Leeham News and Analysis

There's more to real news than a news release.

Pontifications: As customers wait for 787s, some rethink 777-300ERs

Nov. 8, 2021, © Leeham News: Boeing now has passed one year since deliveries were suspended for the 787. There were 105 787s in inventory at Sept. 30. The current build rate is 2/mo.

By Scott Hamilton

LNA identified 93 787s that were ordered in 2020 and 2021 that are believed to be parked, leaving 12 unaccounted for.

Among the aircraft in inventory are:

- 11 787-8s destined for American Airlines, which are owned by Boeing Capital Corp.

- 3 for BOC Aviation, which do not have identified customers.

- 9 for Chinese airlines.

- 8 for the always cranky Qatar Airways.

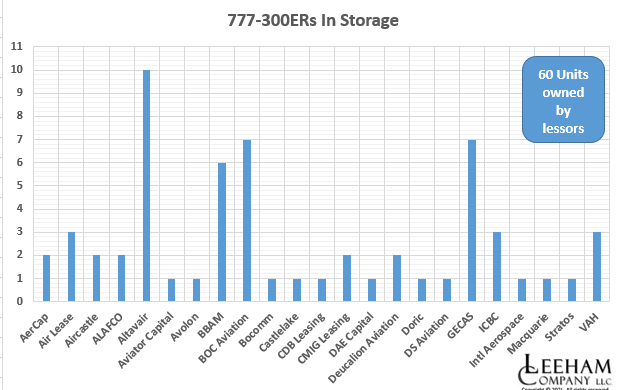

LNA understands that several customers are now looking for substitutions in the Boeing 777-300ER fleet owned by lessors. Of the 116 -300ERs in storage, 60 are owned by lessors. Nearly all are leased to airlines that put the aircraft in storage. But there are some off-lease. The latter includes seven owned by GECAS (now AerCap), which are destined for conversion to freighters via IAI Bedek.

No date to resume deliveries

There is no date forecast when deliveries of the 787 will resume. Boeing too many times suggested dates when the 737 MAX would be recertified, only to be wrong each time. Officials had their hands publicly slapped by the Federal Aviation Administration in the process. No one at Boeing is willing to suggest a date for the 787.

But customers express concern that a resumption of deliveries may not begin until well into the first quarter next year.

There currently are 16 787s scheduled for delivery January-March, according to data seen by LNA. This may be high, if based on a production rate. It’s not possible to conclude how many of these may be rescheduled from earlier periods.

American, Etihad Airways, Korean Air, Vietnam Airlines, and British Airways are slated to receive two aircraft. China Southern Airlines is scheduled to receive one, but deliveries to China are stalled due to the long-running US-China trade war.

LNA is told that in the post-COVID world, airlines are looking at the 2022 deliveries and new traffic patterns that are influenced by belly freight demands. These factors prompt the airlines to take a second look at whether to retire, return to service or find additional 777-300ER lift.

Some carriers have inquired about long-term leases, rejecting Boeing’s suggestion that six-month interim leases are all that’s needed.

The airlines and lessors affected by the suspended deliveries may cancel orders, typically after a delay of this nature of between 9-12 months. The cancellations would be on a rolling basis.

Lease rates and other factors

Although 787s are considerably more fuel-efficient than the 777 Classic, the latter’s lease rates are significantly lower and the revenue potential from the belly capacity is much greater.

Another factor operators and owners must consider is the maintenance, repair, and overhaul (MRO) status of the 777-300ERs. Engine MROs are very expensive. The GE90 costs more than $12m for a complete overhaul.

“GE is very conflicted because 777-300ER viability depends on engine costs,” one 777 owner tells LNA. “So, does GE address that and win more services business or do they stay firm on engine servicing pricing to try and drive new sales of GEnx engines” used on 787s?

Germany’s MTU, a supplier to GE that also has its own MRO business model, is making a strong push in the GE90 market. It is becoming a viable alternative to GE.

Reducing the feedstock

The renewed interest in retaining the 777-300ER in passenger service may reduce the feedstock for aftermarket P2F conversions. Of the 116 -300ERs in storage, 51 are 12 years or older, making these prime candidates for P2F freighters. Twenty-nine of these are owned by lessors but seven of these are the GECAS planes destined for IAI Bedek. Only four are off-lease. Not all of the remaining leased aircraft will return to service, however. The remaining 22 are owned by airlines that parked them.

Airlines have to be careful they don’t end up playing the inventory game like car companies did with computer chips ( or many other industries with various products) .

Some might find that Boeing looks after the airlines that looked after Boeing

Duke:

Boeing has to meet its contractual obligation and even Boeing Management will not diss a good future customer for revenge sake. They understand its business.

