Leeham News and Analysis

There's more to real news than a news release.

Boeing charges, costs nearly $35bn since 1996

By Vincent Valery

Introduction

Nov. 5, 2019, © Leeham News: Boeing already has racked up $9.2bn in one-time charges and additional costs to the accounting block in the 737 MAX crisis.

Some expect there will be more substantial charges before the dust settles. Even Boeing officials said it will be years before all customer claims are settled. Legal liabilities are only partially covered by insurance.

![]() Program accounting, which is unique to the US, allows a company to spread the costs of an expensive development over the anticipated life of the program and the forecasted orders.

Program accounting, which is unique to the US, allows a company to spread the costs of an expensive development over the anticipated life of the program and the forecasted orders.

Other countries require unit accounting or charging off costs as they occur during development.

Boeing is one of few companies in the US to use program accounting. This masks current charges in the GAAP-approved financial statements. A few years ago, Boeing also began reporting non-GAAP numbers on the basis of unit costs as additional information.

With one-time charges and added costs to program accounting assumptions related to the 737 MAX grounding, Boeing’s accounting policies are back in the spotlight. The accounting policy became controversial as deferred production costs spiked on the 787 program.

As commercial and defense programs faced cost overruns and delays, the company had to record billions of US Dollars in charges and various losses over the years.

LNA went through all of Boeing’s annual 10-K filings since 1996 to identify all the charges recorded on commercial and defense programs.

After recording billions in charges since Dennis Muilenburg became CEO in 2016, we assess whether there is more to come in future quarters.

Summary

- Program Accounting fundamentals;

- Dreamliner Deferred production cost controversy;

- Billions in (not so) one-off charges;

- Current and future charges under Muilenburg’s watch.

Unit-Cost accounting on commercial aircraft programs

Most industrial companies use unit-cost accounting. Under that methodology, the firm assesses the cost of producing every single unit. The profit on a given production unit is then:

Profit = Sales Price – Production Cost

If one uses such methodology for aircraft programs, the following usually happens:

The first units coming off the production line are expensive to produce. Those units require substantial rework and more man-hours. Combined with discounted pricing for launch customers, the company records hefty losses under the unit-cost accounting methodology.

As the assembly line gains in efficiency, unit production costs come down substantially. The company records larger and larger profits until the demand for product dwindles.

The first units in a production line usually cost more than three times the mature cost. The production line becomes cash positive typically after 200-250 units, while the line reaches mature costs at 400 units.

Program accounting 101

Boeing elected to use to program accounting in 2003. In a nutshell, this is how it works.

When aircraft deliveries start, the company makes an assumption on the number of units it expects to sell: the accounting block. The company also assumes an average production cost for all the units in the accounting block. The average production cost is set, so the company earns a standard profit margin on sales.

The profit on a given production unit under program accounting is then:

Profit = Sale Price – Average Production Cost

However, the company needs to record deferred production costs for the entire program. The contribution of a given unit to deferred production costs is:

Change in Deferred Production Costs = Production Cost – Average Production Cost

During the early part of the program, deferred production costs go up. The first units are more expensive than the average over the program. As the production line becomes more efficient, the units become cheaper than the program average. The company can recover the deferred production costs.

If production costs materially go up or the program accounting quantity shrinks, the company needs to record a reach-forward loss. In practice, this means the firm does not expect to recover all the deferred production costs on the program entirely.

Program accounting effectively smoothens earnings. Earnings recorded in early delivery years will be higher than under unit-cost accounting. Conversely, they will be lower in later years to recover the deferred production costs.

One should note that deferred production costs include the cost of producing the aircraft themselves, as well as the amortization of production tools and non-recurring expenses.

Controversial Dreamliner accounting

In spite of deliveries starting 3 ½ years late, Boeing hasn’t booked a single charge related to the 787 program.

How is that possible?

Some tests and early production units Boeing proved too problematic to sell. Instead of recording a charge, the company flushed them into Research and Production expenses: $2,693m in 2009 and $1,235 in 2016. This reduced deferred production costs by the same amount.

