Leeham News and Analysis

There's more to real news than a news release.

Iran war threatens Boeing in more ways than just airliner orders

Subscription Required

Now open to all readers.

Editor’s note: When LNA is asked about the progress of Boeing’s recovery, we always express a caveat before answering: It depends on events outside Boeing’s control. The Iran war is just such an event.

By the Leeham News Team

March 17, 2026, © Leeham News: The paradox at the heart of modern commercial aviation is that the materials engineered to insulate airlines from oil price volatility are themselves creatures of the petrochemical complex.

Boeing’s 777X and 787 programs, with their heavy use of composites, face high risks of disruptions and costs due to the Iran War. Source: Boeing.

Carbon fiber composites reduce fuel burn by 20% over legacy aluminum airframes. Yet the polyacrylonitrile precursor fiber, the epoxy matrix resins, the autoclave energy—the entire manufacturing stack—runs on oil. When the Strait of Hormuz effectively closed on Feb. 28, it did not merely threaten jet fuel supply chains. It aimed directly at the raw material foundation of Boeing’s two most consequential programs: the 787 Dreamliner and the 777X.

Airbus faces similar challenges for the A350. A major Boeing composites supplier, Toray Industries, is used in secondary structures, and the impact is far smaller. US-based Hexcel is a major composites supplier to Airbus through its European operations.

Related Stories

- Boeing asks suppliers for Middle East impact

- Middle East impact on Airbus, Boeing

- War will grind on until September

A Supply Chain Built for Efficiency, Not Resilience

Boeing’s shift to composite-primary architecture on the 787 was, at the time of its 2003 launch, one of the boldest material science commitments in commercial aviation history. The Dreamliner would be 50% composites by weight, a figure that stunned an industry still wedded to aluminum.

The 777X, launched a decade later, doubled down, incorporating the world’s largest composite wing box, manufactured using automated fiber placement technology at Boeing’s Everett facility.

The structural logic was sound: lighter airframes, lower fuel consumption, and reduced corrosion maintenance. What the program architects could not fully anticipate was the degree to which the supply chain serving those programs would concentrate, geographically and chemically, in ways that now represent systemic risk.

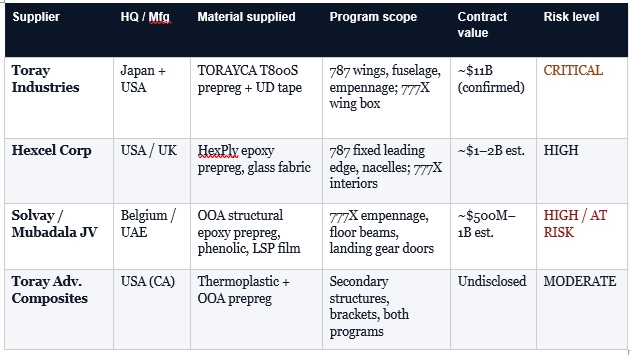

The composite materials supply chain for both programs flows through a remarkably narrow set of chokepoints. At the apex sits Toray Industries of Japan, which holds a supply agreement with Boeing valued at approximately $11bn across the 787 and 777X contract period, confirmed in Toray’s own investor disclosures. Below Toray in the Boeing hierarchy sit Hexcel Corp, the Connecticut-based materials specialist, and Solvay of Belgium, operating through a joint venture with Abu Dhabi’s Mubadala Development Co. These three entities supply the prepreg and unidirectional tape that forms the structural backbone of both aircraft.

Below them, a cluster of Japanese Tier 1 fabricators—Mitsubishi Heavy Industries, Kawasaki Heavy Industries, and Subaru Corporation—consume that prepreg, cure it in enormous autoclaves, and ship finished composite assemblies to Boeing.

The concentration is deliberate. Toray’s T800S intermediate modulus carbon fiber is not a commodity. Its specific combination of tensile strength, stiffness, and interlaminar fracture toughness was co-developed with Boeing over years of material qualification work.

Risk assessments

The switching cost—requalifying a new fiber supplier for primary structure on a certified commercial aircraft—is measured in years and hundreds of millions of dollars. Boeing effectively traded supply chain optionality for material performance. In the stable, low-oil-price environment of the 2010s, that trade looked rational. In the spring of 2026, it looks like a structural vulnerability.

Sources: Company reports, Leeham News.

When Oil Prices Attack the Manufacturing Stack

Carbon fiber begins its life as polyacrylonitrile (PAN), a synthetic polymer produced from acrylonitrile monomer, itself derived from propylene, a petroleum byproduct. Industry research consistently identifies PAN precursors as comprising between 45% and 60% of the total manufactured cost of carbon fiber.