You see the slip side with Air Asia demanding the A321F. They are totally flaky customer, they shift orders like a roulette wheel spinning. Airbus is having a great laugh.

It seems to me is that for planes that were scheduled for delivery this past year may have been ordered some 4-5 yrs back at higher prices ( depending on volume discounts too)

Some buyers just want to renegotiate the price now that the cancel option is theres to exercise, and likey re-order for immediate delivery the same plane for cheaper price. Not all of course.

But when it comes to deferring a delivery for say next year that is on time, Boeing may demurr if their consent is required.

Boeing sales people may be ever accommodating but the finance people wont be so kind and seek to ‘make examples’ to deter others. When its a boom market eccentricities are tolerated

What? Wat da you saying??

Air Lease Corp. has been pretty vocal about the endless delay of 787 since Feb. AW reported it has 34 787 order with 14 due for delivery in 2021 at the end of last year. 3 were canceled this year due to the delay. A few other lease companies have also canceled some 787 orders.

With the way the pandemic situation is currently rapidly deteriorating in the EU, it probably won’t be long before (international) air travel is again curtailed — ominously, there’s already talk of a reinstatement of (some) lockdown measures in central Europe. Statistically, the trend in the US follows that in Europe by about 6 weeks; where that’s concerned, the re-opening of international travel in the US yesterday was very unfortunately timed.

If/when things go further downhill, don’t be surprised to see (many) more outright cancellations.

Duke:

You are running rife with speculation.

The financial people do not drive the decisions in that case. Boeing like Airbus works it out with the customer.

Boeing may pay if they are at fault (or offer service in lieu of) or the customer may loose money on deposits (not if Boeing is at fault).

Re-opening to vaccinated traveler with a recent negative covid test. I don’t think this will be rolled back.

@jbeeko

Even if your assertion turns out to be true, the situation is nevertheless clouded by many ancillary factors, such as:

(1) Define “vaccinated”. For the coming ski season, Austria will not accept travelers who have only had the single-shot J&J vaccine. It will also not accept travelers with a multiple-shot vaccine if the last shot was administered more than 9 months previously.

(2) Most insurers will not give CoViD-related travel insurance cover if the destination country is on a red list. At the moment, large parts of the EU are already red or deep red, and the orange areas are rapidly following. The color is determined by # CoViD cases per 100,000.

(3) Tourists will be deterred from flying if the facilities at their destination are sub-optimally available: for example, a trip to Europe may not be much fun if museums and theaters are closed or have visitor number limits.

(4) Travelers may also be deterred if the healthcare facilities in their destination are overstretched. For example: yesterday, Ireland had just 78 ICU beds available for the entire country, so it may not currently be an attractive destination for many (older) people.

The current travel mess is a monster with many tentacles.

Boeing, through its massive incompetence has completely let its customers and shareholders down.

Don’t forget to add the flying public to that list.

Mark:

In fact Boeing has lined the shareholders pockets and they are equally to blame for voting in the board that allowed the financial gutting of the company. Stock buy back and dividend and not investment in product.

Marginally legal Pyramids Scheme.

The shareholders that didn’t get out at the top are footing the bill, unlike top management (former and current) who got handsome pay by stock options.

If there’s a (relative) shortage of available 777-300ERs, is there any/much interest in idle A330s as a substitute? Sure, they don’t have the belly cargo capacity of a -300ER, but they’re similar in size to a 787, they’re cheap, and they’re available.

At one time earlier this year, AAL expects to receive 13 787 in 2021 and first quarter next year. That would be quite a hole in its fleet planning?

A quick look at the American Airlines fleet at planespotters (not sure how accurate, but…) shows 5 – 777’s & 3 – 787’s parked.

So I’m guessing that they’re not gagging for them…

Indeed, some airline comments on how delayed deliveries are hurting them are with an eye to court cases. They want to justify compensation of some sort from Boeing and it is hard to do that if you blog that delivery delays are great.

AMR CFO said due to the continued uncertainty in the 787 delivery schedule, they have “proactively” removed these aircraft from our winter schedule and beyond.

That’s a good point – I wonder if airlines will be able to claim compensation from BA or AB on missed deliveries if they have aircraft of the same type parked, doing nothing…

What airlines have Boeing really looked after in the past three years?

I suspect that is a short list and indeed the list of those thrown under the bus is longer.

The saving grace for Boeing has been the pandemic meaning their issues in delivering frames was masked by significantly reduced demand.

On the other hand, the pandemic is concurrently a curse for Boeing, because it has created a (financial) situation whereby many airlines have made thankful use of the possibility to cancel aircraft without penalty.

