Leeham News and Analysis

There's more to real news than a news release.

Dissection of the 2015 Airbus order book

Jan. 13, 2016, © Leeham Co. Airbus yesterday reported 1,139 gross and 1,036 net orders for 2015, dramatically out-performing Boeing’s sales figures.

Jan. 13, 2016, © Leeham Co. Airbus yesterday reported 1,139 gross and 1,036 net orders for 2015, dramatically out-performing Boeing’s sales figures.

Boeing’s 737NG outsold the A320ceo family but the A320neo captured 67% of the sales vs the 737 MAX. The A321neo picked up 98.3% of the market against the 737-9.

Boeing dominates the twin-engine wide-body sector, posting 212 gross orders compared with 170 for Airbus. Airbus recorded a 45% market share.

But Boeing’s clear win was due to the freighter sector, with the tipping order the 49 767-300ERFs from FedEx. Boeing sold 71 freighters last year, compared with just four by Airbus.

Lining up passenger-to-passenger model sales only, Airbus sold 166 twin-engine wide-body airplanes and Boeing sold 141, for a 46% market share.

A320 Family

Click on image to enlarge.

Airbus sold 564 A320neo, or 58% of its family sales, followed by 294 A321neos, or 31% (Figure 1). Airbus predicts that over time, the A321 will account for about half the sales.

The A319 series was a non-factor. No ceos and only three neos were sold. One A318 was ordered, an Airbus Corporate Jet model. The A319neo is moving to take over the role of the ACJ and the A318, which isn’t getting the neo treatment, will be terminated along with the rest of the ceo line in about two years.

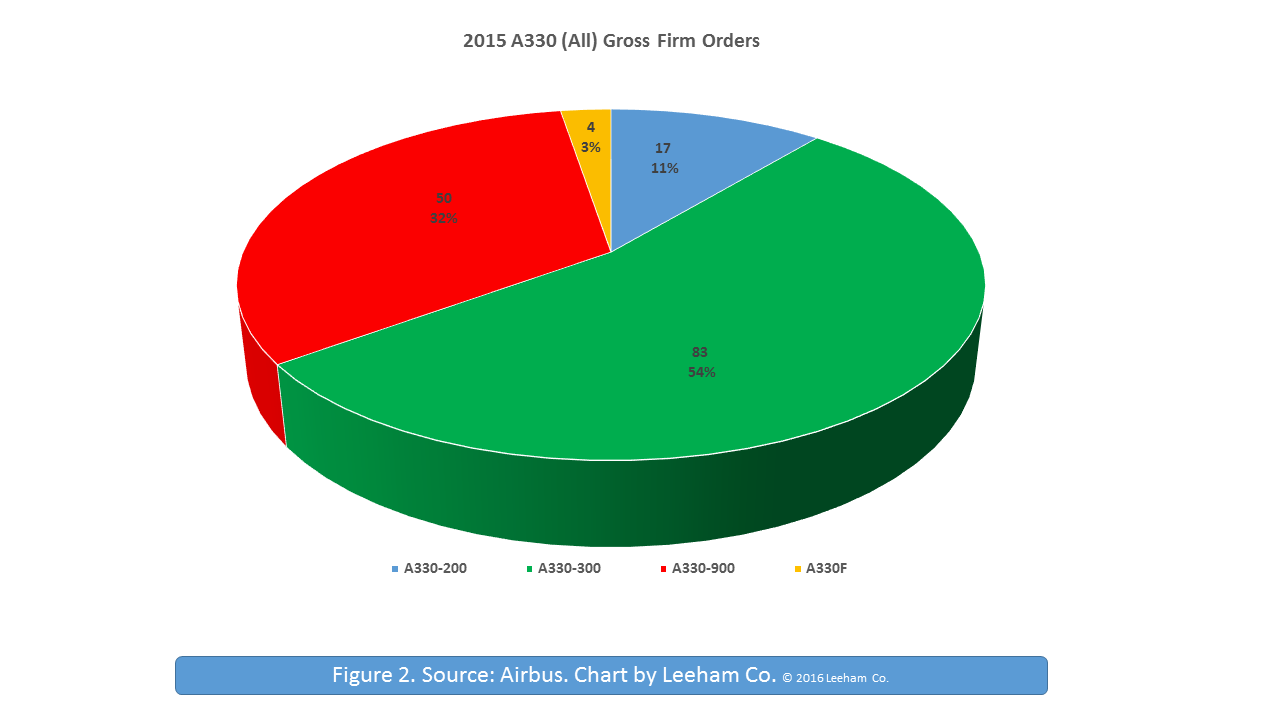

A330 Family

Click on image to enlarge.