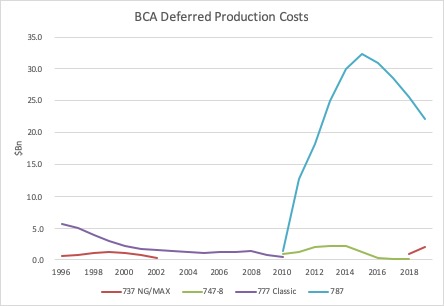

However, the main controversy was of a different order. Below is a plot of deferred production costs on major commercial aviation programs since 1996:

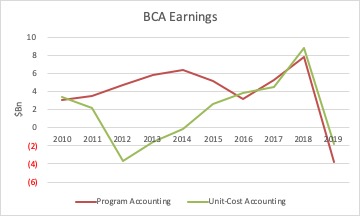

As well as the earnings in the Boeing Commercial Aircraft division under Program and Unit-Cost accounting since 2010:

As one can see, the magnitude of those costs went through the roof on the Dreamliner program. They peaked at $32.4bn at the end of 2016. The highest level on another program was $5.6bn on the 777 Classic in 1996.

Under Unit-Cost accounting, BCA would have lost more than $5bn in 2012-2013. The accumulated difference between Program and Unit-cost accounting was $22.3bn over the 2012-2014 period.

The costs of the 787 program delay materialized in deferred production costs. The first aircraft were stored for extended periods and required substantial rework.

Boeing has dodged the reach forward loss bullet so far due to a strong demand for the aircraft. As of Sept. 30, Boeing still has $22.1bn of deferred production costs to amortize over 706 units in the 1,600-strong accounting block. On Sept. 30, there were 556 787s in the backlog. Boeing announced with its 3Q2019 earnings call that it will reduce 787 production from 14/mo to 12/mo late next year due to soft demand.

The total cost translates into $31.3m per aircraft. Year-to-date, Boeing managed to reduce deferred production costs by $31m per delivery. If demand and production stars align, it is still plausible to fully recover those deferred production costs.

Dozens of billions in charges

If we include the 737 MAX earnings charge, increased costs in the accounting quantity, provision for Jet Airways, and litigation charges, Boeing effectively took $9.85bn in charges year-to-date.

Charges are not an anomaly in Boeing’s history. Below is a plot with charges recorded every year since 2000. We also include the net earnings declared for the year.

We excluded charges related to accounting changes, as well as retirement benefits. We included the 787 aircraft expensed into Research and Development mentioned before.

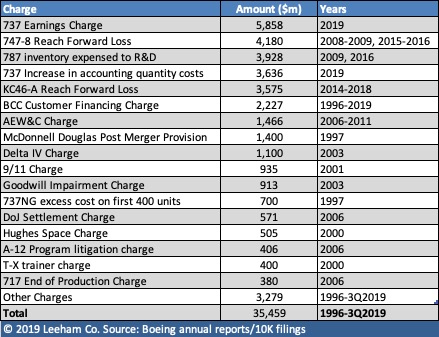

As one can see, Boeing recorded significant charges since 1996. The accumulated amount of those charges is $35.5bn. As a point of comparison, Boeing declared $76.7bn in earnings over the same period. Accounting for corporate taxes, LNA estimates that net earnings would have been at least $20bn higher over the period.

Below is a list of all the charges since 1996 above $375m:

And more to come

Boeing has recorded $15.8bn in charges since Muilenburg became CEO in 2016.

While the 737 MAX has gathered most of the attention, Boeing is in trouble with the KC-46A program. Muilenburg’s Capitol Hill testimony included grilling on the military program from Rep. Garamendi.

Deliveries are running late. Elements of the aircraft, including the refueling boom, need rework. Delivered aircraft had foreign debris. Also, the aircraft cannot safely transport troops or cargo at the moment. Boeing hasn’t declared another reach-forward loss on the program this year, so a new one is likely in the next few quarters.

But these aren’t the only challenges facing Boeing.

Other defense programs declared charge in 2018: $400m for the T-X trainer and $291 for the MQ-25 Stringray. The Mars SLS program is late and over budget. AWACS upgrade and AEW are running into technical issues. More charges from these programs are likely.

Of the $9+bn in charges on the 737 MAX, $3.6bn are in the form of increased costs in the program accounting. Those charges will result in lower profits on delivered aircraft going forward.

