Leeham News and Analysis

There's more to real news than a news release.

2017, a tougher year for European airlines?

By Bjorn Fehrm

January 5, 2017, ©. Leeham Co: The last two years have seen increased profits for the airline industry. Lower priced fuel gave the industry time to breath and to finally earn a reasonable Return on Invested Capital (ROIC).

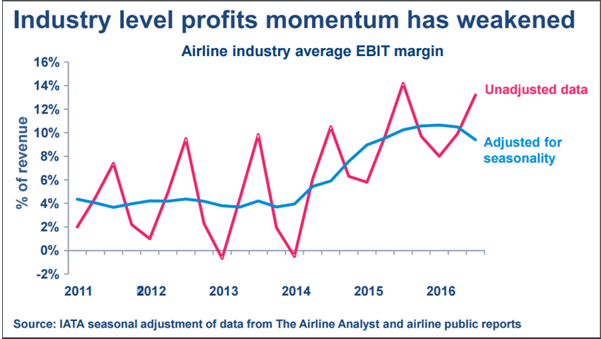

Earnings as a percent of revenue for the industry has been increasing from 5% on a worldwide basis in 2014 to around 10% for 2016, Figure 1.

Figure 1. Airline industry profits. Source; IATA presentation October 2016.

The US and European airlines have been topping the earnings with 18% on revenue for the third quarter of 2016. There are many signs this will not continue in 2017, especially for European airlines.

The European airline landscape

The European airline industry is divided into roughly three segments:

- Flag carriers which still have not managed the transition from state-owned airlines to airlines with a sound business model (Air France-KLM, Alitalia…)

- Those that have come further in the transition to efficient private companies (Lufthansa Group, IAG, ….)

- And the new airlines like Ryanair, EasyJet, Norwegian, Wizz Air….

It’s the latter group which brings the profit levels of European airlines to the levels of 18%. Ryanair is one of the world’s most profitable airline, with more than 20% earnings on revenue and 34% on capital. Easyjet operated at about half the earnings on revenue during the 2016 financial year and earned 15% on capital employed.

The legacy flag carriers have been able to turn a profit, but just. Their colleagues further down the road to normal companies are doing better, returning between 5%-10% on invested capital. But this is still miles away from the best-in-class Ryanair with 34% ROIC.

Why will 2017 be tougher?

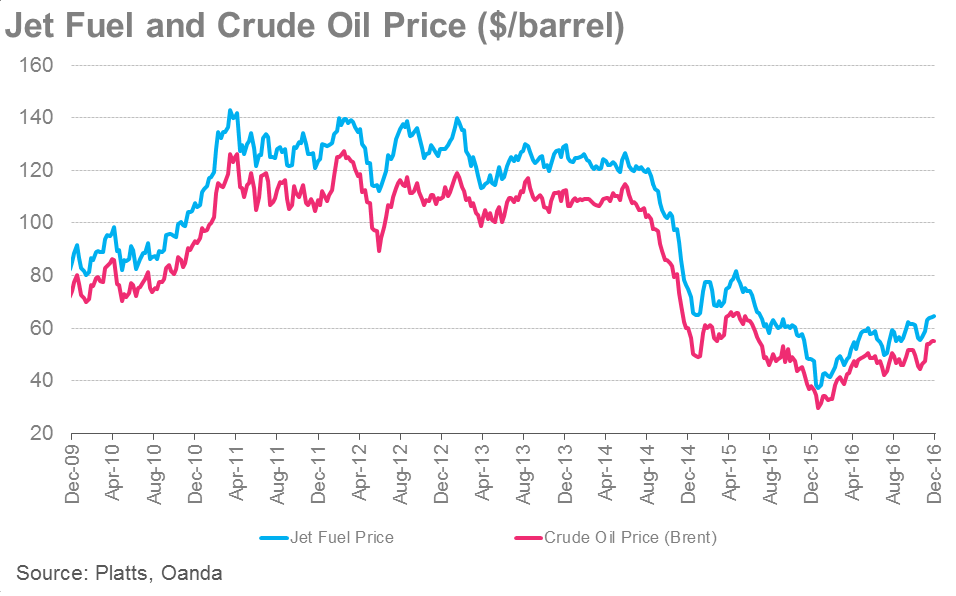

The primary reason the easy times are over is the return of the fuel prices to higher levels. It has passed $55/bbl and the OPEC policy is that is shall rise further, Figure 2.

