Leeham News and Analysis

There's more to real news than a news release.

Boeing sees 4% increase in aircraft demand in next 20 years

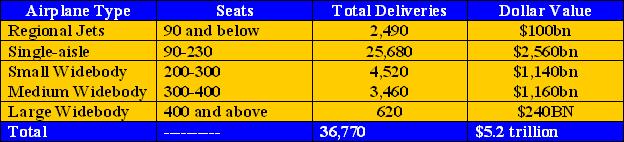

Boeing forecasts a demand for 36,770 new airplanes during the next 20 years, an increase of 4.2%, in its Current Market Outlook. The value of this demand, which covers the entire commercial aviation line from regional jets and up, is $5.2 trillion.

The company released its annual forecast today, for the period ending 2033.

As with previous forecasts, the single-aisle demand constitutes the vast majority, with a requirement for 25,680 airplanes to cover retirement and growth, the latter being driven by the proliferation of the low cost carriers worldwide. The “heart of the market” for the single aisles has moved up to 160 seats, says Randy Tinseth, VP Marketing. This is the 737-800/8 and A320ceo/neo-sized airplane. The Comac C919 and Irkut MC-21 will join this sector when they enter service later this decade.

Boeing predicts that there will be a need for 8,600 twin-aisle aircraft, dominated by the 200-300 seat sector which includes the 787-8/9, the Airbus A330 and the Airbus A350-800. The 787-10, 777 Series, 777-8 and A350-900/1000 fall within the 301-365 seat sector. The 777-9, A380 and 747-8 are Very Large Aircraft of 400+ seats.

Boeing lowered its forecast for the VLA or Large Widebody sector from last year’s 740. Of the 620, Boeing sees 200 VLA Freighters, leaving 420 VLA Passenger aircraft in the forecast. Tinseth said that although the 777-9 nominally seats 407 in three classes, Boeing considers this a medium widebody airplane for purposes of its forecast.

We asked how many of the VLAPs Boeing forecasts as being filled by the 747-8I. He declined, but separately said Boeing sees a freighter market recovery requiring a new-build of 777Fs and 747-8Fs of 2-3 per month. He previously told us he sees this split evenly between the two aircraft type. The math indicates, then, that Boeing sees a potential market for 12-18 747-8Fs per year. The current production rate is 18/yr, and Boeing hopes to eventually increase the rate from 1.5/mo to 1.75/mo. Clearly, without specifically saying so, Boeing doesn’t expect many sales of the 747-8I during the next 20 years.

(Airbus continues to forecast a 20 year sales of ~1,300 VLAPs, a forecast few outside Airbus takes seriously. The current A380 production rate of 3/mo mathematically computes to 720 A380s built during the next 20 years, a figure most observers also doubt.)

Tinseth said that 40% of the single-aisle airplanes are now being delivered to low cost carriers world wide. Forty two percent of the 20-year demand for aircraft will be replacements, he says.

Boeing forecasts that China’s domestic market will surpass the US domestic market in the second half of the forecast. China currently represents 40% of the total Asia-Pacific demand.

The table above hurts my eyes!

Not according to the figures but due to the use of JPG compression.

Please use PNG compression to save pictures with large areas of uniform colors and straight lines. PNG works without loss of information and therefore produces no artifacts like JPG and your tables will look far more brilliant. File size will even be far smaller.

Interesting. It hurts my eyes too but I didn’t know why. I learned somethign today!

Apparently not how to spell though. Sorry!

Concerning the VLAP or Large Widebody segment; if Boeing does not count 777-9’s in their large widebody forecast and they don’t expect to sell many 747-8I’s, that would imply they believe that Airbus will sell another 420 A380’s over the next 20 years.

Right?

“…that would imply they believe that Airbus will sell another 420 A380′s over the next 20 years.”

Even if Airbus manages capture half of that with the A380, it would be fairly decent outlook.

Which Boeing aircraft could cover the other half? A 747-8iNEO or a 777-10X with a folding empennage? An 80 m long A350-1100 would be more than 6 m longer than an A350-1000. A 80 m long B777-10X could gain just 3.5 m.

420 aircraft within 20 years are exactly 1.75 aircraft per month. Last year Boeing delivered 24 VLA but for 2014 just 6 until June.

