Leeham News and Analysis

There's more to real news than a news release.

Airbus posts solid 2022 full-year results despite supply chain problems

By Bjorn Fehrm

February 16, 2022, © Leeham News: Airbus presented its results for 2022 today. The company announced net profits of €4.3bn on revenue of €58.8bn despite several disruptive events during 2022.

Disruptions like the effects of the Russia-Ukraine war and the supply chain ramp after COVID kept the delivery increase for 2022 at half the target of 110 jets, resulting in 661 deliveries instead of the originally guided 720.

Guidance for 2023 keeps the 720 airliner delivery target, an operating profit of €6bn, and a Free Cash Flow of €3bn.

Figure 1. Airbus results highlights. Source: Airbus.

Group-level results

Revenue for 2022 was €58.8bn (€52.1bn 2021), operating profit €5.6bn (called EBIT adjusted, +€4.3bn 2021), and net profit was €4.3bn (+€4.2bn). The results include a net €0.3bn write-off due to mainly A400M contract price adjustment losses. Airbus announced it would pay €1.80 dividend to its shairholders.

Free cash flow for 2022 was €4.7bn (€3.6bn), and the net cash position at the end of 2022 was €9.4bn (2020 €7.6bn).

Guidance for 2023 is:

On condition of no additional disruptions of the world economy:

- Airbus targets ~720 commercial aircraft deliveries for 2022.

- Airbus expects an EBIT Adjusted of ~€6bn

- Free Cash Flow of ~€3bn.

Commercial aircraft

The division had 820 net orders during 2022 (507), with a backlog now at 7,239 (7,082) aircraft.

Of the 664 (611) deliveries during 2022, 516 (483) were A320/A321, 53 (50) A220, 60 (55) A350, 32 (18) A330.

The A320 series is now sold out until 2029. The ramp to 65 per month is planned for the end of 2024, and 75 is delayed to 2026 from 2025. In the early part of 2022, the supply issue was engines, but once this eased, the supply of many parts hit bottlenecks because of chip shortages and special material shortages.

The rumored internal disruptions were the struggle with constant replanning and improvisation from Airbus’ side, trying to handle the situation more than any systemic issues, according to CEO Guillame Faury.

Widebody demand has come back faster than expected. There are no delays in the delivery of widebodies, but the production rate of the A350 is now raised to nine per month by the end of 2025 (at six right now).

The A330neo also sees increased demand. The present rate of 3/month is raised to four in 2024.