Airbus concentrated last year on selling enough A330ceos to fill the production bridge, at 6/mo, to the A330neo. Officials said this goal was achieved and now the sales force will focus on selling the neo.

No A330-800s were sold. Fifty A330-900 orders were booked, but 83 A330-300s and 17 A330-200s were sold. Four A330Fs were also ordered.

Clearly the big Airbus weakness in wide-bodies is its freighter presence. Despite a continuing weak cargo market, Boeing’s outstanding performance in this sector—95% of the orders—remains a Boeing strength.

A350 Family and A380

A350 sales have stalled. There were 16 gross orders but 19 cancellations (in favor of the A330-900), resulting in a net loss of three orders for the year.

Officials say that one reason sales slowed was that the backlog extends to 2020 and beyond. However, Boeing’s 787 backlog likewise extends well out, but Boeing posted nearly 100 new orders (including some being the white-trail Terrible Teens).

Market Intelligence suggests that Airbus was more focused on trying to sell the A380. Little success has been achieved here. There were three orders from an Unidentified customer, but widely reported to three white tails resulting from the SkyMark Airlines bankruptcy. Japan’s ANA participated in the SkyMark reorganization with Airbus backing and it was also reported that a presumed quid-pro-quo was an A380 order.

Whether this is the case or not, Airbus now records 319 program orders. There were 317 orders at the end of 2014. One A380 cancellation was recorded in 2015.

Quote/Clearly the big Airbus weakness in wide-bodies is its freighter presence. Despite a continuing weak cargo market, Boeing’s outstanding performance in this sector—95% of the orders—remains a Boeing strength/Unquote

Both manufacturers A and B are unable to put up with any genuine freighter, one that’s built on purpose for freight logistics, based on professional Logisticians’ specifications, not some ersatz “paxliner-F” compromised adaptation to airfreighting of what originally was conceived as a passenger airliner. The consequence is that dedicated freighter operators (equipped with 744F, 748F, A332F, 777F or 767F or else all kinds of exhausted end-of-life P2F types …) are unable to compete with belly-freighters (Emirates, ANA, Norwegian, THY …) when these are computing their FTK pricing offers based upon marginal costing techniques.

Solely Antonov has developed on-purpose-designed airfreighters (Mriya, Ruslan, …) in recent times, but Antonov doesn’t PRODUCE their airfreighters currently.

The purported “success” of Boeing in this area is in reality a minimalistic score, a denial of the inherent market potential for a dedicated airvector for perishables (with reefer capability), focussing mercantile opportunity rate valuation by means of merchandise relocation to geographical areas with higher purchase power (North America, Europe, Japan, China, Korea …), from emerging economies (South America, Africa, India, Asean sub-continent …) with agricultural excedents. Concept designator : UltraFreighter

There can only be one UltraFreighter : First come, first served !

To whom it may concern ?

I’m wondering whether that’s because the freighter market is not perceived to be big enough for Airbus or Boeing to justly the investment in a freight only design. It’s hard enough for them to get passenger aircraft designs flying. Taking on the freighter design task as well could be too much.

Civilianised version of the A400 / C17? They must be looked at doing that, but nothing so far. Perhaps the airframes are simply too expensive to build as a civilian aircraft.

The Antonovs were developed with Soviet military funding. Busy though they are, there isn’t enough funding now to complete the second 225. Though of course we’d all like to see another one of those in the sky!

Military freighters are developed primarily for heavyduties or rolling stock (tanks, weaponry, ammunitions, …) or infantry/parachutists positioning, not for reefer containers, pallets, ISPF (itemised, small. packaged freight) nor for one-day-chicken, livestock, flowers, fruit & vegetables, fresh fish and seafood, valuables, high tech, machinery, fashion, pharmaceuticals etc

ICAO-registered freighters deliver a yearly 200 billion FTK, whereas the world’s containerised merchandise represent a yearly 10 trillion FTK, or 2% vs 98%. 1 % modal shift equates to 50% upsurge in ICAO statistics. The freight is there waiting for the right tool to be created, and much more new and so far unsuspected airfreight will emerge mssively based on the motto : “the tool creates the need creates the market”.

Horrors! it’s the Jevons Paradox again! See:

https://en.wikipedia.org/wiki/Jevons_paradox

And, of course, since airline freight uses a lot of energy, we must also consider the Khazzoom–Brookes postulate.

See: https://en.wikipedia.org/wiki/Khazzoom%E2%80%93Brookes_postulate 🙂

… and not sutprising at all.

Lowering the price of some required element needed for a product increases its marketability.

