Leeham News and Analysis

There's more to real news than a news release.

Airbus 1Q2026 Results: First quarter “suffering”

By Karl Sinclair

April 28, 2026, © Leeham News: An abnormally downbeat Guillaume Faury, CEO of Airbus, was clearly not pleased with how things progressed in the first quarter of 2026.

April 28, 2026, © Leeham News: An abnormally downbeat Guillaume Faury, CEO of Airbus, was clearly not pleased with how things progressed in the first quarter of 2026.

When asked when commercial aircraft delivery rates will converge with production rates, he said, “We don’t like to guide or to give rates when it comes to monthly production rates or even quarterly production rates. It’s non-linear and tends to be backloaded in Q2 and Q4 in most years. That’s something that we are suffering from probably more this year than I remember we’ve ever suffered in the first quarter. But we believe, we hope, we believe we should be reasonably back to where we should have been by the end of H1.”

Faury outlined a series of issues plaguing the company, calling it a “desynchronization between production and delivery,” which includes panel quality issues, an “administrative delay” that affected the delivery of nearly 20 aircraft to China, the Pratt & Whitney engine problems, ongoing seating shortfalls, the continuing tariff war, and the recently started Iranian War. The latter two were launched by President Donald Trump.

Faury outlined a series of issues plaguing the company, calling it a “desynchronization between production and delivery,” which includes panel quality issues, an “administrative delay” that affected the delivery of nearly 20 aircraft to China, the Pratt & Whitney engine problems, ongoing seating shortfalls, the continuing tariff war, and the recently started Iranian War. The latter two were launched by President Donald Trump.

While he was detailing the current travails of the company, Faury said, “As the basis for its 2026 guidance, the company assumes no additional disruptions to global trade or the world economy, air traffic, the supply chain, its internal operations, and ability to deliver products and services.”

This type of disclaimer is almost always found buried in financial statements and reports as part of the Safe Harbor Statement. Finding it in an earnings call is unusual.

The tenor of the earnings call is somewhat surprising. But Airbus underperformed in its first quarter results. However, this is hardly a “It’s time to sell the silverware” moment.

Company-wide results

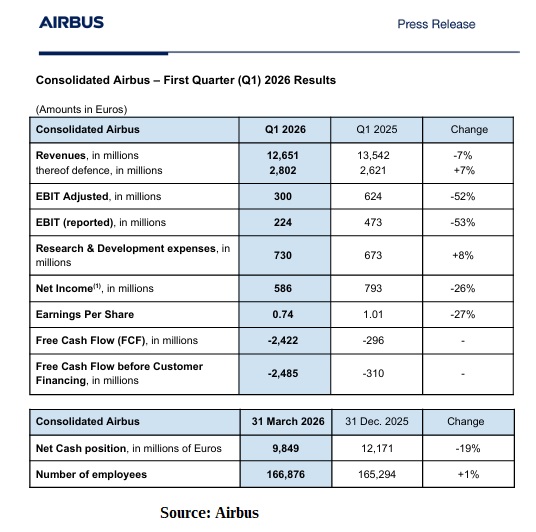

In what can be described as a difficult quarter for the corporation, by Airbus’ standards, the company earned a modest €300m (EBIT adjusted) on revenues of €12.651bn (€624m earned on revenues of €13.542bn in 1Q2025). This is a decline of €891m in sales and €324m in earnings, a whopping year-over-year drop-off of 7% and 52%, respectively.

The gulf widens even further compared with the results of the previous quarter, when the company earned €2.982bn on revenues of €25.984bn. While across the industry, Q4 is habitually the strongest period of the year (when deliveries are backloaded), Airbus expected to perform better in the current quarter than it did. This is highlighted even further, when compared to a strong FY2025, when it delivered 793 aircraft to customers and grossed €73.42bn in revenues and €7.128bn in earnings.

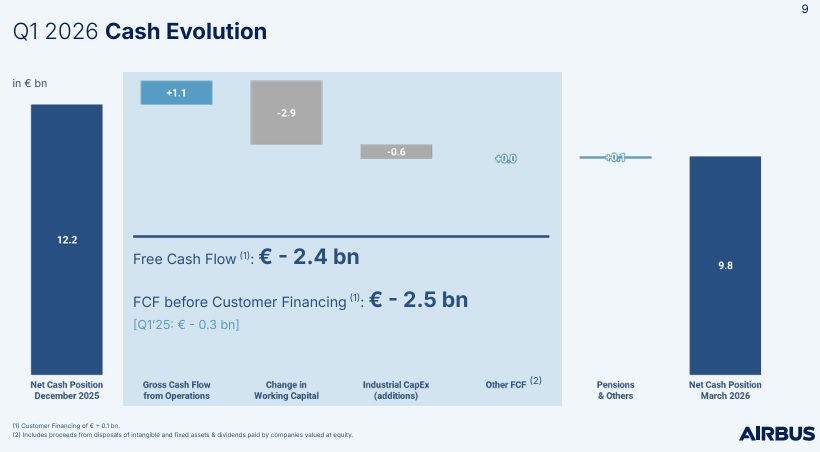

Airbus used €2.422bn in free-cash-flow (FCF) during 1Q2026.