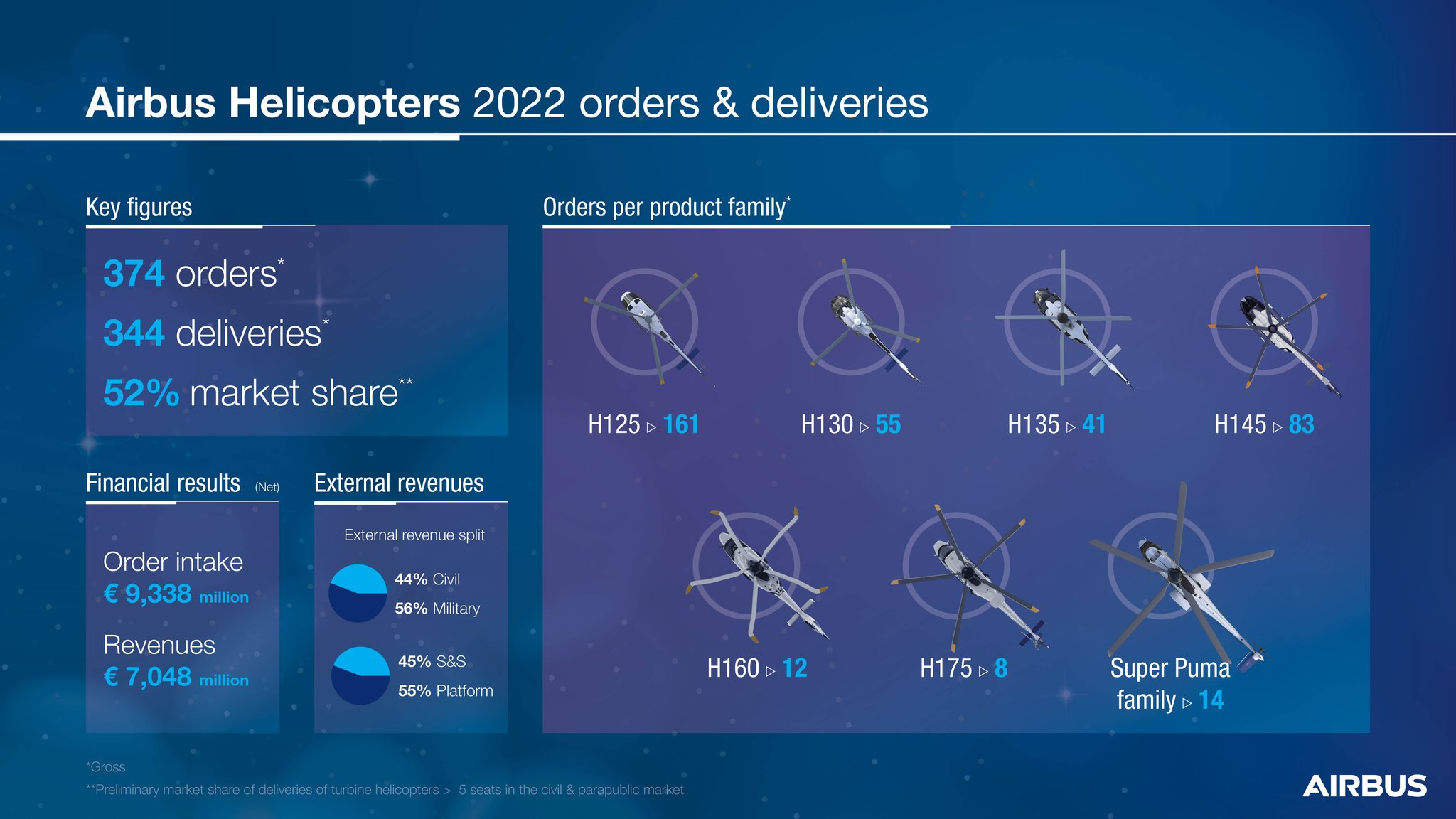

Helicopters

Figure 2. Airbus Helicopters highlights. Source; Airbus.

Helicopters had a solid year. Revenue increased to €7.0bn, Figure 2, (€6.5bn) and EBIT to €0.64bn (€0.54bn). The product program is under renewal, Figure 2, with several countries certifying the new H160.

Defense and Space

Defense and Space had q troubled year with delays of the Ariane 6 launcher and the failure of two Pleiades satellites. The problems with Russia meant the Souyz launchers were no longer available. It leaves Europe without access to space for 2023, and this is a wake-up call, according to Faury. European cooperation must be reinforced after a period of national interests. On the positive side was the agreement of Phase 1B of the FCAS fighter program with Daussault and the contract for the Eurodrone.

Revenues were €10.3bn (€10.2bn), with EBIT at -€0.12bn (€0.38bn).

10 (8) A440Ms were delivered in 2021. The losses of €0.5bn for the program were a result of a contract that does not compensate adequately for inflation effects.

Only shows how incredibly useless analysts are in the only thing they are supposed to do: analysing.

I can’t believe that they missed the last 3 years of Airbus increasing margins to mindboggingly figures (above and beyond 20 percent for the A321 neo for example), and all analysts care are delivery numbers. It also leads to the issue of Boeing being overrated because they only care about negative margin deliveries

Some years ago I pierced the resoning and why managers use analyist (in this case a weather forcast)

We had a heating system we had to shut down mid winter and temps were too cold but it was failing.

So the manager looks at the forecast and says, we can limp it along until next week.

I had looked at the forecast as well, but they are lucky to get it right the next day and at times pouring rain and they would say clear and sunny.

His next remark was, well it gives me something to base a decision on (blame).