This works best on nonessentials. If you can make the price attractive a new market segment will open up.

what exactly do you think the Ruslan/Mriya are? they are military cargo aircraft being used to haul outsize civilian cargo.

McBoeing tried like hell to sell civilianized versions of the C-17 and failed, Lockheed has offered civilianized C-130s for decades as the L100 and has sold some, but not many, and mainly to companies specializing in providing contract cargo lift to militaries without their own or with insufficient cargo aircraft.

the dedicated ground up civilian freighter has only been successful at the very small freighter size, with the Shorts Skyvan being about as big as has ever been succesful

In all due respect, why would you spend $10 billion to develop from scratch a pure freighter, when sales, as indicated by Scott were below 100?

Yep

Same school of thought that wanted to build a water line from Alaska to California.

To the freight market experts out there! I’m wondering the following:

1) In air freight, is there a trend towards decreasing density of air shipments?

2) If Yes to #1 above, would it make sense to develop a purpose-built freighter with maximum “cube-out” capability, rather than “weight-out capability?

3) If Yes to #2 above, how different would such an aircraft be compared to a typical passenger-derived freighter aircraft?

Nicolas

The trend is in an increment to freight densities. From around 0.2 today (1 AGA weighs 6,700 kg plus tara = 1,000 kg), forwarders are eager to consign freights ever denser. Max authorised ICAO AGA MGW is already 11,300 kg (0r d = 0.3 for the merchandise). Future heavy-duty AGAs will be authorised exceptionally with MGW of up to 16.1 metric tonnes.

For the other points in your query, the revolution in airfreighter design will come in a generalisation of the AGA as the basic ULD for main deck shipments. Mriya/Ruslan are not designed for automated AGA handling/latching … besides, the Mriya flies at low cargo hold cabin pressure, proper hold pressure altitude is an option and requires special equipment. The ideal Ultrafreighter will carry 350+ mt payload, whereof 26 AGA, with minimum 4 positions reserved for heavy-duty AGAs (density = 0.34). It will be pressurised. It will rotate in ad hoc docking platforms in less than 55 minutes. Its CATK will undercut belly-freight CATK marginally costed by safe margins, making WB belly-freight obsolete.

Wild assumptions, you almost forgot to mention this ‘ ideal ultrafreighter’ is made from unobtanium.

Closely followed by nomoneyum

The freighter business segment harbours a great many talented Maddock-figures, wisely – expertly – rationalising why the UltraFreighter cannot prosper. Leaders in the exercise of these skills are Tom Crabtree of Boeing and his alter ego @ Airbus, both signing the respective OEM’s GMF/freighters (A) vs WACF (B). Both compilations are nombrilistic self-scratching rationalisations focussing an audience of Investors and Shareholders for why the freighter portfolios of either OEM cannot differ one Iota from exactly what is presently on offer … OMG do those guys have insight with their Crystal Kugl ! I’m impressed, really !

Logisticians are not fools ! Shipping people are the experts ! To sell Ultrafreighters, A and B need to penetrate the fascinating world of Shipping. A and B ignore the possibility to sell UltraFreighters in sizeable numbers, because they never asked the question in the right place !

Heres the real answer:

Looking at Fedex’s 2015 Annual report showing its aircraft purchases, which were 14 767-300F and 13 757.

Thats right their purchases in 2015 were the sort of thing airlines were buying in early 90s!

If only those pesky manufacturers would just slow down the technology/capacity to that of 20 years ago,

I have the answer!

Russia builds the Ultra thingy, Alaska provides the water and they sell in in LA!

Price if oil is going down, CA still needs water, its a natural.

Right, Transworld : http://aircargoworld.com/putin-associate-granted-cargo-contract-for-aeroflot/ … if Putin has another friend with deep shipping experience, speaking Chinese, aged 45, confirmed in Industrial Organisation, familiar with Antonov, Irkut, Migoyan, Sukhoi, Tupolev and/or similar set-ups, he’d be well advised to sign off a nice little cheque putting his friends’ ”pieds à l’étrier” to Head an UltraFreighter venture, together wih Ukrainian, Chinese, Indian, Polish and Indonesian cooperative partners. They can do it ! To Boeing and Airbus, dedicated freighter ON PURPOSE-designs are the 5th wheel of the car …

The question is how fast does it need to be. If you slow down to M 0.4-0.5 and have containers that can be pressurized a bit you can design a large turboprop Aircraft with a small cargo hold overpressurization made to take your AGA’s. The Engines will be around 10 000-20 000shp with counter rotating props close to 200″ diameter (not yet available). Going faster to M0.7 Requires modern UDF’s that are not yet available. Snecmas demon UDF fits the Power requirement. The Tu-95 Engines has the speed and Power but its German BMW Spandau design is from the 40’s. Going at M0.9 and fully pressurized is expensive and you only get 1/7th the Revenue compared to shipping pax (self loading cargo) per kg hence todays freighter volumes. Selling a dedicated cargo airline for 200T payload for up to 8hrs flights at M0.45 for 163MUD ea might be doable once new Engines become available.