“We built $5bn of inventory. That is significantly more than the build-up of last year, almost $1.5bn more build-up…that explains, obviously, the free capital development,” explained CFO Thomas Toepfer.

“We built $5bn of inventory. That is significantly more than the build-up of last year, almost $1.5bn more build-up…that explains, obviously, the free capital development,” explained CFO Thomas Toepfer.

Expectations are that the inventory will unwind in the coming months, reflecting in an improved financial performance in the near future. The silver-lining to the 1Q2026 results is that company earnings were still (modestly) in the black and full-year guidance remains unchanged.

Commercial Aircraft

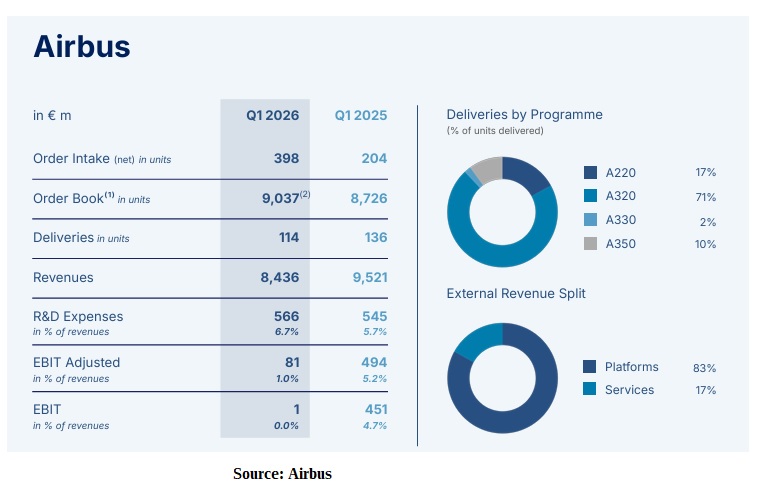

Revenues at Airbus Commercial declined €1.085bn in 1Q2026, year-over-year. This was driven by the “de-synchronization” between production and delivery, with the company unable to handover aircraft to customers and the resulting build-up of inventory waiting for delivery.

EBIT Adjusted plummeted to a paltry €81m, or less than a 1% margin on the €8.426bn generated in sales.

A total of 114 commercial aircraft were delivered (136 aircraft in 1Q2025), including 19 A220s, 81 A320 Family, 3 A330s and 11 A350s.

When asked about any updates on the Pratt & Whitney engine situation, CFO Toepfer said, “The shortage is the same shortage that we were talking about in our full year call. The situation in terms of what they told us they would deliver for 2026 has since then not changed.”

Airbus has also approached CFM, which markets the LEAP engine (which also flies on the A320 family of aircraft), to request help in ameliorating the engine shortage problem.

“We have worked with CFM to the maximum extent possible. They’ve supported us to the extent they can to offset part of the missing engines. But we also must deal with a mix of engines and the flow in the contract. So, it’s something we are trying to leverage as much as we can, but it’s not enough to offset the significant number of missing engines,” said Faury. “Pratt & Whitney remains the key pacer of our A320 ramp-up trajectory and deliveries for this year and for next year, impacting both 2026 and 2027.”

Seats and interiors

Seats and interiors are also in short supply. They are buyer-furnished equipment (BFE), which is ordered and paid for by the owner of the aircraft. There is a draconian solution in that regard, one which Airbus is reluctant to use.

“They impact the way we deliver–the completeness of the aircraft, especially when it comes to seats. You might remember that we’ve delivered, and we are entitled to deliver by contract, aircraft without the seats when the seats are buyer furnished equipment and they are late or very late. We don’t like to be doing this. We like to find solutions with customers. But that’s something sometimes we must do,” explained Faury.

This is the second earnings call in a row (the first being the P&W agreement), that enforcement of contractual rights has been mentioned, regarding equipment from suppliers.

Airlines, lessors and aircraft OEM’s traditionally work together to overcome the myriad of issues that arises over the life of a contractual order without the public ever knowing.

This is a troubling development, if it continues.