Since the start of the pandemic, almost 1200 MAXs have been cancelled.

In addition, many 777Xs and 787s can now also be cancelled by customers who wish to adjust their fleet plans to suit their (pandemic-induced) financial situation.

Thats 1200 cancels AND accounting adjustments.

675 were actual cancels mostly lessors and 570 still on order but pre -payments are in arrears or the airline in administration.

Well, there’s a really quick and dirty way to see where Boeing stands, vis a vis; their backlog;

From the financials

https://s2.q4cdn.com/661678649/files/doc_financials/quarterly/2019/q1/1Q19-Earnings-Release.pdf

Q1 2019 – when the Max was just grounded;

Total backlog of $487 billion, including more than 5,600 commercial airplanes

(On a side not for TWA, which I know he’ll love: Operating cash flow of $2.8 billion; paid $1.2 billion of dividends)

https://s2.q4cdn.com/661678649/files/doc_financials/2021/q3/3Q21-Press-Release.pdf

Fast forward to Q3/2021

Commercial Airplanes delivered 85 airplanes during the quarter and backlog included over 4,100 airplanes valued at $290

billion.

That includes all the orders from SWA & Ryanair and everyone else. (plus whatever was delivered in the interim)

Yah, there’s also a small matter of some $60 billion in long term debt, but that’s another matter

I’d like to make a correction here. In the Q1 – 2019 financials, there is this line:

Total backlog of $487 billion, including more than 5,600 commercial airplanes

See the word ‘including’?

The actual value of the commercial backlog is $399 billion, as noted further down in the fine print:

Commercial Airplanes backlog remains healthy with over 5,600 airplanes valued at $399 billion.

That number is more in line with the average revenue per commercial aircraft at ~$71 million, for both sets of financials.

Finally, a quick look at how things look for BA since the grounding.

At the end of Q1-2019, Boeing delivered a total of 149 for the quarter.

By the end of Q4-2019, Boeing delivered a total of 380 for the year.

Backing out the first quarter, gives us a delivery total of 231 for 2019 since the grounding.

2020 Deliveries were 157.

2021 Deliveries were 241 (so far).

629 aircraft delivered since the Max was grounded.

Backlog was 5,600 at the end of Q1-2019.

Current backlog is 4,100. But we haven’t addressed the orders given to BA.

https://www.boeing.com/commercial/#/orders-deliveries

Using the Boeing website for orders and setting the range for the 737 Max and order from 2019 to current, we get 742 new Max orders (just an added bit of info).

Setting the filter to ALL aircraft types, gives us a total of 1,150 new orders, since the grounding in 2019.

Now it’s a simple inventory/COGS calculation:

Opening backlog after Q1/2019: 5,600

Add sales since then: 1,150

Subtract deliveries to customers during the period: (629)

Backlog without cancellations: 6,121

Actual backlog end of Q3/2021: 4,100

Shortfall: ~2,000

Rough figures, but it gives us a ballpark number as to how much the grounding/covid has cost BA.

-> What airlines have Boeing really looked after in the past three years?

Good question. Those totally devoid of reality couldn’t give a straight answer.

It guess airlines needing to fill capacity because of late 787 deliveries, first would look at types they already operate, extending leases, bringing back stored aircraft. And reshuffle across their networks. Those could be 767, 777s, A330s..

AA retired A330 and 757 fleets last year.

Engine MROs are very expensive. The GE90 costs more than $12m for a complete overhaul.

Is that a per engine rate?

Per engine.

Wow. Follow up question then;

Let’s say you put a new 777 on a tatl route – call it JFK-LHR/CDG. You fly that aircraft there and back, every day and keep it in your fleet for 20 years.

If no unforeseen events occur, how many $12 million overhauls will it need, during that 20 year period?

Thanks

@Frank: I don’t have that answer.

Frank:

My guess is one and that would be at the end.

Its a bit more complicated in that if it gets parked, then sold, you have the issue do you overhaul now before its TOW is gone or do you wait and have an interruption of use a bit down the road.

There is wear matrix of time in cruise, take off and landing cycles that play into it, not just running time.

Frank:

Bjorn has an average of 20,000 hours for a Widbody engine on wing before overhaul.

Using 10 hours a day utilization (Atlantic flight 7 x 365) that is 5.5 years.

A lot of assumptions built into that. Its going to miss trips for various reasons and a weekend schedule might not be on the table.

A 777 flying a daily LA to Sydney route would use a lot more hours of the 20,000 daily. I think that is a 20 hour trip.

77W is an overkill for most Atlantic routes, isn’t it?