Going into scaled-up perishables trading is a paradigm shift in air transport, take the example of fresh fish & seafood (airborne reefered) : 24h-slayed merchandise fetch 3 € premium vs 72h produce (trailered) on eg the Rungis engros auctions. Split the premium fifty-fifty with the fish-farmer and you have the bill for airfreighting paid up with a bonus for both the producer and the carrier. Same goes for ripe fruit brought direct to the retailer vs chill-stopped green fruit ripened artificially before sold to the retailers. Nobody is fooled : no taste, no sugar ! The added value brought to traders from a good freight vector times one year of trading pays up for the tool, threefold. The sales price of the UltraFreighter is not a problem. The problem is getting them built !

Nice idea, fewer and fewer can afford the premiums if anyone ever could.

You could easily do a pilot program with existing aircraft and try it out.

Again, no one is going to invest 10 billion in wild speculating (Wall Street aside and there is was for immediate personal gain)

Like Langlys plane, it will never get off the mental drawing boards.

Transworld, the concept is being tested and proved every day all over the world, eg http://cargofacts.com/a-long-distance-blueberry/ … what I’m aiming at is scaling up the concept to a level where it makes sense to put up with the right tooling on its own merits, so traders can stop fooling around with Boeing or Airbus paxliner-F Corgi 1/43-scaled miniatures, for a disruptive paradigm shift !

Let’s mention passing here that behind this China Cargo Airlines’ charter flight you have COSCO shipping strategists, ie not airline people at all. Shipping people are the forelopers to the 2nd Modal Revolution, already in march. ‘History’ is a winding spiral forward !

Cargo container is filled with goods as they are produced, it costs a lot less than a truck so no need to save up product and fill it later, leaves Germany, is on ship next day, 8 hours to load a modern box boat, arrives in USA 5 days later, another 8 hours to discharge, one day for customs, 1 day for delivery, total 8-9 days. Air freight/loading the truck/packing the container, customs and reversing the process in the USA takes 5 days. It’s got to be worth a lot to make the difference worth while, and belly cargo serves for most of it. Only Asia-Europe is worth while for freighter ops, not tickle my memory, where is the only significant growth in freight? Why do you think COSCO is interested? Now this is the case with oil under $30, so what happens in 5 years time?

F types are a dead end, and Airbus is lucky it is nearly out of it.

“Clearly the big Airbus weakness in wide-bodies is its freighter presence. Despite a continuing weak cargo market, Boeing’s outstanding performance in this sector—95% of the orders—remains a Boeing strength”

Looking back, the freighter business was an excellent place to be absent over the last 8 years. The desert is stuffed with potential conversion candidates. With more coming soon. Boeing ” strength” might be a liability.

http://aviationweek.com/site-files/aviationweek.com/files/uploads/2014/04/c1.jpg

Incorrect. If Airbus could have won the RFP’s, they would have. It’s definitely a sector that they are not strong in right now. Furthermore, all of the widebody freighters bought this year were available to the same audience who bought new. So there’s no liability there. It’s just a matter of preference for the need. I hope this helps.

It won’t be a liability, just not a plus (nice if you can get it)

There continues to be a balance between new and converted.

Why FedEx bought new when there are lots of 767s out there is? Someone crunches numbers and comes up with that, not a clue if they are right.

Its crunchy for everyone.

first order estimate:

used 767 + conversion + more fuel > new 767F + less fuel.

cost for conversion is known,

cost for a used pax 767 should be known.

fuel delta from pip for the engines should be known.

My guess would be the new 767F were sold for well below $50m. Hmm 35?

All true but when engines get overhauled the get the PIPs as well (may be exceptions but mfgs seem to move heaven and earth to make them backfit)

Still an F is lighter than a PAX but how much lighter and with fuel prices going South (and maybe water as well) ? NOt to mention a LOT of used 767s available in near future (feedstock is an aspect, Scott might shed some light there)

So someplace in there FedEx cruched it, now if its right or not, we will never know. They seem to have done fine with a whole lot of MD11s converted even though the first bunch were MD11F

And where were the crunchers when Boeing was making 757F for UPS? Asleep at the control column? Also who knows.

sudden U turn and retired 727s faster than a smack down and bought used 757s (some badly used) and made them into Fs. More better than a new 737F? Me thinks Boeing would have loved to give them one.