What’s the likelihood that an A330NEO launch will presage an A350-1100 launch, using resources that were previously earmarked for the soon to be dead A350-800? Additionally a minimum change A330NEO now makes me wonder if the A350-1100 might have another engine, as Airbus will have more spare resources? Now GE9x would be just about right, if it will fit, does anybody know? It would also spread the risk and increase the market for GE. They aren’t a Boeing subsidiary, after all.

I think there is little pressure for Airbus to launch further A350 versions soon. In 2015 they will ramp up production, delivering them in good numbers to SQ, CX, AF, AA, UA, BA, JAL, LH, QR, EZ for 5 years, before the first 777X enters service. Discounted 777Ws and range restricted 787-10 keeping up the fight for Boeing until 2020. Some may believe the 777x is rightly positioned and just on time. Maybe it is not. Everybody is stumbling over each other to dismiss the A350-800 that Airbus decided to avoid years ago, but what about the 777-8i? A similar niche aircraft from the start?

The viability or otherwise of the 778 will depend on how much the ME 3 are willing to pay, they need it, I only hope Boeing have priced it high enough to make a profit on the ME orders alone. You would expect Boeing to be aware of the aircraft’s limited market, both A and B have been bitten with specialist LR types too many times.

“Which Boeing aircraft could cover the other half?”

– I was speaking from a very pessimistic point of view. However, if things continue the way it is at the moment, I can expect the A380 to gain the bulk of those sales.

I don’t see a hypothetical 777-10X as being 80m long. A 3.5m stretch adds too little on top of what the -9X can carry, to justify its creation as a new variant. You’re probably looking at around less than 30 seats.

There is no doubt that Boeing by itself made earlier a big mistake by introducing B747-8 without making use fully to all the techniques introduced along with B787. Moreover, Boeing repeated the same mistake and put the end of B747-8 by itself by introducing B777-8/9X.

Unfortunately, Boeing indirectly by herself assists in freeing the way totally to Airbus to play alone with VLAP sector.

Well, no VLA plane is exactly selling that well (not including the 777-9) today. Boeing probably misjudged the sales of the 747-8I, but they thought that the freighter version would carry the bulk of the program.

but they thought that the freighter version would carry the bulk of the program.

That was Plan B already, wasn’t it?

Keep in mind that jet fuel prices at the time of program launch were no where near where they are today

There was and is no market to invest the kind of bucks you are talking about. 15 billion or so if all goes right.

747-8 was simply as low a cost effort they could do to stay in the 4 engine market. Driven more by image than reality of ROI.

In short, the market isn’t worth the investment as there is negative ROI (Airbus will have to sell something around 600 A380 to break even and that may be charitable.

Take that same 15 to 20 billion Airbus invested, put it in bonds and the return would be far superior.

For the next ten years the forecast for 100 freighters and 210 passenger aircraft seems reasonable. After that, will there be a re-engine? Otherwise, the forecast is 0.

And the engines come from where ?

Current engines are sourced from 787 or A350.

Can’t use the same engines on 747 and A380 as the weight is vastly different.

NEO of either one is deeply suspect as very shallow market

A330 NEO engines seem to be roughly the right size. (A330 and A380 both have 70-72K lbs of thrust per engine.)

Aeroplane manufacturing by it’s very nature has long been innovative the industry currently has never been more vibrant or competitive.

Having presented & sat through more marketing & marketing meetings than I care to remember I can’t recall many that ultimately became accurate. The timescales involved here illustrate the potential for a high margin for error. US companies seem to be stuffed with VP’s at all levels & all departments many struggle justifying their existence, I cannot comment if Mr Tinseth falls within this category. This prediction is academic & will only be referred to when it goes horribly wrong

Jet travel has been with us for some sixty odd years & the speed the technology moves today is as fast & creative as ever. As a volume manufacturer Airbus has a thirty year history, from a boy Boeing seemingly was always there. After initially dismissing the new upstart Boeing has been forced to react. This has galvanised the industry on both sides of the pond, which is good for all of us.

Parts of the tech are moving fast. Electronics yes, EFB, ADS-B, I pads on the flight deck.

Aircraft themselves are moving slowly. Not like autos where you can re-vamp every 3 or 4 years. We had aluminum aircraft in the 20s and just starting to move past that. when a program cost 10 billion plus, you can’t come out with a new model every 5 years. That means old tech stays around a long time.

And even derivative (777x) avoid common material like Li Al, let alone a spun composite fuselage as they have no direct competitor and can get away with an inferior tech but competitive product.