Nope, carries lots of Pax and freight and economical doing so. Used to be 747s on that route.

JAL and ANA run version inter island (or used to)

IIRC those are 773 in high density layout, day and night with 77W for long-haul.

Just to make it clear, I was referring to the Japanese 773 for domestic flights between hubs.

@TW

So rough estimate – given a 5-6 year overhaul schedule and keeping it for some 20 years, it’ll cost you $72 million for 3 overhauls.

Not cheap.

This document gives some ballpark figures from 2014. It estimates that the first run of a GE90‐115B will be about 2500hrs on the wing followed by a $5M shop visit.

Subsequent runs will be about 2000hrs on the wing and be followed by a $6M shop visit.

Those estimates are based on 8hr missions.

http://www.aircraftmonitor.com/uploads/1/5/9/9/15993320/engine_mx_concepts.pdf

So doing daily 8hr flights for 20 years will mean about 29 shop visits or about $175M/engine at 2014 prices. This also assumes that there are no hours where some parts become time limited and the visits cost even more.

jbeeko:

Good listing but?

There is something wrong with how they show the comparative ref that makes no sense. They say 25,000 hours for a GE90 and then the CFM has far more on wing time?

Not sure I can sleuth it out but a CFM would have a lot more cycles and less on wing time before work was needed.

GE90 would have a lot of easier on engine in cruise time per takeoff cycle.

Think you mean cycles. 2000cycles might be right if you don’t push it too much, but if every T-O is at MTO thust in a hot and sandy environment it comes down (Emirates)

Think you see a heavy shop visit each 16000hr on this high thrust engine. It is really cycle dependent so if you can fly LHR-SYD non stop you more or less half the engine maintenence cost. You carry lots of fuel so the cruise TSFC is extremely important. We will see when Qantas takes the A350-1000XLR’s if RR can let the customer enjoy this or if they take 97% of the savings themselves by forcing power by the flight hour rats onto Qantas. It gets really interesting when BA meets RR and want a better deal for its A350-1000XLR’s…

RR cannot force Qatar into anything. Worst case Qatar dumps Airbus for the more flexible GE powered aircraft.

claes/Frank, TW/jbeeko – “It is really cycle dependent…” That surely is the point, I think; as with flight-safety data, the most important parameter is the number of flights (and for maintenance considerations take-offs at full power), not the time in the air.

Cited TATL utilization above assumes single one-way daily flights, but IIRC back in the late 1970s/early 80s Braniff operated a 747-127 (N601BN, msn 20207, line number 100) as flight BN600 on daily round-trips between DFW and LGW, which equated to 19FH (but only 2FC) per day; indeed, a quick google tells me it clocked 30,500+FH in just six years at BN and flew for 21 years before being stored, then broken up at JFK in 1994.

Compared with 747s that enjoyed greater longevity, this aircraft might have logged relatively modest FCs but likely sported an impressive ratio (for its day, at least) of FH:FC.

Pundit:

Its a balance. For a CFM the cycles overcomes the hours and you need an overhaul sooner.

For a long range wide body, its the hours that wears the engine out.

Take off and landing cycles are much harder wear factor than flight hours but the flight hours catch up.

@TW. For a widebody engine normally the hot section is not designed for more than 2500-3000 full T-O cycles as with 1.x flights/day gives around 7 years of service before its hot section is worn out. You can extend it a bit by doing regular compressor washes and good maintenance. A narrowbody engine is designed to do 15000-20000 cycles before the hot section is worn out, but it does 7.5-12 cycles/day. Hence if you fly less cycles/day you can enjoy a very long life on wing as expected on the A321XLR doing 4-6 cycles/day if working day and night having a chance to be enormously profitable for the airline and the leasing company.

It’s called the razor and blades business model.

Such connundrums may be the least of Boeing’s problems. As if closing borders didn’t damage airlines enough the Body Politic is now seeking $150bbl oil to expedite their “green agenda”.

In this new age of secular inflation it will be impossible to contain pricing on oil if it even approaches this level, it will merely increase the momentum. We all remember what a disaster for the industry $150bbl oil was in 2008 before the GFC put the brakes on ( ah – such innocent, care free times) what price $200bbl or $300bbl oil?

While I think expensive oil caused in substantial part by a carbon fee and rebate system would be great for reducing CO2 emissions that is not likely anytime soon except maybe in the EU.

Oil at $100/bbl will quickly bring locked in production back on line. I doubt the world will see oil over $100 for a sustained period for years or maybe decades.