Mine was, you know you can’t count on it.

All they want is a way to deflect the consequences, aka, well the forecast said it would be warm enough to delay the work.

So that is what analysts are for, someone to blame, you don’t suffer the consequences, they know they will be wrong and everyone is happy (they have a job they know won’t be right but heh, its a living) .

Too bad there is no + or – voting in the Comments section.

You have earned my +

Having worked for one big corporation and sub contract to another and deeply involved in the engineering decisions (ungh), its truly amazing the shenanigans they pull out of the hat under the mantra, its a Business decision.

Anything they can get away with justification wise (analysts ) to hang the hat on no matter how big the lie.

FedEx was a hoot for a thing called Strategic Sours Initiation. Going to save 10 million next year, it disappeared when it cost them 7 million. It was good for a gotcha, uhhh is this the same as SSI? Talk about dirty looks.

Its astonishing that they make any money let alone successful. Probably why I was a worker Bee, I just didn’t know how to squint my eyes right.

It is a strongly partisan environment.

A majority of Analysts are mouth pieces for interested parties.

Remember all those bright boys (and girls) judging the announced Airbus NEO move as unwise and judging Airbus pressured by C-Series but not Boeing 🙂

American lifestyle : “weaponizing everything”.

About 10 percent below delivery targets, and still they have earned more than their target.

Only Apple in the smartphone industry command a way higher margins gap as compared to their competitor

Congrats to Airbus for excellent numbers.

press conference:

https://www.youtube.com/live/8ZwMEjrt3S4?feature=share&t=695

Watching this press conference is a must!

Up to the end!

Quite a lot of unfiltered questions, and most of them were answered…

No PR no BS

Some applaude at the end…

Placeholder.

‘The A320 series is now sold out until 2029. The ramp to 65 per month is planned for the end of 2024, and 75 is delayed to 2026 from 2025.’

Is it sold out with the planned ramp up to 65, then 75 – or do those ramp ups open up additional delivery slots?

Frank.

Sort of. There are new slots being created.I wouldn’t be surprised if they aren’t sliding new birds in the line now as a slow expansion. you dont There are commitments in hand for some percentage of the rate increase and those will be slotted in between the existing orders after the airplanes customers wishing to be pulled forward are moved. Sales says that they can fill the rest of the slots created. The airplanes cost so much that white tails are not built on purpose in usual circumstances. This isn’t like building toasters, they are highly configured and need to to be defined well ahead of the build date. Remember our discussion about LSO freeze dates, the equivalent process at BA for the last day a change affecting a line station in the factory. ABs rate increases this close to whatever they call LSO Freeze shows how strong their market really is.

“sold out” is gapless extrapolation of sold items vs production capacity.

In contrast customers may have arranged ( or will arrange ) increased spacing deliveries.

Future is not static. Customer Airlines go belly up, defer their orders, change their orders …

Congratulations to Airbus, well done.

It would have been nice to see honesty in the estimates for last year when it was clear they would not meet the target. That is baffling.

Nothing wrong with issues in very challenging times.

Airbus’s guidance- verbatim- was that they planned to deliver “around 700” aircraft in 2022. 673 (correct?) / 700 = .961 .

Your point, again?

No. It was 720 for 2022 at the start of that year ( thats what they are comparing with in this years guidance )

Of course it was revised later in 2022 but missed even the revision. Maybe explaining that Chinese airlines have put a hold on deliveries might have helped- as they were likely to be delivered later.

Duke:

Thank you. 720 was the number.

I had no issue with Airbus not meeting targets, its truly a weird supply world out there (Costco has been out of Refried Beans for months now – it was cheese before and Chicken and worst, Grey Poupon!)

Being honest increases your credibility. One of the best accolades I got was from a Branch Manager, he does not lie to us, he tells us the issue, how long he thinks it will take and any delays. We may not like what he tells us but we appreciate his honesty in doing so and we know where things stand fix wise and when it will get resolved.

673 / 720 = .934 of their early-year target, then. Seems good. Apparently those commenters are unfamilar with the word “around”, which does not surprise me.