One should also expect a spike in deferred production costs on the 737 program in the next few quarters. Boeing already incurred sizable storage costs. The company will also hire scores of temporary workers to resume deliveries as fast as possible once the FAA lifts the grounding.

The last 747-8 deliveries will likely happen in 2022. More orders are unlikely. Boeing recorded $380m and $184m in charges for the closure of the 717 and 757 production lines, respectively. One should expect a charge of similar magnitude when the company announced the end of the Queen of the Skies production.

There is another elephant in the room.

From cash cow to future earnings drag

It is no secret that the 777 Classic made an outsized contribution to profits at BCA while the company was sorting out 787 production issues. Boeing was hoping the 777X would continue this.

As outlined in a recent LNA article, demand for the 777X is likely materially less than Boeing envisioned. Boeing launched the program on expectations of 1,200 demand for very large aircraft. GE Aviation used that forecast in its public presentations.

The Boeing Internal Product Development forecast was 700-800. LNA estimates that the number is down to 500.

Some order cancellations from the Big Three Gulf carriers still need to be announced.

Boeing acknowledged in the 3Q2019 earnings call that deliveries would start in 2021 at the earliest. Testing is delayed, mostly due to durability issues with the GE9X.

Just like the 747-8 10 years ago, the 777X is facing a slump in demand for very large aircraft. Boeing recorded $2bn in reach forward losses for the 747-8 in 2008 and 2009. The losses were partially due to engineering resources diverted to the 787 program. Boeing booked another $2.1bn charge in 2015-2016 due to low demand.

With the delivery delay and uncertainty surrounding the 777X certification campaign after the 737 MAX debacle, Boeing will almost certainly book a charge in the next few quarters.

However, the hammer will fall when deliveries start. Boeing will have to announce the accounting block and production rates. With demand lower than Boeing envisioned, both will be lower.

If Boeing produces three units per month, it could take several years for the production line to become cash positive. Like with the A380, there might be not enough demand for the production line to reach mature costs.

The lower demand will translate into higher average production costs than at the time of the launch in 2013. Since Boeing is spending at least $5bn to develop the 777X, a multi-billion charge in 2021 is possible, if not likely.

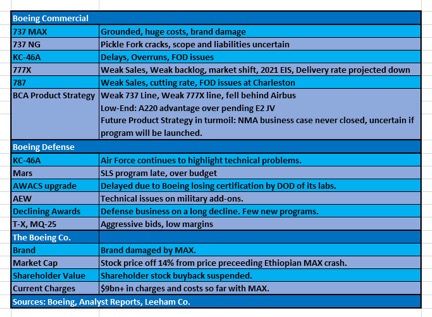

Conclusion: 737 MAX grounding exposes weaknesses

The third quarter of 2019 revealed how critical the 737 is for Boeing’s profitability. Revenues in the Commercial aircraft division were down 41% year-over-year. Instead of recording $2bn in profits, BCA recorded a small loss.

Deliveries of widebody aircraft were marginally higher year-over-year: 57 (one 747, 10 767s, 11 777s, and 35 787s) vs 52 (two 747s, four 767s, 12 777s, and 34 787s). On the other hand, Boeing handed five 737s vs. 138 the previous year.

The narrowbody accounts for close to 50% of revenues and an even larger share of profits. A permanently damaged 737 MAX brand would significantly hurt Boeing’s profitability for many years.

Regardless of the 737 MAX crisis, more accounting charges at Boeing aren’t a matter of if, but a matter of when. High profitability on the 737 program in previous years almost kept those charges under the radar. In the future, not so much.

A well written article.

Just how much trouble is Boeing in?

Its hard to see the light,whether one looks at space,military or commercial aircraft arms of the company.

In two of those areas they have relied on the ever present gov’t ( taxpayers) money.Thats over for the space deivision and looks increasingly shaky in military.

As for commercial aircraft……

They really need a new CEO and mindset.It will most likely take many years.

Would be interesting perhaps to see someone write an opposing view that offers a more optimistic outlook and see how it stacks up.

You’ll see Churchill’s (attributed) observation reinforced for some more time to come, me thinks. 🙂

https://winstonchurchill.hillsdale.edu/americans-will-always-right-thing/

Things aren’t down in flames yet.