The number matters because it means that carbon fiber pricing is not merely correlated with oil; it is structurally downstream of it. When Brent crude moves from $70 to $110 per barrel, as markets modeled in the weeks following the Hormuz closure, the feedstock cost for PAN production moves proportionately. The impact is directly reflected in prepreg pricing.

Epoxy resin, the matrix that binds the fiber in prepreg, adds a second petroleum dependency. The primary epoxy chemistries used in aerospace prepreg, including the toughened epoxy systems Toray supplies to Boeing as TORAYCA 3900-series, rely on bisphenol A and epichlorohydrin as base feedstocks. Both are petrochemical derivatives.

The market for aerospace-grade epoxy resin had already shown significant instability before the current crisis: price fluctuations of 18% to 22% annually have been documented from 2021 to 2025, driven by post-pandemic feedstock disruptions and energy cost volatility in European chemical manufacturing. The Hormuz shock compounds an already stressed baseline.

The third petroleum linkage, the one least visible to supply chain analysts, is energy. Prepreg curing is an autoclave process. The autoclave is essentially a large pressure vessel that applies heat and pressure to composite layups over cycles measured in hours, at temperatures typically between 120 and 180 degrees Celsius.

Japan’s vulnerability to oil

Mitsubishi Heavy Industries operates some of the world’s largest autoclaves at its Nagoya facilities, where it manufactures the 787’s composite wing panels and delivers them to Boeing. Those autoclaves run on grid electricity. Japan’s electricity grid is overwhelmingly dependent on imported liquefied natural gas. Approximately 70% of Japan’s oil imports transit the Strait of Hormuz. The LNG supply picture is similarly constrained. When Japanese energy costs rise—and they rose materially in the weeks following Feb. 28—the cost of curing composite structures at Nagoya rises with them.

The 787 Dreamliner: Production Stress on a Program Already Behind

The 787 program entered 2026 already operating well below its intended production rate. Internal Boeing targets called for 14 aircraft per month from Charleston by 2025. Actual production has recovered to approximately 7/mo, following the quality-control and rework crisis that consumed the program from 2021 onward.

This gap between target and actual output has accumulated as customer delivery deferrals, balance sheet strain, and suppressed cash generation. The Hormuz disruption arrives not as a shock to a healthy program but as additional stress on a structure already operating near its limits.

For the 787, the most immediate concern is not material availability per se. Toray maintains inventory buffers at its Tacoma (WA) and Spartanburg (SC) facilities, which are geographically insulated from the Gulf crisis.

But materials cost money. Long-term supply agreements between Boeing and its Tier 1 suppliers typically contain price escalation provisions tied to commodity indices. A sustained oil price above $100 per barrel triggers those escalation clauses and forces renegotiation discussions that consume management’s attention and ultimately translate into higher program costs at a moment when Boeing’s balance sheet cannot comfortably absorb them.

The company carried approximately $58 billion in debt entering 2026, a legacy of the 737 MAX groundings, the COVID demand collapse, and the 787 rework program. Margin erosion on the 787 at this stage of the recovery is quite painful.

More Japanese exposure

The secondary exposure runs through Japan. Mitsubishi Heavy Industries, Kawasaki Heavy Industries, and Subaru collectively supply approximately 35% of the 787 airframe by value: wings, center wing box, forward fuselage, and landing gear bay. These are not commodity structures.

The 787 wing is a single-piece composite structure of extraordinary complexity, manufactured at Mitsubishi’s Nagoya facility using automated fiber placement over a complex tool, then autoclave cured. If Japanese energy costs force production throttling at Nagoya, or if industrial action accompanies the energy cost shock, as has historically occurred during Japanese energy price spikes, the delivery of finished wing sets slows. Boeing’s line cannot outrun its wing supply.

The 777X: An Uncertified Program Absorbing an Unplanned Shock

If the 787 situation is serious, the 777X situation is acute. The 777X has not yet received FAA type certification. It has no production aircraft in service, no delivery revenue being recognized, and no inventory buffer of mature supply chain relationships to draw on.

Boeing has been building 777X airframes at a pre-certification production rate, storing them as it awaits regulatory clearance. The cost of carrying that inventory—materials, labor, facility overhead—continues to accrue without offsetting revenue.

