the 777X, which is delayed a year but in production. More than 10 777-9s have been produced. This rate is going from 2/mo to 1/mo, LNA learned. The delivery rate of the Classics had been at 3.5/mo. Production of the 747 and 767, already at low rates, are unchanged.

In a separate message to employees, CEO David Calhoun said gradual increases in the 737 rate will “correspond” to market demand from 2021. The production rate of the 787 will be reevaluated after the reduction to 7/mo.

Calhoun predicted Monday that it will be 2-3 years before passenger traffic returns to 2019 levels, pre-COVID.

Passenger traffic has “fallen of the cliff,” Calhoun said in the employee message. This also negatively affects business at Boeing Global Services, although year-over-year revenues were about the same in the first quarter and profits were up slightly.

Cutting employment

Boeing will reduce employment across the company by 10%, intending to do so through voluntary layoffs and attrition. Boeing Commercial Airplanes will take the hardest hit, cutting employment by 15%.

In an appearance on CNBC’s Squawk Box today, Calhoun said, “The industry is not interested in taking delivery of airplanes at the moment. The world market has been stunned. We remain confident it will come back.”

Calhoun said that given global government support for airlines, he believes the “thaw” is beginning, while acknowledging that traffic has fallen off the cliff.

Calhoun sees production rate returning to higher levels within a few years after the return of passenger traffic.

Challenges remain

Boeing faces continued challenges. The Wall Street Journal reported the Department of Justice probe of the MAX development is ramping up.

Calhoun said Monday that Boeing needs to borrow more money within the next six months. Reuters reported this morning that Boeing is working on a bond issue of $10bn or more. On CNBC, Calhoun did not rule out tapping federal funding. Reuters reported this could be up to $17bn.

Getting the MAX recertification slipped from June-July to what appears to be August-September. The latest delay appears tied more to COVID delays than to issues that emerged over-and-above the MCAS problem that grounded the airplanes March 13, 2019.

Boeing moved from a supply issue toa demand issue, Calhoun said, as a result of COVID. Boeing and its customers are working on rescheduling deliveries.

Hi Scott,

I understood David Calhoun mentioned 3-5 years before traffic returns to 2019 level. Am I wrong?

Cheers,

Jean-Luc

2-3 for traffic, 3-5 for production

Scott, I see you are predicting 4-8 years for traffic. Are you aware what the differences are between your forecast and Boeing’s 2-3 years and, if you are, in general what are they (I assume the specifics will be for your subscriptions only)? Is it a difference in belief whether growth will be limited by customer demand (my guess shorter) vs limited by supply (my guess longer, down to airlines being cautious with capacity and needing to rebuild finances)?

Rather than borrow, they could sell all those shares they bought back.

7-8 a month on the 787 is a realistic long term number.

When this recovers in single aisles Airbus will beat Boeing to a pulp. They have easy ramp up to larger numbers and two offerings with an easy stretchy to make the A220 a MAX-8 killer. A321 will beat MAX to death at the top with the -9 and -10 fighting for a bit in between.

SouthWest is making major deferrals though it looks like they will continue to slowly turn the fleet over to newer.

Good news in a way for the engine mfgs, they can get caught up on the fixes and production, though I don’t see RR doing anything but continue to fall off on 787.

Bad news is no new aircraft for some time.

A350-1000 and 777X will lag and I doubt never recover, the A350-900/787 will dominate the wide body sector.

Seems like a sound plan. I just wonder how airlines find he money to take delivery of any of these aircraft.

yes

just wondering too. Airbus cuts rate to 6 from 9-10/mo. for the A350 and BCA barely touches the 787? The folks at BCA get paid by $, even if aggressively discounted, and not by units delivered. Looking at the 2020 positions. Some lessors including Boeing Capital.

Guess lots of arrangements for payment via the capital market or other institutions, but I am a bit lost there. 2 years ahead of resumption of international flights, as W/Bs are rarely used for regional flights like in Japan. Enlight me!

Airbus cut rates to 6 for the A350. Boeing almost nothing.

Just compare apples with apples: A350 family doesn’t compete with B787 but B777; B787 faces A330Neo.

For both A/C size, Airbus and Boeing production rates follow the same reduction scheme, with slight differences due to backlog.

The 787-10 certainly competes with A350, although not on maximum range – which is hardly needed by most airlines.

Of course, you buy WBs that fit, and these days you either buy A339, B789 or A359. That’s what almost all the major carriers buy,

so if you buy one, you don’t buy the other, usually.

See AA, huge fleet of B787, nothing else.

American has more 777s- over 60 , while its 787s are in the mid 40s ( a lot are stored right now, including all 767s)

Thanks Alban but my angle is not that one. It’s about big cars in general. Thought that W/Bs have no sex appeal effective now and for the foreseeable future. It will be easier to get a new delivery slot for those in the mid-term. The next adjustment will tell.

Pleasing Wall Street + the CFO + customers ($) as well…

Hope springs eternal.