Great article, simply BA’s accounting treatment is designed to hide rather than illustrate the true nature of their financials. Program may have a place but the arbitrary nature of the accounting block and the random use of charges makes it meaningless.

The use and abuse of program accounting is just a means of dragging profits to earlier years and mask the upfront costs of developing aircraft. This has made sure that the executives are able to book profits earlier and pocket their juicy bonuses but the drag of amortizing the costs will be felt for some time. Add in the multiple charges it could be argued that they have serially understated the development costs across the board. Combine the two and BA accounts are at best a mess and at worst a cynical ploy to provide shareholders with a less than prudent view.

Some countries accounting systems works a bit like Boeings, as you take large depreciation costs continiously even when the equipment is fully written off, that way you speed up the replacement cycle of equiment as it still cost alot to have the old stuff in your books. New Equipment to replace the old should be faster, better quality, safer and smells better.

Nothing wrong with that at all, when I was a callow youth I worked for a Swiss Multinational that charged ‘superdepreciation’ I think it was called. To my understanding that is almost the polar opposite of what Boeing is doing

Never got into the finanacial but this has aspects of a Ponzi schme to me.

In short, as long as things go well (be it more and more invesors proppig up the ones with the good current takeout) or in Boeings case, great sales.

But as noted, the 777x while not a flop, never looked to me to sell like the 777-300ER.

In the Auto Industry the only way that worked out was pickups. Huge sales and huge profits.

Any car they ever up-sized (Mustang) sold fewer and fewer and never got the profits the mass sales did.

In this case Boeing did not fill in below (VW up-sized tghe Passat but made the Jetta bigger) – no fill in under the Mustang ever hit its popularity.

So now a double whammy, self inflicted MAX (which will be gotten over but the hit is there) and the 777x I think is much lower sale or as noted it could die off the way the A380 did (not sure I would write the 747-8F off yet)

I think the intent is to point out its great to fool yourself as you can come in, make your 10s of millions and then run rather than face your failures.

What was missed was stock buy backs as that massages the third wheel of the scheme. All that money that should have gone into new products.

Amazing and I have no hopes it will change.

The 777-9 is unproven. The 777-300ER is a “trick of all trades pony” and does many missions it was not really designed for pretty well. It killed the A380 and 747, forced Airbus to redesign the A350-1000 by being large enough, lots of range and sturdy enough for shorter range flying. Boeing hopes the 777-9 is as good and durable while delivering similar flexibility, increased size and customers will choose it over the A350-1000. We will see after the first few 1000 flights if Airlines makes good profits flying her and if she is more durable than her French cousin with its British engine.

It is a way not letting managers keep old products too long squeezing profits after all devlopment costs are paid and you squeezed suppliers and swapped them out making big profits at the end of the production run, Boeing does it half way by setting the profit at an average value from the start assuming cost reductions over time. The 787 is a good example when those cost reductions came in a tad late due to all new technology, but they came and are now saving Boeing commercial aircrafts

‘In spite of deliveries starting 3 ½ years late, Boeing hasn’t booked a single charge related to the 787 program.’

I could be wrong but didn’t they write off some of the early frames in a charge once it became clear they were worthless? Not that it detracts from the articles main point.

Reassignment only.

Initially the “ZeroSeries” frames were intended to be sold, handed to customers. Their cost was thus assigned to production outlay. of to the deferred cost basket.

run of things changed that to unmerchandisable. About a $1B moved over to R&D afair?

Fixing the Terrible Teens at rather high cost and massive amounts of work time instead of just scrapping them was based on deferred cost metrics IMU.

There is actually much more than just deferred cost accounting in US GAAP to make it special in a quite distorting way.

US GAAP is said to give 4..8 % “better” reporting than the frameworks used elsewhere on the globe.

The massive tax write off avaliable for R&D out weighed any net gain after remedial work was done.

Sower: reclassified as R&D, as the article says, but no write-offs.

They probably dismantled them and reused valuable components … recovering some % of the costs ??

Sorry Scott, I noted that after posting, I supposed R&D sounds better than a write off

Thank you Vincent for adding up the number we all want to avoid. Avoid because we want to see a vibrant, balanced competitive market place for the airlines and supply chains.

Reading through your article, my conclusion would be short term results were King and processes and accounting, investments and strategies became slaved by that corporate strategy.