I wonder how much of it is related to gas (NG) shortage and high price. Thermal plants are switching to burn oil (or coal to a lesser extent) if possible.

https://www.reuters.com/business/energy/european-gas-price-surge-prompts-switch-coal-2021-10-12/

https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/081021-high-natural-gas-prices-lead-to-increased-coal-generation-2021-carbon-emissions-eia

https://www.cnbc.com/2021/10/13/coal-is-king-as-gas-prices-soar-total-ceo-says-and-its-backfiring-on-cleaner-energy-goals.html

…one of the purposes of COP is to legislate against that very possibility.

Talking to an oil worker informed me that part of the oil industry was damaged by the success of shale oil fracking. A lot of the highly skilled oil workers have left the industry. Fracking creates a lot of oil flow but is unlikely to last. So oil may not come back that fast. The synthetic electro fuels are likely to cost equivalent around $400 barrel though might get to $280 for a refined product.

Oil at $150 barrel will be devastating to mining, metals will skyrocket, it will damage farming, air, sea and truck transport. Inputs will skyrocket,

Mining is about moving huge quantities of dirt, crushing it finely so that flocculants and reagents can concentrate the ore. It’s all done by diesel.

Greenies haven’t reflected upon any of that: for them, the concrete and steel for their wind turbines, the plastics for their solar panels, and the copper for up-gauged electrical networks…are all just conjured into place using a magic wand 😏

@ Scott / LNA staff

FYI: With respect to the above (paywall) article on the A321F and Air Asia, the following article has now surfaced — not sure to what extent you’re aware of it:

“Potential A321neo freighter may not be part of AirAsia’s cargo plan – logistics exec”

“In an interview with Reuters, Pete Chareonwongsak backed away from comments he made last week that Teleport would look to convert a “meaningful chunk” of AirAsia’s orders for 362 A321neo passenger planes to a potential newly built freighter model of the A321neo.

“All I was saying was, if (Teleport is) successful, we’re talking about large orders in magnitude of freighters,” Chareonwongsak said. “Obviously, AirAsia gives us a huge advantage, but that doesn’t automatically mean that we can or we’re able to source freighters from AirAsia.”

…

“Chareonwongsak said Teleport had been involved in AirAsia and Airbus’ discussions about the feasibility of a dedicated A321neo freighter model.

He said Teleport aims to scale up its freight business to a size that AirAsia would consider it for operating part of its fleet for freight. Teleport could also source freighters from other airlines or cargo operators, he added.”

https://www.investing.com/news/stock-market-news/potential-a321neo-freighter-may-not-be-part-of-airasias-cargo-plan–logistics-exec-2671093

Makes little sense to offer new-built A321F IMO.

I believe the A321BCF would be a killer that has a higher capacity than a B737-800BCF.

I’m inclined to agree…but perhaps the potential customers for an A321F are interested in the greater range offered by the neo. Moroever, with an eye to the future, one must remember the new ICAO emissions standards starting in 2028.

Or the higher MTOW of any customer built freighter.

I could swear BCF stood for “Boeing Converted Freighter”

what do you think it means?

I could swear he made a (caffeine-deficit) typo, and meant P2F 😏

@Bryce

Yup. Thanks Bryce.

It’s hard not to feel sorry for Air Asia. Tony Fernandez came up with a brilliant structure to give Asia a quality LCC. I think 40% of the worlds population and 60% of its growth is here. Asia needs aviation to move its people and freight around their mountainous island nations.

I suspect Air Asia has temporarily wound its projections for passenger traffic back due to COVID but increased its expectations for freight: hence the attempt to convert A321neo orders to A321F.

The A321F looks like it would have the right “gauge” and range. I suspect based on A321LR to get the MZFW up, A321XLR or hybrid (A321XLR sans RCT)

…also, The Baltic Dry Index, the key barometer of global freight activity which is a close as a proxy for airline freight rates as there is has fallen precipitously in the last few weeks implying that stupidly high freight rates have spiked and with it the rational for PAX airliner as freighter model. OK, so an airliner is no bulk carrier but still.

Its still valid as the freight issue for Aircraft is lack of Pax wide body runs.

If the Pax flow picks up, there is more freight capacity and the conversions begin to fall off as to making any sense.

You want to lead the Gold Rush, not be the last guy in the field.

Mammoth is a case in point that I believe is going to totally fail.

Existing converters will have a market, its not going to be spectacular but it never has been. If you are not rolling now you will fail.

There is a regional trend in the US with On line ordering, but that is not the heavy fright area.

Fastship:

Oddly One of my benchmarks for future growth or drop is the hydraulics industry. Well not mine as much as a magazine I get.

Its remarkably accurate on predicting the business cycle 3 to 6 months down the road.