Figure 2. IATA fuel price monitor. Source: IATA

The low fuel price gave struggling airlines some time off the hook. Now the reality is gradually returning. The effect is immediate. Airlines like Air Berlin and Alitalia are already in serious difficulty. And so is their major shareholder, Etihad Airways, meaning that there will be no more bail-outs from their major code-share partner.

The major legacy groups, Lufthansa, IAG, Air France-KLM, are all wrestling with how to counter the emerging low cost long haul threat. Norwegian Air Shuttle will fly the Boeing 737 Max 8 from Edinburgh to New York during 2017 with tickets at €65 one way says the company.

IAG will start a low cost long-haul operation, but how is not clear yet. Air France-KLM has announced it will do the same, this time as a new company tied to the group headquarters. Will the powerful French pilots’ union accept that? They haven’t so far.

Lufthansa is expanding Eurowings as fast as their touchy relation with their pilots’ union allows. The question is if Eurowings can operate long-haul successfully. So far they have messed up the destinations they have tried.

Will these low-cost initiatives get airborne and start to cruise? And will they be competitive with Norwegian, Wow Air or the Gulf carriers? This will all pan out in 2017.

With fuel prices returning to higher levels and many airlines having used the grace period inefficiently, 2017 will be a crucial year for these that did not turn the corner during 2015/2016.

The impact of legacy costs is the key issue for most of the original flag carriers and has been for many years. British Airways has been described as a massive pension fund deficit with an airline attached. What surprised me was the relatively small increase on returns that a relatively large drop in fuel costs has given rise to for many carriers. I fully agree with Bjorn’s final comment

Will resist best those Airlines who actively explore additional revenues/cost reductions concommittally in the following four directions : (1) reduce ground turn-around time to better control trip time; (2) boost revenue b.w.o. selected Product Differentiation strategies; (3) appoint freight coaches to boost payfreight contribution (cf Vueling, American Airlines, Norwegian, Delta etc …); (4) try new ways to turn IFEC into revenue (ex : contract out 44″ x 25″ KabinKino video flatscreens as “Mobilier Urbain” on-board your aircraft cf JCDecaux, in-flight instantly-monetized Visa-card shopping wiith catalogue, combined with AliBaba/Amazon 24h/48h delivery etc …).

I see two big risks to legacy carriers, not only will fuel go up but business class travel in Europe looks like taking a hit as Brexit and a downturn hit. If business travelers and traveling workers are getting pushed out of business class and economy plus then the LCCs are often more comfortable, not to say cheaper in a price sensitive business world. I pointed out in another post that if you have to fly economy trans Atlantic you might want to take Norwegian instead of BA, there is more space. It seems to be the common that LCCs have more space as they aren’t pushing to fit so much business seating.

Air travel has changed very much but the employees,especial the pilots have turned a blind eye to it. Seats crammed in to a point where a bus is more comfortable, fees for everything, and if were not for the price of oil being down,

many airlines would be going belly up.

With the influx of low cost and ultra cost carriers, major legacy airlines have no choice but to cut costs, wages and benefits.

Many travelers today only look at the price of the ticket and so Ryan air, Spirit, Allegiant, Easy jet, Frontier will continue to grow and the legacy carriers and their employees need to adjust to the new normal.

Not just the airlines but the quality of life is diminishing, medical costs rising, energy costs going up, wages stagnant. etc.

Think about it, oil is down and interest rates are almost zero and yet many countries and companies are hurting.

Those who dream of the good old days returning will fare badly whereas those who can face reality will weather the oncoming storm.

Would investment in alternative fuel sources such as refuse derived or crop based fuels be a way of getting out of the grip of the major oil producing nations? It might limit the power of OPEC to impose the unwelcome cost increases as discussed in your article. Use of such alternative sources may increase long-term fuel price stability.

