Leeham News and Analysis

There's more to real news than a news release.

Airbus issues “conservative” post-COVID forecast

By Judson Rollins

Introduction

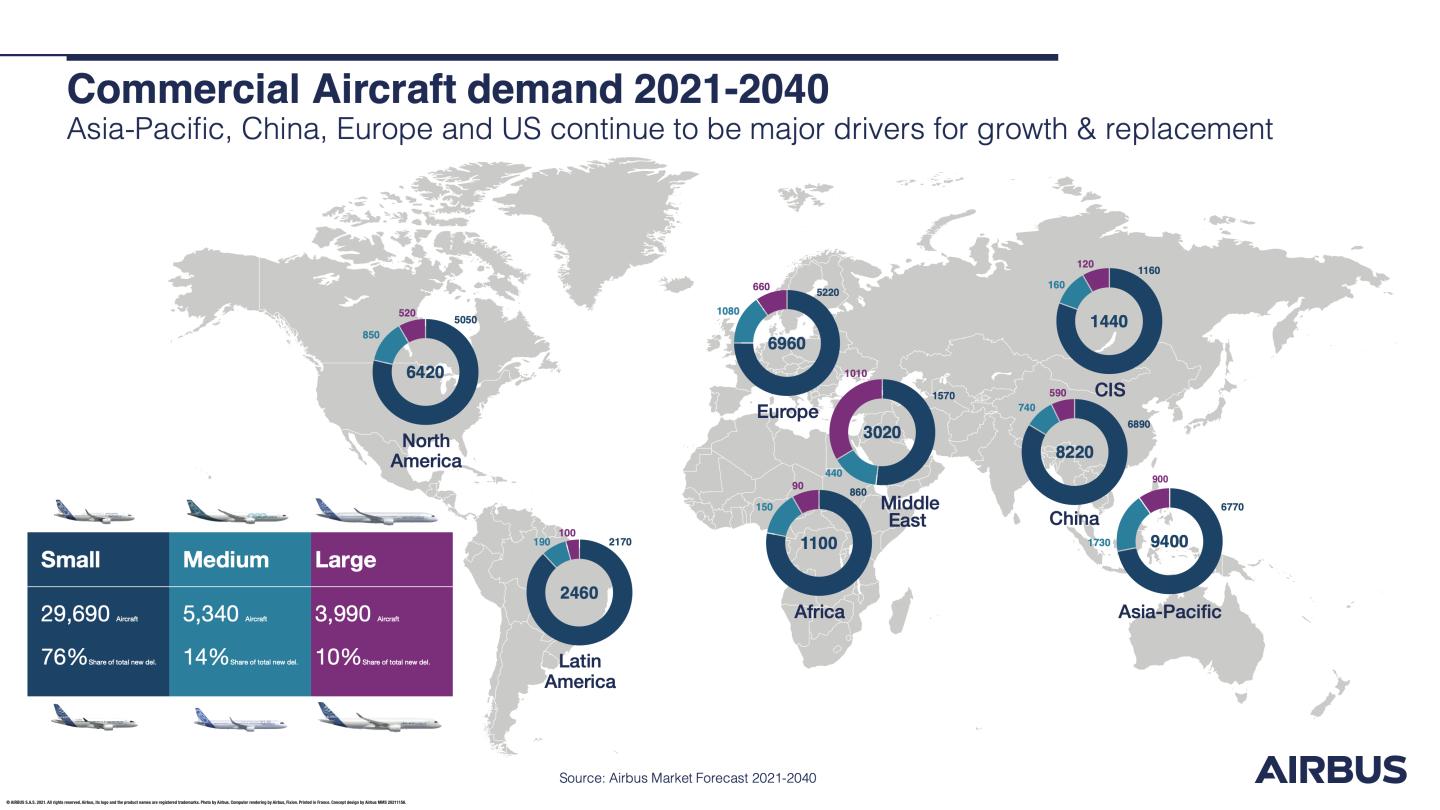

November 13, 2021, © Leeham News: On the eve of the Dubai Air Show, Airbus released the first edition of its annual Global Market Forecast (GMF) since the COVID-19 crisis began.

The manufacturer sees approximately 39,000 passenger aircraft with 100+ seats and freighters being produced by 2040. 29,690 will be small aircraft, 5,340 medium, and 3,990 large. Airbus’s category definitions now take both size and range into account; the A321XLR is categorized as a “medium” airplane, reflecting its inroads into routes currently operated by smaller widebodies.

Chief Commercial Officer Christian Scherer said that Airbus took a “corridor” approach to forecasting a global traffic recovery using high and low scenarios. In the low case, traffic would recover to 2019 levels by 2023, or 2025 in the high case. He said the high scenario is basically an extrapolation of recent traffic trends across key markets.

He expressed optimism that the wave of COVID-driven order cancellations had peaked. “The resilience of our industry has been remarkable. Owners continue to believe in their investments and put capital into their fleets.”