Promoting, deferred costs, streamlined selfcertification, grandfatered

requirements,

keesje – not ‘ a vibrant, balanced competitive market place for’ shareholders?

They reassigned early production fames to development costs as opposed production costs. So out of one column into another column.

The reason, nobody would buy early production frames.

No, the reason they would not buy them was they were so hosed up build wise they could not sell them.

Cheaper to give someone a LN 80 x 787-8 than fix the ones they had to standards.

Not that the repair crews would not have had a lot of fun but only something like Ethiopian Crown burned 787 was worth that sort of effort. And even that one I expect was a research case and tech test of real world damage not one up bring up to standard.

Transworld – how do you think ET crown-repair cost was covered/accounted for: insurance or research..?

Eventually most were sold, outside of 2 static test frames and 5 donated or scrapped by Boeing , all the rest had owners eventually. Mexican AF has a nice presidential jet along with 2 others as BBJ. Others of the early ones went to ANA and JAL and some to Ethiopian.

Boeing need a new CashCow= Competitive NarrowBody, FSA, yesterday.

How can the #1 stake holder, the US government, support this? The usual portfolio I guess.

– Condemn Boeing certification, blame FAA (-> compensations)

– Fire (buy out) Boeing board, forget

– Inject $10B tax cuts, “level the playing field..”

– Fund NASA research pushing required techn to TRL 7 asap

– Import restrictions to ensure 737 soft ditch / turn over FSA

– Publicly hammer WTO, Airbus should stop unfair pratices

The massive tax write off avaliable for R&D out weighed any net gain after remedial work was done.

Sudden requirement for 200 737 MAX for the airforce. Also new non stealth smaller tanker design which must be capable of transporting 200 passengers.

Grubbie – is that cycnical, or what? You are obviously a student of human nature…

All effective reactions that could help BA remain afloat, but what happens when more people/astronauts die because of non-financial issues entrenched at Boeing? Most people in the media seem to forget that more than anything, a serious lack of competence is what is staring us in the face here. This ineptitude exists equally among the rank and file engineers (hired/transplanted since the merger) as well as among management. No mater what Boeing/FAA/US government does about this mess financially, that lack of competence (both technical and leadership) would be the gift that keeps giving. Physics of a bad products cannot be “deferred” indefinitely. Reality of a badly design/manufactured airplane will come home eventually sooner or later. Same could be said about bad product strategy.

It looks like you are right, but there are skilled engineers around Boeing and not yet in the right positions. Just look how PWA Commercial jet Engines kind of pulled itself in the hair and came back after Congress/USAF life support. PWA will soon be on the green side with its PW1000-series after a few 100 more SB’s.

@claes

Absolutely agree.

P&W’s resuscitation is an excellent example and exactly what is needed at Boeing. Bringing P&W back to life required major re-ranking and re-training of the staff – great many in upper/middle management were terminated or demoted. It did not happen without some major internal tensions; many eggs were broken to make that omelet. furthermore, P&W had to admit to themselves that they had a competence problem (which is the hardest part, culturally). As of late, Boeing seems to be in denial about the competence issue at the core of this… As far as the current regime is concerned, Boeing’s business model relies mostly on heavy-handed legal and political action to grease the gears of business, as opposed to designing and manufacturing good quality/competitive products. Until that philosophy changes, debacles like the MAX may be a reoccurring theme, unfortunately.

Great article. Thanks!

Anyways, after reading this article, I believe that if Boeing is to remain viable it needs to begin a New Aircraft Program within a year – and this program has got to be financially successful. However, given Boeing’s latest experience developing the 787 the 737 Max and the KC-46, I just don’t think Boeing can do it. Seriously, since the Ptoemkin-village 787 Rollout of 2007, it’s been one aircraft-development fiasco after another. Failure is new normal.

So, do ya’ think the Boeing executives are gutsy enough to “Pull the Trigger” on a new aircraft program? Considering that the development and deferred costs combined of the 787 Program had to have exceeded 50 Billion Dollars I’d say they would have to be pretty gutsy – or cunning enough to not be around when the aircraft is fielded so someone else can take the blame. I can’t wait to see how it all goes down.

I’m sure there is more than enough talent, experience and guts in many clever people at Boeing. The question would be how to bring them to the steering wheels.