Additionally, if overall CO2 emissions are reduced compared to oil based fuels (something I understand is offered as a reason for their use), it could go some way to meeting this industry’s moral and (reluctantly entered into) contractual obligations to the Paris climate change agreement. I understand that BA pulled out of a synthetic fuel production project some years ago when oil prices fell. Are they regretting that now? I have read that Virgin has started to investigate this and Fed Ex has started to actually use wood waste based fuel products, citing emissions benefits as one reason. Easyjet has produced a design study for a fuel cell based system to power aircraft while taxying to and from the runway.

How long will it take before other operators wise up to the potential benefits of diversifying away from fossil based fuel dependency? Many other major businesses are now taking the impact of their operations on the climate seriously (reference to the RE100 group, for example). It’s time the aviation industry did so too.

I have not noted any articles re environmental matters on this blog, despite the past year having been a momentous one (Paris Agreement and subsequent ratification) and also despite the aviation industry being one of the world’s major polluters. Is this is an omission that could be corrected in future articles? I would be happy to contribute.

The respite from high fuel prices airlines (and the rest of us) have enjoyed derives largely from US frackers entering the market. Saudi Arabia opened up the spigots to drive them out, and has largely succeeded as they need $60-70/bbl to make money. Prices may rise to this level, but I think not beyond or the frackers will get back in the game. There are a lot of projects on hold.

Alt fuels don’t work anywhere near this price and don’t have enough capacity to make a dent even if they did. They are a research project until there is some dramatic breakthrough.

I’m reminded of the way in which the price of wind generated electricity has fallen here in the UK. A few decades ago electricity generation via wind power was the preserve a few ‘eccentrics’. Now on shore wind generation is price competitive with the previously lowest cost option; gas generation. Prices per kwh for off-shore wind generation with the advent of new technologies (e.g. floating platforms) and mass production techniques resulting from ever larger scale schemes (e.g. Hornsea Project 2 @ 1.8GW) are falling fast. Ever increasing deployment of renewables will eventually smooth out price volatility for the domestic power consumer, as would happen for aviation if it deployed bio-fuels. The same is happening with the newer technology, solar: a 648MW plant, the world’s largest was recently commissioned in India, as that country seeks to reduce reliance on coal. I still feel that the aviation industry would benefit from recognising its role in the world and moving forward with an attitude that embraces changes and the possibilities that this brings. Fed Ex (in the example I previously quoted) has adopted a wide ranging CSR approach to its activities and perhaps that is enabling it to move forward with bio-fuels and to show others that it can be done?

“Now on shore wind generation is price competitive with the previously lowest cost option; gas generation”

No its not. The retail/wholesale price is misleading as of course its subsidised eg

“The London Array, Britain’s biggest wind farm, with 175 turbines, ….. The foundation predicts its Renewables Obligation subsidy in its first year of full operation will be £160million ”

Then you have to provide extra transmission lines to the wind farms, eg Germany has imbalance with most renewables in one area and consumption in another.

Then there is the variability of say wind which has to be backed up by thermal, where the real cost isnt borne by the renewable source but offloaded onto the thermal generation ( which is both a selectable output and maintains the frequency essential for normal grid operation)

This isnt the place to discuss this in more depth nor bring it up regarding airlines

I don’t believe any of the alternative fuel sources are even break even at this point, and don’t appear to be getting close.

Thanks for your reply fthoma. But if I can direct you to the following article, I think you’ll see that Fed Ex are using a wood based biofuel as a blend (not 100% admittedly) to produce what they call “alternative jet fuel”. It’s part of a drive to obtain 30% of their aviation fuel from alternative sources by 2030. The reason given in the article is greater price stability. To quote:

“As a heavy user of fossil fuels, we know how important it is to reduce our consumption and make trade-related energy more sustainable. Respect for our environment makes this an imperative. And reducing reliance on oil lessens the market volatility that slows growth.”

See:

http://www.edie.net/news/7/FedEx-commits-to-future-of-aviation-fuel/?utm_source=dailynewsletter,%20edie%20daily%20newsletter&utm_medium=email,%20email&utm_content=news&utm_campaign=dailynewsletter,%20c7cdeeab34-dailynewsletter

I had thought Ryanairs profitability was partly due to its airliner trading business- buy them cheap and sell them at a profit at 5 years or so. As well its likely to benefit from Irelands very low tax rates – not the standard 12.5% but the ultra low rates you can get under special deals. A quick look at their financial statements shows they are on the ‘adjusted profits’ game rather than using the commonly accepted standards.