Global traffic expected to recover between 2023 and 2025

Airbus sees a two-year permanent lag in demand growth versus the pre-pandemic trendline but does see global traffic returning to 3.9% annual growth, down from 4.3% previously.

Scherer repeatedly emphasized the level of “conservatism” in the company’s forecast, pointing out that Boeing’s competing Current Market Outlook (CMO) assumes a larger replacement market. He expressed optimism for replacement trends, saying that average replacement age has decreased by 2-3 years in recent years.

Airbus raised its expectation for replacement aircraft to 40% of total production, up from 33% in its 2019 GMF. It attributes a large portion of its replacement forecast to a global push for increased sustainability and that 13% of airplanes currently service use previous-generation engine technology.

Scherer pushed back on assertions by a Boeing executive at a previous media briefing that Airbus is “flooding the market” with single-aisle aircraft beyond what market demand can absorb. “We’re not the ones controlling the marketplace. We’re in an industry that builds to order.”

Freighter market to be dominated by conversions

The European manufacturer sees demand for 2,440 freighters including conversions, of which 1,490 are expected to be replacements. 880 are expected to be new builds. Express freight is forecast to grow by 4.7% per year, while general cargo (comprising 75% of the market) will grow 2.7% annually.

Scherer said, “Yes, there is a bit of a frenzy around dedicated freighters, but the airplanes available today aren’t the most efficient available today. So, there will be a rapid erosion in the residual values in the [freighters] being delivered today.”

He declined to comment on any further native-build freighter products under consideration.

Services market expected to resume pre-COVID trend

Airbus’ pre-pandemic forecast of around $4.8 trillion of services over the next 20 years was maintained despite a COVID-related dip of 20% through year 2025 period. It still foresees a need for more than 550,000 new pilots and 710,000 technicians over the next 20 years.

Besides factors relating to the pandemic, I wonder if the Airbus projections also made allowances for factors relating to the increasing climate frenzy?

We already had “flight shaming”, but we now also have “no-fly pledges” (see link) — which are bound to be popular among the bandwagon crowd on social media. Add to that the various discussions of levies on air tickets, duty on aviation fuel, bans on short flights, etc., and it all starts to add up to potentially ominous news for the aviation sector. Switching to SAF won’t offer much solace, since it’s (currently) much more expensive than kerosene.

https://edition.cnn.com/travel/article/flight-free-travelers/index.html

Incidentally, the term “post-CoViD” is probably a misnomer, since many/most virologists think that the virus is here to stay. It will probably become more controllable, but still retain unpredictability — which is very damaging for the travel industry. The current, worsening situation in (parts of) the (highly-vaccinated) EU illustrates this point. This will probably (continue to) have a much greater effect on longhaul than on domestic/regional travel. Airbus seems to think differently, since the current projections are only slightly lower than the most recent projections pre-dating the pandemic.

@Bryce

CC – check

I was not brave enough to raise the point about covid being here to stay and being sure to bamboozle any return to ‘normal’

The bug has hardly gained a foothold yet in Africa, when it does very nasty variants indeed are guaranteed to fly around the world

Covid is widespread in Africa, like all other continents except Antarctica.

There’s a difference between “being widespread” and “getting a foothold”.

Africa has remained relatively unscathed by CoViD.

https://www.google.com/amp/s/www.bbc.com/news/world-africa-54418613.amp

Is there reason to believe it will “gain a foothold”? In that article, what sticks out to me is “Africa is home to the world’s youngest population with a median age of 19 years”.

It is very much there (following ivory-coast and nigeria myself closely). But seems people do not get that sick. Environment led genetic advantage?

@Bryce

One of the few certainties about this bug is that humans know little about it and that all attempts at control have been unsucessful

To make predictions about something one does not know nor understand is foolish –

One could make a parallel with Boeing’s predictions as to future aircart market

@DoU @Albert Gnadt @Ivory Coast

There is evidence to believe that the virus is very adaptable beyond the point and context of the initial crossover and has spread very far from with great success

The virus has evaded all attempts & predictions of eradication or control

Africa appears better equipped to resist, but is not immune to viral infections

There may well develope a variant which will spread to much more lethal effect than so far – to predict the contrary would be un reasonable

Evolution, Historic:

Gains in transmission

Decrease in lethality.

Dead hosts don’t propagate much. 😉

Increasing regulation will definitely have a big impact that is missed based on extrapolating from historical projections.

Flight Shaming is good up to only a point. There is no shortage of phony hypocrites out there who feel entitled to screw up the planet.

https://nypost.com/2021/08/05/john-kerrys-private-family-jet-took-16-trips-this-year-alone/

Tangentially related:

“China satisfied with Boeing 737 Max changes, seeks industry feedback”

“BEIJING (REUTERS) – China’s aviation regulator has told airlines it is satisfied that design changes Boeing proposed for its 737 Max plane could resolve safety problems, in a sign it is closer to lifting a more than two-year flight ban in Chinese skies.

The Civil Aviation Administration of China (CAAC) invited airlines to give feedback on a proposed airworthiness directive for the 737 Max by Nov 26, according to an undated notice seen by Reuters.