How’d Boeing do in meeting their claim of 500 737 Max MAX deliveries in 2022 ? 380 (I’m being generous) / 500

= .76 . I won’t mention the 787, or their other lineup.

Then there’s the question of Boing’s margin on those planes; Frank and Bryce have covered that pretty well.

Boeing had to start from a complete stop of 737 production, much harder to get back up again. Also the delivery of existing stored planes was slower than expected ( probably because it was top management who chose the number rather than the line staff)

Airbus had some pauses due to covid but reduced production mildly at its multiple sites but never had a cold FAL to restart.

Remind me why BA resisted to cut back its 737 production for so long after it was grounded?? Because, cough, cough, those imaginary FCF thanks to delayed payments to suppliers was going to come back …. pause, check note, to bite in the you know where 🤭

It’s BA’s self-harm (MCAS) one after another (excessive production + mgmt’s blind optimism of how soon the MAX can fly again + worry of the unwinding of supply chain cash hoard).

BTW didn’t BA promised to clear its 737 MAX inventory in two years (back in 2020)? Who said (in)famously those inventory was “*as good as cash*”??

“Boeing had to start from a complete stop of 737 production …”

Boeing knew that, right?

i.e. their communication was fully fantasmagoric (or however you call that.)

Dec 2022 delivery: 109.

Any chance those who insisted to project full year’s delivery # based on 9 mths’ # come forward and apologize they were wrong?? 🙄

Congratulations to Airbus.

Well oiled machine firing on all cylinders.

I would say they are missing gallons of oil through no fault of their own and are managing the low oil supply as best they can.

And no $16bn surprise such as deferred production costs!

no negative impact of rising interest rates…

Because Airbus main figures are done under unit accounting not program , which Boeing does as a comparison on its annual accounts only

I note that Airbus commercial aircraft revenue is €40 bill despite their very high deliveries and a free cash flow of only €4.7 bill

@Dukefurl

That is interesting, one would think their revenues would be higher. Hmmmm.

Yes. Its about the same revenue as the Renault Group € 46 bill but their free cash flow was roughly half of Airbus total business segments. Plus they had the shutdown of their major Russian business

Hmmmmmmm, There revenue’s were higher.

Very high deliveries, huh? As compared to what? 2018? The year before? To Boeing? I thought everyone was saying they missed the 700 target and fell short? Which is it?

————————————————————————

Well, let’s dive in, shall we?

In 2021 they delivered 611 aircraft for 36.164 billion Euro’s.

EBIT was 4.175 billion Euro’s.

(I wish I knew how to make that ‘euro’ sign)

In 2022 they delivered 661 aircraft for 41.428 billion,

EBIT was 4.8 billion Euro’s.

Revenues up 14.6%

EBIT up 15%

1 Euro is about $1.22 USD

So those revenues from Airbus commercial is about $50.5 billion.

EBIT is ~$5.85 billion.

Free cash is $5.7 billion.

———————————————————————-

Now….about FCF and why, for Airbus – it really isn’t a thing;

From a business site:

“Free cash flow is important to investors and business analysts because it shows how much cash your company has at its disposal.

They often assess your free cash flow to determine whether your company has enough cash to repay debts, issue dividends and buy back shares.

Positive free cash flow can indicate you have plenty of cash left over to pay bills or investors, or to reinvest in new opportunities. In contrast, when it’s negative, it can mean your business isn’t generating enough cash to support growth.

Even so, it’s important to mention that negative free cash flow isn’t always a bad sign. For example, it could indicate that your company is heavily investing in growth that could potentially result in high returns and pay off in the long run. On the other hand, excessive positive free cash flow can signal that your business is holding its assets idle rather than reinvesting them for growth. ”

So let’s see…Does Airbus have a DEBT problem.

Nope. IIRC they were up some 9 billion Euro’s after all debt was accounted for.

Dividends: They’re declaring a 1.8 Euro dividend.

Buybacks: Nope.

——————————————————

Now….since it’s a duopoly and everything is very easy to compare, do you want to have a look at how the competition fared in 2022?