You have to wonder about their arithmetic when they make this claim

2015 passengers per staff member 9,451

2016 passengers per staff member 9,738

Thats supposed to be +30% change in one year ![ Its 3%]

investor.ryanair.com/wp-content/uploads/2016/07/Ryanair-Annual-Report-FY16.pdf

Standouts :

They took delivery of roughly a months output of the Boeing 737 line and Total revenue per passenger decreased by 2%.

“Flag carriers which still have not managed the transition from state-owned airlines to airlines with a sound business model (Air France-KLM, Alitalia…)”

It hurts to see KLM placed in this segment with AF and AZ. They were privatized decades ago and succesfully developed into a succesfull profitable international networkcarrier, feeded by e.g their innovative JV with NWAC.

It seems the AF merge has kind of paralized the company. In the past the company was decisive and had support of employees at all levels to move ahead if needed. Trust & relations between employees and management made strikes non-existant.

Indeed, I had a recent trip from Toronto to Dubai where I flew via KLM, and returned via AF. The KLM journey was tolerable, as I flew in “economy”. The flight attendants were very pleasant, polite, and very helpful. As the vast majority of passengers were English speaking, the flight crew addressed the passengers in English, Dutch, and French. The seats were quite cramped for me (I am 6 feet tall), but I had just enough clearance between my knees and the back of the front seat to be able to move around a little (1 or 2 inches of clearance). The AF return flights (2) were absolutely horrible. The flight crew addressed the passengers primarily in French. Occasionally, the long winded (1+ minute) French message was followed by a short (10 second) English translation. As we neared Toronto, after numerous long French messages, and no English ones, we specifically asked an attendant when we would get our customs declaration form (mandatory) for Canadians returning to Toronto. The attendant was irate, and informed us that passengers had been informed previously (in French I guess), and did not want to go and get us some forms. We had to insist. Over all, the attendants were sullen, unfriendly, and unhelpful. The food was inferior to what KLM had provided. The seats were horrible! My knees were pressing against the seat in front for the entire flight (747 and 777 for KLM, 777s for AF). I could not not move my legs at all! 32 pitch indeed! NOT!. Also, several people quite close to where we were sitting were very ill with the flu. They coughed the entire 10 hours we were on the plane (8 hours + 2 hours of sitting not travelling). They did not ever cover their mouths as they coughed, and the crew did nothing give them masks or at least ask them to cover their mouths. Of course, with 24 hours of landing, both my wife and I came down with a very bad flu, and only now have finally recovered.

All in all, it was the worst trip I had ever taken, and I will NEVER again use AF.

I was surprised KLM was still flying 747s, so I looked it up and a quite a few of their fleet date from the early 90s, so could be up to 25 years old. Not the only old timer still flying, just phasing out the Fokker 70s as well , by the E175 the plane Fokker should have built years ago.

For their wide body fleet the mix of 747, 777 and A330 seems uneconomic, 787s are coming into the fleet but they have A350s on order as well. For a smaller airline like this they seem to be unable to make up their mind.

But cant as bad as the previous Swiss who ordered the Convair 990s, DC10 and MD11 which were replaced by the A 340.

Klm used to have 35 747s, -300s and -400s, mostly combi’s together with 20 M11/767s for long haul.

743/M11/767 were replaced by 777s/A330 and 744ERF’s. Now the 744s are phased out, 4 per year.

773ER’s were introduced for growth later. The 787-9/-10s will replace A332/-3’s, A350s to replace the 777-200ER fleet.

68 Widebodies in service for longhaul today.

Fokkers have been used for decades by daughter Cityhopper. Replaced by Embraers. Europe and leisure (Transavia) is done with 737s since the eighties.

Over the last 10 years, KLM has been the profitable part of the joint AF-KLM entity.

The style of internal human relations in KLM can be traced personally to Sergio Orlandini ref http://news.klm.com/in-memoriam-en/ … Air France’s executive roster has no equivalent, unfortunately (at least to my knowledge ?)