The directive outlines specific procedures for pilots to perform in case of problems similar to those that emerged in two deadly crashes before the plane’s grounding in March 2019.”

https://www.straitstimes.com/asia/east-asia/china-satisfied-with-boeing-737-max-changes-seeks-industry-feedback-document

And when the grounding is lifted Im sure more Max orders will follow soon after

Oh yes…just like the MAX orders are pouring in from other countries…😏

Not according to Calhoun

@DoU

You forget – China runs a tight ship – reg approval is bait for the gullible, and an indication to third parties that proper procedure is respected

In the current let’s bomb China wargaming chatchit- for China national airlines to buy the products of a US MIC mainstay is not inevitable – but the prospect is another switch

It does appear on the surface that CAAC may have ‘slow walked” MAX recertification?

Turn it around:

The US has more effective leverage on EU:EASA than on CN:CAAC.

(Imu Why easa accepted a half baked solution : interim path until -10 eis )

In an otherwise reasoanble and cautious report this phrase stood out for it Boeing like truth evasion

“The resilience of our industry has been remarkable. Owners continue to believe in their investments and put capital into their fleets.”

It would be more accurate to state that governments have, often in extremis, bailed out many airlines which have allowed them to, until now at least, survive

You raise some good points.

– Taken broadly, the industry is basically on the edge of insolvency — though, to be fair, this has been the case on previous occasions in many countries. The only parts of the industry that have managed to stand on their own feet were/are LCCs and dedicated air freight companies.

– Not sure to what extent it is true to say that “owners continue to believe in their investments” in a scenario in which investments generally can’t be ditched without penalty. The mass use of penalty-free cancellations of 737MAXs shows that quite a few customers ran for the exits. Large numbers of orders were deferred to later dates, and/or downsized.

The industry as a whole has incurred crippling debt; the only salvation at the moment is that interest rates / loan terms are relatively favorable. However, one can wonder to what extent governments will be willing to provide further support when a (large portion of a) green-frenzied electorate is becoming increasingly anti-aviation.

What crippling debt?

This isn’t 1960s anymore , very high gearing is normal now.

American Airlines for example isnt investment grade credit rating but can access borrowing and buy and lease new planes.

Here you go:

https://www.ft.com/content/0a334f3e-3bb3-4ff3-96ed-39a5b3fe821b

This is known in industry parlance as “marketing fluff”.

I would not take it so literally.

@Trevor

In common parlance this is known as lying

It depends who you are talking to – AB is talking to those who wish to believe in miracles almost as much as they do

In many cases the ‘bailouts’ were loans which would result in Government equity should they not be paid back. In the case of Lufthansa they have just been paid back. In most cases in the US the ‘bailouts’ were payments to not furlough employees.

First (big) order news from Dubai:

“Airbus Gets Mega-Order for 255 Jets From Wizz, Frontier, Volaris”

“(Bloomberg) — Airbus SE received a mega-order for 255 narrow-body jets from the constellation of discount carriers founded by airline entrepreneur Bill Franke.

The follow-on deal with Indigo Partners LLC is for the A321 model, the larger version of Airbus’s top-selling narrow-body family of jets. It is valued at more than $30 billion before typical industry discounts.

Wizz Air Holdings Plc will take the biggest share of the batch, ordering 102 planes, while U.S. discounter Frontier Group Holdings Inc. will buy 91 jets. Mexico’s Volaris Aviation Holding and JetSmart Airlines SpA of Chile ordered 39 and 23 planes each.”

https://www.bnnbloomberg.ca/airbus-gets-mega-order-for-255-jets-from-wizz-frontier-volaris-1.1681709

I wonder when they are due to be delivered? Rate 70/month here we come?

Interesting question.

Also noteworthy that this order really allows WizzAir to turn up the heat on Ryanair, which is still limited to the much smaller 737-800 / 8200, and is involved in a public standoff with BA regarding the MAX 10.

Airbus is killing it. Poor Boeing.

Bloomberg had an article today saying Emirates will lower the 112 777X remaining firm orders even more still — out of the 150 original ones.

Hre’s the link: https://tinyurl.com/weurmakp

Same old same old

‘In 2014, he axed a deal to buy 70 Airbus A350s, which constituted the single biggest order loss for the European planemaker at the time. ”

Its a re-negotiation tactic, thats all.

@DoU

There’s no point in retaining an order for a plane whose EIS keeps on slipping, and slipping, and slipping…

So 4,000 ‘big’ aircraft over the next 30 years, or so. Let’s assume he means A350’s & 777’s. That breaks down to ~133 a year, or 11ish a month, from both OEM’s. Seems a tad bit high, no? Unless perhaps you include 787’s and A330’s in there…

5,340 ‘medium’ aircraft.

If you throw in all current widebodies into the ‘big’ category, it looks like there is a case to be made for the MMA/NMA/797/MoM aircraft, no?

Evolution, Historic:

Gains in transmission

Decrease in lethality.

Dead hosts don’t propagate much. 😉

.