Sad day for Boeing employees and supply chain. And it’s still on the optimistic side as always. The robustness of the “~5000 aircraft” backlog (~85% MAX) , program accounting, free cash flow, portfolio were lowish. A cash drained company hitting the wall. Stake- and shareholders should have woken up out of their non-GAAP EPS rush way before Covid-19.

In complement to Keesje numerous issues:

– cost of Charleston plant closure (totally useless now)

– cost of supply chain support

– refunding of cancelled orders deposits

-very weak bargaining position for future sales means low profits on future sales.

and, the most important issue, the future:

– Strategy to fight A 200 A321 1ND 322, and COMAC C919(nobody mentions this terrible competitor any more, but it will come eventually, and limit the potential of the very large SA chinese market, chinese certification for MAX will be a quid pro quo of C919 FAA approval) ,

talents for developping a 737 replacement,

– money to finance this development.

too many challenges for a management whose legitimacy and competence are doubtful!

Charleston will not close for a number of reasons, in fact Everett will loose the 787 line.

Charleston is where the tail section is built and assembled to the center fuselage section (separate from the assembly of the 787)

As setup, Charleston only can assemble a -10 as it won’t fit in the Dreamlifter.

C919 does not threaten Boeing or Airbus. Only internal China will take it (forced) and only on non competitive routes. It failed to follow certification’s requirements and has no patch to do so.

Iran might take some for internal use.

tahnk you Transworld

Please elaborate on “C919 has no patch to follow certification’s requirements”

I can not think of any non compliant design feature that can never ever be modified

the chinese will certainly do whatever it takes to have the C919 FAA certified.

even if that means a C 919 NG

Its not design features so much – the plane is an almost copy of the A320- but the design process and procedures were supposed to involve the FAA as they went . For some reasons the FAA pulled out/was prevented from accessing documents? and the certification process was left in limbo.

https://www.ainonline.com/aviation-news/air-transport/2018-10-17/comac-c919-stumbles-faa-flight-deck-standards

You cant refund a cancelled order deposit…. maybe for some of the longest delayed 737 max , but not for all the other orders.

It seems that even cancelling and losing the deposit opens up airlines to paying Boeing ( or Airbus) some of the discount given for larger orders.

Thats the whole reason airlines get discounts of the nominal price,the quantity of the order , you pay deposits in steps closer to delivery , you have to take the order no matter what

An airline if really wanted can get back all deposits for 737 MAX and cancel all orders. Boeing position about 737MAX is so precarious that they don’t really arguments to won in a court. Some already went this path, others still waiting because Boeing is a bully and vengeance Boeing and 1 of 2 in the world.

If and when Boeing negotiates a LOAN with the Fed, the latter should use their shares as backup guarantee of the loan with the share price pegged the day the loan is finalized. Once loan is repaid, the Fed, having used Taxpayers Funds to Save Boeing should be compensated with the Gain on those shares when they are returned to Boeing. Fair deal for Boeing who needs the Cash, and Fair to the Taxpayers who made their Funds available in this Drama. It should be noted, that most of Boeing Cash loopholed have been caused by their multiple self-inflicted criminal actions and recently with the Covid-19 scenario.

How much money has Boeing scooped up in prepayments for the MAX order book. ( ~~4700 orders outstanding.)

What did they do with the money? 🙂

They have to pay it back in case the order is canceled due to too late delivery.

Not the answer. Theory. 🙂

i.e. the proper question here is can they if cancellations exceed the planning horizon. bought back shares, even assuming they are redistributable no longer have the value they used to have.

The giant is thunderstruck surrounded by multiple opponents in a dingy corner of the ring..Will be very tough and long for Boeing to get out of this intact and scratchless..

You’ve mixed up sides, didn’t you?

The dingy corner _is_ Boeing’s corner. 🙂

“.. Boeing to get out of this intact and scratchless..”

That will take endless buffing out the preexisting scratches and a massive refurbish/rebuild under the hood.

Of course..! with the addition of demand side issues now.

Notice in this take, both Everett and Charleston stay on line with the 787, but they are hedging the bets when it goes to rate 7 (which Charleston can do)

https://www.flightglobal.com/airframers/boeing-has-time-to-review-787-production-strategy-in-light-of-rate-cuts-ceo/138146.article

I believe Charleston also has room for a second line if they need to go higher.

Once Everett is off line they will not resume.

Charleston was built for 10 per month. The critical factor is the multiple ‘join tools’ to stitch together the barrel sections and Boeing has a lot of IP in this area

Charleston FAL is a U shape while Everett is the more efficient single direction line. The assembly time at Everett is quicker/better quality? and you might have the worst of worlds by creating a new second line at Charleston and phasing out Everett.

Yes, Bloomberg has reported that Boeing would favor the Everett line because the worker quality is higher and the financing of the facilities makes the 787 line important for Everett. Although they don’t wish o close either line and will not unless circumstances force it.

Sorry guys, I don’t buy it.