BCA sold 480 jets, got $25.8 billion and lost $2.370 billion.

Dividends? Nope.

————————————————————-

Margin for Airbus: 11.6%

Margin for BCA: (9.2%)

And about those revenues…

(The only way to see how they did and how much they should have been getting, is to do a comparison. Since there are only 2 horses, it’s fairly easy)

Let’s have a look see at the delivery mix and the revenues generated at both AB & BA;

—————————————————————————-

In 2022 BA delivered 480 aircraft for revenues of $25.867 billion.

In the delivery mix, there were 387 narrow bodies and the rest were wide bodies. About 80% NB’s.

In 2022 AB delivered 661 aircraft for (USD Eq) ~ $50.5 billion.

In the delivery mix, there were; 53 A220, 516 A320 Family, 32 A330 and 60 A350. 86% were NB’s.

Narrow bodies typically have:

1) A lower ticket price

2) A lower margin

In USD, BA earned in revenues an average of $53.9 million a delivery with an 80/20, narrow to wide split.

AB earned $76.4 million (using the euro to USD exchange) per delivery, with an 86/14 split.

Even if you keep it in Euro’s, they earned 62.674 million per delivery.

With a higher mix of supposedly cheaper/lower margin aircraft.

————————————

Imma go out on a limb here and say that in this 2 horse race, the 2022 OEM Derby had a horse that should have been sent to the glue factory.

Show me where I can find it from “its annual account”!! It’s not part of the 10K. Why would BA show unit accounting in its annual account? 🙄

Boeing has been showing unit accounting alongside program accounting, for the BCA numbers in its annual accounts ( not quarterly) since around 2002 .

Same as you dont know the FAA can give approval for 777X test flights for certification under LOA and not just TIA

Facepalm. Just one thing to prove: link please.

BTW that’s not what I posted. Another mistaken identity🎈. Help.

That’s double of BCA revenue 🤭

Very true. Having look at delivery mix:

BA: 480

NB: 387

WB: 93

AB: 661

NB: 569

WB: 92

So the number of the higher ticket price aircraft delivered were essentially the same. AB delivered 182 more narrow bodies.

I don’t think that Airbus all of a sudden got massive increase in aircraft ticket price. These things are negotiated years out. I think it’s a case of Boeing having to heavily discount it prices – when customers bailed on contracts because of the Max grounding and 787 stoppage.

The concessions made were probably substantial

Having look…

What the heck king of English is that???

Have a look at the delivery mix, please

What I am reading is Airbus has throttled back the single aisle ramp up and is working on wide body increase.

That is an up front thing to do. Ok, we got plenty of data and call it like it is not what we want it to be.

On a side note, Boeing looks to pick up more P-8 contracts and the Wedgetail to replace the failing AWACs. The Wedgetail was an ambitious money loosing program but it looks to pay dividends now.

Look like that move to DC will pay off big time for Boeing- hitting up Uncle Sugar for those very sweet defense ™ contracts..

Wedgetail was a project for the RAAF, which lost money mainly on the radar side , not sure if that was a separate contract with Northrop Grumman.

Putting a fixed scanner onto a 737 fuselage would have just been a development of the designs and data for the E-3 707 Awacs

As for the airframe, no need to new build any 737 NG models , as most if not all the previous production was from used 737-800 or 700s

Boeing stopped production of the 737MadMAX long, long before they

made their claim of 500 MadMAX deliveries for 2022. Why then did

Boeing not come nearly as close to their target at Airbus did theirs?

Which company’s veracity would one sooner trust, if required (trusting any large and hence powerful entity is not someting I prefer to do) ?

A miss of 25% or so is *much better* in the eye of some beholders

Can’t wait to see what happens when the fourth FAL opens 😁

I’m going put it as “Fourth Assembly Line”, for now.

PR-talk until firmly shown otherwise, which is what that company

now does best. Hey, maybe it’ll happen, like the NBA / NTA / NSA / NMA..

throwing resources at a late programme makes it later.