The pumps and motors are a long lead item for all machinery and when a mfg sees things slowing down they throttle back.

Fastship – Are you looking at this, or something else: https://public.tableau.com/app/profile/damian3851/viz/TACIndexmonthlyairfreightrates/Dashboard1 ? Have you an alternate link, please?

No. The Dry Index is the more liquid market and generally acknowledged as the lead indicator for macro economiists.

The link given by Pundit clearly indicates air freight.

Are we talking about air freight or are we talking gibberish?

As I said, I was talking the Dry Bulk Index. Air freight is a tiny fraction of the global freight market and is a lagging indicator of economic activity.

The Baltic Dry Index reflects supply & demand for the shipment of the raw, bulk commodities that make their way through the value chain to eventually become the manufactured items some of which (a tiny amount) in the fullness of time becomes air freight.

Imagine a Capesize ULOC vessel carrying 400,000 tonnes of bauxite from Australia destined, after a two month passage for an aluminium mill in Louisiana whose energy bill is now six times what it was a year ago when it bought the bauxite and has a customer (ironically) needing aluminium lithium plate to sell to an aerospace customer who has an order for air-freighters for delivery in two years time and that carriers customers, say a cell-phone maker in China who sees demand falling away at the very time his input costs are rising steeply. Well, you get the picture of why the Dry Bulk Index is the leading indicator and the Air Freight Index a lagging indicator.

The aerospace industry is notorious for never getting in synch with the macro economy.

Fastship – “…The Dry Index is the more liquid market…” Ha, funny, that!

Interesting that’s there’s now no estimated date for 787 deliveries to resume.

Curiouser and curiouser..

It may be that Boeing has learned to shut up and get the approval from the FAA first.

The first effort by Boeing was to use a set of random sampling that the FAA did not like. It may well be that random sampling is ok, but has to be broader and over all air-frames.

Or it could be not allowed at all and each shim has to be confirmed.

In theory, if you measure the gap at .010, you put in a .008 shim, you are good and don’t need to re-check (said gap can’t be more than .005).

Boeing got a slap from the FAA on the 777X as well when they rejected what Boeing was proposing (and there are still no official FAA flight tests being done). In that case the FAA flat said Boeing was not being responsive in answering the question and giving out the details.

Boeing to away with it for so long that is part of the culture and that is hard to break once it sets in.

So stay tuned on the 787. It is truly mind boggling it is not being delivered but there we are.

I guess anyone objective would be mystified when the airframer handpicked a couple produced in relatively close succession to one another as representative samples.

It takes some serious match to sort out random sampling for quality control. I am not remotely in that area.

Boeing may have believed the proposal was valid vs a get away with. The FAA disagreed.

I had a match major roommate in collage. Phew, the weird arguments he got into with his fellow match majors.

In the end the FAA wins the argument (if they are doing their job). Boeing could have valid reasons for their stand (no disagreement that being suspicious is the first thought)

I am not sure why they can’t do full inspections for shim fit on aircraft until they sort it out.

Hate to see a good aircraft just sitting there.

-> Hate to see a good aircraft just sitting there.

Wait til you see all the skeletons in the closet.

It is strange that large space rocket composite structures can be made at very fine tolerances and Boeing getting stuck now at Line number approx 1000. How will those close to 1000 aircrafts in service be inspected and fixed? Will FAA set a hard life on the structure?

Claes:

I would ask two questions.

What are the tolerances on a rocket?

Are those items machined?

I know Diesel Fuel injectors are machined down to .00010

I built a lot of houses and close was good enough even with 3 stories. You were lucky to get 1/4 inch fit and I saw some 2 and 3 inch problems (we did not cause them).

Wood is impossible to build to the tolerances you can make an injection system component.

I find it stunning a spun fuselage can get built down to or needs .005.

Dominic Gates:

FAA complains Boeing is appointing people lacking expertise to oversee airplane certification

https://mobile.twitter.com/dominicgates/status/1458590827056275461

The future is Bright? No.

EXCLUSIVE Boeing U.S. worker vaccine exemption requests top 11,000 -sources

https://mobile.twitter.com/byEricMJohnson/status/1457836935787933699

Here’s more on that topic:

https://www.bnnbloomberg.ca/boeing-vaccine-backlash-builds-as-11-000-workers-seek-exemption-1.1679011

Pedro:

250,000 people are killed by hospitals in the US each year, what has that got to do with 787 and aircraft production?

What has carpentry or housebuilding got to do with 787 and aircraft production?

@TW

I sometimes have difficulty to see how one can’t connect the dots.

How many staff BA willing to let go? Production ramp up as planned??