Valery, does Airbus also book these deferred Production Cost, and are their Tax Authorities allowing for the same treatment as in the Boeing’s case. Shouldn’t the WTO also be looking at these areas?

Airbus accounts on IFRS rules.

Losses/outlay when they occur.

Profits when they are “realised” i.e. the product is paid for.

Conservative valuation of assets.

i.e. as an example you can’t value in stock stuff ( finished or semi finished ) at accumulated cost like Boeing seems to do.

Why would the WTO care how accounts are prepared? Airbus typically looks to book costs as they are incurred, have said that there are specific instances where thy match costs over time or to production but at a far lower level than Boeing. the A380 may have been a financial disaster but this has little impact on current Airbus financials as the hit was taken in the main many years ago.

Build a new aircraft? I personally doubt it.

If for no better reason than the accounts so elegantly presented in this article.You can defer sunk costs but they will never ‘dissapear’.

After 5 years of hawking the MOM it has become increasingly clear that whist there may be a small gap in the market there is no real market ($$) in the gap.

Had they not bothered with the 737-10 and now a dash 9er to cover the longer ranges – then perhaps yes but they have really committed themselves to the MAX route now imho.

If Boeing was a “Ponzi scheme” (as has been alluded to), it would’ve been done as a company decades ago.

Boeing generates BILLIONS in free cash flow. Repeat- Boeing generates BILLIONS in free cash flow. Even adding all its costs, expenses, fines, compensation, etc. Boeing somehow returns BILLIONS of dollars back to shareholders. There is nothing “Ponzi scheme” about that.

Also of note, the majority of Boeing’s revenues and profits is from its commercial aviation unit, not its military. In other words, it simply doesn’t rely on “government contracts” to keep it functioning as a company.

Some people simply want to make stories or believe in something which doesn’t exist. Occam’s Razor is best served here.

I have to disagree and I don’t allege, I flat out feel it is.

Granted its a legal ponzi scheme.

What they have been doing is kicking the plane down the runway (in aircraft terminology)

Like a Ponzi scheme, if it all goes right, it goes on for years.

Sooner or latter there is a hiccup, suddenly you don’t pay the investors what they are promised and it crashes .

Boeing has gone way out on a limb as was noted not just on the 777X but on the TF-X trainer, the Navy Tanker and the KC-46 keeps cropping up in negatives.

Is Boeing going down in flames? I don’t think so. Can they hit the skids severely? Yep. How bad, as all this comes due in the same time frame, pretty bad.

The only program I can think of that is returning well is the 787 (just cut production ) and the 767 F (and those numbers are small)

Huge loss leaders for a long time at best and if they can’t execute a KC-46, how is the TF-X or the Unmanned Fueler going to go?

They claim the move to digital production saves it all.

Massive Baby Boomer retirements coming (a lot like me, maybe I don’t have the moon but will get by and I just quit) that is going to have a massive impact all across the mfg sector. No one was any where near as good as I was at what I did and knew, let alone for what I got paid.

But they hosed MCAS and the KC-46 and that is dead nuts simple stuff in aircraft terms.

Of course, according to Boeing enthusiasts who used to be members of the Fleetbuzz posting forum, everything’s still seems to be honky dory at Boeing.

That being said, all critics of Boeing that are commenting in this blog should show some restraint in their criticism of the company. Since Boeing is obviously going through tough times and could risk being enveloped in an existential crisis, this is not the time to step all over them.

Huh?

Don’t kick someone when they are down — got it?

–

http://www.bobdylan.com/songs/positively-4th-street/

https://www.youtube.com/watch?v=aehwEu8SBSo

I see this sentiment appearing everywhere. Airlines, analists.. the desire to present a balanced picture of an unbalanced situation.

The question is if this relentless hammering of Boeing and its failures is bringing something new to the table.

Amen my friend.same people day after day.I have no dog in hunt, but just same old same old.

I don’t really see “relentless hammering”.

For the s*t they’ve done over a longer period and in scope of the monomaniac drive behind it

I’d judge the current style of dissemination as “mild”.

you’d see “relentless hammering” if it were a foreign entity and for a much lesser trespass at that.

cue : Toyota, Shell, VW.