( stolen from Mythical Man Month 🙂

From UAL, BA notifies 37 Maxes due in ’23 to arrive in ’24; UAL expects a further six due in ’23 to arrive in ’24. Let me see, 37 + 6 = 43. Shocking but not shocking.

I’m interested to see the uptick in the A330neo production rate, from 3 to 4 a month. I’ve a feeling this program is going to be wildly successful. It started off as “who’d ever want to buy that?”, and now, not much later with a pandemic in between, the production rate is being increased. Plus, everyone who flies on it seems to like it (quiet, comfortable, etc).

As much as anything else, the beginnings of the A330p2f market will probably be instrumental. The proposition is heading towards, sell your old A330s into the p2f market, buy A330neo for comparatively little, operate that knowing that there’s a good second hand price (into the p2f market) at the end of its service. That makes it sound like the second hand car market. Well, it is. The point is that it’s a market that can involve an awful lot of widebody Airbuses, but is a market that’s not really going to involve any more widebody Boeings.

I can also remember Boeing dismissing the A350; words such as “late”, “not as good” were being used. But that’s headed towards 1,000 orders. Those numbers don’t match 787’s, yet, but the difference seems to be that Airbus are making money on them where Boeing isn’t on theirs.

From reading Scott’s excellent book and seeing there Leahy’s drive for market share, it’s quite remarkable how Airbus has gained market share whilst being profitable. On an even competitive basis, the only way normally to achieve that would be on price; being cheaper. Yet, they’re not. The failings of Boeing to invest and react properly to market movements is writ large in Airbus’s seemingly unimpeded financial figures. Airbus has even “got away” with doing an entire megajet program (A380), without serious damage to their overall position.

Agreed Matt, except for one thing:

The 787 and the A350 don’t compete against each other. The 787 competes with the A330Neo and the A350 competes with the 777X.

Looking at the bigger picture, even if Airbus breaks even on the A330Neo, given the losses that BA has taken on the 787 program….it’s a win.

They wanna sell 1500, 1600, 1700 units and lose money on the program? Sure. Help yourself.

We won’t even start on the 777X program and their $6.5 billion write off. That story is done and dusted.

Oh Mr. Leahy was wheeling and dealing alright, because he was playing with house money. Have not read Mr. Hamilton’s book but I sure he also included the “amazing” deals Leahy was known for, again it was about market share.

Now I feel old, I don’t need to read a book about, I lived through it.

I also think the A330neo will do quite well. AB appears

to be sitting pretty, while not resting on their laurels (rainy day fund, WoT, A321XLR..).

If the foretold A330 replacement cycle hits in a couple of years (Boeing is saying the same for a 777 replacement in a couple of years) then it makes sense for the A330NEO to get a number of orders, competing with the 787 and A321XRL.

Sitting on its laurels may be happening now, and no that is not a bad thing. Already there is talk of re winging the A320, not a new gen, and stretching the A220. Not exciting stuff but financially prudent. Airbus has 8 years of A320 family backlog to turn into cash so they have years of strong financial numbers like last year.

After years of seeing Boeing stockholders fly in First Class, Airbus stockholders are now flying in first class. They will not want to go back to coach.

Re-winging the A320 series with AB’s Wing of Tomorrow technology seems a logical and likely

next move. Maybe a 2027-8 launch?

At UPS request, Airbus is planning an A330neo as a cargo version. This should be longer than the A330-900.

I think you are confused by the A350F , which is ( supposedly) longer than the 900 version its based on.

Doesnt make sense to stretch the A330 a fairly low production rate plane

TOULOUSE—”With demand for widebodies returning forcefully, Airbus has decided to substantially increase production of the A330neo and A350, while working on the potential launch of an A330neo-based freighter..”

https://aviationweek.com/air-transport/aircraft-propulsion/airbus-boosts-widebody-production-slows-narrowbody-growth

That Aviation Week link regarding Airbus is worth a full reading- at least for the evidence based community. I think this A330neo freighter will be happening, and sooner rather than later.

Any news on the proposed Boeing 787F ?