Into this financial structure, the Hormuz crisis introduces two exposures specific to the 777X that do not affect the 787 in the same way. The first is the Solvay-Mubadala joint venture. Solvay and Abu Dhabi’s sovereign wealth vehicle, Mubadala, established a manufacturing JV to supply out-of-autoclave structural prepreg, phenolic prepreg, and lightning-strike protection film for the 777X empennage, floor beams, and landing gear door structures.

The manufacturing facility for this JV is physically located in the Abu Dhabi emirate. Iranian retaliatory actions following the Hormuz closure have included missile and drone strikes against UAE port infrastructure, including strikes proximate to Jebel Ali and Abu Dhabi. The probability of a direct strike on an industrial composite manufacturing facility in Abu Dhabi may be low, but it is no longer zero. For supply chain planners managing a program with no production buffer, even low-probability disruptions require contingency analysis.

As bad as a strike on UAE production facilities would be for Boeing, Airbus has extensive critical production volume there today. At Strata Manufacturing, Airbus is building half of all A320 ailerons, all A330 ailerons, many flaps and tailplanes, A350 inboard flaps, and an increasing volume of A400M parts. Loss of any of this capacity would be very disruptive. Airbus began contracting with Strata in 2010 and has billions in contracts through 2030.

The 777X’s composite wing

The second 777X-specific exposure relates to the composite wing. The 777X wing box and panels are the largest composite structure ever integrated into a commercial aircraft. It is manufactured using the world’s largest autoclave at Boeing’s Everett facility. It measures 130 feet long and 30 feet in diameter. The prepreg consumed in that wing box flows primarily through Toray, and the wing manufacturing process is deeply energy-intensive.

Boeing’s Everett facility draws power from the Pacific Northwest grid, which is substantially hydro-generated and therefore less exposed to natural gas price spikes than Japanese facilities. This is genuine insulation. The prepreg itself, however, is manufactured at Toray’s Tacoma and Spartanburg operations, and those facilities also consume significant industrial energy. The recent closure of the Alcoa Intalco smelter has reduced demand and provided capacity for Boeing’s future energy needs to be met within the existing generation capacity.

The certification timeline adds a further complication. Every month the 777X remains uncertified is a month during which Boeing absorbs production costs without revenue recognition. If the Hormuz disruption extends into mid-2026 and provokes sufficient input cost inflation to force renegotiations of supply agreements, these renegotiations will consume exactly the program management bandwidth that should be focused on advancing the certification case. Boeing cannot afford to fight on two fronts simultaneously.

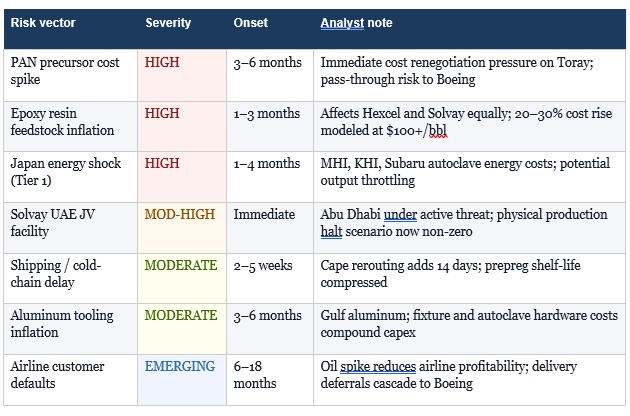

The following risk matrix maps the primary disruption and their estimated severity, onset timeline, and key analytical implications. The framework reflects a sustained Hormuz disruption scenario, defined here as partial or complete closure persisting beyond 90 days, which now appears to be the base case rather than the worst case.

Sources: Company reports, Leeham News.

Cold Chain Under Pressure

One risk vector that does not appear in standard aerospace supply chain analyses deserves separate treatment: the cold chain integrity of prepreg in transit. Aerospace prepreg is a temperature-sensitive material. It must be transported and stored at temperatures typically below minus 18 degrees Celsius to arrest the cure reaction of the epoxy matrix. It carries a defined ‘out-life’; a maximum cumulative time at ambient temperature beyond which the resin has advanced too far in its cure cycle to produce acceptable structural properties. Typical out-life specifications for primary-structure prepreg range from 10 to 30 days, depending on the specific material system.

The rerouting of global shipping around the Cape of Good Hope, driven by the effective closure of both the Strait of Hormuz and the continued Houthi interdiction of the Red Sea, adds approximately 14 days to transit times between Asian prepreg manufacturers and their North American destinations.