First it would take significant investment to get the -10 built in Everett. Right now it can’t be (you would have to repackage the fuselage assembly and engineering to go with it)

I don’t buy Charleston is less well setup. they may not have the level of skill Everett does.

The Charleston facility is also more economical as the fuselage sections all come from there or Italy (sans the nose and its a wash).

Jobs agreements are in place with South Carolina as well (which Washington State failed to implement)

A few other points tucked away in the pdf of the earnings call:

737 Pickle fork issue has cost $471M to date, no forecast on how much more its going to cost.

737 production cost increases = $6.3B = +$2M/aircraft, how are the margins looking now?

Anyone done the maths on 787 profitability? ie. will they ever recoup the $16.8B deferred production costs remaining?

but hey, Dave is not going to pull a wage this year so its all good!

The losses can be written down by offsetting tax expenses in more profitable years. Those for 787 have mostly already been written down over a period of several years. Some 737 losses have been as well, in 2019 and will probably continue for some time. They can be carried forward until profits resume.

I don’t believe it works that way with deferred accounting.

From memory Boeing still had 20 + billion overhand on the 787 program.

They have done write offs from time to time but not a whole program.

Pickle Fork may be a oh, hell, we will give you a MAX, its not like we don’t have a lot of them laying around.

All losses are ultimately either written down to reduce subsequent tax liability, or absorbed by subsequent profit, or absorbed as an R&D cost. Boeing has used all 3 methods, also taken charges on the 787 and 737 and will likely continue to do so as things remain tough,

Boeing will not survive Covid-19, as an auditor I know when there is a going concern issue.

Boeing will survive but the commercial side will be a smaller part of their business for some time to come. They will need to make major adjustments, as will Airbus. But they have stuffiest diversity that their existence will continue.

The whole point of the bailout exercise over the past few months has been to establish in investors’/creditors’ minds that the govt won’t allow Boeing to go out of business. Now that they’re enacting their survival plan without a bailout what on earth makes you think they won’t survive?

Actually its an interesting assessment and its not been thought though clearly by many.

Firstly Boeing consists of two major different sides, Military and Commercial Aircraft.

The military side is safe.

But BCA?

1. 747-8F is in die off mode. Fuel prices make the 747-400F viable so the economics favor a 400F or a 777 (of which there will be many older refitted for F feed stock)

2. 767: Living on the KC-46 and F versions. But again with 767s coming available like popcorn, the F portion is dead.

3. 777X: Whats its future. Very iffy right now. Lot of eggs in the ME3 basket. Big sunk cost and no viable return for 10 years if ever.

3. 787: Clearly viable, good bird now, but at what rate? Historically Rate 8 for a wide body is a high. So count on rate 8 for 8-10 years.

4. 737MAX: Dropping like a rock. Not gone, 450 to put in service and slow ramp up. Crippled for the rest of its production.

No future product in this area.

Airbus will be able to produce 100 single aisle in a month when the A220 is fully on line. They can compete on availability and price.

So its a fair question , how long can the BCA portion of Boeing limp along with no new product and bad management?

Huge structure producing few aircraft ?

BCA can be shut down and Boeing Military live on but then its sim,ply a defense company.

Bankrupt? Probably not, restructure, oh yea its very possible.

Bjorn’s Corner has recently talked about the hype cycle, but it works in a negative as well as positive sense. Just as positive hype is meant to attract support and resources, negative hype is intended to drive them away.

Fortunately the markets see it differently. Many here are actively rooting for the demise of Boeing, and have predicted it endlessly. But outside Leeham, most Americans are more interested in Boeing doing well, and the benefits that brings.

You are arguing for success/failure being based more on (anti)hype and not on actual performance

especially in the context of Boeing as a “well managed” company in the shareholder ecology.

Yes that is true. Boeing performance in the real world does not match its performance in the share holder space. We see the opposite for some other companies.

But reality sometimes has push through impact.

The MAX failure has sucked up all available hype and then some. 🙂

No, not arguing that at all. Like I said, hype works both ways, positive and negative. The truth is in between. The truth has the most value. But the purpose of hype is to drive the issue away from the truth.

Truthful observers will look at both positives and negatives and fairly evaluate. The hype observers will take continuous shots that are derogatory and emphasize only the negative, nd also amplify the negative to create a maximally damaging perception. They are obvious in that regard.

https://www.bloomberg.com/news/articles/2020-04-30/boeing-kicks-off-mega-bond-sale-to-shore-up-funding-in-crisis

Boeing seems to have raised $25b via bonds. ( alleged interest reaching $70b )

Lets see what happens.

Unbelievable they are producing 777X when it is not certified.

They did that with with the MAX too and how did that work out.

@Leon: Producing airplanes to meet delivery dates in advance of certification is SOP.

After the MAX self-certification scandal with exemptions and hidings, who would really think all regulations were met on the 777X?

I would expect regulators will check the 777X more in detail.

So how long will this certification process take? Especially now that regulators learnt from the MAX scandal and the global certification process will likely change.