@Vincent: Boeing is still working on the 787F. I’m looking for Paris Air Show, maybe

Hamilton

Thx.

” … the evidence based community”

😏

-> “Some airlines are also pondering follow-on A350 orders as the European Union Aviation Safety Agency’s (EASA) certification conditions of the Boeing 777X and timing of its entry into service remain unclear.

LH?? IAG?

Yup I vaguely remember this. Thx.

Airbus had a sweet heart deal of repaying loans only if the program was successful. One of Boeing’s many failings in competing with Airbus, Boeing should have went to DC and ask for the same deal.

Ahhhhhh, the old ‘gov’t money’ and subsidy argument, huh?

Boeing get’s public cash, as well:

https://subsidytracker.goodjobsfirst.org/parent/boeing

$74,990,849,922

$75 billion.

Anybody can google and find some obscure website to evidence to back one’s arguments.

https://www.lexingtoninstitute.org/wp-content/uploads/EuropeanSubsidiesBrochureFinal.pdf

Boeing arrogance got the best of them. They got out hustled by Airbus, my argument if Boeing was savvy, they should have went to DC and asked for the same deal.

The veracity and solidity of *presented evidence*

can often be discerned. Those who make vague assertions without providing support usually do so because they don’t have any of that evidence-thingie.

The commenter here who repeatedly, over months, claimed that Airbus called their aircraft “delivered” at the time the wind and fuselage- providing no evidence whatsoever, of course- is one sterling example, but there are others. 😉

“..at the time the wing and fuselage were joined..”

No edit button available at this time.

Hello Williams,

As you run down sources, I was wondering if you could clarify your comment above about higher revenues.

Thanks

On a side note:

You thought that AB revenues should be higher, correct?

Well – as another comparison, I offer you this:

This is the annual report for 2018, right off the Boeing website (you find them reasonably suitable as a verified source for this, yes?). Their most successful year, ever:

https://s2.q4cdn.com/661678649/files/doc_financials/quarterly/2018/q4/4Q18-Earnings-Release.pdf

They delivered 806 aircraft (580 NB & 226 WB – 72/28 mix) for Total Revenues at BCA of $60.7 billion.

As noted above 86% of Airbus’ 2022 commercial deliveries were NB, as opposed to 72% in Boeing’s 2018, where 28% were the higher priced wide bodies.

806 Deliveries

72% NB

$60.7 billion in revenues

Airbus 2022

661 Deliveries

86% NB

$50.5 billion (equivalent USD) in revenues

The Boeing margin for 2018 was 13%, while Airbus had EBIT of 11.6% in 2022 – but this can be attributed to the higher mix of wide bodies, which do deliver better profits.

———————————————————–

So, I’m curious;

What kind of revenues should Airbus have had, in your opinion?

@ Frank,

I thought they would be in the $60 Billion range. I incorrectly thought Airbus was producing more Narrow Bodies than what they are now.

Thought the revenues be a little higher but anyway you slice a great financial year.

@Williams

$60 billion in revenues? That’s Boeings best year ever. No groundings. No virus. No supply chain issues. 800+ deliveries.

They made $50 billion on 661 deliveries. They did produce more narrow bodies. 86% were NB.

Airbus achieved 84% of Boeing’s best year ever in commercial, with a much higher narrow body mix, in a turbulent year.

After running the numbers – I know it’s a great year, given all the circumstances. It looks even better when compared to the competition in the duopoly.

If you feel that their revenues were low, then you must be absolutely shocked with the figures of $25.867 billion that BA posted – about half of what Airbus did.

The difference between the two was that Airbus delivered ~180 more narrow bodies and got ~$25 billion more revenue.

Remember that a significant percentage of AB’s NB (half or so??) delivered are the pricier A321neo. OTOH BA is doling out compensation nonstop to customers for delay deliveries (MAX 7 and 787).

@Pedro

You know, I thought that too – but then I had a look at what the delivery breakdown was:

https://en.wikipedia.org/wiki/Airbus_A320neo_family#Operators

A319Neo: 12

A320Neo: 1,657

A321Neo: 939

I’m not sure what the mix was in 2022, but if it is close to the same and the Airbus backlog is:

A319Neo: 79

A320Neo: 2,323

A321Neo: 3,679

BA is in for a rough ride in the financial arena – as they deliver more of the pricier A321Neo’s.