Daily utilization of course is a factor, the regionals fly less time than the internationals (777s)

Yep I’m sure they were discounted so heavily that they are probably losing money on every sale, you know Boeing…

Regardless the 767 is a pure profit machine for Boeing now so it’s hard to see how it could be a weakness for them.

When you buy an end-of-life 767F out from the desert, or you take on an end-of-life 757 paxliner to do a P2F, you have (imperfectly !) solved your planning requirements for … up to 8-10 years. The banks are backing your project fully aware of the timeline to the scrapyard !

When you buy a freighter newbuild off the assembly-line, your time-line stretches to 25-35 years. The banks are aware of the new horizon and act accordingly. A world of a difference in cash repayments !

It is tantamount to finance 25 M$ at 4 % interest over 8 years, vs 76 M$ at the same 4 % interest over 35 years, yearly repayments are of the same 4.1 M$, if you can live with that ? But with the newbuild, your spares/maintenance/fuel costs are significantly lower.

Hang on the total aircraft freighter market in 2015 was Boeing 71 Airbus 4 that according to my math is a Gand total of 75. Why would anybody invest billions in an annual market with a total pure freight requirement of 75 aircraft ?

@ Kinnear : I’m desperately trying to make the point so that you and others here can understand it Let me try once more.

ICAO-registered freighter business is composed of dedicated freighter business plus belly-freight business onboard paxliners. The second group calculated their freight rates based upon marginal costing principles. The first group cannot but calculate their freight rates based upon full costing.

As the cost levels differ like apprx 35 cents of an € per FTK for dedicated freighters vs some 23 cents of an € per FTK for the belly-freighters, or 35 % lower cost levels, guess where the traffic is going ? Belly-freight is expanding, whereas “dedicated” freighters are in regression. I’m putting “dedicated” in emphasis, because those aircraft are paxliner-F types, not on-purpose-designed airfreighters.

The Ultrafreighter will be built to a cost target of between 12 and 18 cents of an € per FTK, making belly-freighters obsolete. At this new cost level, a great many types of freight which were uncompetitive before, will start moving by airfreight. I’m talking of mercantile opportunity-driven mercandise, mainly perishables, moved in reefered AGA containers.

Man, you can’t imagine the quantities of freight waiting to be moved !

The carbon signature left in the athmosphere by present-time airfreighters (being 20 to 35 years old A300F, L1011F, MD11F, 747F … and all kinds of obsolete hence inefficient P2F types) will greatly improve when replaced by latest technology powered Ultrafreighters with the result that ITC/UNCTAD will encourage the conversion to the new modal solution.

Well of course, who knew?

I am sure old Vladmir will be happy to write the check. Let us know how that turns out.

Cleaner engines are a plot by the US to destabilize Russia.

‘A350 sales have stalled. There were 16 gross orders but 19 cancellations (in favor of the A330-900), resulting in a net loss of three orders for the year.

Officials say that one reason sales slowed was that the backlog extends to 2020 and beyond. However, Boeing’s 787 backlog likewise extends well out, but Boeing posted nearly 100 new orders (including some being the white-trail Terrible Teens).’

Is this something to do with Airbus looking to hold out for good margins on the A350 whilst Boeing has bitten the bullet, has mentally written off the development costs and is prepared to discount. the A359 is almost in a unique slot in the market and if there is limited competition then maybe Airbus is looking to make that slot pay. The A351 on the other hand has substantial competition and an unwillingness to sell at low margin may have hampered its progress against the B777-9.

Both will be looking around 2020-2 to fill a voracious production line at 13/4 per month. So at some stage both will be pricing with a view to keeping the lines humming. The right price is one at which you can sell at. Sunk costs are already been and gone.

You may be right but you could also be putting lipstick on a pig.

Sunk cost also affect the future, if you do not recover sunk costs then you have no future.

I simply do not buy that. Yes you can loose money on one program and cover it with another but you keep doing that and your company is truly sunk.

Boeing has product issues because they did not invest in the new airframe they needed at the right time.

The 737-9 is proving to be totally uncompetitive and floating or sunk cost or not, even if they sold it for 5 million if it can’t do the mission no one is going to buy it.

The right price is not what you can sell it at, the right price is what you can sell it at and make money for both the company and its future.

Sell at a loss and its a death spiral.