@Uwe

I’m talking about the social media commentariat and on what’s being said about Boeing in the blogosphere and/or in comments sections in blogs, online newspapers (etc.).

Thus, I’m not talking about the pontifications of pundits who operate within major U.S. based news organizations; nor about what U.S. politicians, U.S. based lobbyists, America Firsters (etc.) are saying — you know, the ones who were taking aim at Toyota, BP, VW (etc.).

“The question is if this relentless hammering of Boeing and its failures is bringing something new to the table.”

So what?

Let the Hammers keep falling, and when Boeing has had enough, then maybe they will change and do the right things. Until then, Boeing doesn’t need your help, and they don’t need anyone’s pity. And furthermore, Boeing sure as hell doesn’t need someone “Bringing something New to the table”, as you phrased it: Boeing Execs know right from wrong – and if they don’t, then they are a bunch of Psychos.

Did you read about what that empty-suit of a Boeing Board Chairman did yesterday? He gave his unqualified endorsement of “Dennis the Menace”. That ain’t Progress: that’s Pathological (it’s.almost.Psycho)!

Keep swinging those Hammers!

@Jimmy

I’m not out to “help” Boeing. I just find the relentless hammering repetitive, and frankly, quite boring.

As for “bringing something new to the table”; that was more about possibly directing more of the hammering and criticism towards the current U.S. economic system where Reaganomics appears to have run amok — that corporatism in America, in fact, seems to have long since reflected the basic beliefs, values, and norms shared by a majority of Americans.

@OV-099:

Hmmm….please quote where those ex-members are posting everything is “hunky dory” at Boeing. Thanks.

That was written with a sarcastic intent — sorry, if that didn’t come across. 😉

BTW, the “chief analyst” has been rather quiet lately.

@OV-099,

Great we got it cleared up. 🙂

@ jacobin777

Any Ponzi scheme returns large sums of money to its investors as long as it lasts. Recall Bernie Madoff; in his case it took almost 30 years for the scheme to fall apart. Also, he was not always a Ponzi, he became one late in his career in the mid to late 1980’s. I agree that Boeing in many respects operates similar to a Ponzi scheme, but it enjoys certain legal immunity from the generally accepted accounting rules that allows it to kick the can down the road (for the foreseeable future). Perhaps being unique in that sense provides value to the shareholders as a safe heaven stock?

Ponzi schemes at some point in time end. Boeing as a company is 10x more scrutinized than Bernie Madoff ever was. Its not even a remotely close to “like-for-like” comparison.

Does Boeing have problems? Certainly and I’ve been openly critical of Boeing management on their decisions(at least on other websites).

I don’t drink the Boeing “kool-aid” and I feel Boeing’s BOD has done a great disservice to the company by allowing the Muilenburgs and McNerneys and other CEO’s of Boeing to “run amok” without holding their feet to the fire (not to mention their absurd compensations).

Ostensibly, it seems people can’t simply understand (or want to accept) that while Boeing has “screwed-up” big time, they have done tremendously well as a company – at least when it comes to revenues and profits-something which a Ponzi scheme inherently can’t do.

Boeing isn’t anything like a Ponzi scheme. But one part of it’s cash flow won’t he holding up in the years ahead. Thats the deposits and other payments airlines make in advance of delivery. The massive order skyline, sometimes 5 years and more ahead has been very lucrative in getting advance money to offsetting the charges detailed above. When it reduces there goes the cash flow……maybe this is one of the reasons for NMA hesitation, not so much development costs but the first 400 planes sold well below cost just the other profitable planes cash advances drops off.

@Dukeofurl,

You might be correct however we just don’t know.

MAX:

https://www.reuters.com/article/us-boeing-737max-easa/boeings-max-likely-to-return-to-european-service-in-first-quarter-regulator-idUSKBN1XE1U1

Good spot TW.

I can’t quite square the optimism of the headline with the content of the article. Seems to me Ky is saying that the earliest it can be back in European skies is Q1 2020, *if* all goes well. Yet the headline makes the assumption that it *will* all go well

Thank you.

My take is I am just handing out and waiting to see what happens.

There has been so many is a done deal to , ooopps, we have to work some more that I don’t think there is any way to know.

Cross integrating the two computers would seem to have been a much more major task. But maybe they had preliminary work done and just had to execute it.