Makes me wonder – the orders are definitely slanted in the A321Neo’s favour, vs the A320Neo. Is there a big push by Airbus, behind the scenes, to clear out the A320Neo backlog as fast as possible – to make way for an A220-500?

@Pedro

Yah, you’re right. I had a quick look at Planespotters and the A321Neo production list. A quick, unscientific scan has them delivering about 300 of them, in 2022.

They pushed out 516 in the A320Neo family, so it’s looking like a 60/40 split, or better – in favour of the A321Neo.

Maybe you should read Scotts book nonetheless.

Just to refresh or more like correct your fond memories?

RLI is an interesting steering instrument.

Overall rather profitable for the lenders.

Much more functional than those “no consequences” tax gifts Boeing received on a regular basis.

No my memory is just fine, I don’t need to Google my facts.

The rising of Airbus because of Leahy was well documented with every major order victory by AV weekly, ATW and WSJ to name a few.

Congrats to Airbus, they hustled in the 90s , and have been reaping the rewards for a while now.

Investors/speculators/traders wish to enjoy a bigger handout in a “free” “capitalist” world!

I wonder why stale arguments are reheated periodically from these same posters 🤔

Your spinning makes me laugh sometimes, thanks.

I have to wonder in a so called information age, how many act like (or in fact) they live under a rock?

-> Boeing Looks To Give Up A Tax Break

“The Boeing Company is bringing an unusual request to state lawmakers in Olympia: Please take away our airplane manufacturing tax break.”

https://www.google.com/amp/s/www.opb.org/news/article/boeing-company-washington-lawmakers-airplane-manufacturing-tax-break/%3foutputType=amp

Pedro….

You did notice that was 3 years ago….

So? Those that fail to learn from history …

“Boeing should have went to DC and ask for the same deal”??

-> Today, Boeing’s board approved a grant of 25,000 shares to CEO Dave Calhoun. Half will vest in 1 year, the other half in 2 years That’s worth $5.3 million at todays price

https://mobile.twitter.com/dominicgates/status/1626707746157662208

Calhoun has every incentive to stay on for two more years!!

Pedro

Calhoun staying is probably a good thing. His direction of late has been correct. Clean up the existing programs, continue to staff. Grab a Nass/Darpa truss wing demonstrator contract and continue forward. All of that is good….. he is still connected to the past craap, but of late doing a decent job….

Just effin’ remarkable- and indefensible, under that

company’s straitened circumstances.

“We can’t afford a new airplane: we need that money to make our visionary™ CEO even richer! All Hail Our Great Leader! Hoo-Rah! Hoo-Rah! Hoo-Rah!”

Adding: That’s sure to go over well with Boeing’s already pissed-off suppliers.

Also very telling;

From the Airbus financials, long notes;

https://www.airbus.com/sites/g/files/jlcbta136/files/2023-02/Financial%20Statements%202022.pdf

CEO Compensation 2022

(including share based compensation)

6,269,678 Euros

($7,649,000 USD)

At the other member of the duopoly, Calhoun is pulling down about $21 million a year.

https://financialpost.com/pmn/business-pmn/boeing-offers-ceo-5-3-mln-incentive-to-stay-through-recovery-2

Boeing offers CEO $5.3 mln incentive to stay through recovery

‘Calhoun was Boeing chairman and then became CEO in January 2020 after the board fired Dennis Muilenburg. Calhoun had total compensation of $21.1 million in both 2020 and 2021. In 2021, the board approved a long-term incentive award target of $16 million.’

Reuters: Airbus says Air India to lease jets on top of record order

I found it interesting that there’s always slots available for *sizable* orders.

-> Airbus will start delivering narrow-body A320neo-family jets to Air India *at the end of this year*

Current production rate (nominal?) /mth

A350 5.6

A330 2.8

A220 7