Fully agree with your view but where Boeing are now the only thing they can do to reduce the loss on the Dreamliner programme is to produce and sell as many as possible and get the unit production into profit

@geo

You have suggested this more than once on this forum, could you substantiate your concern about the a351 please.

Thanks

the A350 series will never match the B787 in terms of orders as long as AB is pushing the a330 neo. this has nothing to do with A359 being in a unique slot in the market or ab holding out for max profit.

Even if the 787 went well beyond the R&D budget, all those 1000+ frames will always generate some revenue for the EOM as long as they are flying.

AB should have been man enough to go with a clean sheet design, a neo will always be old technology.

From a passenger experience perspective, a330neo will never compare with the a350 or a 787.

The only purpose of a neo aircraft is for the airline to save on fuel expenses, which savings they would rather pass to the share holders instead of passing them to the pax.

Quite true, while there is some overlap between the A330neo and the A350, there is also enough difference (take the Delta order for both).

The 787 will continue to do well because it was first on the scene, and Boeing is the dominant widebody producer. (Look at big orders like JAL or ANA – they’re replacing 767s)

But this big thing here is that the 787 and A350 don’t really compete with each other. Yes they are majority carbon fibre planes, but in terms of size and mission they are not in the same bracket – the A359 and A35x are replacements for the quad-engine A340 and competition to the 777.

Yes there are those who pit the 787-10 against the A350-900, and while the large Dreamliner does carry more passengers, in terms of range it’s more of competition to the A330-900.

But overall, if you consider that Airbus sold less than 400 large, long-haul A340 aircraft (vs 1500+ for B777), the A350 project is already a success that has gained huge market share from Boeing.

Finally, to say that from a passenger perspective the A330neo will never compare to the next-gen planes is stretching things – they should also be updating the interior. Yes the windows are smaller, the pressurisation and humidity are lower.. but we’ve survived all these years with those, and it’s not suddenly going to change.

By that reasoning the 777X will also be old tech and never compare to an A350 or Boeing’s own 787?

Quite right, if you are losing the argument one must re-frame the question.

“From a passenger experience perspective, a330neo will never compare with the a350 or a 787”

2-4-2 vs 3-3-3.

And if you consider the narrower 787 cabin (vs the A350) the A330neo is the winner in my book.

Yes that extra centimeter per arm really makes a difference.

Airliners individual configurations make the difference. At least with the higher humidity, cleaner air and larger windows you will be getting that on every craft regardless of airline.

In 2016, the ethical controls of air transport – basically now merely a commodity – have shifted into the hands of air transport End Users, ie of all those who cash out the price of tickets (aka, the travellers themselves) and of people to whom aircraft and airports are their workplace, away from the Producers (OEMs and Airlines); reformulated, an airline who passes on the benefits of technological advances to shareholders and not to End Users, will be evicted from the market from the natural play of Demand vs Offer.

Modern time fleet planners apply technological advances for aeroplanes to grow in size at same trip cost then they lower prices to attract more passengers until the cabin load factor rationalises the choice of the larger, technologically more advanced aircraft. This holds also for all the WB so also for the A333 NEO, clearly. And with 222″ – 207″ = only 15″ wider cabin, the A359 @ 9 abreast is marginally less passenger-friendly vs the A333 @ 8 abreast. Consequently, A333 NEO sales feed on its specific A333 APEX content, with no or little impact upon A359 sales. What we have is a transfer of industrial manpower resources from one FAL to the other because ramp-up is restricted by the Airbus Compagnonship Rule, whereby A359 free slots are scarce, so sales deviate from one type to the other depending on which of the two has the earlier delivery. This is not “cannibalisation” but “complementarity” …

“A350 sales have stalled. There were 16 gross orders but 19 cancellations (in favor of the A330-900)”

That is direct cannibalization.

That’s a mere reshuffling of the cards on Leahy’s expert hands. Those 19 free slots sold under pressure months ago are now again available for re-marketing, to fetch harder contract sales proceeds closing terms … and watch out where they’ll end up ! At some place strategically hand-picked by Leahy to maximise the Notoriety impact of further A350 penetration !

Anyone know what happened to the Transaero A380 orders? Looks like 1 cancelled and 3 now listed as with Air Accord. Anyone know who Air Accord are?

Nice catch!

According to an Airbus spokeswoman, Air Accord is a purpose-founded company based in Bermudas. It was founded just before Transaero made their A380 order, so it seems this company was originally something designed to emulate Aeroflot’s arrangement for any non-Russian airliner they operate (which are also all officially registered in Bermudas). The reason behind this would be the significant penalty tax they’d have to pay for “importing” non-Russian aircraft.