For a material with a 30-day out-life, an additional 14 days in transit compresses the working window available to fabricators from receipt to layup and cure. This forces either faster consumption cycles, which are operationally demanding, or acceptance of higher scrap rates when material approaches its out-of-life limit before it can be processed. Either outcome adds cost. Neither is visible in standard supply chain analytics focused on unit price rather than material yield.

Three Risks in Boeing’s Carbon Fiber Supply Architecture

The Hormuz crisis has done what crises typically do: it has revealed structural vulnerabilities that were present before the trigger event and will persist after it. In Boeing’s composite supply chain, three fault lines are now clearly visible.

The first is concentration without substitution optionality. Toray’s dominance in structural prepreg for both programs is not inherently problematic. Toray is a world-class manufacturer and a committed partner. The problem is the absence of a qualified alternative.

The FAA’s composite material qualification process is rigorous for defensible reasons: the structural integrity of commercial aircraft depends on predictable, repeatable material behavior. Qualifying a new fiber supplier for primary structure, achieving the same FAA Master Drawing List approval that Toray’s T800S currently holds, requires years of testing, coupon work, structural element tests, and component tests before any airframe integration. Boeing cannot simply pivot to Mitsubishi Chemical’s carbon fiber or Hexcel’s AS7 fiber for the primary 787 structure on a compressed timeline. The qualification infrastructure does not exist to permit it. This means that Toray’s supply reliability is not merely important — it is non-negotiable, and that non-negotiability is a structural risk.

The second fault line is geographic clustering of Tier 1 fabrication in a single high-exposure country. Japan’s energy import dependency, and specifically its Hormuz dependency, at approximately 70 percent of total oil imports, means that a Middle East conflict simultaneously pressures the cost structure of every major Japanese composite fabricator serving the Boeing programs.

Mitsubishi, Kawasaki, and Subaru do not compete with each other for Boeing supply; they serve different structural sections of the same airframe. Their collective energy cost exposure to a Hormuz closure is additive, not diversified. If all three face the same energy cost shock simultaneously, the aggregate impact on 787 wing and fuselage production economics is substantial.

UAE manufacturing

The third fault line is the UAE manufacturing presence for an uncertified program. Establishing prepreg manufacturing in Abu Dhabi through the Mubadala-Solvay JV was commercially logical. It gave Boeing access to a sovereign wealth fund’s capital and regional manufacturing capability, while giving Mubadala an anchor position in the global aerospace supply chain.

In a stable geopolitical environment, these benefits are real. In the current environment, the facility sits within the operational range of Iranian ballistic missiles that have already demonstrated a willingness to strike UAE infrastructure. The supply chain planning community has not fully incorporated this risk into its standard scenarios. It should.

The Demand Side Amplifier

Any analysis of supply chain disruption that stops at the factory gate is incomplete. The oil price shock transmitted through the Hormuz closure does not merely inflate Boeing’s input costs. It simultaneously degrades the financial health of Boeing’s airline customers. Aviation fuel remains the largest operating cost for most carriers, typically accounting for 20% to 30% of total operating expenses. A sustained move from $70 to $110 per barrel in Brent crude translates directly into airline margin compression, forcing network rationalization: route cancellations, capacity reductions, and, critically for Boeing and Airbus, delivery deferrals.

The history of the 787 program is already punctuated by delivery deferral cycles: the global financial crisis, COVID, and the 2020 quality hold collectively resulted in years of delayed customer deliveries.

Each deferral cycle imposes both direct costs: penalty clauses, storage and preservation of completed aircraft, customer compensation, and indirect costs in terms of program economics and customer relationship damage.

A sustained oil shock in 2026 that provokes meaningful airline delivery deferrals would represent the fourth such cycle for the 787, arriving precisely when the program was supposed to be generating the stable cash flows needed to service Boeing’s debt burden.

The 777X customer base, which includes Emirates, Qatar Airways, Lufthansa, and British Airways, among others, is disproportionately composed of long-haul carriers for whom fuel cost is existential. Emirates, the largest 777X customer with more than 150 aircraft on order, operates one of the world’s most fuel-intensive route networks. The airline’s financial calculus on its 777X deliveries becomes materially more complex in a sustained high-oil environment. Delivery deferrals from Emirates alone would have program-level consequences for Boeing.

What Boeing’s Supply Chain Leaders Should Be Doing Now

The near-term priority is an assessment of the inventory position. Boeing and its Tier 1 procurement teams should immediately audit current prepreg inventory positions at Everett and all major Tier 1 fabrication sites, with specific attention to out-of-life status and consumption projections against current build rates.