The bright spot of the quarter was the addition of 398 net orders to the backlog, which is now more than 9,000 aircraft, including a much-needed order for 20 jets in the A220 program. There was also a record freighter order by Atlas Air Worldwide, for 20 A350 freighters. This was a major win for Airbus, winning out over the Boeing 777-8F. Atlas has been an exclusive Boeing customer and operator.

Despite the plethora of headwinds, all guidance regarding yearly deliveries of 870 aircraft and all planned production rates remain unchanged.

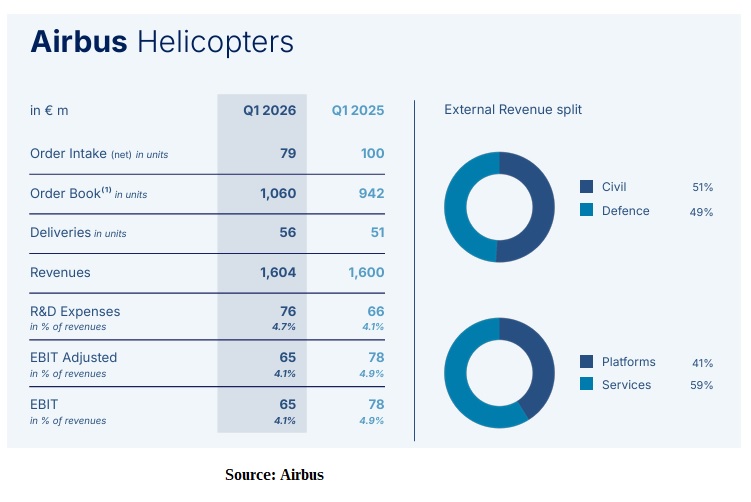

Airbus Helicopters

Revenues at Helicopters leveled out through the first quarter (€1.604bn vs €1.6bn in 1Q2025), with EBIT adjusted dipping to €65m and a 4.1% margin (€78m and 4.9% in 1Q2025).

“In Q1 of this year, we delivered 56 helicopters, five more than in the first quarter of 2025. Revenues stayed flat at €1.6bn, reflecting a less favorable delivery mix in the first quarter. As a result, EBIT adjusted to the 65 million euros, reflecting a solid performance from programs offset by higher R&D expenses,” explained Faury.

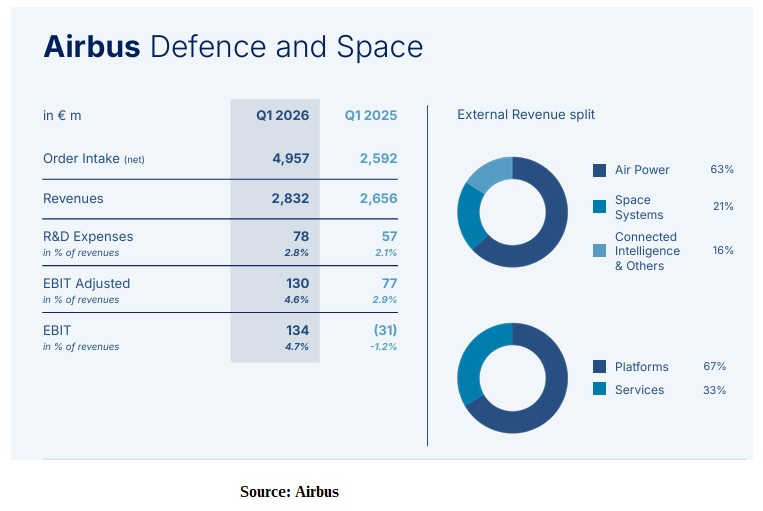

Defence and Space

The bright spot of the quarter was Defence and Space, with increased revenues and EBIT adjusted. This is undoubtedly driven by the Iran War and mounting tensions between Europe and the United States.

“We finished Q1 with a very strong order intake of €5bn, mostly on the air power side, reflecting the need from our customers for military aircraft and services,” detailed Faury.

Revenues were up €176m, EBIT adjusted gained €53m and the margin grew from 2.9% to 4.6%, during 1Q2026.

This is a welcome change for the division (and for all of Airbus), which had been a drag on the company’s financial results, in previous quarters.

Maintaining guidance for now

Despite all the headwinds that Airbus faced in the first quarter, it is holding firm to the guidance issued at the beginning of the year for 870 commercial aircraft deliveries, EBIT adjusted to ~€7.5bn, and free cash flow before customer financing of ~€4.5bn.

However, the inclusion of the Safe Harbor statement when discussing FY2026 guidance figures seems odd. It is also understandable when all the Geopolitical, economic, and supply-chain upheavals are factored in.