UAL, the BA/LM JV, expects in a worst-case scenario to lose 15% of its workforce, so far 1% of its workforce had permanently left the company.

sqɐɾ ɥʇoq pɐɥ ǝʌ,I puɐ ǝuᴉɟ ʎlǝʇnlosqɐ lǝǝɟ I

Boeing October deliveries have fallen to a “trickle” (term used by Dominic Gates in the Seattle Times):

“Among Boeing’s 27 deliveries last month were 18 737 Maxes, one 747 freighter, one 767 freighter and two 777 freighter”.

18 MAXs is underwhelming, in view of the huge inventory.

Net orders: just 7.

https://www.cnbc.com/2021/11/09/boeing-delivered-27-planes-in-october-airlines-still-waiting-on-new-dreamliners.html

***********

Mind you, Airbus October deliveries were also not stellar, with just 36 units delivered.

“2 A220-300, 1 A319neo, 17 A320neo, 2 A321ceo, 12 A321neo, 1 A350-900, 1 A380”

Orders: 22 (not sure if this is net or gross).

https://www.aviation24.be/manufacturers/airbus/airbus-registered-22-orders-and-delivered-36-aircraft-in-october-2021/

GE breaks up into three companies

-> “Given the extremely heavy legacy GE influence among Boeing’s top ranks, one has to wonder if this is a preview of the airplane maker’s future state.”

https://mobile.twitter.com/jonostrower/status/1458105988075032576

Their major divisions are unrelated to each other . They sold the rail locomotive division a few years back

Its now down to these plus a few others

Healthcare

Energy

Aviation engines

Boeing isnt a conglomerate like GE is , as its aviation focused and related businesses in defence and plane services

Easy peasy:

– BCA;

– Boeing Defense;

– Boeing Space.

Do you really think there’s currently any synergy between those 3 divisions?

No boss wants to be Boss of a smaller company…

Golden handshakes can take care of that 😒

Boom time? Boeing has the upper hand in bargaining??

-> “In the medium term Boeing still faces all the lasting damage issues of a serious and potentially permanent loss of market share, challenged or uncompetitive main commercial programs, and a heavy burden of debt.”

https://mobile.twitter.com/dominicgates/status/1458105121506676739

-> “The continued delivery drought leaves Boeing in a precarious position,” according to a London-based analyst Nick Cunningham.

“The 18 MAXs delivered are far less than the level needed to stanch the co.’s cash bleed”

Previous projection from the co. to deliver over half of its inventory of MAXs and 787s didn’t happen with most deliveries pushed out to 2022 and 2023, along with the revenue they bring.

Paying off the co.’s massive debt (over $62 billion as Q3) “will make it hard for Boeing to make the necessary investments to improve its competitiveness.”

What “investments to improve its competitivness”?

– The 777XF that won’t be launched in Dubai?

– The NMA/NSA/NBP litany?

– Episode 2 of the KC46 cabaret?

– The 007-esque Black Diamond project?

…

Boeing restored a net total of 17 MAXs to its firm order book, likely after renegotiation with concessions to the customers.

Edit

-> … likely after renegotiation with concessions to the customers according to the Seattle Times.

-> It may look like a single line, but it’s actually the track of two aircraft. Airbus has just completed its first transatlantic #Fellofly with two A350s between Toulouse and Montreal.

https://mobile.twitter.com/flightradar24/status/1458109197313314817

-> These two #A350 “fellos” performed the 1st transatlantic flight as paired aircraft from Toulouse to Montreal airport! What’s #fellofly? A follower retrieves wake energy lost by a leader, reducing engine thrust & fuel consumption of over 5% per trip.

https://mobile.twitter.com/Airbus/status/1458100108143300619

Well, all those parked 787s are lined up nose-to-tail…is that something similar? 😄

It says 6 tons of CO2 saved on one short flight.

How come those flights across the Atlantic never seem short to me?

SQ 23/SQ 24 19/18 hr

That is something I can really do without. If I’m needed in Singapore, I’d probably do something like:

Fly to west coast – visit a couple of days

West coast to Hawaii – grab some sun for a couple of days

Hawaii to Japan – eat some sushi and bullet train around for a few days

Japan to Philippines – go dive for a few days

Philippines to Singapore – OK, I’m here.

It’s really cool to fly the polar route and all, but you have to be young to take that flight. I can’t imagine how tough it must be in economy.

@Frank

Why not save yourself a lot of time and expense and just take 2x comfortable A380s via The Gulf?

Many polled business travelers have said that they prefer that option to a direct flight in a smaller aircraft — even if the latter does have the iconic service of SIA.