If Toray’s Tacoma and Spartanburg buffer positions can sustain current 787 production rates for 90 to 120 days without replenishment from Japan, the logistics rerouting risk is manageable in the near term. If buffer positions are thinner, as they often are in lean manufacturing environments that optimize for inventory turnover, the risk window is shorter.

The Solvay-Mubadala position requires separate, urgent treatment. Boeing’s 777X program office should confirm whether an emergency inventory build of out-of-autoclave prepreg for empennage and floor-beam applications is feasible, given current facility capacity. Boeing should initiate a qualification review to determine whether Solvay’s Belgian manufacturing operations can produce equivalent materials under the existing supply agreement if the Abu Dhabi facility becomes unavailable. That review should not wait until a disruption occurs.

On the contract economics front, Boeing’s procurement leadership faces a genuine nightmare. The escalation provisions in long-term supply agreements are designed to share input cost risk between the airframer and its suppliers. In a sustained high-oil scenario, those provisions will be invoked. The suppliers have no alternative if they are to remain economically viable.

Boeing’s objectives

Boeing’s objective should be to negotiate escalation structures that are transparent, index-linked, and capped in ways that allow financial planning, rather than allowing open-ended escalation that introduces budget volatility into already-pressured program economics.

The medium-term imperative—and this is a multi-year structural recommendation rather than a crisis response—is to invest in qualification to build supply chain optionality. Boeing should accelerate the material qualification pathways for at least one additional carbon fiber source for secondary-structure applications across both programs.

Primary structure qualification is a decade-long project; secondary structure qualification is a 2- to 3-year project and provides meaningful risk diversification. Hexcel’s AS7 and Mitsubishi Chemical’s TR50S are both plausible candidates for secondary structure applications and have existing aerospace qualification histories in other programs. Getting them onto the Boeing Master Drawing List for 787 and 777X secondary-structure applications provides a hedge without requiring the full primary-structure qualification investment.

The longer-term technology trajectory offers some comfort, if not near-term relief. Boeing has been investing in thermoplastic composite research that would partially decouple structural composite manufacturing from the epoxy resin supply chain. Thermoplastic matrices—polyetheretherketone (PEEK) and polyetherketoneketone (PEKK) being the primary aerospace-grade candidates—are not petroleum-derived in the same feedstock sense as bisphenol A epoxy systems. They also offer out-of-autoclave processing potential and infinite shelf life, eliminating the cold chain risk entirely. The barrier is cost and manufacturing maturity: thermoplastic composite processing for large primary structures remains significantly more expensive than thermoset prepreg, and the capital investment required to retool fabrication facilities is substantial. These technologies are not a solution for 2026. They represent the supply chain resilience case for 2035 and beyond.

The Bottom Line

The Strait of Hormuz crisis has exposed, with unusual clarity, the degree to which Boeing’s composite-intensive program portfolio is structurally coupled to global oil markets in ways that go far beyond jet fuel. The 787 and 777X programs—representing the core of Boeing’s commercial recovery thesis—rely on a prepreg supply chain that is petrochemically dependent at the raw material level, geographically concentrated in Japan at the fabrication level, and physically present in the conflict zone through the Solvay-Mubadala JV in Abu Dhabi. None of these linkages are irrational in isolation. Together, in the current environment, they constitute a material risk profile that was predictable and possibly downplayed by program architects.

For the 787, the primary concern is cost rather than availability. Toray’s North American manufacturing footprint provides meaningful insulation from logistics disruption, but the petrochemical cost escalation will flow through the supply chain regardless of geography. Boeing’s ability to absorb those costs without passing them to airlines without triggering delivery deferral requests from airlines simultaneously facing their own fuel cost pressure will determine whether the program’s cash generation trajectory holds through 2026.

777X’s acute concern

For the 777X, the concern is more acute. An uncertified program with no revenue offset, a Tier 1 supplier facility in an active conflict zone, and a certification timeline that was already subject to regulatory scrutiny is now absorbing a supply chain and cost shock on top of those existing pressures. The probability that the 777X achieves its current certification timeline without further delay has declined as a direct consequence of the Hormuz closure—not because of any single point failure, but because of the management bandwidth consumed by supply chain crisis response.

The Hormuz crisis is, in a sense, the first real geopolitical stress test of the composite-primary aircraft architecture that Boeing pioneered with the 787. The architecture has proven its aerodynamic and fuel efficiency beyond any reasonable doubt. Its supply chain resilience—the other half of the value proposition—is now being tested under conditions its architects did not fully anticipate. The outcome of that test will shape aerospace supply chain philosophy for the generation of aircraft programs that follow.