What Air Accord are going to do with those three A380s (the 4th was removed from the order book) is anyone’s guess, of course. My hypothesis is that Air Accord as the middleman “inherited” Transaero’s order when Transaero closed shop. Down payments were made on the first three, so unless Air Accord defaults on due payments in the future, Airbus can’t simply cancel those orders. There could be some legal wrnagling behind the scenes as well between Transaero’s creditors etc. I kind of presume that the same (or a very similar scenario) is true for Transaero’s 747-8i orders, which are also still on Boeing’s books.

Some source on the Air Accord background – German only, I’m afraid.

http://www.aero.de/news-23242/Bermuda-Gesellschaft-uebernimmt-drei-A380-Auftraege.html

Well done research!

“The A321neo picked up 98.3% of the market against the 737-9.”

It is pretty clear that the dash 9s are beyond what most customers are interested in. The 738 is a very capable aircraft, but the 739 is widely disliked by frequent fliers. Some of that is the fault of how the US airlines outfit and pitch them, but I think it also reflects a stretch too far.

I think apart from MAX 739 seatpitch, the quieter spacier cabin, container/pallet capability, extra seatrows, up to 4000NM range, airfield performance and superior engine options of the A321NEO might weigh in too.

Passengers don’t know the difference. A crowded A321 is no better than a crowded 737.

$64 question is does the 737-9 have a future when the market moves up the next notch or is it simply not enough and you go with an A321 at that point?

The old 900 sold decently, be interesting to see and of course most if not all the orders offer the option to upsize given notice on the order.

+1 to this.

the -9, 321 and 757 are all horrible experienced for boarding and deplaning which next to seat pitch are the 2 things passengers are most likely to hate.

the 767 is one of the most passenger loved aircraft because the 2-3-2 layout means fewer passengers per aisle which makes for fast and painless boarding/deplaning. add the fact that being older, many are still flying around with generous seat pitches (compared to a recent 737 or 320) and you have happy passengers.

a340 is nice this way also as 2-4-2 is still pretty good and due to being configured for long range, they are usually more generous in seat pitch.

every time I get on one of these new jets with the densified seating, it is awful. if there is a seatback screen it is so close to my face I need to wear reading glasses to be able to focus on it. untying my shoes means either a hernia or a trip to the aisle, and half the time, most of the foot space is taken up by the IFE box that some moron at the seat company put where my feet are supposed to go.

There is only one door to go out of, except for larger widebodys.

twin or single aisles still have to go out that one door.

The ‘densified seating’ is a myth, you have the same width on all 747s with 10 across seating. 1/2 inch is the thickness of your fingers. The passengers are still buying all those ‘densified’ seats, and if they want more space there is premium economy and business class if you pay for it.

Last times I used an A320 with LCCs in 2015 always two doors were used for boarding and disembarkment. The call was, rows 1 to.. use front door, rows .. to .. use back door.

I had no experiences with 737 in 2015.

Generally the same, I prefer to fly short haul on LCCs as the boarding is quicker, and given that there is no difference between LCCs and legacies in tourist. Sometimes legacies can be worse in tourist as they try and make more space for business class, which probably explains why AF look like going broke, you would never fly them while you can get a better seat on Ryanair.

I don’t think it really matters whether it is A or B when looking at the LCC formats. This experience is what I suspect purgatory is (if I were a god fearing Catholic that is).

The manner in which these flights have become a truly unpleasant experience from beginning to end is quite remarkable. The seat pitch/width is marginal and the embark/ disembark process dehumanising.

I Remember the original products in Europe Ryanair/ easy jet/ go/ buzz etc etc, I don’t think I am wearing rose tinted spectacles in saying things have gone seriously downhill over time

I used the a321 frequently in the 90s, Lufthansa/ Austrian/ swissair I think. I always liked them in spite of the fuselage wobble on landing

For less lateral seat promiscuity, less hazzle at boarding/deplaning and no ombilical string attaching you to some luggage item checked in underfloor (you have only carry-on), fly with H21QR. Travellers will fight to get onboard, untypical awareness of aircraft type/seat particulars will allow the operator to collect higher ticket yields vs the (3+3)-liner next door (Product Differentiation). A definite win-win bargain !

Along with the Multi Freighter we are back into Easter Bunny and Santa Clause area again.

If Airbus or Boeing (or both) felt that concept (if you want to call it that) would give them a competitive advantage (and it would if it had any merit) they would jump on it in a hot minute.

So back to Von Doniken, anyone can spin a plausible sounding story and then trying it disprove it is beyond the resources of most of us (and not worth it for those who do have said resources)

Passengers don’t know the difference. A crowded A321 is no better than a crowded 737.