@bryce

That’s still 12 hours for the first leg. Fly to the UK first, go see Man U play…

SCOOP

Boeing & lawyers for the families of victims of the MAX crash in Ethiopia are set to announce a deal that will effectively end almost all the civil suits + limit the scope of Boeing’s damages and further investigation into the causes of the accident

https://mobile.twitter.com/dominicgates/status/1458253024514621444

Buying off further investigations. Victim families need to go on with their lives, so will settle.

Justice? Boeing will add half a billion to their 60B debt. Executives off the hook.

Congratulations. Justice is done.

Keesje — Quite.

Compensation for this deal comes from insurance co. (Punitive damage would come from the co.)

-> Any trial in this matter between Boeing and any Plaintiff that is party to the Stipulation shall be limited to the issue of compensatory damages.

The Parties to this Stipulation shall take no further discovery on the issue of liability stemming from the ET302 accident

-> Boeing agrees to be solely liable for the deaths in the ET302 accident

“All claims against defendants Rosemount Aerospace (maker of the Angle of Attack sensor) and Rockwell Collins (supplier of the MCAS software) are hereby dismissed with prejudice and without costs”

“The defendant, Boeing, has admitted that it produced an airplane that had an unsafe condition that was a proximate cause of Plaintiff’s compensatory damages caused by the Ethiopian Airlines Flight 302 accident.”

-> “The jury *shall not hear evidence on issues of liability.*

The parties further agree that *no evidence or argument about punitive damages will properly be the subject of discovery or be admitted*.”

-> “The Stipulation has been entered into between Defendants and all Plaintiffs except for two Plaintiffs who have abstained.”

-> This is the closest yet to a full admission of blame for the MAX crashes

* Boeing accepts sole liability

* The pilots and 2 suppliers specifically exonerated

*Still short of telling us exactly what went wrong in the MAX design and certification

Link to the Seattle Times article

https://t.co/0iOkoxzRHy?amp=1

https://mobile.twitter.com/dominicgates/status/1458502649846714369

-> With the possibility of further revelations of wrongdoing in court proceedings now remote, Boeing’s leadership can leave it to the lawyers to work out the precise compensation amounts while they move on.

-> Ralph Nader:

“A strange settlement without Boeing having to guarantee any dollars whatsoever.”

“The great American tort law system, assuring individual justice against wrongdoers, has been reduced to a collective slap on Boeing’s wing”

https://mobile.twitter.com/dominicgates/status/1458542411848712193

Fastship — some readers, like this bear of little brain, might be confused by your obviously very well informed knowledge of all things air cargo (if such is not too-o-o far OTT).

You say that “[a]ir freight … a tiny fraction of the global freight market … is a lagging indicator of economic activity” and that “[t]he aerospace industry is notorious for never getting in synch with the macro economy,” while at the same time opining: “The Baltic Dry Index … is [as] close … a proxy for airline freight rates as there is…”

Rate trends in this “tiny [market] fraction” reflect, of course, supply of and demand for capacity in the air-freight sector — albeit (you say) lagging other indicators. Are you able to suggest, please, by what calendar margin, based on these superior global freight-market trends, air-cargo rate movements may be anticipated and how aerospace might best profit from the knowledge?

Fastship – CORRECTION: my previous first sentence should read: “…knowledge of all things cargo…”.

Dominic Gates:

FAA complains Boeing is appointing people lacking expertise to oversee airplane certification

https://mobile.twitter.com/dominicgates/status/1458590827056275461

Wings clipped??

UPDATE

The FAA this summer found Boeing-appointed engineers who oversee airplane certification work on behalf of the agency “are not meeting FAA expectations.”

By year end, new rules will take effect requiring the FAA to approve or reject every appointee.

During the pandemic downturn, Boeing offered early retirement to many senior FAA-authorized safety engineers. In one specialty more than 20 such Boeing engineers left in a single month.

“I go to meetings now and don’t know the names. Brain drain!”

With regard to the Boeing “settlement” of the Ethopian crash lawsuit, it should be noted that the company has only avoided *punitive* damages — mediation or a jury will decide the amount of *compensation* awarded to the plaintffs, which may yet be huge.

It should also be noted that not all plaintiffs agreed to the “settlement” — two families didn’t sign up to it.

Also noteworthy: “Boeing explicitly agreed that the pilots were not at fault” — a big shock for the denialists who regularly tried to pin this on the flight crew.

https://www.theolympian.com/news/business/article255715616.html

If it takes years, the human reality is, the victim families need to get on with their lives. Children have to study, mortgages be paid etc. parents supported, so they have little options than to settle. Company lawyers know.