Airbus has to settle for a frame and skin emulation of an aluminum aircraft because they did not have the spun tech (and Boeing may hold the killing patent on that right now if I read it right)

Its not the optimum use of the composites but it was all that Airbus could manage.

“And even derivative (777x) avoid common material like Li Al, let alone a spun composite fuselage as they have no direct competitor and can get away with an inferior tech but competitive product.”

How the 777X gets away with it is:

1) by getting an engine that’s 5% better than the TXWB

2) by resizing it above its competitor

3) by telling it’s customers to pack in more seats at 10 abreast.

Remember, the 777X beats the 787 too in CASM, even though the latter has this “spun tech”, but it’s for all the reasons mentioned above.

…and Airbus too does a single-piece barrel construction for the A350 section 19 and I believe on the A380 as well.

” Airbus has to settle for a frame and skin emulation of an aluminum aircraft because they did not have the spun tech (and Boeing may hold the killing patent on that right now if I read it right)”

A bit a Readers Digest here. The technology was there before. There’s no killer patent at Boeing. E.g. the Hawker4000 and A380 tail cone are produced the same way.

http://www.mmsonline.com/cdn/cms/Viper%20machine%20%202.jpg

I wonder if Boeing would use the same technology again if they had the choice today. E.g. for optimizing strenght, stiffness and weight in different parts of the fuselage, assembly and maintenance, the mandrell / winding process isn’t the best.

Airbus didn’t “settle for a skin emulation of an aluminum aircraft” but concluded it was the more flexible production technology after talking to everyone in the industry.

One major difference between cars and planes is that the customers and “end users” are not the same in aviation – airlines buy planes but passengers fill them. Do a cabin refresh every few years and most passengers will think they’re on a relatively new plane while the airframe itself may be decades old.

200 Very Large Freighters seems sporty. In the last 10 years, Boeing has sold 69 747-8Fs.

http://en.wikipedia.org/wiki/Boeing_747-8

Did I read this correctly? Boeing considers the 777-9X to be a medium widebody? Hard to imagine an airline that would consider the 777-9X to be medium sized.

Indeed. It would be almost like saying that the 747-400 – with a 3 class seating of 416 – is a medium widebody. Either that, or Boeing sees the realistic seat count as being much less than 400 on the -9X for most of its prospective customers.

The X in 777X, does that mean proposed, as per usually terminology, or is that the name of the aircraft like the MAX, the X?

Now that the new 777-8 and -9 models are going into production, the “X” will disappear.

It is just a hint for the airlines: only economical in X-abreast.

With BMW’s its 4 wheel drive.

The B747-8 is a B747-400 NEO, essentially.

Not really, it is a stretch and I believe it has a new wing as well

Its much more than a ‘neo’. There is a completely new wing which of course the 737 got as well.

“NEO” = new engine option. Few if any other major changes. “Option” implies the new and existing engines are alternatives.

The 747-400 went out of production at line number 1419; the first 747-8 [a -8F] was line number 1420. New wing, stretched fuselage, new engines, increased MTOW and ZFW et al. No -400 option ergo the -8 was not a NEO

747-400 vs -200? All new systems, two-crew operation, new engines, 12-ft span increase et al. Replaced the -200’s and -200F’s. Also not a NEO. The closest thing to NEO’s in 747 history was when the P&WA JT9D-7R4G2 replaced the -7Q and the GE CF6-80 replaced the -50

Mr. Hamilton,

Someone observed that a 20 year forecast has absolutely no value! We both belong to a web-site that greatly admires the A380.

Why do the primes go that far out; and what is the history of the 20 year look ahead for the commercial airline manufacturers?

I have been reading your fair and balanced reportage for years.

Just curious.

Jim Rush

Mid-West, USA

Long-term planning, such as that for the highly capital-intensive airplane/engine industry requires long-term outlooks. Boeing says it’s been doing its CMO since 1950 and tends to be conservative. Boeing woefully underestimated the demand for the 737 and 777, for example, and, I think the 747 (over 45 years, to be sure). Airbus only estimated a demand for 400 (this is no typo) A320s and way underestimated the A330.

My impression (purely as an outside observer of the aviation industry) is that there is a fundamental philosophical difference between the predictions of Airbus and Boeing. Both agree that there is going to be a huge number of people flying medium to long haul in future. Airbus believes they will be primarily carried on fleets of very large planes through major hubs, while Boeing thinks they’ll take smaller planes with direct routings. Personally, I suspect things will end up somewhere in the middle.