FAA may act sooner and some strong indicators would emerge there from the critique

And hanging out is the manual trim issue. Another hard call as its been allowed for all these years.

It is a hard call in the US for the FAA, but the EASA can do it as they’re not the primary certifying body for 737. And as they’re not politically accountable it’s no skin off their noses how much chaos it would cause.

It has indeed become a waiting game, I’ve learned not to trust any projections or predictions about what’ll fly and when it’ll do so.

For me the bigger issue is that it’s clear that a major world OEM has been doing it wrong for a long time, and it’s necessary for that to be put right or for them to be put out of the business. Putting it right likely means scrapping all their current designs ASAP (could be a while though) or doing a full recertification of them. We just don’t know what gremlins there are in the design and manufacturing. We do know that the current certification system failed to spot some issues before two disasters. If they don’t start at least actively looking, I ain’t getting on board one of their planes.

If the FAA and Boeing don’t start moving in a proper direction then we are going to be looking at more disasters.

Only this morning the BBC has an artic about 787’s O2 system. https://www.bbc.co.uk/news/business-50293927

Yep, 777, 767, 787, 747, falling out of the sky left right and center.

“” it’s clear that a major world OEM has been doing it wrong for a long time, and it’s necessary for that to be put right or for them to be put out of the business “”

They have to do it right but then Boeing is not competitive.

Now the MAX won’t fly without simulator training. No training was a big point why airlines bought it.

On the ET302 report the OEW was mentioned, 47090 kg. No wonder Boeing is hiding its bad OEW.

The economic numbers are not good too, that’s why Boeing tried so hard for a big fan diameter, but could not reach what Airbus could.

So why would airlines buy the MAX now, it won’t be so cheap that it is worth it. The compensation Boeing is offering is dreck. On top of that airlines have to deal with a bad reputation. Not east to find flight attendants, especially in the US. Nothing to earn with the MAX.

Frankly – what is the cause of “all this” ? …. SIMPLE

An high-tech engineering company run by financial people and lawyers who understand and care only about those two things – and we can see/hear it in any statement made by any BO official.

Solution ?????

Firing the CEO solves nothing – you have to replace whole board and whole management and whole company culture created by those people.

We can see that Airbus works differently.

Bombardier with technically good results – the business ones not too good – still they produced modern very nice plane at cost for them too high but for Boeing would be unbelievably small.

The overall long time pressure on MONEY only without looking right or left brought the inevitable results.

They probably dismantled them and reused valuable components … recovering some % of the costs ??

Just imagine the kind of plane they could have developed with that money, plus all those people would be alive today..how sad. Short term penny pinching is VERY expensive. The 2 MAX crashes exhibit the exact same flawed decision making with the DC10 cargo doors.

This is really a consequence of dealing with Boeing. I don’t see a great deal of culpability with Collins but you can see the issues a supplier faces

https://www.nytimes.com/2019/11/07/business/boeing-737-max-collins.html

Mostly I see you try to squeeze top notch products out of a company that is now low ball you get bad results.

I know of two companies that use Indian Software writers. In both cases it had to be redone once it was provided.

Software writers do not know equipment. So they write to spec but you have to know and understand what the equipment does and works let alone how sub sets of it work (often same end results but different mechanics to get there)

The best software writers for HVAC equp0iment was a former HVAC tech. The rest we had to train and tell them what was needed.

Its not Indian Software writers, they may be good or bad, any outsources software writer is ignorant unless they are former industry people (whichever industry it is). And it still takes a close coordination between a the in the field and the software guy to get it working right.

It took two of us three years to correct the messed up software on one critical building . That just scrubbed the worst of it.

There are still issues (which will bite them when they occurr)

And now we see what I was looking at. The software upgrade in question and not coming as fast as promised. More delay possible.

https://www.chicagobusiness.com/manufacturing/audit-could-delay-737-max-return

First its a major job to change what they moved to do (better to have stuck with the singles and made the dual talk a latter upgrade)

Now, stay tuned.

It seems FAA and EASA are working together and EASA is asking for a certain standard. No excuses. I think it’s good they are working together, protecting FAA from politics.

Great article from 4 years ago!

How did you make the adjustment from operating profit reported under program accounting to that from unit accounting? (2nd graph)