Nonsense.

Perhaps correct with a budget or AI carrier surrounded by ill informed passengers intent only on flying on their annual holiday or a weekend jolly, I can only imagine your perspective is perhaps gained from the front office.

The more knowledgeable flyer clearly identifies the inherent benefits of A’s single aisle over B’s in any guise budget or not.

The variation in this single aisle product disparity on sectors up to three hour is not often brought under question.

That being said if your flying a five hour single aisle sector it’s quite common for people to choose different carrier for the superior cabin experience that I have outlined.

I have flown 5 1/2hr single aisle and hated it until I realised it was just the lack of seat recline and no seat back entertainment. They also had two empty back rows to meet the payload /range.

Did it again the following year on a different carrier who did have such niceties.

Come on. If a traveler has 2 choices of flight to get to a destination, and one flight will be cheaper and get there at a better time for the traveler, 99.99% will choose the cheaper flight, regardless of the metal getting them there. Most travelers don’t care about aircraft typ.

Not sure, I see a lot of empty seats on 777s lately, but none on A334/340 services to the same destination. Pax are learning and it it’s only a 5% difference…. Looks like some of them are talking with their feet and wallet.

I have the choice and actively avoided 10 abreast 777 this week. I booked EK A380 instead and informed the 777 airline via facebook. Response: “but the EK flight has 10 abreast too!”

Nope,, just a poor working smuck and no, neither my wife nor I can afford to cherry pick one over the other, we take what we can with what we can afford (and trust me, Alaska is not a fun place to travel to or from if you work for a living, nearest US airport is 1500 miles so any trip is equal to half way across the US)

I have not been in an A320, she has, said max nix, the 737 was better, not because it IS better, just the seats they had vs what Frontier had were better.

Somebody hereover mentioned FedEx’ and UPS’ freighter aircraft puchase patterns (—-> 757 P2F, 767F, 767 P2F …) as antithesis to invalidate the UltraFreighter motion, but that doesn’t pan : both carriers are toying with express parcels, kurier mail and e-commerce deliveries. They are like baby children in the sandbox, toying brrrrrrr with 1/43-scaled Dinky caterpillars.

I’m talking about FREIGHT men !, real CARGO ! Wake up to the fascinating world of shipping, and consider Modal Revolution nº 2, from Triple Es to AGA-liners ! That’s for grown-ups, we’re not in the schoolyard anymore !

The yard you are in sure isnt the schoolyard!

Thanks for coming forward with your finger up to say mea culpa, dukeofurl, yes, I’ve been able to retrace those nostalgic comments higher up to yourself, about those Dinky Toy airfreighters, 757 P2F and 767F.

Sandbox recreational miniatures !

May I suggest that you dry the water behind your ears, dukeofurl !

One of the most childish things in the world is to take the make the statement the other person is childish and they claim to be an adult.

I have a beyond low opinion (keeping it polite) of anyone who pulls that nonsense out.

All right, children, let’s grow up.

Knock off the crap or I will close comments.

Hamilton

Will Air Canada replace their growing A321 fleet with 737-9’s in a few years. that would indicate they want to get some seatrows out, get rid of the container business and reduce NB flying to the Caribbean.

http://cdn.airplane-pictures.net/images/uploaded-images/2009/4/14/42480.jpg

I can see Air Canada publicly fully embracing the 737 MAX as their future NB, but somehow not doing away their 321s..

http://aviationweek.com/commercial-aviation/air-canada-turns-boeing-next-single-aisle-fleet

This was a few years back and at the time – before the fuel price collapse- they were facing bankruptcy – again. A switch over may have had immediate cash flow effects ( for Embraer fleet taken off their hands) that were specific to AC situation and not really connected to whether ‘A or B’ was a better plane.

It seems that like the Qantas LLC offshoot Jetstar, AC and its sibling Rouge will have a different fleets.

Perhaps like Australia it has would be thought of as long range domestic routes ( plus routes to US and Caribbean) and combined with heavier premium seating the 737 fits the niche quite well.

Figure 2 is interesting. With no sales on the A330-800 last year and very few sales before that, I wonder whether or not Airbus will even build the airplane. If not, that is a big hole in is product line vs. Boeing. Airbus struggled with the A350-800 as well.

AndreiX, I think in the segment where the A330-800 is, there are many good A330-200s and 767-300ER’s. With current fuel prices the pressure to replace is low.

Don’t know how many 787-8’s or 777-8’s were ordered in 2015, but I would hesitate drawing far reaching conclusions based on it.

Pingback: Airbus Group News